Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Citado por Google

Citado por Google  Similares em

SciELO

Similares em

SciELO  Similares em Google

Similares em Google

Permalink

Permalink1. Introduction

One of the big crises, on a global scale, is the absence of food production that can be managed to cover the needs of all the population. In this sense, the risk of absence of food presents itself as the biggest problem that humanity [16] faces. According to figures of the FAO (United Nations Organization for Food and Agriculture) and the BM (World Bank), the world will suffer food shortage, therefore it is necessary to begin producing more and of a better quality. For that it is necessary that the manufacturers know the production costs and that these are lower so that allows them to gain access to the markets at an accessible price generating a margin of utility adapted for the producers.

In case of the dairy cattle in Peru, it represents the main source of income for the stockbreeders, being one of a few activities that can develop in the high parts of the south of the country. Likewise, it is important for its multiple intentions, such as the production of dairy products and meat. That is why the development of the cattle is urgent to improve the quality of life in many communities, turning out to be crucial to brake the migration to the cities [24].

The milk production for the year 2015 was 1,903,177 tons, in 2016 of 1,954,232 tons and for the year 2017 of 2,010,985 [23], for many small and medium producers it is not profitable because of the low prices that the big industrial enterprises like, GLORIA, NESTLE and LAIVE pay. They establish the conditions of purchase as for: quality, quantity and price, conditions that have to be accepted by the producers. Therefore they have seen suitable to produce cheese in an artisanal way; paria type cheeses, which are made from cow's milk, are semi-hard, yellowish and have a mild flavor.

It is an important economic activity in the south of the country, and has been given relevance in different regions of the coast, turning into an alternative to generate a major profitability for the producers, giving the product a greater added value.

This is the origin of the problem of artisan producers of dairy products to be able to determine the unit costs of the goods to be produced. The lack of an adequate cost system makes it difficult to control the resources used in production, which increases the costs and the low profitability that is obtained [3]. In the case of Prolac Aymara, it is necessary to know the main activities to be carried out, as well as to know the elements of the cost involved in production, to optimize the use of resources, produce quality goods at low prices, making exploitation more profitable and sustainable.

The research poses a current problem, because for the cottage industry it is essential to determine the costs incurred in the production of one kilogram (Kg) of cheese, establish the sale price and being able to determine the utility.

The objective is to propose the standard cost system for artisanal cheese producers to correctly determine their production costs and obtain quality products, which allows them to place them on the market, at a higher price and be preferred to those of the competition, optimizing the benefit.

The research consists of four parts: The first will be the introduction. The second is based mainly on observation, review of different articles and excellent research on the subject. The third one presents the descriptive, explanatory and documentary methodology, as well as the bibliographic review.

In the fourth part, the results of the investigation are considered. Finally, I present the conclusions that were reached as a result of the research carried out and the bibliographical references.

2. Theoretical frame

2.1. Production of milk, cheese and butter

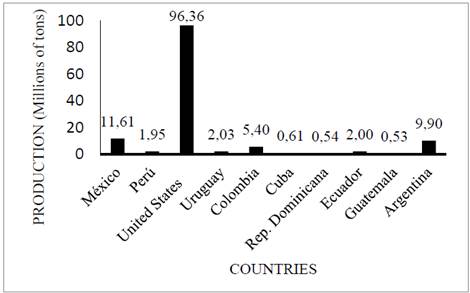

On a global scale, the first producer of milk is the United States of North America, followed at a distance by Argentina and Mexico, as shows in Fig. 1.

In Peru, cattle represents one third of livestock production, with 80.00% in the south and in the jungle, in extensive or semi-intensive production systems and 20.00% in the coast in an intensive way [1]. In addition, the country has different ecological levels, with different pastures and breeds of cattle, which makes the physical chemical composition of milk different in each of the regions [18].

