Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkCuadernos de Administración

Print version ISSN 0120-3592

Cuad. Adm. vol.26 no.47 Bogotá July/Dec. 2013

The value of proactive environmental strategy: An empirical evaluation of the contingent approach to dynamic capabilities*

El valor de la estrategia ambiental proactiva: una evaluación empírica del enfoque contingente de capacidades dinámicas

O valor da estratégia ambiental proativa: Uma avaliação empírica do enfoque contingente das capacidades dinâmicas

Carlos Eduardo Moreno**

Juan Felipe Reyes***

*Este artículo es resultado de un proyecto de investigación titulado "Validación y aplicabilidad de la teoría Visión de la Empresa Basada en los Recursos Naturales para el caso de las MiPyMes colombianas", realizado de junio de 2008 a enero de 2011 por el Grupo de investigación en Productividad, Competitividad y Calidad de la Universidad Nacional de Colombia. El artículo se recibió el 13-08-13 y se aprobó el 09-10-13. Sugerencia de citación: Moreno, C. E. y Reyes, J. F. (2013). The value of proactive environmental strategy: An empirical evaluation of the contingent approach to dynamic capabilities. Cuadernos de Administración, 26 (47), 87-118.

**Doctor en Ciencias del Medio Ambiente, State University of New York, College of Environmental Sciences and Forestry, Syracuse, New York, Estados Unidos, 2004; Especialista en Ingeniería Ambiental, Universidad Industrial de Santander, Bucaramanga, Colombia, 1999; Ingeniero Industrial, Universidad Industrial de Santander, Bucaramanga, Colombia, 1995. Profesor Asociado, Departamento de Ingeniería de Sistemas e Industrial, Universidad Nacional de Colombia, Bogotá, Colombia. Pertenece al grupo de investigación Competitividad, productividad y calidad. Correo electrónico: cemorenoma@unal.edu.co

***MSc. Ingeniería Industrial, Universidad Nacional de Colombia, Bogotá, Colombia, 2011; Ingeniero Industrial, Universidad Nacional de Colombia, Bogotá, Colombia, 2008. PhD Student, Departament of Business Administration, Aarhus University, Aarhus, Dinamarca. Pertenece al grupo de investigación CORE: Change, Organisational Renewal and Evolution. Correo electrónico: jfreyesr@unal.edu.co

Abstract

The authors propose and test an explicative model for organizational environmental competitiveness. In doing this, they integrate insights from the dynamic capabilities perspective, contingency theory, and the natural resource-based view of the firm. The study evaluates whether perceived uncertainty in the business environment moderates the relationship between a dynamic capability of proactive environmental strategy and competitive advantage, drawing from survey data from 129 firms in Bogotá, Colombia, and using a partially constrained approach to structural equation models of latent interaction. Results suggest that both, perceived uncertainty on customer preferences and changes in the environmental strategy of competitors, and perceived uncertainty on environmental resources and services, moderate the relationship between process and product-related environmental practices and cost advantage.

Keywords: Contingent approach, dynamic capabilities, competitive advantage.

JEL classification: C83, L21, M19.

Resumen

En este artículo se prueba un modelo que explica la competitividad entorno organizativo. Con este fin, integra conceptos del enfoque de capacidades dinámicas de la teoría de la contingenciay de la visión de la empresa basada en los recursos naturales. Se evalúa la hipótesis de que la incertidumbre percibida en el entorno empresarial modera la relación entre la capacidad dinámica de la estrategia ambiental proactiva y la ventaja competitiva, empleando datos de una encuesta a 129 empresas de Bogotá y un enfoque parcialmente restringido de los modelos de ecuaciones estructurales de interacción latente. Los resultados indican que la incertidumbre percibida acerca de las preferencias de los clientes y de los cambios en la estrategia ambiental de los competidores y acerca de los recursos y servicios ambientales moderan la relación entre procesos y prácticas ambientales relacionados con el producto y la ventajas de costos.

Palabras clave: Enfoque contingente, capacidades dinámicas, ventaja competitiva.

Clasificación JEL: C83, L21, M19.

Resumo

Neste artigo, prova-se um modelo que explica a competitividade em um ambiente organizativo. Com esse objetivo, integra conceitos do enfoque de capacidades dinâmicas, da teoria da contingência e da visão da empresa baseada nos recursos naturais. Avalia-se a hipótese de que a incerteza percebida no ambiente empresarial modera a relação entre a capacidade dinâmica da estratégia ambiental proativa e a vantagem competitiva, ao empregar dados de uma pesquisa a 129 empresas de Bogotá e um enfoque parcialmente restringido dos modelos de equações estruturais de interação latente. Os resultados indicam que a incerteza percebida sobre as preferências dos clientes e as mudanças na estratégia ambiental dos competidores e sobre os recursos e serviços ambientais moderam a relação entre processos e práticas ambientais relacionados com o produto e a vantagem de custos.

Palavras-chave: Enfoque contingente, capacidades dinâmicas, vantagem competitiva.

Classificação JEL: C83, L21, M19.

Introduction

Corporate approaches to the management of environmental issues have gravitated around two strategies: Merely complying with environmental laws and regulations, and moving from beyond compliance to a more proactive approach (Hunt and Auster, 1990; Roome, 1992; Aragón-Correa, 1998; Sharma and Vredenburg, 1998; Klassen and Whybark, 1999; Bowen et al., 2006; Aragón-Correa et al., 2008). While intervention choices in the former are often driven by environmental regulations that prescribe specific technologies and processes, the latter involve firm initiatives based on managerial discretion and the interpretation of environmental issues as opportunities (Aragón-Correa and Sharma, 2003).

Within the resource-based perspective on corporate environmental strategy (Hart, 1995; Buysse and Verbeke, 2003), simultaneous and sustained investments in resource domains are manifested in the firm's environmental pro activity. In his extension of the original resource-based view on corporate strategy (Barney, 1991; Amit and Shoemaker, 1993, Hart, 1995) argues that competitive advantage is derived through the firm's relationship with its natural environment. Consequently, the extant literature has focused on studying the effects on competitiveness of two environmental strategies, namely pollution prevention and product stewardship (Hart and Dowell, 2011).

Since Roome (1992), pollution prevention has typically been associated with continuous improvement and innovation (i.e. Total Quality Management: TQM). Synergies may exist between waste prevention and Lean Manufacturing (King and Lenox, 2001; Rothenberg et al., 2001; Zhu and Sarkis, 2004; Harrington et al., 2008; Yang et al., 2011). Pollution prevention strategies require companies to develop resources, such as physical assets, the technologies and skills required to use these resources, organizational learning, and cross-functional integration (Russo and Fouts, 1997). Complementary, a product stewardship strategy (Hart, 1995; Christmann, 2000; Vachon et al., 2001) entails integrating stakeholder perspectives that represent the voice of the environment into product design and development (Buysse and Verbeke, 2003). Thus, the process-centered focus in the optimization of environmental factors is broadened to include the entire supply chain of products (Seuring, 2004; Linton et al., 2007), which makes product stewardship an area of study that can be closely linked to green supply chain management (Sarkis, 2012; see Zhu and Sarkis, 2004).

