English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

Permalink

Introduction

Article 373, paragraph 1 of the 1991 Political Constitution of Colombia established the Board of Directors of the Banco de la República (hereinafter the Bank) as the monetary, exchange and credit authority, with an explicit and non-delegable function: to maintain the purchasing power of the Colombian currency. In turn, Article 1 of Law 31 of 1992 defines the Bank as a legal entity of public law, a state agency of constitutional rank, with its own legal regime, of its own special nature, with administrative, patrimonial and technical autonomy. Article 2 of this law adds that “the Board of Directors of the Bank shall adopt specific inflation goals, which must always be lower than the last recorded results”; in addition, it shall use the instruments of the policies under its charge and shall make the recommendations that are conducive to the same purpose.

Although what is expressed in Article 373 of the Political Constitution and in Law 31 of 1992 with respect to the mission of the Bank’s Board of Directors seems to be clear, an interesting debate has arisen in Colombia regarding the fact that the Bank, in the search for price stability (inflation control), sets annual inflation targets ranging between 2% and 4% (3% on average as a long-term goal), and it is believed that this constitutional mandate has negatively affected economic growth and, therefore, the generation of employment. In addition, although the Bank is in charge of monetary, exchange and credit policy, this policy is not sufficiently coordinated with the fiscal policy headed by the national executive branch, causing restrictions to the growth of economic activity and, consequently, to employment. It is suggested that the supposed lack of coordination in the management of the comprehensive economic policy by the economic authorities has been directly responsible for the failure to achieve full employment as a social aspiration. In other words, the anti-inflationary monetary policy is blamed for the poor economic performance of the country and the low generation of productive employment, thus reviving an old ideological battle waged between Keynesians and monetarists at the end of the 20th century, which was thought to have been overcome with the issuance of the 1991 Political Constitution.

In overcoming this constitutional discussion, the control of legality exercised by the Constitutional Court of Colombia through the issuance of Ruling C-481/99 has been of utmost importance. The Court sufficiently supported the non-existence of rivalry between monetary and fiscal policies in the legal system. Moreover, the Court insists on the imminent need to coordinate monetary policy instruments with economic policy in general in the development of the social content of the Colombian State. Thus, this article seeks to contribute empirical evidence to the debate on the apparent supremacy of the inflation targeting strategy in Colombia.

A review of the available literature provides valuable theoretical elements to understand the importance of central bank independence and autonomy in the face of the new challenges of increasingly interconnected decentralized economies. The methodological aspects of this research study focus on the construction and analysis of an unemployment sacrifice ratio in terms of inflation control according to the analytical framework of the Phillips curve. The modest results in terms of employment generation and formalization in the country are not attributable to the rivalry of monetary policy with economic policy in general; rather, they are a more complex effect derived from the premature deindustrialization that, together with the rapid boom in trade and services and the asymmetries of the accelerated economic opening in 1990, undermined the capacity of the Colombian economy to generate more and better jobs. The results suggest that in no way the reduction of inflation has meant an increase in unemployment as perceived by heterodoxy, therefore, the inflation targeting scheme implemented in Colombia since 1991 is shown to be successful.

Literature review

The last quarter of the 20th century marked, at a global level, the weakening and discrediting of Keynesian economic ideas and the resurgence of the monetarist conception anchored in supply-side economics. The new model of world economic development rapidly shifted from the economy of demand to the economy of supply. The former was based on expansionary fiscal policy and the role of the money supply as the driving force behind productive expansion. Its essential purpose was full employment of labor. The latter was based on economic growth thanks to the accumulation of productive factors and improvements in their combination (technological change). Thus, the change in the world economic model meant an adjustment in the priorities and instruments of economic policy. Macroeconomic theory and policy shifted their attention and emphasis from short-term effective demand to the determinants of long-term economic growth based on cost reduction, price and wage flexibility and progressive increases in productivity and international business competitiveness.

This change of model also implied substantial changes in the object of economic policy intervention. The recurrent episodes of stagflation in the 1970s in developed economies were both the trigger and the justification for focusing economic policy measures on containing inflation through restrictive monetary policies and the establishment of independent central banks responsible for constantly monitoring the behavior of the national output gap and identifying with certain precision the phase of the economic cycle on which to base the actions of the economic authorities. Granted, monetary policy measures could not be concentrated in the hands of the national executive branch, who would be tempted to abuse monetary issuance to increase public spending and overheat economic performance. This is precisely where the need arises to guarantee price stability under the leadership of an independent, autonomous and technical body capable of understanding the functioning of the economy and of articulating inflation control measures with economic policy in general.