In the first decade of this century, there were 850,000 agricultural units with dairy cattle that were assigned to the dairy basins, 80.00% to the formal industry and in other areas, 100.00% to the cottage industry [20]. Regarding the concentration of milk production in Peru, it is in the hands of small, medium and large producers [8], and the increase in productivity is mainly achieved by the advance in feeding and the genetic improvement of livestock production.

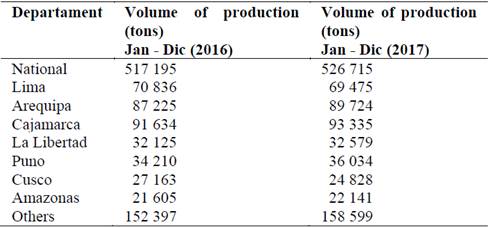

The Table 1 shows the volume of milk production per region in the years 2016 and 2017 with Lima, Arequipa, Cajamarca, La Libertad and Puno standing out. On the other hand, the big milk industry is located in three main basins, which have lately been extended in La Libertad and Lambayeque and it is formed mainly by three big companies: Gloria, Nestlé and Laive [21].

Table 1. Production volume of milk according to region 2,016 - 2,017 (to the second quarter of each year).

Source: [22]

As for the production of milk derivatives, they discovered that out of milk they could obtain its derivatives; and the same way, as they were experimenting and investigating, they have developed a variety of products (cheeses, butter, yogurt, sweets, etc.) [7]. Dairy products are the derivatives that are obtained by means of any milk processing. The diversity of products changes from region to region and among countries, according to the feeding habits, the available technologies of milk processing, the market demand, and the social and cultural circumstances [2].

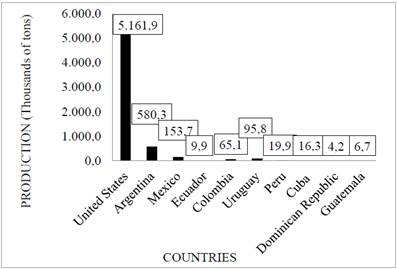

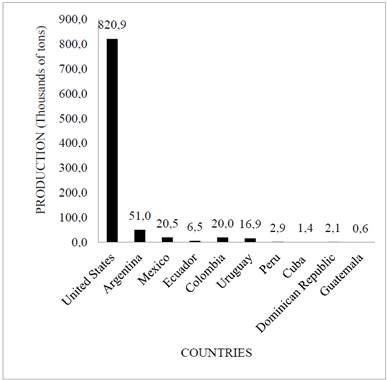

In Fig. 2, cheese production on a global scale, and in Fig. 3, butter production on a global scale, it shows that they emphasize countries as the United States of North America, Argentina and Mexico, Peru located in the seventh place. Therefore, the consumption of milk derivatives in the country is low: 0.24 Kg/hab/year in cheeses, while in Argentina, the United States, etc. it is 10.53 and 12.79 respectively. In butter 0.06 Kg/hab/año, being higher in other countries. (DairyWorld Markets and Trade, USDA, 1997). So, it is important to increase production for the benefit of the consumption of the population [9]. At the same time, the craft production of dairy products reaches volumes of (43.00% of the production of national fresh milk. In Lima, about 50.00% of the consumed cheeses are handmade and come from different regions [20]. It is called 'artisanal', the process by which the producers themselves turn the milk into finished products such as cheese and sell them in the same plant to traders or transfer them to markets in different regions of the country.

For the production, it is fundamental the hygienic quality of the milk and its derivatives, cheese, among them, for being the one of greater popular consumption. In accordance to the Peruvian Technical Norm (NTP) 202.09, fresh cheese is the product without maturation. In this sense, in the making of cheese, it is necessary to use milk of healthy cows, adequate fat, observe good hygienic practice (BPH) and milk submitted to a process of pasteurization [4,11]. Nevertheless, in Peru, the cheese is generally |prepared with milk without pasteurization, which “is an effective method to eliminate harmful bacteria that may exist in milk, but it is not 100.00 % effective” [12,15].

