English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

Permalink

1. Introduction

The industrial sector is the main engine of economic growth in countries around the world, driving the development of key macroeconomic variables such as gross domestic product (GDP), employment, poverty reduction, increased competitiveness, and productivity in emerging countries[1-4] , there is a relationship between economic indicators and financial performance [5].

Corporate financial performance can be defined as the overall corporate valuation of the main financial statements, balance sheet, the cash flow and the income [6]. In addition, capital structure influences a company's financial performance and results [7] is a key indicator, such as return on investment (ROI), sales growth, and earnings per share (EPS) [8].

Measuring company performance is of vital importance for companies; those that perform well are more likely to improve their long-term development, positively contributing to macroeconomic variables and society [9].

However, currently, in the scientific literature, there is ambiguity in financial performance and business crisis metrics, making it impossible to classify companies as “good “or “bad” [10].

The importance of the quality of financial information has an impact on the efficiency of the economic benefits of companies in the industrial sector, allowing the accurate evaluation of financial performance for decision making [11].

During the COVID-19 pandemic, financial and operating performance in industrial sector companies was affected. [12-14], due to stagnant production, restrictions, border closures, global conflicts, and uncertainty in the manufacturing sector, in addition to rising interest rates, inflation, and political uncertainty [15], profitability is the most affected sector due to the pandemic [16], generating distrust in the industrial sector [17].

On the other hand, in the global context of OCDE member countries analyzing labor productivity according to GDP per hour worked, the color scale shows green as the highest production per hour and red as the lowest, with the Nordic countries as the most productive, including Ireland with a value of 132 dollars per hour. However, Colombia ranked last in this category at 14.3 USD/Hour (Fig. 1).

At a regional level, according to the monthly manufacturing survey with a territorial approach conducted by DANE, the following are the most relevant data for the region [19], taking as cut-off June 2023-2024, analyzing the fundamental variables of the manufacturing sector such as production, sales, and employment in Fig. 2, it can be seen how only 4 departments represented in the green bar of the 15 studied achieved positive variations in real production, analyzing the department of Santander recorded a negative 6.9% in this variable.

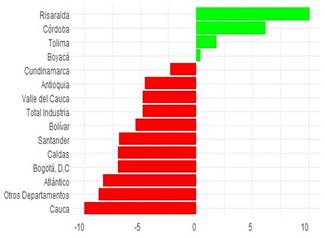

Source: DANE [19]

Figure 2 Variation in Real Production in the manufacturing sector Colombia June2023; Jun.

The same behavior was seen in the variation of real revenues; only 26% of the total number of departments managed to increase their revenues; revenues the sector in the Santander department decreased by 8.3% (Fig. 3).

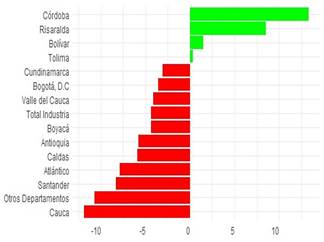

Source: DANE [19]

Figure 3 Variation in Real Revenues in the manufacturing sector Colombia June2023; Jun.

Finally, in the employment variable, only three departments managed to increase this indicator; in the case of Santander, there was stagnation in the generation of new employment, with no positive or negative changes (Fig. 4).

In light of the above, the following research question is posed.

How can Santander’s manufacturing sector design a financial performance index to measure performance and project execution capacity?

Considering the previous context, for Shumpeter, in the concept of economic development, entrepreneurs play a relevant role in countries’ financial growth by including innovations and originality in products, markets, and methods, and the economy advances [20], [21]. Ansoff and E. J. McDonnell [22] stated that as a corporate strategy, business planning and the way it evaluates present and future corporate performance through the design of budgets is fundamental, where performance increases when planning is directed toward flexible and innovative environments [23]. On the other hand, competitiveness has been a fundamental factor of research since 1970 in different dimensions, nations, regions, sectors, companies and products. [24]. Porter’s five forces model is an important reference in strategic management, where the integration of the model influences the profitability of the industry [25]. Resource-based theory studies how the company's multiple tangible or intangible resource bundles affect corporate performance, developing strengths or capabilities that allow a differentiating approach with the competition, optimizing resources, achieving superior performance and reaching sustainable competitive advantages [26]. It is important to incorporate corporate governance for the efficient management of resources to be competitive in the long term [27,28]. Competitive advantage is achieved through the resources of the companies or through cooperation between them [29].

2. Methodology

2.1. Data description

To perform the analysis of this research, information from the Compite360 platform, which offers information on the business dynamics of the Santander department in Colombia. This information contained 2392 records of companies in the manufacturing sector that presented information on their financial statements as of December 31, 2023. The variables involved in the analysis were the values reported for assets, liabilities, equity, sales, net profit, debt level, return on equity, return on assets, net margin, and debt-equity ratio. From the variables, the composite indicator called FPIMS was calculated as a financial measure that accounts for the performance and capacity to execute projects in manufacturing companies in the Santander department in Colombia. Correlations between the results obtained from the FPIMS and the origin variables were estimated. Subsequently, the manufacturing companies were classified according to their high, medium, and low performance according to the values recorded by their FPIMS.

