English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

Permalink

INTRODUCTION

Bitcoin's price is notoriously volatile and influenced by various factors, including the demand for decentralized payment methods (Polasik et al., 2015), government regulation (Shanaev et al., 2020), and investor interest in cryptocurrencies (Georgoula et al., 2015). Text-based social media like Twitter and Reddit also significantly impact Bitcoin's price dynamics. Studies show that Bitcoin-related news can predict its price (Yao et al., 2019), while activity on platforms like Twitter strongly influences the volume and volatility of Bitcoin transactions (Shen et al., 2019). Celebrity tweets, such as those from Elon Musk (...), have shown notable impacts on Bitcoin markets. (Ante, 2021) and Donald Trump (Huynh, 2021)-and found notable impacts on Bitcoin markets. Similarly, activity on Reddit, including the number of posts by new users on subreddits like "/r/Bitcoin," has proven to be a significant long-term predictor of Bitcoin's price (Phillips & Gorse, 2017).

While the relationship between text-based social media and Bitcoin's price has been widely explored, the effect of audiovisual content, such as movies, series, videos, and documentaries, remains under-researched. Audiovisual media, readily accessible on platforms like YouTube and Twitch, can significantly influence viewers' ideas and behaviors (McCormick et al., 2019). For example, documentaries on climate change have been shown to provoke reactions among viewers, while content in movies and television can shape behaviors related to smoking, violence, and sexual initiation (Brown et al., 2006; Charlesworth & Glantz, 2005; Johnson et al., 2002). Furthermore, the growing influence of financial influencers, or "finfluencers," on platforms like Instagram and YouTube-who offer investment advice to large audiences-raises questions about the quality and reliability of their content, especially given the rise in fraud and legal issues. A recent proposal to introduce a quality index for finfluencers, the "FinQ-Score," suggests a framework to help users make informed decisions, a tool that could be extended to assess cryptocurrency-focused creators on audiovisual platforms.

To address this gap, this study analyzes how audiovisual content consumption influences Bitcoin's financial variables through correlation analysis and econometric modeling, focusing on platforms like YouTube and Twitch. Findings indicate a positive and statistically significant impact on Bitcoin's price and volume associated with the number of subscribers to cryptocurrency-related YouTube channels. At the same time, models based on Twitch data show no significant effect. The paper is structured as follows: Section 2 provides an exhaustive literature review; Section 3 describes data sources and methodology; Section 4 presents findings, including correlations between cinematic content and Bitcoin variables and econometric model results. Finally, Section 5 offers conclusions and future research suggestions.

THEORETICAL FRAMEWORK

Cryptocurrencies are encrypted digital currencies that ensure secure transactions through blockchain technology (Junmde & Cho, 2020). Cryptography transforms readable information into complex cryptographic codes, making them difficult to compromise (Milutinovic, 2018). These encrypted codes are recorded on a block-chain-a distributed ledger that securely tracks all transactions, ensuring transparency and immutability.

Within the cryptocurrency ecosystem, most other cryptocurrencies are called Altcoins. Altcoins share a foundational structure with Bitcoin but often feature modifications in parameters such as total coin supply and block mining time. Some Altcoins have also introduced unique operational features, distinguishing themselves from Bitcoin's original design (Hileman & Rauchs, 2017). Blockchain technology underpins all cryptocurrencies, enabling decentralized transactions and enhancing security through cryptographic measures (Feng et al., 2024). This technology's key advancements include public ledgers and governance mechanisms that allow direct peer-to-peer transactions (Vinkóczi et al., 2024). However, the security of blockchain platforms depends on the robustness of their underlying code, and vulnerabilities persist despite measures like encryption, digital signatures, and hash algorithms (Zhou et al., 2024). Consequently, developing a trustworthy cryptocurrency ecosystem remains a significant challenge (Feng et al., 2024).

Despite technological advancements, the cryptocurrency market faces mul-tifaceted challenges. Notably, cases of deliberate price manipulation are prevalent, with some individuals artificially inflating or deflating prices to profit or create unrealistic expectations around new cryptocurrencies. Such practices often mislead investors by promising substantial returns, thereby increasing perceived risk and reducing both investment and adoption willingness (Gandal et al., 2021; Smith & Castonguay, 2020). This lack of stability and the potential for exploitation impact overall trust in cryptocurrencies and highlight the need for improved security and regulatory measures within the ecosystem (Buhbut et al., 2024).