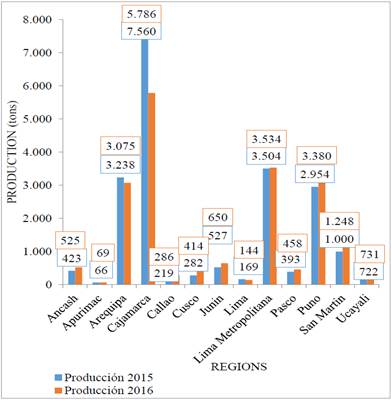

Fig. 4, cheese production by region, shows that the cheese production for the year 2015 is 21,395 tons and for the year 2016, it registers a decrease to 20,777 tons; likewise in both years it is appreciated that Cajamarca, Lima, Arequipa and Puno stand out.

2.2 Process of artisanal production of cheese and butter

In the process of production of cheese and butter the performance of the following tasks is seen: First, it is necessary the reception of milk for the production of cheese, then the normalization, pasteurization, addition of rennet, curdled, salty, court of the curd, Remove the serum, molded, mold release, maturation and sent to the warehouse for sale.

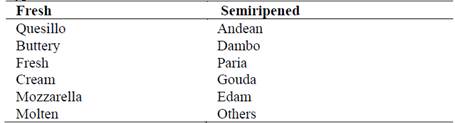

In Peru, there exist regions that produce different varieties of cheese, nevertheless, the best known are: fresh cheese, paria, andean, dambo, gouda and others, as shows in Table 2.

Paria Cheese, original from the highlands and the south of Peru, fresh, pale yellow in color, with particular characteristics of the area, milk quality, treatment in the production, confer specific characteristics. Fresh cheese is the one consumed without ripening process; its consumption is higher, due to its low cost, its nutritional characteristics and habits of consumption [20]. For the present research I have taken as a case the production of handmade cheese called Paria type.

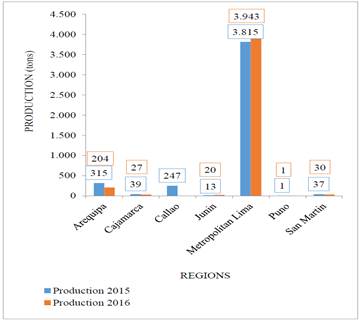

With regard to the butter production, it is very low in the country. In 2,015 the production was 4,527 tons, and in 2016 it was 4,276 tons. Once the curd has been obtained to produce cheese, the liquid part, which still contains grease, remains, from that moment the whey can go through a new production process to obtain the cream with which you proceed to prepare the butter.

Fig. 5 shows that the butter production, it is very low in the country, the year 2,015 was 4,527 tons and the year 2,016 was 4,276 tons.

2.3. Costs of standard production

With regard to costs of production, today at world level it is trying to become competitive, i.e. produce quality goods at low cost. I define the cost of production also called in production as the sacrifice of resources needed to produce a good or service, therefore, the producer relates the income obtained at the price of the goods sold and the cost of manufacture. In the same sense, the production cost is generated in the process of transforming the raw material into completed products [2].

In the goods production cost is generated, the same one that must be kept as low as it may be possible; the difference between the revenue for sales and the cost of production indicates the gross profit of the producers. In this sense in the process of making goods resources that are known as elements of the cost are needed, that is to say, those that are necessary to establish the cost of producing an article, these are 3: Direct raw material (M.P)., direct labor (M.O)., indirect costs of manufacture (C.I.F). [10].

On the other hand the productive process in the agricultural sector, as it has already been said is different to other industrial sectors, it considers the work that transforms the raw material, with the employment of labor to produce goods that will help meet the demand of the market.

Concerning the costs of production, they have different classifications according to the author consulted [14]. However, as can identify each one of them in the productive process cost elements are classified into: direct costs, when they can be identified in the product, indirect costs, when involved in the productive process but could not be identified in the product.