The methodological approach adopted in this study for the design of the FPIMS is the multivariate statistical technique of principal component analysis (PCA), for data processing we used the r Studio programming language with the R commander extension and the factor miner plugins.

The suitability of the sample for the application of the PCA technique is based on the Kaiser-Meyer-Olkin (KMO) and Bartlett tests, where values greater than 0.50 are acceptable for KMO and for Bartlett with a p-value of less than 0.001 [30,31], in addition, for the grouping of the variables, the total variance explained must be greater than 60% [32]. The rationale of this procedure is to allow recombining the base variables into a new group of several combined variables that are unrelated to each other, thus classifying different evaluation indicators and synthesizing the correlation between different parameters, achieving the location and interpretation of relevant data hidden in large data structures [33,34]. Finally, four machine learning models were used to estimate the value of the FPIMS. The models used were linear regression, decision tree, random forest, and gradient boosting.

3. Results

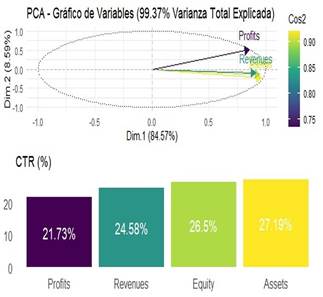

The applied KMO and Bartlett tests showed results of 0.72 and 0.000, being convenient the application of the PCA, the above is in accordance with Çelik & Sürücü. (2024); Dotters-Katz et al. (2024) [35,36]. According to Fig. 5, the total variance explained in dimension 1 by the four variables is 84.57%, which is in accordance with previous studies of Cui et al. (2021) [37]. The same figure also presents the cosine of the variables and the weighting according to the PCA statistical method.

In the first instance, the composite index was calculated from the variables that make up the dataset and was called FPIMS, for which the following equation was used:

A descriptive analysis of the FPIMS values is presented in Table 1.

Table 1 FPIMS descriptive analysis

| Category | FPIMS |

|---|---|

| Mean | 10.095.455.047.224.000 |

| Standard Dev. | 4.554.506.791.535.490 |

| Min | 540.0 |

| 25% | 5940792.0 |

| 50% | 54000000.0 |

| 75% | 328221607.5 |

| Max | 67763276930.0 |

Source: Authors’ elaboration.

Subsequently, a correlation analysis of the variables that make up the data set with the FPIMS was performed, which allowed us to establish that there is a high correlation between the variables Assets, Liabilities, Equity, Sales, and Net income with FPIMS, which suggests that the composite indicator tends to be higher in companies with a larger financial size, which can be considered as a scale of the company size. Likewise, the relationship between FPIMS and Net income reveals that companies with higher profitability have a higher value for the composite indicator (See Fig. 6).

The distribution of companies according to their FPIMS levels was then carried out; however, the high dispersion of the data makes the graph difficult to interpret (See Fig. 7). Considering the above, the data were analyzed without considering outliers. In Fig. 8, a higher concentration of companies is observed at a high level; here, a high dispersion is also observed although the outliers are removed.

To continue the analysis, four machine learning models were used to predict the FPIMS value: linear regression, decision tree, random forest, and gradient boosting. For each model, the current values were compared with the values that the prediction delivered. The results are presented below.

Based on the results of the machine learning model, we can infer that, for the linear regression model, the R2 performance measure presents a value very close to 1, which indicates an almost perfect fit to the data. Despite this, the prediction may be influenced by the FPIMS estimation methodology, which is based on a linear equation.

Considering the linearity of the model, it could be over-adjusted, so it is not advisable to consider this option when making the prediction (See Fig. 9). The results obtained using the decision tree model were R2 = 0.957, which suggests a good fit. However, the RMSE result, another performance measure determined for the models, indicates a significant number of errors in its predictions compared with the other models performed (See Fig. 10).

Considering the performance results of the random forest model (see Fig. 11), it can be observed that it has better measures than the decision tree, with an R2 of 0.976, and that, when considering the average of multiple decision trees compared to the previously mentioned model, it has a lower propensity to overfitting. Finally, the results of the gradient boosting model, presented in Fig. 12, show outstanding performance compared to the others, with an R2 of 0.989 and the lowest RMSE of all, which suggests that it is the most accurate model to estimate FPIMS among the tested models. The R2 and RMSE values of all models are presented in Table 2.

Table 2 Model’s fit measures.

| Model | R2 | RMSE |

|---|---|---|

| Linear Regression | 7.251.443.036.590.290 | 0.99999 |

| Decision Tree | 1.190.025.549.022.340 | 0.95729 |

| Random Forest | 8.959.624.213.932.260 | 0.97579 |

| Gradient Boosting | 5.957.273.702.727.070 | 0.98929 |

Source: Authors’ elaboration.