Supply-side economics is based on the thought of Say (2001) and his famous and controversial Say’s Law. For this author, the crisis of overproduction and unemployment that Europe went through in the eighteenth century was not due to a generalized excess in the supply of goods, but to the surplus of goods in some markets, while there was a lack of goods in others. Say added that one could not speak of an excess supply of labor, nor of an under- utilized capacity of the economy. For him, the possibility was that in certain markets there was a shortage of labor or capital while in others there was a surplus (Rodriguez, 2003). Similarly, the new classical school of thought led by Lucas, Jr. (1990) regained vigor and spirit after the waning of Keynesian and post-Keynesian ideas in the early 1970s. According to this globally influential school, national production, and not effective demand, is the essential axis of the economy and, therefore, of contemporary economic policy.

The foundation of the theoretical and empirical edifice of the economics of demand is the economic crises caused by problems of insufficient effective demand, as pointed out by Keynesianism after the Great Depression of 1929. According to this paradigm, short-term economic policy should focus on finding ways to stimulate consumption and private investment and promote exports of goods and services through a competitive exchange rate. Under this logic, the State acquires a leading role as planner, guide and investor through expansionary fiscal policies that, combined harmoniously with monetary policies, will lead to full employment as the supreme goal. The post-war discourse dealt with how to achieve a high rate of production and employment that would not only benefit workers but also employers by expanding their profits (Kalecki, 1943). Although the concept of full employment has a certain theoretical and empirical complexity, it was considered to be the absence of involuntary unemployment (Tobin, 1996), besides being a desire of any progressive capitalist society.

However, the supremacy of supply-side economics implied a new protagonism of central banks with more explicit inflation targeting functions. Colombia could not be on the sidelines of the new world economic architecture. Prior to the issuance of the 1991 Political Constitution, the Bank was in charge of a multiplicity of economic objectives, many of which were difficult to fulfill. The absence of an explicit objective of preserving the purchasing power of the currency as a priority meant that the Bank’s decisions were subject to the political sway of the presidents in office, with serious consequences in the increase of the consumer price index (CPI) due to recurrent monetary issues, large fiscal deficits as a result of the excessive increase in public spending and repeated devaluations to satisfy the interests of powerful exporting groups. All this led to the need to grant the Bank sufficient autonomy to ensure a low and stable inflation rate and to achieve the maximum sustainable level of national output and employment without incurring inflationary pressures.

The political discussion about the independence and autonomy of the central bank in Colombia within the framework of the Constituent Assembly of the early 1990s did not meet with any resistance. In a new political constitution of liberal lineage such as the one under construction, it was more than necessary to implement a target inflation scheme such as the one proposed. Finally, Title XII of the 1991 Political Constitution incorporated the independence of the Bank and, subsequently, a set of legal and institutional arrangements were put in place to make price stability a reality. In fact, the debate between inflation control and full employment arose later within a group of heterodox economists who criticized the inflation targeting scheme as a capitalist competitive deflation strategy. Thus, the Constitutional Court of Colombia, through Ruling C-481/99, clarified that the search for price stability is inextricably linked to the nature, functions and autonomy of the Banco de la República (hereinafter, the Bank). Through this institution with a significant degree of autonomy, the State seeks to preserve the purchasing power of the currency. The Ruling adds that the purpose of the Bank is not exclusively to fight inflation, which is the basic function of the Bank, but also that the Board of Directors cannot be indifferent to other economic objectives, since its decisions must be coordinated with the general economic policy and develop the social content of the Colombian State. It is not surprising that the existence of autonomous and independent central banks in the world is part of democracy (Blinder, 1998; Kalmanovitz, 2000).

The Court has been emphatic in pointing out that there is no distance between monetary and fiscal policy, since the Bank works towards two essential objectives: (a) to achieve and maintain low and stable inflation rates, and (b) to stabilize product growth rate around its sustainable levels in the long term (Urrutia, 2002; Uribe, 2005, 2012). Along the same lines, the Court, by means of Ruling C-485/93, declared the first paragraph of article 15 of Law 31 of 1992, as well as its paragraph, unconstitutional. It established that when the Bank acts as a representative of the State in the different international financial organizations, it must act in coordination with both the general economic policy and the international policy of the Government. “If in all markets there were price flexibility (upward or downward) and people had full access to relevant economic information, no relationship between inflation and unemployment would be expected” (Larraín, 2004, pp. 82-83). Inflation is caused by the monetary expansion that a central bank can bring about by trying to stimulate production. Higher production will lead to the absorption of more workers hired at higher wages (labor costs) that businessmen will pass on to the prices of the goods and services they offer. Since in the long run the larger money supply does not necessarily represent greater production according to the quantity theory of money, the greater demand for goods and services would not be compensated by an increase in economic activity nor in employment, thus generating inflationary pressures on prices.