In summary, cryptocurrencies offer innovative solutions like decentralized transactions and robust security through blockchain technology. However, the ecosystem must address volatility, security, and trust issues to achieve widespread adoption and reliability.

Bitcoin

There are various definitions of Bitcoin, all agreeing on its creation by Satoshi Nakamoto in 2009 is independent of a regulatory entity, and is based on blockchain technology. However, we choose to highlight Fosso Wamba et al. (2019), who define Bitcoin more holistically as "a currency based on computer systems that has no physical, legal counterpart, used as a means of exchange through computer systems and online communication protocols" (p. 3).

While the cryptocurrency has had its ups and downs over the years, Bitcoin has experienced exponential growth in recent months, reaching up to US $72,000, surpassing Silver for the first time in history, and positioning itself as the crypto-currency with the highest market capitalization and price (Elliot, 2024). Another singular characteristic of this type of currency is that Bitcoin transactions have a peer-to-peer nature without intermediaries. Therefore, the operation only requires the consensus of both parties involved in the transaction to be carried out (Fosso Wanba et al., 2019). These transactions can be conducted at any time, twenty-four hours a day, seven days a week. Additionally, the majority of these transactions correspond to investors wishing to speculate rather than buy goods and/or services (Dyhrberg et al., 2018).

Volatility

Bitcoin volatility is considered one of the main variables representing present risk in the cryptocurrency market (Chinazzo & Jeleskovic, 2024; Hu, 2019). This volatility is one of the obstacles that hinder the use of this crypto asset as a means of exchange and is the reason it is positioned as a high-risk investment instrument (Baur & Dimppfl, 2017).

Over the past years, perceptions of Bitcoin regarding volatility have changed on different occasions. Such was the case in the years preceding the large price surges in 2017, where it was believed that the asset's variability was decreasing, but without ruling out the possibility of future changes in this trend, considering the market's immaturity (Bouoitour & Selmi, 2016). Additionally, it was estimated that if the trend at that time extended sufficiently, Bitcoin would reach the volatility of other fiat currencies by 2019 or 2020 (Cermak, 2017).

The projections and diagnoses regarding the Bitcoin market have changed over time as the understanding of the various factors influencing volatility improves. For this reason, the literature reports that past volatility values are good predictors of future values and exchange volume (Aalborg et al., 2019; Conlon et al., 2023). Additionally, macroeconomic or financial variables have been observed to have a very low influence on Bitcoin variability (Guizani & Nafti, 2019).

Bitcoin and Media

Attention to Bitcoin prices began to rise following its rapid price surges and declines starting in 2017 (Zhang & Wang, 2020). The aforementioned led news media to report on the latest Bitcoin-related events. However, these news reports may contain more than objective information, such as the emotions conveyed. Some news reports and emotions impact the audience that hears them, which is then received by the public, including investors. The analysis of these emotional processes within the media has resulted in the discovery that, through Machine Learning tools, the text within Bitcoin news can be used to predict the price of this crypto asset (Yao et al., 2019). Similarly, Bitcoin returns are also influenced by sentiments in online news reports obtained through computational linguistic techniques (Polasik et al., 2015).

Furthermore, at a more specific level, evidence has been obtained that news related to Bitcoin experts generates short-term price movements that follow the direction of the conveyed sentiment (Karalevicius et al., 2018). In other words, if the sentiment is positive, the price rises, whereas if it is negative, it declines. This reveals some mechanics explaining how the media influences the Bitcoin market. The literature regarding the relationship between Bitcoin price and the media is relatively scarce, considering social media activity. However, it is worth noting that these platforms are powerful channels through which reactions to these news travel.

Bitcoin and Social Media

Various news outlets post about Bitcoin and other topics on social media. Bitcoin posts on each platform and website have been the subject of studies and discussions in recent years, which is why we will now delve into them.

This platform has motivated academics to use the information contained within it to represent investors' thoughts, emotions, or behaviors. It hosts a large flow of short messages created by users, which collectively provide clues about the dynamics followed by different groups of people discussing the same topic.

As with Bitcoin literature, multiple articles analyze the text in Tweets, identifying the sentiments within them. This is then used to predict the behavior of the cryptocurrency's price (Colianni et al., 2022; Pant et al., 2018; Sattarov et al., 2020). Similarly, emotions from Twitter have been shown to be related to Bitcoin variables such as price, exchange volume, returns, and volatility (Gao et al., 2021).