It was not until Aragón-Correa and Sharma (2003) that proactive environmental strategy was seen as a dynamic capability. Following Eisenhardt and Martin's (2000) definition of dynamic capabilities, they demonstrate that proactive environmental strategy is dependent on specific and identifiable processes, is socially complex and specific to organizations, requires the path-dependence and embeddedness of specific capabilities (see below), and is non replicable or inimitable (Aragón-Correa and Sharma, 2003, p. 74). In addition, Aragón-Correa and Sharma (2003) suggest that dynamic capabilities are contingent on both environment dynamism and on managers' interpretations of their business environment (Ambrosini and Bowman, 2009). Their propositions imply that aspects of the firm's external environment, such as state uncertainty, complexity, and munificence, affect the development of a proactive environmental strategy and also the firm's ability to profit from such strategy (Hart and Dowell, 2011, p. 1473).

The dynamic capability perspective has had a significant impact on research regarding organizations and the natural environment (Hart and Dowell, 2011). Most of the research conducted until now (e.g., Rueda-Manzanares et al, 2008; Sharma et al, 2007; López-Gamero et al, 2011a) has explored the first branch of Aragón-Correa and Shar-ma's (2003) propositions, which relates to understanding how external contingencies affect the firm's deployment of capabilities and resources to develop a proactive environmental strategy. In contrast, less effort has been given to exploring the second branch of Aragón-Correa et al.'s (2003) propositions, which concerns the assessment of the net benefit of proactive environmental strategy in the context of the competitive environment in which the firm is embedded (Hart and Dowell, 2011, p. 1473; Ambrosini and Bowman, 2009, p. 40).

In this article, we draw from the theoretical framework proposed by Aragón-Correa and Sharma (2003) in particular, and from the dynamic capabilities and environmental strategy literature in general, to empirically test an explicative model of environmental competitiveness (Wagner and Schaltegger, 2004) that corresponds to the contingent (moderation) perspective on dynamic capabilities. Hence, after reviewing the relevant theoretical approaches and state of the art, we derive hypotheses from the theory, op-erationalize constructs such as proactive environmental strategy, perceived environmental state uncertainty, and environmental competitiveness, evaluate the reliability and validity of such measures, and test these hypotheses through structural equation models of latent interaction effects. This article ends with a discussion of results and some propositions for future research.

1. Theoretical foundations and research hypotheses

1.1. Dynamic capabilities and environmental management

Proactive environmental strategy is defined as a pattern of corporate practices beyond the requirements of environmental regulations and standard actions aiming to reduce the environmental impact of operations (Sharma, 2000; Aragon-Correa and Sharma, 2003). A growing literature has been concerned about the implications of proactive environmental strategy on competitive advantage (Hart, 1995; Sharma and Vredenburg, 1998; Christmann, 2000; López-Gamero et al, 2009). The majority of these studies are theoretically driven by the Resource-Based View of the firm (RBV) (Wernerfelt, 1984; Barney, 1991), and particularly, its extension to the natural environment (Hart, 1995). This means that the research has predominantly followed an endogenous perspective because the aspects of the external business environment are not considered.

A conceptual contribution that addresses this issue characterizes proactive environmental strategy as a dynamic capability (Aragon-Correa and Sharma, 2003). Dynamic capabilities are proposed as an extension of the RBV in order to stress the exploitation and reconfiguration of firm-specific resources to address changing environments (Teece et al, 1997, p. 510). Dynamic capabilities are defined as "the firm's processes that use resources —specifically the processes to integrate, reconfigure, gain and release resources— to match and even create market change" (Eisenhardt and Martin, 2000). Furthermore, dynamic capabilities have the ability to confer competitive advantage given their path dependent histories (Teece et al, 1997) and idiosyncratic processes (Eisenhardt and Martin, 2000).

Aragón-Correa and Sharma (2003) take the characteristics of dynamic capabilities to support their view of proactive environmental strategy, arguing that a proactive environmental strategy is therefore "tacit, casually ambiguous, firm specific, socially complex, path dependent, and value adding for consumers, [and it] may provide a competitive advantage" (Aragon-Correa and Sharma, 2003, p. 74). We also support this argument as follows.

First, a proactive environmental strategy is able to confer improvements in competitiveness and performance (Hart, 1995; Russo and Fouts, 1997; Sharma and Vredenburg, 1998; López-Gamero et al, 2009). That is, when a proactive environmental strategy focuses on process development and efficiency, the firm is able to reach cuts in terms of costs as waste is reduced and operations are optimized (Klassen and Whybark, 1999; Christmann, 2000; González-Benito and González-Benito, 2005). On the other hand, practices towards product/service stewardship enable firms to explore new markets and differentiate from competitors (Reinhardt, 1998; Maas et al, 2012) as well as reaching a higher reputation (Gilley et al, 2000).

Second, the details of a proactive environmental strategy are specific to the particular firm, which indicates the idiosyncrasy of such dynamic capability (Aragon-Correa and Sharma, 2003). As managers are responsible for the implementation of strategies, the extent to which a proactive strategy is deployed depends upon how managers interpret the natural environment (Sharma, 2000). That is, the uniqueness of a proactive environmental strategy is determined by the particular interpretation of environmental issues as opportunities or threats (Sharma, 2000) as well as the perceived level of impact of environmental constituencies (Banerjee, 2001). Depending on the managerial interpretations, managers are able to influence in different ways the resource allocation and decision making so as to convert pressures into effective actions to deal with the natural environment (Bansal and Roth, 2000; Colwell and Joshi, 2013).

Third, a proactive environmental strategy can be understood as a dynamic capability that is path dependent as the firm has followed a trajectory of competence development (Teece et al, 1997). By following such a developmental trajectory, the firm has accumulated the necessary resources to move from merely reactive and compliance-oriented, to more proactive approaches (Hunt and Auster, 1990; Roome, 1992).

Fourth, as a dynamic capability, a proactive environmental strategy requires the complex integration and configuration of a series of tacit resources and capabilities (Aragon-Correa and Sharma, 2003). Particularly, the focus on pollution prevention of a proactive environmental strategy "builds within a firm the resources of organizational commitment and learning, cross-functional integration, and increased employee skills and participation" (Russo and Fouts, 1997, p. 539). A dynamic capability of proactive environmental strategy is able to integrate, re-configure and re-combine those resources and capabilities (Aragon-Correa and Sharma, 2003). Furthermore, a proactive environmental strategy allows firms to develop new resources (López-Gamero et al, 2009). The literature suggests the association of a proactive environmental strategy with competitive valuable environmental capabilities, such as shared vision, continuous improvement and stakeholder integration (Hart, 1995; Sharma and Vredenburg, 1998), as well as process innovation and implementation (Christmann, 2000). The complexity of a proactive environmental strategy is also given by its integration into the strategic planning process (Judge and Douglas, 1998), administrative, entrepreneurial and technical dimensions of the firm (Aragon-Correa, 1998).