Although criticisms are part of democratic systems in any country, heterodoxy argues that the basic model underlying neoliberal discourse and practice is based on three types of relationships, namely: (a) unemployment allows the regulation of wage inflation according to the Phillips Curve (lower wage inflation leads to higher unemployment), thus providing the appropriate theoretical and epistemological scaffolding for wage cost reduction; (b) aggregate demand varies in the opposite direction to the interest rate. This means that, in order to contain inflation, it is inevitable to raise interest rates, slowing economic activity as a source of job creation and unemployment reduction; and (c) the Taylor rule, which establishes that when inflation exceeds the target, the central bank raises the interest rate and slows effective demand and, consequently, contracts production and employment.1

In short, the three economic policy measures described here are focused par excellence on price stabilization and the preservation of the corporate rate of return, not on guaranteeing full employment. It should be added that the logic of capitalism requires a quantity of employment that cannot be reduced without adverse effects on economic activity (contraction of output); therefore, in this new epistemological view, inflation is not responsible for regulating unemployment; on the contrary, unemployment is the instrument par excellence used by the banks to contain inflation. This phenomenon has been called ”competitive deflation”, understanding that it is a necessary condition to improve international competitiveness by increasing real wages (Le Gall, 2016). In this epistemological view, the benefits of labor productivity growth are ignored; at least for two reasons: (a) it is the basic source of the improvement in real wages and living standards and, (b) it is the anti- inflationary force in the sense that it counteracts or absorbs the rise in nominal wages (MacConell and Brue, 1997).

Returning to full employment, it represents the maximum point at which aggregate demand (GDP measured through the expenditure method) cannot grow any further, nor can employment. In other words, it is theoretically the level of economic activity at which people who are unemployed, want to work and are looking for work, are able to enter the labor market. Full employment is associated with the natural non-accelerating inflation rate of unemployment (NAIRU). Apparently, in Colombia’s constitutional order, inflation control has a higher priority in the national agenda than full employment; contrary to what happens in the United States where, with the issuance of the Employment Act of 1946, full employment was given the highest priority over the other objectives of U.S. economic policy (Rodriguez, 2018; Arrow, 1974). At least it is perceived that, today, this situation has been clarified in Ruling C-481/99. It is undeniable that the Bank’s independence has curbed the excessive expansion of the money supply and primary issuance as a frequent practice in the past in Colombia and in other countries of the region that have experienced hyperinflationary phenomena with slow recoveries.

On the other hand, the neoclassical tradition tried to give a lucid answer to the recurrent question among economists in the 1960s: how much economic growth is necessary to reduce unemployment, so that an economy reaches full employment? Thus, a famous empirical regularity was born, enunciated in 1962, known as Okun’s Law in honor of its author. This law states that unemployment entails enormous intertemporal economic and social costs due to its depressive effects. Similarly, since the publication of Phillips’ seminal paper (1958), which established an inverse relationship between unemployment and the rate of change of money wage rates in the United Kingdom between 1861-1957, the Phillips Curve gained remarkable popularity in macroeconomics and economic policy decisions in the capitalist world. This relationship “is really just an empirical description of what was true in the data without any particularly good theories as to why it should look that way, how it would change in response to policy, and what might make it unstable.” (Snowdon & Vane, 1999, p. 438). These two empirical regularities, although they do not escape criticism, have helped to understand that there is an inconsistent relationship between real output and unemployment, as well as the Phillips curve that inversely relates the rate of change of inflation and the rate of change of unemployment as an exchange mechanism.2

Throughout its economic history, Colombia does not report hyperinflationary episodes as other countries in the region do, a fact that creates confidence in the central bank as the economic authority. The Constitutional Court in Ruling C-481/99 emphasizes that the autonomy of the Banco de la República, and of its governing body, the Board of Directors, is not accidental, but constitutes an essential element of its constitutional configuration, since it was considered by the Constituent Assembly as an indispensable means to control inflation (p. 1)

It adds that:

establishing inflation goals is a reasonable strategy to preserve price stability. In fact, authoritative doctrine considers that the goals help to reactivate and coordinate the anti-inflationary forces within the public sector, and outside it, around a specific numerical value, thus strengthening the commitment to price stability (p. 3).

In 1990, inflation in Colombia was 32.36% with an unemployment rate of 10.6%, but by 1999 inflation had fallen sharply to 9.36% and unemployment had risen to 20.1%. Although these figures may suggest the existence of a short-term inverse relationship between inflation and unemployment, it should be remembered that the Philips Curve is not an immutable empirical regularity; on the one hand, and, on the other hand, inflation affects the entire population while unemployment is concentrated in the unemployed labor force as a proportion of the total population. This should not necessarily be interpreted to mean that inflation control is more important than the fight against unemployment; both are essential and complementary macroeconomic objectives in the economic policy of any country.