Some choose not to use emotion analysis but instead estimate investor attention on Bitcoin with the number of Tweets containing the term "Bitcoin" within the text. They have found that this number of occurrences is capable of driving the next day's values, particularly volatility and Bitcoin exchange volume (Shen et al., 2019).

Even publications focusing solely on tweets from individual accounts, often belonging to celebrities, exist. Such is the case of Elon Musk, whose messages on the platform have been studied regarding Bitcoin behavior but without significant results (Ante, 2021). Conversely, other researchers have found that sentiments in tweets from former United States President Donald Trump are correlated and can predict variables in the Bitcoin market (Huynh, 2021).

Thus, it is pertinent to discuss other social media that generate Bitcoin-related content to see if they impact the value of this cryptocurrency. Now, let us move on to Facebook.

Various types of relationships exist between information about Bitcoin and Facebook, whether focusing on its characteristics as a social media platform, a company, a developer of tools, or a proponent of new proposals regarding Blockchain. For example, the Bitcoin exchange volume has been analyzed concerning the emotions contained in financial news within a highly popular Facebook group, with results indicating no significant relationship between the two variables (Jerdack et al., 2019).

This research focuses on the Bitcoin group with the most followers at the time, named "Bitcoin Chart." This emphasis is relevant for investigative designs related to social media, highlighting the need to find data sources representing the highest possible number of interactions. Indeed, one of the criticisms the authors make of their research is that it would have been valuable to collect more news from other highly popular Facebook groups (Jerdack et al. 2019).

Studies analyzing Facebook from a corporate perspective have discovered that Facebook's financial instrument prices have influenced the price of Bitcoin (Bartos, 2015). Likewise, it has been proposed that the growth of this social media and Bitcoin follows the behavior of mathematical models such as the Gompertz function (Peterson, 2019). Consequently, Peterson (2019) suggests that the price of Bitcoin is not necessarily the result of investment emotions but instead follows the characteristics of network economies.

However, some publications have chosen to study Bitcoin through the open algorithm developed by Facebook: "Prophet." This has been used to model energy consumption projections and the amount of technological waste generated by Bitcoin mining (Jana et al., 2022), as well as the relationship between Bitcoin, the gold market, and US monetary changes (Akdag & Emsen, 2021).

Finally, Facebook has also created its own cryptocurrency called "Libra." This cryptocurrency measures the impact of its volatility with changes in the price of Bitcoin (Senarathne, 2019), and it is also compared with other cryptocurrencies like Ethereum (Li & He, 2020)

YouTube

YouTube is another platform that significantly impacts internet users. It is primarily based on video-format information, distinguishing it from the aforementioned media, whose primary element is text. However, studies relating this platform to Bitcoin are scarce, as only one publication relating both terms could be located. Hence, it is crucial to analyze this research.

The methodology used to obtain data was 'Web Crawling," a programming tool that identifies YouTube videos about Bitcoin and records figures such as views for each video (Partida, 2019). This researcher's methodology aids in extracting data from YouTube, thus facilitating the selection of videos for our research.

This platform comprises various discussion topics, and literature has shown interest in what is discussed on it when Bitcoin is the main topic. Some publications discuss Bitcoin subjectively and other cryptocurrencies, often sparking larger, longer discussions with a higher likelihood of going viral online (Glenski et al., 2019). Conversations found in subreddits like "/r/Bitcoin" have revealed that metrics such as the number of posts, novice authors, and new subscribers are capable of predicting Bitcoin's long-term price (Phillips & Gorse, 2018). Similarly, along with the subreddit "/r/BitcoinMarkets," they precede the behavior of price volatility and cryptocurrency returns (Phillips & Gorse, 2018).

Like literature on other social media, interactions within Reddit have been analyzed in terms of the emotions they contain. Consequently, results affirm the ability of these variables to predict Bitcoin's price (Prajapati, 2020). Additionally, other publications consider variables such as the language used in studying emotions on Reddit, thereby reducing errors in predicting Bitcoin prices (Glenski et al., 2019). Furthermore, Reddit data have been utilized to examine the accuracy in predicting the direction of Bitcoin price movements (Wooley et al., 2019), the words most correlated with Bitcoin price dynamics (Burnie & Yilmaz, 2019), and the ability to forecast financial bubbles in the prices of various cryptocurrencies, Bitcoin included (Phillips & Gorse, 2017).