Some empirical verification subscribed to the dynamic capabilities approach in the context of environmental management has been advanced in the literature. Menguc et al. (2010) argue that a dynamic capability of proactive environmental strategy not only is characterized by the aggregation of pollution control measures but it also implies top-management support. It emerges as a response to the pressures from environmentally sensitive customers and exerts a positive influence on firm performance (Menguc et al, 2010). They also found that a proactive environmental strategy as a dynamic capability builds on the entrepreneurial orientation of the firm, and this relationship is stronger at higher levels of regulatory pressure (Menguc et al, 2010).

The dynamic capabilities approach has been evidenced as a mechanism to improve environmental performance. Judge and Elenkov (2005) characterize a dynamic capability of organizational change arguing that the pursuit of goals towards environmental performance requires adaptability and innovative-ness. Similarly, based on a case study, Wu et al. (2012) suggest that the dynamic capability for strategic change towards sustainability is a multidimensional construct that entails scanning, identification and reconfiguration capabilities.

Empirical studies also approach path-dependencies of dynamic capabilities in environmental management. Russo (2009) explores how dynamic capabilities influence the ability to improve environmental performance, which leads him to argue that "the creation and deployment of environmental management skills would appear to be a prime example of the development of a dynamic capability" (Russo, 2009, p. 308). In particular, the study approaches the path-dependent learning processes that characterize environmental management as a dynamic capability. Path-dependent learning is manifested through "efficiencies dealing with waste handling in a routinized fashion, in conducting and responding to audits in recognizing and prioritizing possibilities for improvement" (Russo, 2009, p. 310). In a similar vein, Zhu et al. (2013) explore path-dependencies in dynamic capabilities for environmental management systems and total quality environmental management in terms of learning from the experience with other organizational systems such as ISO 9000.

1.2. Environmental management and competitive advantage

The dynamic capabilities perspective is an integrative approach to understand sources of competitive advantage (Teece et al., 1997). As we supported that a proactive environmental strategy may be understood as a dynamic capability, it has the ability to impact the resource base of a firm to safeguard competitive positioning (Hart, 1995; Aragon-Correa and Sharma, 2003). Particularly, a proactive environmental strategy is characterized by pollution prevention and product stewardship approaches (Hart, 1995; Sharma and Vredenburg, 1998). Pollution prevention affords opportunity for sustained competitive advantage through the accumulation of tacit resources embedded in large numbers of people (Hart, 1995, p. 1000). On the other side, product stewardship affords a firm the opportunity for sustained competitive advantage through the accumulation of socially complex resources involving fluid communication across functions, departments, and organizational boundaries (Hart, 1995, p. 1001). The literature has suggested the term "eco-competitiveness", referred also as environmental competitiveness or eco-advantage (Esty and Winston, 2006), and understood as the share of the overall competitiveness of the firm, which can be influenced by environmental management activities (Wagner and Schaltegger, 2004).

The contribution of a proactive environmental strategy to such eco-competitiveness has been studied in terms of costs and differentiation (Lopez-Gamero et al., 2009). As Shrivastava (1995) has shown, in the input system, competitive advantage from environmental technology appropriation stems from materials and energy conservation. In the throughput system, manufacturing for the environment improves production efficiencies and minimizes waste and pollution, which is important both for the company's image and to minimize environmental liabilities. Thus, cost savings relative to competitors result from reducing costs of implementing regulations as well as the avoidance of installing and operating end-of-pipe solutions since the firm engages in continuous total quality environment management programs rather than control mechanisms (Hart, 1995; Sharma and Vredenburg, 1998). Empirically, Christmann (2000) finds support for the association between a firm's use of pollution prevention technologies and the cost advantage it gains from a proactive environmental strategy.

On the other hand, the pollution prevention approach of a proactive environmental strategy has the potential to improve employee morale and labor productivity (Klassen and Whybark, 1999; Ambec and Lanoie, 2008).

Hence, costs of recruitment, turnover and absenteeism are subject of reduction (Ambec and Lanoie, 2008). Additionally, a proactive environmental strategy implies strong managerial practices that allows a firm to meet the requirements of the regulations that are applicable (Bansal and Hunter, 2003). That results in additional cost savings as there are better relationships with the regulator and other stakeholders, which are reflected in less frequent environmental inspections from the regulation, and fewer fines and penalties that could take place (Bansal and Hunter, 2003; Lo et al, 2012).

Similarly, the differentiation advantage may arise from higher revenues that are derived from meeting the customer's environmental needs through eco-design, building product position and customer loyalty on green attributes (Esty and Winston, 2006). However, while differentiation advantage typically arises from the customer's willingness to pay more for the product or service if they believe that it is more valuable, this type of advantage usually depends on the fit of the product's characteristics, the market needs and the company's ability to credibly communicate the product's environmental characteristics (Reinhardt, 1999; Galdeano-Gómez, 2008). Furthermore, differentiation benefits include legitimacy and improved corporate image that allow the firm to experience preferential treatment from customers and other stakeholders (Sharma and Vredenburg, 1998). A similar argument leads Hart (1995, p. 994) to argue that "competitive advantage might best be secured initially through competitive preemption." That is, advantage can be achieved either by gaining preferred or exclusive access to raw materials, locations, productive capacity, or customers or by establishing rules, regulations, or standards tailored to the firm's capability (Hart, 1995, pp. 994-995). Thus, through differentiation, a proactive environmental strategy allows the firm to create more opportunities for business growth, increase of sales and profit by exploring new markets "that are untapped and where competition is scarce" (Menguc et al, 2010, p. 287).

In summary, a dynamic capability of proactive environmental strategy stimulates firms to generate high margin products by implementing cutting-edge technologies which can enhance profit growth (Menguc et al, 2010). This implies the mobilization and alteration of the resource base so that the firm can realize rent generations and improved competitive position. Therefore, we formulate the following hypothesis regarding the outcome of a proactive environmental strategy: Hypothesis 1: A dynamic capability of proactive environmental strategy exerts a positive influence on the firm's competitive advantage.

1.3. The business environment as a moderator

As mentioned above, dynamic capabilities allow addressing complex and changing environments. An important argument here points to the ability of dynamic capabilities to confer competitive advantage and improve firm performance under these conditions of shifting environments (Teece et al., 1997). That is, firms face fast rates of change, unexpected discontinuities and unpredictable events that require the reconfiguration of operational capabilities else they will be eroded and become core rigidities. The development of dynamic capabilities implies "enabling and inhibiting variables within and outside the firm" (Ambrosini and Bowman, 2009, p. 46). Thus, the conditions of the external environment moderate the relationship between dynamic capabilities and firm performance (Eisenhardt and Martin, 2000; Zahra et al., 2006; Ambrosini and Bowman, 2009).