Since 1993, the Bank’s Board of Directors has focused on setting annual inflation targets and, since 2003, on establishing inflation bands in order to anchor the decisions of economic agents, align policy instruments, and ensure that inflation moves between two bands with a lower limit of 2% and an upper limit of 4% (with a long-term average target of 3%). It could be said that the central bank’s price stabilization policy has been relatively successful and has generated credibility and confidence among economic agents. The figures show that, in certain years and periods after the issuance of the 1991 Political Constitution, for example, since 1997, except in 1998 and in the periods 2006- 2008, 2015-2016 and 2021-2022, the observed inflation has been lower than the expected inflation, fully complying with the targets set, as shown in Figure 1.

The debate has focused for more than three decades on the possible trade-off between inflation and full employment as rival objectives. The impact of manufacturing industry on economic growth and the generation of productive employment has been relegated to the background. Unfortunately, the country has forgotten that early industrialization has negative effects on economic growth, since manufacturing production in itself is technologically more dynamic compared to other branches of economic activity. Now, the formal manufacturing sector shows an unconditional convergence of labor productivity unlike the rest of economic activities (Rodrik, 2013) and the presence of a process of “premature deindustrialization” (Rodrik, 2016) that shows that developing countries are transforming into service economies without having gone through an adequate experience of industrialization, causing nefarious effects on productive employment.

Methodology

This research study took as official sources of information statistical time series of quarterly and annual frequency from the Colombian national accounts system in constant terms taking 2015 as a basis, and the labor market statistics of the National Administrative Department of Statistics of Colombia (DANE). For the analysis of the deindustrialization process, the study used international databases such as the World Penn Table 10.0 (Feenstra, Inklaar & Timmer, 2021) and the dataset prepared by the Growth and Development Center of the University of Groningen, Netherlands (Timmer et al., 2014), which includes a set of ten branches of economic activity (ISIC Rev. 3.1) from annual time series of value added (1950-2011 and employment 1950- 2010), internationally comparable information in the regions of Africa, Asia and Latin America.

For the analysis of causal relationships, in the case of quarterly time series, these were seasonally adjusted. Due to the presence of a unit root in the series used (non-stationary series), a cointegration process was carried out by expressing the variables in first differences in order to avoid estimating spurious regressions without statistical and practical validity. The estimation method of the models corresponds to ordinary least squares. In the analysis of the process of deindustrialization and tertiarization of the Colombian economy, several econometric models were estimated by dividing the statistical sample into two subsamples, as follows: 1950-1989 (before the trade liberalization process) and 1990-2011 (period of the current economic opening), in order to show the effects of premature deindustrialization on the generation of employment in Colombia. Finally, by means of the calculation of a sacrifice coefficient, the effects of the price stabilizing measures implemented by the Bank on unemployment in the theoretical framework of the Phillips curve and the calculation of the NAIRU for the measurement of potential GDP by the economic authorities are shown.

Analysis of results

Economists generally believe that there is a perfect relationship between GDP and employment (positive relationship), on the one hand; and between GDP and unemployment (negative relationship), on the other; which automatically and directly suggests that, in order to reduce the unemployment rate to its natural level, it is enough to force the productive apparatus to grow above a certain level. This assertion is very popular in the media, but quite simplistic and inaccurate. The functioning of the economy is compared to that of a machine which, with a certain amount of fuel and an efficient operator commanding it, can produce goods in a repetitive and incessant way. Unfortunately, the fuel of the economy is the changing and unpredictable behavior of economic agents guided by incentives or disincentives, by rationality or irrationality, by selfishness or empathy, by the desire for profit or by cooperative and altruistic principles whose desired purpose would be the common good.

It is convenient to test for the Colombian economy the inconsistent relationship between GDP and unemployment in the framework of Okun’s Law with time series corresponding to the period 1980-2022 by means of an econometric model expressed in first differences (non-stationary series), based on the following specification:

(1)

(1)where  = Change in real unemployment; β

0 = constant term indicating the rate of change in long-run unemployment given by structural factors, that may be demographic, institutional, technological, etc.; β

1 = Factor relating changes in unemployment to changes in output, which reflects the dynamic relationship between changes in unemployment and long-run economic growth; Y

t

= Real GDP; ε

t

= Error term.

= Change in real unemployment; β

0 = constant term indicating the rate of change in long-run unemployment given by structural factors, that may be demographic, institutional, technological, etc.; β

1 = Factor relating changes in unemployment to changes in output, which reflects the dynamic relationship between changes in unemployment and long-run economic growth; Y

t

= Real GDP; ε

t

= Error term.

When estimating the model by ordinary least squares, the following results are obtained (Table A1 of Appendix):

(2)

(2)

(3, 3917)(0, 7602)3

R

2 = 33.12%;

R

2 = 33.12%;  = 31.45%; DW = 1.922404.

= 31.45%; DW = 1.922404.  = Okun’s coefficient calculated from: β

1 = 3.4 then: 1/ β

1 = 1/3.4 = 0.3.