Google is a platform considered one of the largest search engines available on the internet and is also regarded as the primary source of information search by cryptocurrency investors, surpassing Yahoo, Bing, or Ask (Aslanidis et al., 2022). Typically, Google Trends is used to visualize search levels over time based on queried words or terms. Thus, it measures the attention users direct toward searched terms or concepts, which, for our research purposes, will focus on cryptocurrencies and/ or Bitcoin. For example, Abraham et al. (2018) managed to predict the direction of changes in the price of Bitcoin using information from Twitter and Google, using variables such as search levels relative to words like "Bitcoin" or "BTC." On the other hand, Zhang and Wang (2020) conducted research that coincides with Abraham et al. (2018), as they measured investor attention using Google Trends data and suggested it has significant predictive power in the behavior of the top twenty cryptocurrencies at the time of the study. Similarly, there are relative search levels for the word "Bitcoin" that show high levels related to the price of the cryptocurrency (Kristoufek, 2013; Mittal et al., 2019).

Furthermore, there is evidence that investor attention measured by Google Trends also intensifies sharp changes in the price of Bitcoin, driving upswings and exacerbating downturns (Kristoufek, 2015). Likewise, there are records of research using cryptocurrency return (including Bitcoin), volatility, or volume as variables that cause changes in investor attention (Lin, 2021; Urquhart, 2018). Remarkably, these investigations, unlike the previous ones, suggest that cryptocurrencies influence investor attention rather than the reverse. This sparks a discussion regarding the cause-effect relationship of the crypto-investment context. Alternatively, there are research comparisons of relative search levels corresponding to different concepts and/or search terms regarding Bitcoin. Yelowitz & Wilson (2015) suggest a correlation of Bitcoin with terms related to programming, speculative investors, libertarianism, and criminal activities. Thus, cryptocurrency correlates positively with criminal and programming terms. In this way, we can already understand how Google Trends is used in relation to Bitcoin, as suggested by the findings described above.

We will attempt to analyze the predictive capacity of the variables under consideration through linear regression (simple or multiple), as these variables will enable us to suggest the degree of correlation between visualizations through audiovisual material and the volatility in the price and/or volume of Bitcoin.

DATA AND METHODOLOGY

Research Design and Purpose

This study is an empirical investigation with an exploratory purpose. It aims to quantitatively examine the relationship between audiovisual content on cryptocurrencies and the Bitcoin market.

Data Sources

Bitcoin Data: Historical Bitcoin data, including price and transaction volume, was extracted from Coingecko. The data covered the period from July 7, 2019, to July 11, 2022, and were collected daily.

Audiovisual Content Data: Data on Bitcoin-related audiovisual material were collected from three primary sources:

Study Period

The selected period, from July 2019 to July 2022, reflects a phase of significant growth in cryptocurrency-related content on platforms like YouTube and Twitch and high volatility in the Bitcoin market. This period captures key economic events likely to impact user behavior in terms of search and subscription patterns, providing a solid foundation for analyzing correlations with Bitcoin's price and transaction volume.

Data Collection and Processing

1. Cinematic Material: A set of titles relevant to cryptocurrencies was identified by consulting databases such as IMDb and Rotten Tomatoes, using keywords like "Cryptocurrency," "Crypto," "Blockchain," "Bitcoin," and "Bitcoin-mining." Each title's search volume was obtained from Google Trends to create a weekly time series. The final list of titles is shown in Table 1. In particular, both the price and volume of Bitcoin were obtained from www.coingecko.com, covering the period from July 7, 2019, to July 11, 2022. These data were collected daily and then transformed into weekly data by averaging the values from Monday to Sunday for both volume and price, following Kristoufek's (2013) methodology. This approach not only allowed Bitcoin data to align with other time series that could only be obtained on a weekly basis (such as YouTube channel data from Socialblade) but also reduced data kurtosis, as suggested by Dehouche (2021).