A stream of literature addresses different dimensions of the external business environment in order to understand the role and nature of dynamic capabilities, while giving special attention to characteristics of the industry. An early examination of the survival in the typesetting industry illustrates that a dynamic technical capability allows the firm to survive and adapt when confronted with radical, competence destroying technological change in the business environment (Tripsas, 1997). Subsequent research in the film industry indicates that the successful impact of dynamic capabilities on firm performance is determined by characteristics of the industry, such as the level of demand and stability of consumer tastes (Shamsie et al., 2009). Recently, Wilden et al. (2013) found that dynamic capabilities exert a positive influence on firm performance when "accounting for context dependencies" (Wilden et al, 2013, p. 87), such as the level of competitive intensity.

In summary, the understanding of how dynamic capabilities favor firm performance when addressing the external business environment is consistent with the contingency theory (Burns and Stalker, 1961). That is, competitive advantage builds on the proper alignment of endogenous variables with exogenous context variables (Lawrence and Lorsch, 1967).

Empirical research subscribed perspective evidences, the role of the business environment as a moderator is the relationship between organizational strategies and performance (Prescott, 1986; Venkatraman and Prescott, 1990; Mcarthur and Nystrom, 1991). In particular, this stream agrees upon three general dimensions of the business environment, namely uncertainty or dynamism, munificence and complexity (Dess and Beard, 1984; Boyd, 1990; Mcarthur and Nystrom, 1991).

Environmental uncertainty is defined as the perceived inability to predict the change and characteristics of the business environment accurately and the impact on organizational decisions due to the lack of sufficient information about external events (Duncan, 1972; Milliken, 1987; Lewis and Harvey, 2001). The literature discusses a variety of related terms such as dynamism, volatility, and high-velocity, which to some extent refer to the same notion of unpredictability of change (Goll and Rasheed, 2004). Ambrosini and Bowman (2009) note that as dynamic capabilities impact the resource base of a firm that result in competitive advantages, the uncertainty of the business environment determines whether these advantages are temporary or sustained. That is, "dynamic capabilities are contingent on both environment dynamism [uncertainty] and on managers' interpretations of their business environment" (Ambrosini and Bowman, 2009, p. 41). We, however, recognize that munificence, complexity, and elements of the business environment other than uncertainty are relevant in order to understand the nature of dynamic capabilities but we have not discussed them in detail since they are outside the scope of this research.

Despite the significant advancement in this field, it is concluded that more research in the contingency approach is needed to analyze internal and external contingencies in the study of dynamic capabilities (Barreto, 2010). This will certainly contribute to understand the context dependency in the competitive value of dynamic capabilities (Winter, 2003; Barreto, 2010).

In the context of environmental management, Aragón-Correa and Sharma (2003) elaborate on the contingency perspective and suggest that uncertainty, complexity and munificence influence the development of a proactive environmental strategy as a dynamic capability and the firm's ability to improve competitiveness from such a dynamic capability. Their argument leads to two sets of propositions. First, dimensions of the external business environment moderate the relationship between firm capabilities and proactive environmental strategy. Second, dimensions of the business environment moderate the relationship between proactive environmental strategy and competitive advantage.

On the one hand, concerning the first set of propositions, the extant literature suggests that firms facing uncertain business environments tend to take more risks and be more proactive. Therefore, such firms are more likely to make investments in developing the necessary resources and capabilities that lead to a proactive environmental strategy (Aragon-Correa and Sharma, 2003). This implies the consultation with stakeholders and to shape administrative processes and structures to explore innovative ways of coping with such unpredictable external changes (López-Gamero et al, 2011a). By doing such investments in resources and capabilities, firms "attempt to anticipate events and implement preventive actions rather than merely respond to events that have already occurred" (Aragon-Correa and Sharma, 2003, p. 77). Research has been particularly active regarding this area, including the empirical testing of Aragón-Correa and Sharma's (2003) propositions by Sharma et al. (2007), Rueda-Manzanares et al. (2008), López-Gamero et al. (2011a), and López-Gamero et al. (2011b).

On the other hand, in their second set of propositions, Aragon-Correa and Sharma (2003, p. 77) state that differentiated structures and integration of firms under uncertain environmental conditions allow them to "achieve stability by reducing the risk of concentrating on a single product or market segment". Along with Ambrosini and Bowman (2009), these authors claim that to the extent that a proactive environmental strategy is understood as a dynamic capability, it will then lead to competitive advantage depending on the level of perceived uncertainty in the business environment.

Empirical studies in business and the natural environment explore contingencies in the external environment. Russo and Fouts (1997) found that higher levels of industry growth make a stronger influence of environmental performance on firm profitability. They argue for the opportunities to reduce risk, the rapid maturation of a technology, and the expected organic structures to be in place under such conditions (Russo and Fouts, 1997). On the other hand, Goll and Rasheed (2004) evidenced that in more uncertain environments, social responsibility exerts a higher influence on financial performance. That is, firms seek social legitimacy that "provides them with some protection from the unpredictabilities they face" (Goll and Rasheed, 2004, p. 44). However, empirical literature that supports the moderating role of environmental uncertainty on the relationship between a proactive environmental strategy and competitive advantage remains absent. Recently, Menguc et al. (2010) studied the direct effects of environmental uncertainty on a proactive environmental strategy and firm performance, respectively. Interestingly, their results indicate that environmental dynamism exerts a negative influence on sales growth.

We thus build on the above-mentioned arguments on the opportunities that uncertain environments offer to develop innovative approaches to deal with the natural environment and achieve competitive advantage. Thus, we formulate the following hypothesis:

Hypothesis 2: Perceived uncertainty in the business environment moderates the relationship between a dynamic capability of proactive environmental strategy and competitive advantage; the higher the perceived uncertainty, the stronger the impact of a dynamic capability of proactive environmental strategy over competitive advantage.

2. Methodology

2.1. Data

Jointly with Moreno et al. (2013), data collection in this study follows a web survey strategy, using a questionnaire directed to environmental managers or their equivalent from Bogotá-based firms. At the time the survey was conducted, targeted firms were participating mostly in the first or second levels (out of five) of the "Gestión Ambiental Empresarial" (Corporate Environmental Mangament, or CEM) program. The CEM program is an assistance-and-education initiative (see Parker et al., 2009 about this type of programs in general) intended to engage firms from Bogotá in environmental improvement, and is currently developed by the Bogotá's Secretary of the Environment (http://www.ambientebogota.gov.co/). By addressing these firms in the study, we make sure that they are in the process of responding to environmental issues throughout the gradual implementation of both engineering and management practices.

The survey was directed to a pre-recruited, non-probabilistic panel (Couper, 2000) consisting of 360 potential responders. After conducting the necessary procedures for verification of the quality of the data in web-based studies (Sax et al., 2003; Gosling et al., 2004), 167 questionnaires were retained for subsequent analysis, out of 189 questionnaires completed. Next, we performed an analysis for non-response bias by comparing both responders and responses across three selected waves in a cumulative response rate function (Armstrong and Overton, 1977) for a six-month interval. We found no statistically significant differences between the re-sponders' demographics and their responses. Finally, we examined our sample to identify missing data and apply remedies accordingly (Hair et al, 2010). After analyzing missing values in homogenous blocks of variables, we excluded five cases and imputed one score for an additional case using a regression method. Thus, we retained 162 cases for subsequent analysis.