Inside the cost systems there exist, the predetermined costs: They are those that are calculated before the production process, they are of two types: Standard costs; they are the most exact and they are calculated mathematically or by means of observation; dear costs, they are those who are calculated by the experience, in many cases approaches are alone, as it itself they have error margin and therefore they are not the most appropriate, consequently its use is not advisable. The standard cost calculation represents that the costs should be under an achievable performance [5]. There are carefully predetermined costs and help to the managerial control.

The standard cost system, it is recognized extensively, it allows to plan and control all the necessary activities that must be realized in the companies, for the purpose of maximizing the results of the producers. On having been calculated mathematically according to the needs for every organization, it can be used in the different economic sectors, from there that is the most used one by the industrial enterprises on a global scale. Being a tool of accounting widely used throughout the world. Studies in developed countries have shown rates of use of this system, 73.00% in the UK and 86.00% in Japan. The changes calculated by the standard pricing between the actual costs incurred in the production process with the costs absorbed by the standard applied, generate variations [6].

Variations or deviations can be positive or negative; the positive occur when you have lower costs to those considered in the standard; and negative are the opposite, i.e., when the standard does not cover the costs that have occurred. The deviations are generally minimal, and therefore, it is necessary to update the standards whenever it is necessary, since they allow the owners or the management to realize periodic comparisons of the standard costs with the real costs, in order to correct the shortcomings. This cost calculation by the benefit that it offers is applied for any cost system, being already for orders of work or for processes.

With regard to the marketing of products there is the formal and informal market, the market puts the price in the sector, the same affects the usefulness of the producers. The supermarkets are supplied by industry formal, in both, the plaintiffs of the lowest income are attended by transformers craft [13].

3. Materials and methods

3.1. Location

For the research it has been taken the case of PROLAC AYMARA, which is a producer and gatherer of milk to produce artisan Paria type cheese Prolax Aymara make, which is located in the town center Thunco district of Acora, province and department of Puno, at an altitude of 3867 masl. (Meters above the sea level); the climate has a very rainy weather from October to March and intense cold in winter from May to August; activities in the agricultural sector have specific characteristics.

3.2. Sources of information

A set of procedures, reasoned tactics and remarks shaped by the scientific method have continued to achieve the stated objective, it has been determined the standard of the cost of the cheese and butter. Proceeding to collect theoretical and practical knowledge of the primary and secondary sources, then processing it for the respective description and analysis. In the study analytical, descriptive and explanatory methods have been used.

The main skills used in the investigation are; observation, the application of this practice allowed to know about direct form and in detail the operative part of the Cheese Plant as for times, employment of materials, forms, methods, step procedures, and other necessary activities in the cheese making; also; bibliographical review, investigations and articles considering the relevance and importance of the information about the topic: Documentary analysis was applied to this practice to analyze sources as notebook of notes, reports of production and others handled by the producer regarding an average month, to propose the application of standard costs for the production of handmade cheese type paria, optimize prices and the utility of the producer may be generalized the model to the other manufacturers. Finally table summaries complementing the part quantitative research have been done.

4. Results

The milk is a highly perecible product, that is why every day, as the case may be, it is old or is assigned to the production of derivative goods; a strong tendency being observed at present on the part of the producers to produce products with added value such as: Paria type cheese, butter and others; for which it is necessary to identify the elements of the cost that intervene, and to be able to apply the system of costs of standard production, so that they are the most suitable, fact that can be observed in the Fig. 6.

The default costs include standard costs (*) and estimated costs (**).

(*) The standard costs are set before the start of the production; by its accuracy are the most used at present by industrial enterprises in most of the economic sectors. (**) The estimated costs are not the most appropriate; therefore they should not be taken into consideration.