Table 1 Cinematic Material Used

| Variable | Title | Year | Type of content |

|---|---|---|---|

| P1 | How to Sell Drugs Online (Fast) | 2019 | TV Show |

| P2 | Unfriended: Dark Web | 2018 | Movie |

| P3 | Done | 2015 | Movie |

| P4 | Crypto | 2019 | Movie |

| P5 | Hacker (Anonymous) | 2016 | Movie |

| P6 | Deep Web | 2015 | Documentary |

| P7 | Cryptopia | 2020 | Documentary |

| P8 | Bitcoin: The End of Money as We Know It | 2015 | Documentary |

| P9 | Hidden Secrets of Money | 2013 | TV Show |

| P10 | Keiser Report | 2009 | TV Show |

| P11 | The Badger | 2020 | Movie |

| P12 | Viraali | 2017 | Movie |

| P13 | Bitcoin Heist | 2016 | Movie |

| P14 | The Rise and Rise of Bitcoin | 2014 | Documentary |

| P15 | Banking on Bitcoin | 2016 | Documentary |

| P16 | Startup | 2016 | TV Show |

| P17 | Forhoret (Face to Face) | 2019 | TV Show |

Source: Author's elaboration.

2. YouTube Channels: To capture relevant YouTube data, the most popular cryptocurrency-related channels were manually selected based on total views, resulting in a final sample of 50 channels (see Table 2). Data from Socialblade included weekly subscriber gains (YT_nsubs) and view counts (YT_nviews) per channel. The incognito mode was used to avoid biased results from cookies (Tan et al., 2018).

Table 2 YouTube Channels Used in the Study

Source: Author's elaboration.

3. Twitch Metrics: Data were collected from Twitch by identifying relevant programming categories, namely "Crypto" and "Bitcoin." From TwitchTracker, we gathered weekly averages for viewers (TW_AvgVwrs) and the number of active channels (TW_Channls) within these categories.

Model Specification

To investigate the impact of YouTube engagement on Bitcoin, we proposed the following regression models (Equations 1 and 2):

Where:

BTC_PriceBTC_Price: Bitcoin price at time tt,

BTC_VolBTC_Vol: Bitcoin transaction volume at time tt,

YT_NwSbsYT_NwSbs: new YouTube subscribers in cryptocurrency channels at time tt,

YT_VwsYT_Vws: new views in cryptocurrency channels at time tt,

ZZ: control variables such as the CBOE VIX index (Bouri et al., 2017) and the Dow Jones Industrial Average (Jerdack et al., 2019)

Similar models were used for Twitch metrics, incorporating viewer and channel data from Twitch. This methodological framework establishes a foundation for analyzing how audiovisual engagement on social media platforms correlates with Bitcoin market behavior.

The variable YT_VwsYT_Vws represents the number of new reproductions in cryptocurrency-related channels at time tt, while ZZ denotes a set of control variables. These controls include the CBOE VIX index (Bouri et al., 2017) and the Dow Jones Industrial Average (Jerdack et al., 2019), both of which have been shown to impact cryptocurrency markets.

For the models based on Twitch metrics, we propose the following specifications (Equations 3 and 4):

In these models:

BTC_PriceBTC_Price is the dependent variable representing Bitcoin's price at time tt,

BTC_VolBTC_Vol represents Bitcoin's transaction volume at time tt,

TW_AvgVwrsTW_AvgVwrs is the independent variable for the average number of viewers of Bitcoin-related content at time tt,

TW_ChannlsTW_Channls represents the number of channels broadcasting Bitcoin-related content at time tt, and

ZZ is the set of control variables, as used in the YouTube-based models.

Each model variable was made stationary by applying the first differences to ensure the accuracy of YouTube model interpretations. Additionally, multicollinear-ity was checked using Spearman's correlation index, confirming that none of the independent variables had a high enough correlation to affect regression outcomes. No issues of heteroscedasticity or autocorrelation among residuals were identified.

After these adjustments, the refined econometric models for YouTube's impact on Bitcoin are Equations 5 and 6:

For Twitch, after similar adjustments, the econometric models to study its impact on Bitcoin are Equations 7 and 8:

Where ΔΔ represents the first differences of the original variables. In all four models, we expect β1 and β 2 to have positive and statistically significant coefficients, indicating a favorable relationship between increases in viewership or channel activity and Bitcoin's price and transaction volume.

RESULTS

Cinematographic Material

The results of Spearman's correlations of the different films, shows, and documentaries with the financial variables of Bitcoin show a low magnitude for each of the contents, both in terms of price and volume. In fact, the audiovisual production that shows a greater positive association between the price of Bitcoin and the search level of the title in Google is How to Sell Drugs Online (Fast), with a weak correlation of 0.177, while in the case of the volume traded, the audiovisual production with a stronger positive association with the level of search for the title is the television series "Startup," with a Spearman's correlation of 0.159. In addition, in both cases, these titles are the only ones with sufficient statistical significance to reject the null hypothesis of a correlation equal to 0 (see Table 3).