Considering the results obtained, the FPIMS, in terms of estimated values, performance levels in companies in the department of Santander, its correlation with financial variables, and the possibility of being predicted using machine learning, this index can be the basis for determining the performance and capacity to execute projects in manufacturing companies in the department of Santander from five perspectives. The first factor is related to companies’ financial capacity to develop projects, considering that higher FPIMS may be related to greater liquidity and solvency. The second perspective considers the level of risk in developing projects, taking into account that a low FPIMS may suggest a higher risk if these companies attempt to carry out ambitious projects without the financial capacity to support them. Regarding the third perspective, the FPIMS can support the process of allocating resources to projects, if companies with a high FPIMS can take on larger projects, whereas those with a low FPIMS can focus on projects with less resource demand. The fourth perspective considers FPIMS as a tool that supports companies in building and optimizing project portfolios because it allows for the identification of the most feasible projects based on the company's financial strength. Finally, the fifth perspective offers the possibility that the FPIMS can be considered as an argument for obtaining project financing, taking into account that the PIMS shows the company as financially healthy and with a low probability of default.

4. Discussion

The manufacturing sector is considered a key driver of national growth and economic development [38]. However, the manufacturing sector faces several challenges related to achieving sustainable development, poverty reduction, and economic growth [39].

The analysis of financial indicators has conventionally been used to assess the financial health of companies by contrasting internal financial metrics with those of other companies in the same industry [40]. Financial efficiency is of interest to internal and external stakeholders for strategic decision-making and is fundamental for the sustainability of companies evaluated through financial metrics that allow to analyze the economic behavior of the company [41]. This financial decision-making can be supported by financial forecasting models [42]. Identifying how to mitigate companies’ financial risks and promote innovation is a fundamental factor for the economic development of countries’ economies [43].

The case of emerging economies, such as Colombia, specifically the manufacturing sector of the Santander region. The results obtained confirm that since there is a high correlation between financial accounts assets, equity, sales, and income with the FPIMS index, the scale of financial performance is related to the size of the company. Company size can become a performance challenge for profitable production and financing metrics [44]. Large companies have more robust and modern systems that allow better management of information for decision making, reducing risk and allowing them to access more sources of financing at lower cost, which improves financial performance [45]. On the other hand, small and medium-sized enterprises (SMEs) present various challenges in terms of innovation and sustainability due to the existence of barriers in accessing sources of financing [46]. Currently, the sector under study is facing specific problems related to the increase in fuel prices, the deterioration of the region's roads, the lack of financial inclusion of SMEs and the lack of innovation leading to high costs for entrepreneurs that are extrapolated via price, generating loss of competitiveness in the sector.

In addition, it is important to manage project financial risks as a subset of overall project risk management and as a key variable for project compliance derived from funding and profitability, with financial performance becoming a critical factor in the success of a project [47,48]. It is essential that the project office calculates the financial performance and evaluates the results obtained in all phases of the project to find the optimal financial structure and balance between investment and profits [49]

Having non-conventional metrics to measure the financial performance of projects in the region of Santander, the manufacturing sector will allow to analyze the competitiveness of the sector, carrying relevant information to decision makers in order to mitigate financial risks to adopt strategies to improve the financial performance of companies, leading to the generation of corporate value or that will strengthen the financial sustainability contributing to the improvement of macroeconomic metrics achieving local and regional economic development. Therefore, financial results can be considered as the quantification of the objectives achieved by the companies as presented in financial metrics [50].

5. Conclusion, limitations, and future directions

After developing the research in which the Financial Performance Index (FPIMS) was proposed and analyzed, the four main conclusions are shown below First, the capacity of the FPIMS is to reveal the capacity of organizations to develop projects. In this way, and based on the identified correlations of the index with the variables of assets, liabilities, and net income, it can be stated that it also offers the possibility of estimating the financial strength and size of companies. The second conclusion is related to the machine learning models used for the prediction of the FPIMS (linear regression, decision tree, random forest, and gradient boosting), considering that in general, the performance measures showed a good level of fit. However, the gradient boosting model is the most suitable for monitoring financial performance.

The third conclusion is related to the practical implications of FPIMS because the analysis conducted on the companies allowed them to be classified according to their solidity, which can support strategic decision-making processes, resource allocation, and the creation of project portfolios, considering that companies with a high level of FPIMS may have a greater capacity to develop large projects. Finally, the fourth conclusion is related to the opportunity that the FPIMS offers to contribute to the competitiveness of the manufacturing sector in the Santander region considering that it can offer useful information for reducing financial risks and improving performance, which can be key to the growth of the said sector. It is necessary to consider a number of important limitations of this study: first, this study used cross-sectional data; future studies may use longitudinal data that would allow corroboration of the findings presented. Secondly, the study was based on quantitative methods, which analyze large volumes of data; future research may focus on mixed methods, which include case studies, focus groups, and focus groups to validate the numerical results.