= Okun’s coefficient calculated from: β

1 = 3.4 then: 1/ β

1 = 1/3.4 = 0.3.

According to Okun’s (1962) literal interpretation, for each percentage point of growth in national product (GDP), the variation in unemployment would be -0.3 percentage points and, analogously, a one percentage point increase in the unemployment rate reduces national product by 3.4 percentage points. In other words, if GDP increases by 1%, unemployment would decrease by 0.3%, and if unemployment increases by 1%, then GDP would decrease by 3.4%.

The Bank is very conservative in the adoption of economic policy measures and in the selection of policy instruments such as the intervention interest rate and the free floating of the exchange rate. The existence of an inverse relationship between the inflation rate and the unemployment rate is still believed, known in the economic literature as the Phillips Curve, according to which the decrease in unemployment in the short term would be feasible thanks to the increase in inflationary pressures, which will eventually undermine the purchasing power of Colombian consumers.

When representing the inflation and unemployment rates in Colombia for the period 1980-2022 in a line graph, it can be seen that from 1980 to 1997 inflation and unemployment were inversely related with a correlation coefficient of −0.74, but in 1998 this relationship changed drastically; a direct relationship emerged between inflation and unemployment with a correlation coefficient of 0.41 (the lower the inflation the lower the unemployment and vice versa); the relationship of association between these two economic variables even becoming weaker. If we take the entire period from 1980- 2022, the correlation coefficient is only −0.16. Several authors have shown in recent decades that, in most countries of the world, the relationship between the inflation rate and the unemployment rate (Phillips Curve) no longer exists in the classical form (Figure 2). Currently, the underlying empirical relationship is between the variation of the inflation rate and the variation of the unemployment rate.

Gómez & Julio (2000) and Nigrinis (2003) provide empirical evidence on the non-linearity of the Phillips curve in Colombia. The curve is convex, which means that the best time to stabilize inflation is the boom phase of the economic cycle, inevitably generating a contraction of employment and an increase in unemployment, which is the cost that society has to pay for moderate inflation. Gómez & Julio (2000) estimate the non-accelerated inflation unemployment rate of 8.4%, which equals the natural rate of unemployment, a situation in which any economy would be in a situation of full employment. As an example, if, as of September 2022, according to DANE, the unemployment rate in Colombia was 10.7% (2,696,316 unemployed persons), considering that the NAIRU is effectively 8.4%, this would imply that to maintain an inflation rate between 2% and 4%, the economy would have to keep 2,116,734 persons unemployed. This would correspond to the sacrifice of keeping the labor force unemployed at the expense of preserving the purchasing power of the Colombian currency, as established in the 1991 Political Constitution (articles 373 and 374).

To develop monetary policy, the Bank calculates the potential GDP, which is defined as that which isolates fluctuations of a cyclical or transitory nature, which generate deviations from its medium- and long- term trend. One of the greatest difficulties of economics (of an insurmountable nature) is precisely to give exact explanations to inexact phenomena and to make forecasts about unknown objects. However, in order to understand something about how potential GDP operates, it is appropriate to add some figures to the description. Thus, a real potential GDP in 2015 of 3.24% in the Colombian economy in crude calculations could mean the creation of 735,875 new jobs, that is, unemployment could fall from 11.1% to 8.05% with the aggravating factor that this rate is lower than the NAIRU (8.4% as described below), which would be interpreted by the central bank as an undesirable situation of inflationary pressure that warrants in theory sacrificing employment to stabilize prices (competitive deflation).4

Using quarterly frequency series of GDP for the period 2001:1-2022:4, we proceeded to calculate Colombia’s potential GDP through a Hodrick-Prescott (1997) filter. In Figure 3, the blue line represents the actual or observed GDP recorded by DANE in the national accounts system and the red line represents the trend GDP. It is observed that in some quarters the blue line was below the red line and in others it was above it. There is a quite noticeable fact: in 2020 the blue line moved considerably downwards with respect to the red line. This year corresponds to the COVID-19 pandemic that caused GDP to fall to 6.8% with high unemployment and increased poverty. That situation is similar to the one experienced by Colombia in the Great Depression of the 1930s.

When the blue line remains above the red line, it means that effective GDP grows more than potential GDP, i.e., aggregate demand is greater than aggregate supply (inflationary pressures are present and the monetary authority acts by raising the intervention interest rate to cool consumption, which reduces production and, consequently, employment); in conclusion, unemployment decreases, but at the cost of inflationary pressures and, when the opposite occurs, aggregate supply grew faster than aggregate demand with lower inflationary pressures, but with an increase in unemployment.