In the case of correlations using the YouTube search level, the title with the highest positive association between price and search level was The Rise and Rise of Bitcoin, with a Spearman's correlation of 0.264. Table 4 shows that correlations above 0.3 are not obtained in this case either, so they can be considered weak correlations. Idem, for the case of volume and search level, the correlations are even lower.

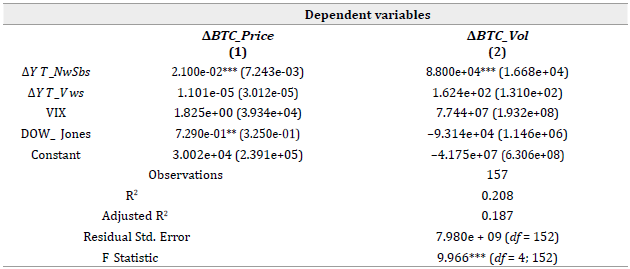

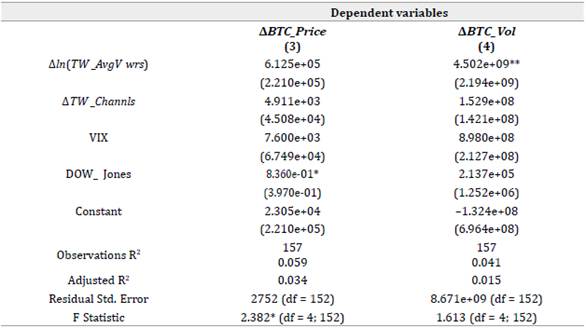

YouTube and Twitch

Tables 4, 5, and 6 show the results of the proposed models. The first model has the first difference in Bitcoin price as the dependent variable, while the second model has the first difference in Bitcoin volume as the dependent variable. As independent variables, in both models, we have the number of new subscribers in channels with content associated with Bitcoin and the number of new views in channels of this topic, together with the control variables previously mentioned in Section 3. In both models, AY T _NwSbs has a positive and statistically significant impact on the price of Bitcoin. The foregoing implies that an increase of 1,000 subscribers from one week to the next (first difference) produces an average effect of $21 on the price of Bitcoin.

The rest of the variables maintain the expected sign but are not statistically significant. In the case of Twitch, although the natural logarithm of the average number of viewers is statistically significant in the model whose dependent variable is volume, the F test indicates that the model is not statistically significant.

Table 3 Correlations between Bitcoin's Financial Variables (Price (P) and Volume (V)) and Google Search Levels (G)

| Var | Spearman's (P) | P-Value | Var | Spearman's (V) | P-Value |

|---|---|---|---|---|---|

| P1G | 0.177 | 0.027* | P16G [Diff] | 0.159 | 0.046* |

| P3G [Diff] | 0.121 | 0.133 | P10G | 0.057 | 0.480 |

| P4G | 0.101 | 0.208 | P11G | 0.026 | 0.742 |

| P9G | 0.099 | 0.217 | P15G [Diff] | 0.022 | 0.789 |

| P10G | 0.08 | 0.317 | P1G | 0.021 | 0.791 |

| P15G [Diff] | 0.076 | 0.342 | P7G [Diff] | 0.004 | 0.964 |

| P7G [Diff] | 0.058 | 0.470 | P6G [Diff] | -0.003 | 0.969 |

| P16G [Diff] | 0.045 | 0.579 | P14G | -0.005 | 0.952 |

| P11G | 0.043 | 0.590 | P12G | -0.015 | 0.847 |

| P2G [Diff] | 0.029 | 0.716 | P9G | -0.018 | 0.819 |

| P17G | 0.011 | 0.891 | P4G | -0.024 | 0.767 |

| P12G | -0.005 | 0.952 | P2G [Diff] | -0.039 | 0.62 |

| P5G [Diff] | -0.037 | 0.643 | P5G [Diff] | -0.073 | 0.366 |

| P8G | -0.077 | 0.338 | P3G [Diff] | -0.084 | 0.295 |

| P6G [Diff] | -0.077 | 0.338 | P8G | -0.086 | 0.286 |

| P13G | -0.082 | 0.306 | P13G | -0.091 | 0.259 |

| P14G | -0.0113 | 0.157 | P17G | -0.138 | 0.084 |

Note. “Diff” indicates that this is the first difference in the time series. *** =0.1 %; ** = 1 %; * = 5 %.