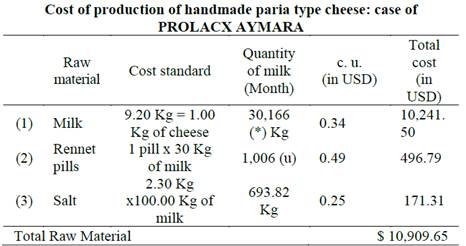

In the production of 1.00Kg of cheese type paria, the standard for the raw material, in this case the milk, will depend on the quality, the same that is related to the race and the type of feeding of livestock. The most widespread breeds of cattle in the country are the creole; Holstein Frissium and Brown Swiss or Brown Swiss. To obtain 1.00 Kg of paria type quality cheese, 9.20 Kg of milk are used, to the current market price of $0.34; other direct materials are the rennet or pills to cut milk, depending on the type of product, one for every 30.00 Kg; and 2.30 Kg of salt for 100.00 Kg of milk.

With regard to the indirect cost of manufacture, it is composed of all that is necessary for the production: such as water, electricity, fuel, depreciation and other.

In the butter production there exist two ways of obtaining it: the first one, is skimming the milk, in which case the milk does not lose its white color, the only thing that suffers is a decrease of the fat, then this same are processed in order to obtain the cheese, proving the product obtained with less fat, i.e. the light cheese. The second form: first, the milk is processed to obtain cheese, the whey remains like by-product, which is sent to the skimmer to obtain the cream or skin that still remains, in a small quantity in the whey, to obtain the butter. The process followed in the manufacture is similar in both cases. The final serum is sent to the livestock feed. In this way nothing is lost and in turn it prevents waste that may cause pollution to the environment.

When you remove the cream from the milk using the electrical cream remover, for every 15.00 Kg of milk it takes 4 minutes and you get 0.50 Kg of butter. For the second case, that is to say when removing the cream from the serum: per 100.00 Kg of serum it takes 30 minutes and 0.80 Kg of butter is obtained.

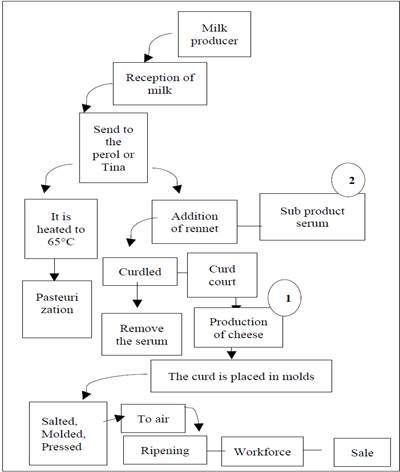

In the production of cheese and butter, the following process, see Fig 7.

In the case of artisanal production of paria type cheese, the process is performed with natural procedures and follows the following process: for the production of cheese, the milk in the best conditions is received, i.e. prior standardization with which to control the quality considering the color, acidity and fat; then it is sent to the perol or tina in which before the warming up it is pasteurized to 65ºC, which allows you to delete microbes in the milk, with the purpose of obtaining quality products for human consumption. Immediately, it is cooled to 38ºC - 45ºC, you add calcium chloride that can have been lost, you add the rennet or synthetic (chemical) to cut the milk and obtain the curd and separation of whey.

It then proceeds to cut the curd that is the solid with sharp instruments, to give rise to its separation of whey, which is the liquid. The same one settles, occurs the remove of serum; to the curd, adds salt in proper proportion 2.30% with which you will get the main product cheese and the byproduct serum to you can give different uses.

(l) Production of cheese; cut the curd, is then sent to a molded, that is the process where in a suitable table for this purpose , placed the curd in molderas, with a capacity of 1.00 Kg, then proceeded to its pressing, to give greater consistency, solidity and delete or squeeze the serum that still had the curd. Finally withdrew the moldera sends the product to the room of maturation and/or warehouse with cheese ready for sale.

To determine the standard cost of production paria type cheese the following procedure is followed, see Table 3.