In terms of size, 33 firms (20.4%) employ 10 employees or less, -which classifies these firms as "micro-enterprises" according to Colombian law. We decided to exclude these cases from our final study sample, based chiefly on the reasons reviewed in Tilley (1999) and Mir and Feitelson (2007), namely, that voluntary action in micro-enterprises is unlikely as environmental awareness or eco-literacy are low in their owners, financial and human resources are limited, and most regulatory or voluntary initiatives require a formal environmental management structure more typical of larger firms.

In summary, our definitive sample included 129 firms: 55 (43%) firms with a number of employees between 11 and 50; 48 (37%) between 51 and 200, and 26 (20 %) with more than 200 employees. Of these cases, 100 firms (77.5%) belong to the manufacturing industry, and the remaining 29 firms (22.5%) belong to other industries, such as services and commerce (chiefly, health services, waste management, and logistic activities).

2.2. Measures

Our scale items were measured using Likert scales. The validity of the instruments was evaluated through Exploratory Principal Component Analysis (EPCA) with varimax rotation, and the usual tests (Hair et al, 2010) were performed on the factors obtained, specifically, the calculation of reliability estimates (i.e. Cronbach's alpha). Data on the items retained, their factor loadings, and the percentage of the variance explained by each factor are presented in Appendix A. Following Walls et al. (2011), we draw from the relevant literature so as to capture in our measures environmental strategy in the form of management practices, initiatives, and technologies, deriving competitive advantage from such strategy, and not from environmental performance, thus assuming that the relationship between environmental and financial performance may be explained by environmental strategy (Claver-Cortés et al., 2005).

Proactive Environmental Strategy. Eight items, adopted from Aragón-Correa (1998), Christmann (2000), Zhu and Sarkis (2004), Chan (2005), and Aragón-Correa et al. (2008), assess the degree of adoption of proactive environmental practices, initiatives and technologies, using a five-point Likert scale ("1 = we have not considered this issue at all" to "5 = we are leaders in this practice in our sector"). The EPCA analysis indicated that all items were retained in two first-order factors, which we labeled "Environmental Management Practices" (ENMP) and "Process & Product-related Environmental Practices" (PPEP) (Cronbach's alpha = 0.816, and 0.763, respectively). When these two factors are complemented with good housekeeping practices (which we did not include in our measures for proactiveness), such extended distribution of environmental practices is found to be consistent with other studies that characterize three general dimensions of an environmental technology portfolio (e.g., Klassen and Whybark, 1999; Buysse and Verbeke, 2003; Gavronski et al., 2012).

Environmental Competitiveness (Eco-Ad-vantage). Eight items, partly adapted from Sharma and Vredenburg (1998), Christmann (2000), and Karagozoglu and Lindell (2000), assess the impact of environmental management activities on costs, revenues, and differentiation opportunities through a seven-point Likert scale ("1 = very unfavorable" to "7 = very favorable"). Exploratory factor analysis showed that six of these items were retained in two first-order factors, which we labeled "Cost Advantage" (CADV) and "Differentiation Advantage" (DADV) (Cronbach's alpha = 0.695, and 0.757, respectively).

Perceived Environmental State Uncertainty. Among the three types of perceived uncertainty that are generally recognized in the literature (Milliken, 1987), we operationalize measures for environmental state uncertainty, which "occurs when managers perceive their general business environment or one of its components to be unpredictable" (Aragón-Correa and Sharma, 2003, p. 77). Seven items, adapted from Chan (2005), Kemp (1998), and López-Gamero et al. (2011b), evaluate how predictable or unpredictable may be a series of issues that might arise in the business environment of the firm in the future through a five-point Likert scale ("1 = completely unpredictable" to "5 = completely predictable"). All items were retained in two first-order factors which, following Chan (2005), we labeled "Environmental Products, Markets and Demand" (PU-EPMD) and "Environmental Resources and Services Used by the Organization" (PU-ENRS) (Cronbach's alpha = 0.863, and 0.870, respectively).

2.3. Methods

To test our hypotheses, we performed structural equation analyses of interaction effects -between proactive environmental strategy and environmental state uncertainty, in which both independent variables involved in the interaction are first-order latent constructs inferred from multiple indicators. Schumacker and Lomax (2010, p. 327) argue that while several multiple regression studies have used nonlinear and interaction effects, these effects have been rarely tested in path models. For continuous observed variables, a nonlinear relationship could exist for a product of two observed variables, and since Baron and Kenny (1986), and even before (see discussion in Baron and Kenny, 1986, p. 1174), this has been the preferred approach for testing moderation effects.

A moderator can be seen as "a qualitative or quantitative variable that affects the direction and/or strength of the relation between an independent or predictor variable and a dependent or criterion variable" (Baron and Kenny, 1986, p. 1174). Drawing from the seminal approach established by these authors, the model in Figure 1 shows how the impact of proactive environmental strategy (predictor) on competitive advantage (outcome) may vary depending on perceived environmental state uncertainty (moderator). The moderating effect in this model is captured by the interaction or product of the predictor and moderator variables.

We follow the protocol of most prior studies in treating ordinal variables with five or more categories as continuous variables, drawing from evidence that suggests that this is not likely to have a considerable practical impact on the results (e.g. Johnson and Creech, 1983). And, from among the various approaches to estimating this type of interaction effects, while noticing that "best practice is still evolving" (Marsh et al., 2012, p. 438), we estimate our models in LISREL 8.8 through the partially constrained approach (Marsh et al., 2006).

However, for purposes of preliminary analysis (see Marsh et al., 2006, p. 230), we estimate our hypothesized models in LISREL 8.8 following the latent variable approach (also known as factor score approach) to interaction effects proposed by Schumacker (2002). Here, the latent interaction variable is defined by multiplying the latent variable scores of the exogenous latent independent variables (Schumacker, 2002, p. 40).

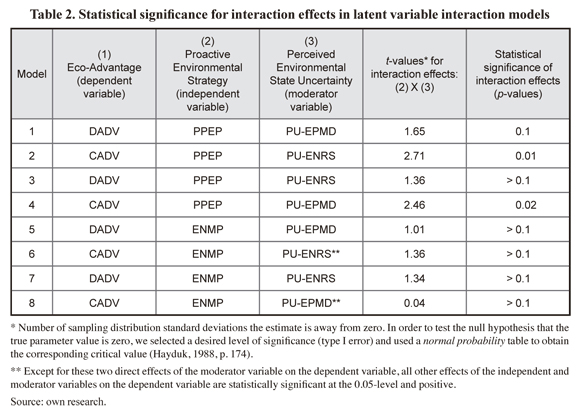

Table 1 shows the means, standard deviations and correlations for the variables (first-order factors). Table 2 presents the T-values for the interaction effects and their associated statistical significance for each of eight models that correspond to our research hypotheses. Four models (i.e., models 1, 3, 5, and 7 in Table 2) evaluate the relationship between two types of proactive environmental strategy and differentiation advantage, including the moderating effects of two types of perceived environmental state uncertainty. Complementary, four additional models (i.e., models 2, 4, 6, and 8) evaluate the relationship between two types of proactive environmental strategy and cost advantage, including the moderating effects of two types of perceived environmental state uncertainty.