Source: Author's elaboration.

Table 4 Correlations between Bitcoin Financial Variables (Price (P) and Volume (V)) and YouTube Search Levels (G)

| Var | Spearman's (P) | P-Value | Var | Spearman's (V) | P-Value |

|---|---|---|---|---|---|

| P14Y [Diff] | 0.264 | 0.001*** | P10Y [Diff] | 0.161 | 0.044* |

| P17Y | 0.252 | 0.002** | P4Y [Diff] | 0.131 | 0.102 |

| P1Y | 0.180 | 0.024* | P13Y [Diff] | 0.121 | 0.131 |

| P9Y | 0.162 | 0.043* | P5Y [Diff] | 0.118 | 0.142 |

| P15Y [Diff] | 0.151 | 0.058 | P15Y [Diff] | 0.113 | 0.159 |

| P4Y [Diff] | 0.12 | 0.134 | P14Y [Diff] | 0.086 | 0.286 |

| P10Y [Diff] | 0.09 | 0.263 | P1Y | 0.033 | 0.679 |

| P2Y | 0.044 | 0.583 | P9Y | 0.013 | 0.867 |

| P8Y [Diff] | 0.031 | 0.696 | P7Y | 0.003 | 0.971 |

| P5Y [Diff] | 0.027 | 0.738 | P6Y [Diff] | -0.003 | 0.969 |

| P3Y [Diff] | 0.02 | 0.806 | P12Y | -0.015 | 0.856 |

| P16Y [Diff] | -0.042 | 0.605 | P2Y | -0.027 | 0.741 |

| P12Y | -0.043 | 0.593 | P8Y [Diff] | -0.038 | 0.639 |

| P11Y | -0.051 | 0.525 | P17Y | -0.038 | 0.629 |

| P6Y [Diff] | -0.077 | 0.338 | P11Y | -0.058 | 0.474 |

| P13Y [Diff] | -0.093 | 0.249 | P3Y [Diff] | -0.061 | 0.451 |

| P7Y | -0.115 | 0.150 | P16Y [Diff] | -0.066 | 0.411 |

Note. "Diff" indicates that this is the first difference in the time series. *** = 0.1 %; ** = 1 %; * = 5 %.

Source: Author's elaboration.

CONCLUSION

The current literature on Bitcoin comprises a wide variety of studies aiming to recognize the factors influencing its behavior. One approach frequently analyzed is the relationship between social media and this cryptocurrency, where it has been discovered that people's behavior on the web can be useful in predicting variables such as price and its variability.

Table 6 Bitcoin Financial Variables and Twitch Coverage

Note. *p < 0.1; **p < 0.05; ***p < 0.01.

Source: Author's elaboration.

Firstly, the significant results obtained regarding search levels suggest that the popularity with which people search for cryptocurrency-related productions on Google and YouTube generally has a low monotonic correlation with historical Bitcoin data. This link tends to be of similar magnitude over time, with no identified lag period for which Google or YouTube searches are more strongly associated with Bitcoin variable changes in different weeks.

Linear regression of statistics from YouTube reveals that the number of new subscribers to cryptocurrency channels has a positive effect on Bitcoin returns and its exchange volume. This behavior suggests that people's decision to subscribe to a YouTube channel about cryptocurrencies could be linked to investor behavior. However, it is also possible that market events may drive subscriptions on the video platform in the opposite sense. Therefore, this finding may become a motivation for future research, which could explore with causality tests the most likely predictive direction in which these variables are linked.

On the other hand, the performances of the models created based on YouTube information show a considerable capacity to explain variations in Bitcoin returns and its exchange volume. While this capacity implies that other variables not included in the model play a larger role in estimation, the results obtained with YouTube could lead to its predictive capacity being beneficial in models considering a greater number of explanatory variables. Thus, by comparing the predictive capacity results between YouTube and Twitch, it is determined that the variables from the former platform mentioned are more useful in estimating Bitcoin returns or exchange volumes.

Based on the aforementioned resolutions, this research provides an initial background of the relationship between audiovisual material and Bitcoin, assuming it possesses linear or monotonic characteristics. Thanks to the description and comparison of the different available sources of information, new methods for obtaining data on audiovisual material on social media and the web are also presented.

Future research could extend these types of studies to other video content platforms, such as Instagram or TikTok. Additionally, depending on data availability, search engines other than Google and YouTube can be incorporated.