According to Gómez (2020), measuring the natural rate of unemployment (despite the numerous efforts of many researchers in the world) is very difficult because the unemployment rate is changeable in the long run due to demographic and structural factors, such as birth rate, emigration, aging, labor informality, changes in the economic cycle, etc. The unemployment rate is seasonal (for example, it is considerably low during the months of November and December of each year and then rises in the first three months of each year); in contrast, the inflation rate is not seasonal but strongly autoregressive, i.e., current inflation depends on past inflation.

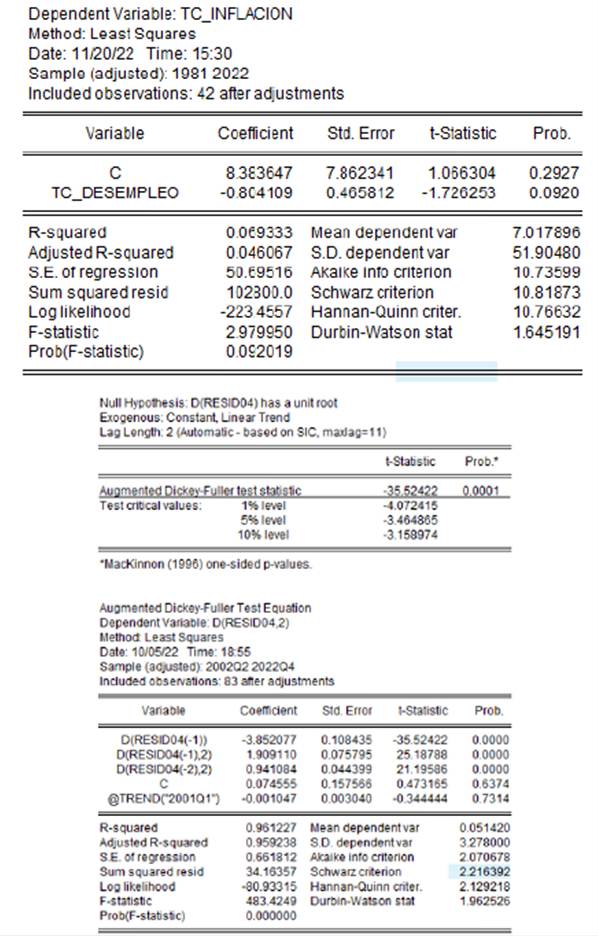

From equation 3 (expressed in growth rates), we proceeded to estimate the natural rate of unemployment for Colombia for the period 1980-2022. The unemployment rate only explains 6.93% of inflation, i.e., there are other variables with greater explanatory value, for example, the money supply not considered in this analysis. The interpretation of this model is summarized as follows: if the unemployment growth rate increases by one percentage point, then the inflation growth rate will decrease by 0.8041 percentage points and vice versa (Table A2 of Appendix).

(3)

(3)

(7.8623) (0.4658)

R

2 = 6.93%;  = 4.61%; DW = 1.645191

= 4.61%; DW = 1.645191

Alternatively, considering that β 1 = −0.8041, then 1/ β 1 = 1/−0.8041 = −1.24. For each percentage point of growth in the unemployment rate, the variation in inflation would be −1.24 percentage points and, analogously, a one percentage point increase in the unemployment rate would reduce inflation by 0.8041 percentage points. It is worth noting that, although the effects on inflation and unemployment rates appear to be large, they are actually small. It should be remembered that the values are expressed in terms of the growth rate of the respective inflation and unemployment rates as calculated by DANE.

The natural rate of unemployment for Colombia in the indicated period was calculated from the quotient β 0 / β 1, replacing in the formula: 8.3837/ − 0.8041 = 10.4%. This value is consistent with theory since it is close to the average unemployment rate in the period 1980-2022 of 11.1%, although it differs from the NAIRU value estimated by Gómez & Julio (2000) of 8.4%, a value used by the Technical Committee of the potential GDP calculation and by the Technical Directorate of the Autonomous Committee of the Fiscal Rule of the Ministry of Finance and Public Credit for fiscal policy purposes.

Based on annual inflation and unemployment data in Colombia for the period 1980-2022 and considering the sub-periods 1980-1989 (before the economic opening) and 1990-2022 (after the opening), the unemployment sacrifice coefficient is calculated as an effect of inflation stabilization. This coefficient is defined as the accumulated excess unemployment above the equilibrium level (or natural rate of unemployment, which in Colombia is equivalent to 8.4%) divided by the reduction in inflation per period. This sacrifice coefficient represents the cost in percentage points of additional unemployment for each percentage point reduction in inflation.

Thus, the sacrifice ratio in the 1980-1990 period was only 0.38%, which means that, for each percentage point reduction in inflation, unemployment increased by 0.38 percentage points; in the 1991-2022 period it was −0.12 and in the 1980-2022 period it was only −0.04 percentage points. Note that in the last two periods the coefficient was negative, which means that the great achievements in the stabilization of inflation in Colombia in aggregate terms have not meant increases in unemployment; on the contrary, the figures indicate that additional jobs were surely generated, thanks to the recovery of the purchasing power of the national currency favoring private consumption and investment and, consequently, greater production, which drives job creation, as shown in Table 1.