Fit statistics are not shown in all models for the latent variable approach when they are just identified and therefore yield a perfect fit. All items retained in the EPCA are used to make up for the latent variables. Although we used normalized scores rather than the original data, we could not reject the assumption that a multivariate normal data distribution may be violated. Accordingly, we fit our measurement models to the normalized data using Robust Maximum Likelihood as our estimation method (Jöreskog et al., 2001).

The results show no evidence for interaction effects in any of the models that included environmental management practices. However, for all models we do observe a direct and positive effect on firm performance of the two dimensions of proactive environmental strategy. Given that our main purpose with this article is to provide an empirical verification of the contingency approach to dynamic capabilities, in the remaining we will focus on a deeper evaluation of the three models for which we have found statistical evidence (at the 0.1-level or below) through the latent variable approach for the moderating effects of perceived environmental state uncertainty on the relationship between proactive environmental strategy and competitive advantage.

As we referred already, we do so through the application of the partially constrained approach to structural equation models of latent interaction. When there are multiple indicators of constructs, latent variable approaches offer "a much stronger basis" (Marsh et al., 2012, p. 438) for evaluating the underlying factor structure and providing more defensible interpretations of the interaction effects. Also, the partially constrained approach has the advantage of relaxing the assumption of multivariate normality of the data (Marsh et al., 2006, p. 255).

We use our original survey data to estimate the effect of the interaction between proactive environmental strategy (ξ1) and perceived environmental state uncertainty (ξ2) on competitive advantage (η). Here, we follow the notation and procedure provided by Marsh et al. (2006, p. 241). In our data, the structural equation with the interaction term is:

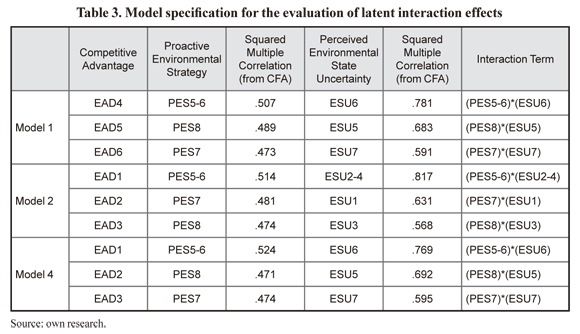

η=γ1ξ1+γ2ξ2+γ3ξ1ξ2+ζ (Equation 1)where each of the latent variables η, ξ1 and ξ2 has three indicators. The interaction term in Equation 1 is formed by matched pairs of indicators (items) according to arbitrary and non arbitrary combinations (see below). However, while each of the first-order factors for PPEP and PU-ENRS consists of four indicators, the remaining PU-EPMD factor contains three indicators.

From among several approaches available in the literature to deal with this situation, we use item parceling, which is recommended when the interest of the researcher lies in modeling relations among the latent constructs (Bandalos and Finney, 2001; Little et al., 2002). Consequently, our matched product indicators are based on single indicators from the three-item factor PU-EPMD, and two single indicators plus one item parcel in each of the factors PPEP and PU-ENRS. As noted by Marsh et al. (2006, p. 246; Marsh et al., 2012, p. 442), this strategy has the advantage of both using all the information available and do not reuse information. In determining our parcels, we follow the procedure recommended in Little et al. (2002, p. 166).

After the parceling of items in each of the factors consisting of four items, we are left with the same number of indicators (three) for the two first-order latent factors for the interaction term. This allows us to match the indicators in order of the reliabilities of the indicators (Saris et al., 2007) obtained from Confirmatory Factor Analysis (CFA) for each model, matching the items with the highest reliability from one predictor to the item with the highest reliability in measuring the other latent predictor, and so on (Marsh et al., 2012, p. 441). Brown (2006, p. 131) explains that the squared factor loading can be considered as an estimate of the indicator's reliability.

To avoid multicollinearity, we used mean-centered measures for the sets of observed indicators. The fit of our models in CFA is evaluated through the use of robust maximum likelihood statistics. For the purpose of testing our research hypotheses, the final specifications for our models are provided in Table 3. We evaluated the unidimension-ality of the sets of indicators being parceled, a condition associated with the use of item parcels in studies where the interest is centered on the structural parameters (Bandalos and Finney, 2001), finding that none of the modification indices was different than zero and none of the absolute values in the matrix of standardized residuals for the indicators being parceled was above 2.58, according to the tests suggested in Vieira (2011, p. 61).

3. Results

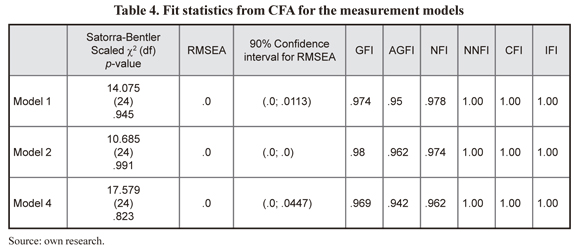

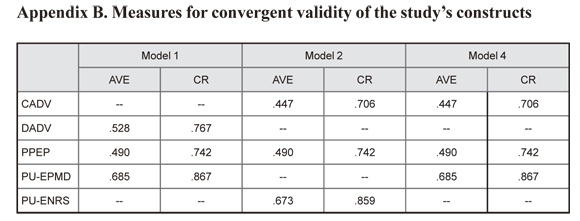

Statistics from CFA are shown in Table 4, indicating good fit for the measurement models. We evaluated the convergent validity of our measures in CFA by calculating both the average variance extracted (AVE) for the items loading on each of our constructs and construct reliability (CR). A good rule of thumb for adequate convergence would be an AVE of .5 or higher; complementary, a CR of .7 or higher suggests good reliability (Hair et al, 2010, p. 687). The values computed for the AVE and CR are shown in Appendix B and suggest adequate convergence for our constructs.