(*) It is the average total milk per month, according to daily report, due to that from day to day there are small variations in production and therefore in the reception.

RM = Milk + Rennet pills + Salt

The total cost of raw material is given by the sum of milk, rennet and salt value.

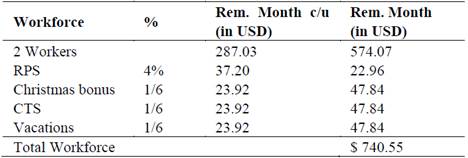

Workforce = Remuneration (2 workers) + RPS + Christmas bonus + CTS + Vacations

According to Table 4, the total cost of labor is obtained from the remuneration of the personnel plus the labor benefits.

PROLAC AYMARA has two permanent workers subject to the benefits of law: scheme of health benefits (RPS), compensation for service time (CTS), bonuses and holidays.

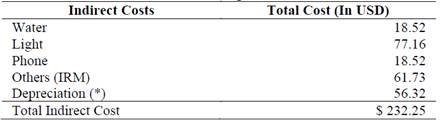

(*) The depreciation is calculated based on the goods used as the production like cooking pot, blowpipe, table and others.

Indirect production costs = Water + Light + Phone + Depreciation + Others

According to Table 5, Water, electricity, telephone, depreciation and others are added to have the total cost of indirect production costs.

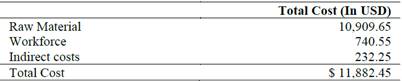

The Table 6, it is obtained from the sum of the three previous elements.

Total Cost = Raw Material + Workforce + Indirect Costs

Calculation of the entire production of cheese

P. T. = 30, 166.00 Kg de leche / 9.20 Kg = 3,279.00 Kg

Total production of cheese = Liters of milk / Standard milk cost

For the total paria type cheese production per month, 30,166.00 Kg of milk were processed. Of 9.20 Kg. of milk for each Kg of cheese, 3,279 Kg is obtained.

Determination of the margin of utility.

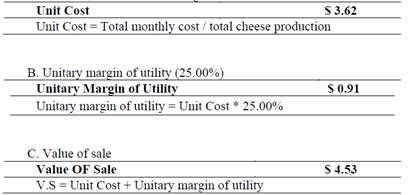

A. Calculation of the unit cost:

U.C. = $ 11,882.45/ 3,279.00 Kg

(2), Obtained the cheese, stays the by-product whey that is approximately 85.00% - 90.00% of the milk that I deposit to the production process, contains still a small fat quantity, can be submitted to a new process or be sent for the food of the cattle. In case of processing this one it will be sent to the machine, to obtain the cream with which the butter is prepared, staying the part liquidates whey; the cream allows to ripen for two days; seguidamente it is sent to the mixer and salted then to happen to the molded one and packing or packed and the revenue to the store for its sale. In the case in study PROLAC AYMARA does not produce butter and send the by-product whey to the cattle for consumption.

5. Conclusions

At present, there is a strong tendency of the milk producers to produce dairy products, so the problem of determining their costs arises. In this regard, the standard costs permit to have a better control of the activities of the productive process determining in advance the costs of artisan production of cheese, to optimize the use of resources, improve production, so appropriate pricing when making the exploitation is more profitable and sustainable.

It is essential to determine the costs of standard production and that these are as low as possible, which allows login to markets with high quality products, at a competitive price. For the case of PROLAC AYMARA. The cost of production of 1 kilogram of cheese is $ 3.62 considering a profit margin of 25.00%. The sale value is $ 4.53.

For many producers by the small amount of milk produced, the difficulty of access to the channels of communication or by the low price of milk the only alternative is to produce quality cheese, being an important economic activity for enhancing its usefulness.

The Paria type cheese characterizes the current production of cheese in the country, allows giving a higher added value to the milk and creates jobs, aspects that improve the economy and quality of life of many producers.