Table 1 Cost in terms of unemployment due to inflation reduction (sacrifice ratio)

| Year | 1980 | 1990 | 1991 | 2022 |

| Inflation (%) | 25.9 | 32.4 | 26.8 | 11.4 |

| Inflation variation (%) | 6.5 | -15.4 | ||

| Unemployment (%) | 9.5 | 10.6 | 10.1 | 11.0 |

| Natural unemployment rate 1980-1989. | 8.1 | |||

| Natural unemployment rate 1990-2022. | 9.1 | |||

| Natural unemployment rate 1980-2022. | 10.4 | |||

| Excess unemployment above natural rate 1980-1989* | 2.5 | |||

| Excess unemployment above natural rate 1990-2022* | 1.9 | |||

| Excess unemployment above natural rate 1980-2022* | 0.6 | |||

| Unemployment sacrifice ratio 1980-1989 (%) | 0.38 | |||

| Unemployment sacrifice ratio 1990-2022 (%) | -0.12 | |||

| Unemployment sacrifice ratio 1980-2022 (%) | -0.04 |

Note: *Excess unemployment was calculated as the difference between the unemployment rate in the year of study and the natural unemployment rate of the respective period. The natural rate of unemployment in the different periods was estimated by means of regressions of unemployment against inflation. Both variables are expressed in growth rates using the ordinary least squares method.

Source: own elaboration.

Discussion

The arguments for and against the target inflation policy under the Bank’s direction are varied, such as the one expressed by the Chicago School’s money neutrality theory, which states that the monetary policy that contributes to reduce price level does not necessarily affect variables such as production and employment. The Court is aware that the variables of the economic system are interdependent, therefore, the monetary, credit and exchange policy must be consistent with the general economic policy. Hence, the National Government is represented on the Board of Directors as the governing body of the Banco de la República through the participation of the Minister of Finance and Public Credit. The Minister of Finance and Public Credit, representing the President of the Republic, is one of the seven persons that make up the Board of Directors, including the five co-directors.

As commented in another section, empirical evidence indicates that the discussion should not revolve around the apparent rivalry between price stabilization and full employment, but rather around sustained economic growth as a generator of employment based on bolder productive development policies. The Colombian manufacturing industry had a better economic performance between 1990-2010 compared to 1950-1989, in which industrial and productive development policies were marked by the adoption of the import substitution industrialization model that gradually lagged behind trade and other services. Thus, in the 1990-2010 period, for each percentage point in- crease in national income, manufacturing industry increased by 1.05% compared to 0.99% in the period prior to trade liberalization. The performance of trade in the two periods cited was superior to that of industry, although the highest coefficient corresponds to the 1990-2010 period of 1.73% for each percentage point increase in national income.

Unfortunately, it is not possible to compare the effects of national income on industry and trade employment in each period because most of the estimated employment models are not statistically significant (p-value > 5%). In the 1950-1989 period, for each percentage point increase in national income, trade employment increased by 1.007% (one to one). In the 1950- 2010 period, national income had a greater impact on trade value added (1.50%) than on industry value added (1.15%). In turn, national income had a stronger impact on employment generated in commerce (2.26%) than that generated in industry (1.38%), as shown in Table 2.

Table 2 Effects of national income on value added in manufacturing industry, commerce and on sectoral employment in industry and commerce in Colombia 1950-2010

| Period. | Variable | Coefficient | Standard error | P-value | R2 | R2 adjusted | Durbin Watson |

| 1950-1989 | Industry VA | 0.992731 | 0.164165 | 0.0000 | 0.497064 | 0.483471 | 1.318700 |

| Commerce VA | 1.420015 | 0.129744 | 0.0000 | 0.764011 | 0.757633 | 1.602434 | |

| Industry employment | 0.103275 | 0.275491 | 0.7099 | 0.003784 | -0.02314 | 1.252234 | |

| Commerce employment | 1.007274 | 0.232881 | 0.0001 | 0.335822 | 0.317871 | 2.175661 | |

| Industry employment vs Industry VA* | 0.216206 | 0.334488 | 0.5222 | 0.140876 | 0.067237 | 1.892048 | |

| Commerce employment vs Commerce VA | 0.746093 | 0.145502 | 0.0000 | 0.478586 | 0.433893 | 1.906730 | |

| 1990-2010 | Industry VA | 1.053441 | 0.271896 | 0.0010 | 0.441361 | 0.411959 | 1.675068 |

| Commerce VA | 1.733136 | 0.211183 | 0.0000 | 0.77997 | 0.768389 | 1.829474 | |

| Industry employment* | 2.276791 | 1.286287 | 0.0928 | 0.141556 | 0.096375 | 1.962954 | |