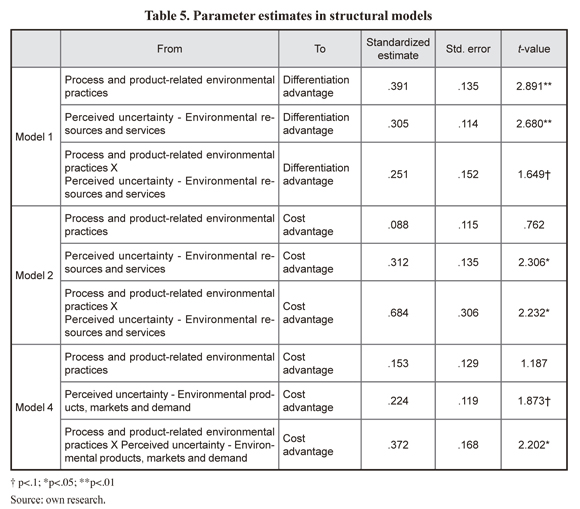

Results from the estimation of Model 1 (see Table 5) support the direct and positive effect of process and product-related environmental practices on differentiation advantage (Hypothesis 1); also, these results might suggest that a positive moderation effect exists for the perceived uncertainty of environmental products, markets and demand on the relationship between proactive environmental strategy and differentiation advantage, though this moderating effect is not fully supported by the significance level for the interaction effect. The fit indices for this model are c2 (62) = 80.009 (p = 0.0616), RMSEA = 0.0476, SRMR = 0.0686, NNFI = 0.965, and CFI = 0.967, which are indicative of good fit of the model to the data.

We observe strong evidence in support for Hypothesis 2 in Model 2, suggesting that the higher the perceived uncertainty on the environmental resources and services used by the organization, the stronger the impact of process and product-related environmental practices on cost advantage. In contrast, the direct effect of process and product-related environmental practices on cost advantage is not significant in this model. The fit indices are c2(62) = 71.569 (p = 0.190), RMSEA = 0.0347, SRMR = 0.0668, NNFI = 0.956, and CFI = 0.959, which suggests a very good fit.

In Model 4, the main effects are not statistically significant, while the interaction effect is statistically significant (p < .05), as shown in Table 5. Therefore, the higher the perceived uncertainty in environmental products, markets and demand, the stronger the impact of process and product-related environmental practices on cost advantage. We find no evidence of a significant direct effect of process and product-related environmental practices on cost advantage. The fit indices for Model 4 are c2(62) = 74.824 (p = 0.127), RMSEA = 0.0402, SRMR = 0.0685, NNFI = 0.973, and CFI = 0.974, which jointly suggest that the model fits the data very well.

4. Discussion

Our study offers evidence to support the claim that a dynamic capability of proactive environmental strategy can explain rents and competitive advantage (Teece et al, 1997; Makadok, 2001). That is, competitive benefits (e.g., gaining preferred access to customers and commanding a premium price on products) are likely to result from the development of more advanced environmental practices (see Popp, 2005) in a proactive environmental strategy, such as input substitution, process modification, eco-design, and green purchasing. While a thorough understanding of the relationship between a proactive environmental strategy and firm performance is lacking in the context of Colombian firms, interesting insights emerge from the resource-based view and the dynamic capabilities perspectives. They suggest that such advanced, environmentally proactive practices, require the adoption of a particular set of routines and operations (Aragón-Correa et al, 2008) that, in turn, depends on the complex coordination of human and technical skills (López-Gamero et al, 2009) and fluid communication across organizational boundaries (Hart, 1995), which are crucial for meeting customer environmental needs. Thus, the positive implications of a proactive environmental strategy on competitive advantage supported by our findings indicate the ability that such a dynamic capability possess so as to purposefully reconfigure and affect the firm's resource base (Zahra et al, 2006; Helfat et al, 2007).

Considering the type of competitive benefits related to cost-advantage in our study, there is indication that environmental management practices might serve as a way to lower labor costs "by reducing the cost of illnesses, absenteeism, recruitment, and turnover" (Am-bec and Lanoie, 2008, p. 57) and to increase employee awareness regarding their contribution to waste reduction, recycling, and the reduction of maintenance costs (Rondinelli and Vastag, 2000). Additionally, environmental management systems could enable co-operation between authorities and enterprises (Hamschmidt and Dyllick, 2001), thereby reducing the risk associated to this relationship (Bansal and Hunter 2003; Am-bec and Lanoie, 2008; Lo et al, 2012).

Furthermore, our analysis allows the examination of a relevant aspect of proactive environmental strategy from a dynamic capability perspective (Aragon-Correa and Sharma, 2003). That is, the ability of proactive environmental strategy to confer competitive advantage under conditions of shifting environments, characterized by unexpected discontinuities and unpredictable events (Teece et al., 1997). In particular, we analyzed uncertainty of the business environment as a contingency that moderates the relationship between a proactive environmental strategy and competitive advantage.

Definitions of environmental uncertainty based on managers' perceptions of the business environment "imply that firms respond to a general environment as it is interpreted by the decision makers and that its unper-ceived characteristics do not affect either the decisions of the actions of management" (Aragón-Correa and Sharma, 2003, p. 76). In other words, exogenous factors affect each firm differently, as they are moderated by managerial perceptions; ultimately, the successful performance of dynamic capabilities will depend on managers' judgment to determine what dynamic capabilities to deploy, and how and where (Ambrosini and Bowman, 2009, p. 40).

On the one hand, we observe that elements of perceived environmental uncertainty related to the extent to which a firm depends on both natural resources and environmental services, moderate the relationship between process and product-related environmental practices and cost advantage. In the face of growing pressure coming from internal and external stakeholders for improved environmental performance of products and services throughout their life cycle, managers scan their firm's environment looking for answers to three questions (Jabnoun et al, 2003): (1) how important are these resources and services for the firm, (2) what is their availability, and (3) to what extent is their control competed between companies. In turn, uncertainty increases when the perception is that the organization has no control of these resources and services when they are not easily available and thus are highly competed (López-Gamero et al, 2011b).

Faced with greater uncertainty, managers can opt for "building a high degree of adaptive capability" (Wang and Ahmed, 2007; cited in Ambrosini and Bowman, 2009, p. 45). While this response is not exempt of risks, the argument from contingent theory would suggest that in uncertain environments greater structure differentiation and the use of more sophisticated integration devices pays off (Lawrence and Lorsch, 1967; cited in Aragón-Correa and Sharma, 2003). In particular, the development of such adaptive capability in the form of differentiated structures for product redesign, process modification, cross-functional coordination, and stakeholder integration at the supply chain level and with external stakeholders (Hart, 1995; Sharma and Vredenburg, 1998; Christman, 2000; Sarkis, 2012; Hart and Dowell, 2011) will be successful when competitors need to incur the costs of building and maintaining their own capacity to adapt the organization (Ambrosini and Bowman, 2009) to pressures from stakeholders for an improved environmental performance.

The argument presented here is supported by two prescriptions provided by López-Game-ro et al. (2011b) to managers facing this type of uncertainty. They argue that "organizations must develop ways to exploit these resources, which other firms are also seeking, if they want to ensure their own survival", and also "develop and sustain effective relationships with their business environment", including cooperation with other firms and keeping in touch with key stakeholders (López-Gamero et al, 2011b, p. 434).