| Commerce employment* | 0.098931 | 0.494078 | 0.8434 | 0.002106 | -0.05042 | 2.297542 | |

| Industry employment vs Industry VA | 1.039344 | 0.236872 | 0.0003 | 0.503304 | 0.477162 | 1.815203 | |

| Commerce employment vs Commerce VA* | 0.174706 | 0.248827 | 0.4911 | 0.025290 | -0.02601 | 2.318432 | |

| 1950 - 2010 | Industry VA | 1.150825 | 0.175099 | 0.0000 | 0.552558 | 0.528588 | 2.002657 |

| Commerce VA | 1.504909 | 0.109641 | 0.0000 | 0.764607 | 0.760549 | 1.840625 | |

| Industry employment | 1.377500 | 0.639877 | 0.0357 | 0.076611 | 0.027144 | 2.018268 | |

| Commerce employment | 2.255236 | 0.579490 | 0.0003 | 0.207063 | 0.193392 | 1.874735 | |

| Industry employment vs Industry VA | 0.713261 | 0.145533 | 0.0000 | 0.232139 | 0.191004 | 2.002955 | |

| Commerce employment vs Commerce VA | 0.445077 | 0.116470 | 0.0003 | 0.169971 | 0.125506 | 1.945323 |

Note: *Models with neither statistical nor practical validity. VA: Value added. All models were estimated in natural logarithms and first differences. The models of employment in industry vs. total GDP in the 1950-1989 sample and employment in industry and commerce vs. total GDP in the 1990-2010 sample are not statistically significant (prob. > 5%). All models estimated for the period 1950-2010 are statistically significant (prob. < 5%).

Source: own elaboration with information from Dataset The Groningen Growth and Development Centre (n.d.).

The empirical evidence provided indicates that, in Colombia, since World War II, trade had a better dynamism than industry both in its contribution to total value added and employment, whose impact is very significant (if total value added increases by 1%, employment in services will increase by 2.26% while, in industry, if total value added increases by 1%, employment will increase by 1.38%).

To summarize, in the Colombian economy in the period 1950-2010, employment generation depended to a greater extent on the good performance of trade value added; although it is fair to understand that the manufacturing industry could have a greater impact on productive employment than trade if the following empirical finding is considered: if trade value added increases by one percentage point, employment in trade will increase by 0.44%; on the other hand, if manufacturing value added increases by 1%, employment will increase by 0.71%. For this reason, economies, regardless of their size, degree of development and level of trade openness, should focus on industrial and productive development and not let trade gain the upper hand and hegemony. It is worth remembering that in Colombia’s economic history, the Colombian coffee industry gained prominence due to the generation of foreign currency and the manufacturing industry became accustomed to occupying a secondary place.

Conclusions

In Colombia, since the issuance of the 1991 Political Constitution, the debate between the stabilization of inflation by the Board of Directors of the Banco de la República using the monetary, credit and exchange policy channel and the achievement of full employment under the responsibility of the national executive through fiscal policy has become more visible. The Constitutional Court in Ruling C-481/99 pronounced in this regard, arguing that monetary policy must be coordinated with economic policy in general.

The calculation of the unemployment sacrifice coefficient for Colombia in the period 1980-1989 (pre-opening) is 0.38%, while in the period 1990- 2022 (post-opening) it is -0.12%. These data suggest that inflation stabilization measures have been successful in not leading to increases in unemployment; on the contrary, as inflation was reduced by one percentage point, unemployment also decreased by 0.12%. This could also be interpreted as evidence against the empirical validity of the questioned Phillips curve, in favor of the thesis that the Banco de la República inflation target has not accelerated unemployment, given that in Colombia, since 1998, the inflation and unemployment curves have been moving in the same direction with a positive correlation coefficient of 0.41%.

There is widespread confidence among economists in economic growth as an engine of employment generation and unemployment reduction. The empirical evidence provided by this research shows that the GDP/employment and GDP/unemployment relationships are inconsistent over time. The former presents a positive correlation of 41.7% and the latter, a negative correlation of 50.8%. This implies that unemployment is not corrected only by making the economy grow at a certain level as suggested by Okun’s Law. For Colombia to reduce its unemployment by 1%, national product must grow by 3.4%.

The impact of national income on sectoral value added and on employment shows a greater economic dynamism of commerce with respect to manufacturing. In the period 1950-2010, the generation of employment depended to a greater extent on the good performance of the value added of commerce; although the manufacturing industry managed to have a greater impact on productive employment than commerce itself, taking into account that if the value added of commerce increases by one percentage point, employment in commerce will increase by 0.44%. On the other hand, if the value added of manufacturing increases by one percentage point, employment will increase by 0.71% (almost twice as much).