On the other hand, our results show that elements of uncertainty related to how managers perceive changes in customer preferences and the environmental strategy of competitors moderate the relationship between process and product-related environmental practices and cost advantage, and even between the former and differentiation advantage. The need to respond to these changes will lead some innovative firms to deploy and/or develop their organizational resources and capabilities to collaborate with regulators, facilitate alliances with community groups and non-governmental organizations, obtain environmental information and distribute it among employees, communicate with stakeholders, and educate to and engage with consumers (López-Gamero et al, 2011b).

As Aragón-Correa and Sharma (2003, p. 78) have argued, in more uncertain business environments firms will find it harder to obtain the information they need to duplicate the environmental capabilities of their competitors. Vis-á-vis uncertain customer preferences and changes in the environmental strategy of competitors, intra- and inter-organizational environmental capabilities involved particularly in product stewardship, may afford a firm the opportunity for sustained competitive advantage through the accumulation of socially complex resources involving fluid communication across functions, departments, and organizational boundaries (Hart, 1995, p. 1001; Shi et al, 2012).

Thus, the value of the dynamic capability of proactive environmental strategy stems from collaboration in supply chain networks, given the possibility for inter-organizational learning, which entails a problem solving routine connecting the focal firm with its suppliers and/or customers (Vachon and Klassen, 2008). Similarly, value stems from stakeholder integration (Sharma and Vredenburg, 1998; Verbeke et al., 2006), which represents "the ability to establish trust based collaborative relationships with a wide variety of stakeholders, especially those with non-economic goals" (Sharma and Vredenburg, 1998, p. 735) and helps build a firm's legitimacy to cope with uncertainty in its business environment (Goll and Rasheed, 2004; Hart and Dowell, 2011).

We find it interesting to recall that none of our models involving the environmental management practices (ENMP) construct offered evidence for interaction effects associated with perceived environmental state uncertainty. One possible explanation for this observation is found in Buysse and Verbeke (2003), who argue that environmental management standards and procedures such as the development of a written environmental plan or the implementation of the ISO 14000 standard do not demand performance beyond what is required by environmental regulations. Similarly, Andrews et al. (2006) have shown that the presence of management systems is correlated with significant improvements in the environmental impacts of unregulated aspects of business, such as spill avoidance or energy conservation, but that management systems do not correlate with reported improvements on regulated areas, such as air and water emissions. Seen in this light, environmental management practices should not be assimilated to the dynamic capability of proactive environmental strategy, and hence the theoretical expectation of moderation effects of perceived uncertainty would not apply to a model that includes an interaction effect involving such practices.

Final remarks

Our research shows that the uncertainty perceived by managers in the firm's business environment moderates the link between a firm's proactive environmental strategy and competitive advantage. To our knowledge, an empirical examination of Aragón-Correa and Sharma's (2003) proposition has remained absent from the literature until now. Interestingly, we observe that interaction effects are significant only in our models where process and product-related environmental practices are present, in contrast with those where environmental management practices are included, regardless of the dimension of perceived environmental uncertainty that is used as a moderator of the relationship between such practices and competitive advantage.

We believe that our findings are relevant for the community of peers and practitioners alike. In responding to the call for greater efforts needed "to incorporate both internal and external contingencies within analyses" of the performance effects of dynamic capabilities (Barreto, 2010, p. 277), our results suggest that the value of the dynamic capability of proactive environmental strategy is at least contingent upon the perceived uncertainty of the firm's external environment in two dimensions that have been previously revised by López-Gamero et al. (2011b): in relation to information uncertainty associated with changes in customer preferences and the environmental strategy of competitors, and to the extent to which a firm depends on natural resources and environmental technology services.

The necessary validation of measurement instruments for a relatively unknown territory within the dynamic capability perspective has limited the amount of observed variables that formed the latent factors remaining in our model. We believe that in turn this poses a limitation on the generalizability of our results, as there still might be relevant dimensions of our measures that are not being empirically captured and which could potentially impact the stability of our results. Consequently, additional work should be conducted in our business context to validate the empirical content of each of these constructs. Specifically, there is a need for further discussion and testing of measures for cost advantage and differentiation advantage, ultimately aimed at the promise of superior predictive validity.

While our study provides some empirical support for the contingent approach to dynamic capabilities advanced by the work of Winter (2003) and Aragón-Correa and Shar-ma (2003), and adopted into the dynamic capabilities research agenda by Ambrosini and Bowman (2009) and Barreto (2010), there is still much to be done. For instance, Teece's (2007) revisit to the definition of dynamic capability states that "the ambition of the dynamic capabilities framework is nothing less than to explain the sources of enterprise-level competitive advantage over time" (Teece, 2007, p. 1320). On the one hand, this implies a limitation in our study related to relying on a cross-sectional data sample to evaluate a phenomenon that is dynamic in nature. And, on the other hand, it suggests that an interesting extension of this study could be the analysis of how the development of external contingencies (e.g., uncertainty in the business environment) over time affects the role of proactive environmental strategy as a source of enterprise-level competitive advantage.

Additionally, when adopting the dynamic capability perspective to characterize a proactive environmental strategy, there are implications on the firm's resource base. Further research in the context of environmental management could explicitly study how such reconfiguration of the firm's resource base actually takes place. In other words, an interesting question to be answered is how a firm's resources are built and combined into a proactive environmental strategy in order to face uncertain environments and maintain competitiveness.

References

Ambec, S. and Lanoie, P. (2008). Does it pay to be green? A systematic overview. Academy of Management Perspectives, 22 (4), 45-62. [ Links ]

Ambrosini, V. and Bowman, C. (2009). What are dynamic capabilities and are they a useful construct in strategic management? International Journal of Management Reviews, 11 (1), 29-49. [ Links ]

Amit, R. and Schoemaker, P. J. H. (1993). Strategic assets and organizational rent. Strategic Management Journal, 14 (1), 33-46. [ Links ]

Andrews, R. N. L., Hutson, A. M. and Edwards Jr. D. (2006). Environmental management under pressure: How do mandates affect performance? In C. Coglianese and J. Nash (Eds.), Leveraging the private sector: Management-based strategies for improving environmental performance. Washington, D.C.: Resources for the Future. [ Links ]

Aragón-Correa, J. A. (1998). Strategic proactivity and firm approach to the natural environment. Academy of Management Journal, 41 (5), 556-567. [ Links ]

Aragón-Correa, J. A., Hurtado-Torres, N., Sharma, S. and Garcia-Morales, V. J. (2008). Environmental strategy and performance in small firms: A resource-based perspective. Journal of Environmental Management, 86 (1), 88-103. [ Links ]

Aragón-Correa, J. A. and Sharma, S. (2003). A contingent resource-based view of proactive corporate environmental strategy. Academy of Management Review, 28 (1), 71-88. [ Links ]

Armstrong, J. S. and Overton, T. S. (1977). Estimating Nonresponse Bias in Mail Surveys. Journal of Marketing Research, 14, 396-402. [ Links ]

Bandalos, D. L. and Finney, S. J. (2001). Item parceling issues in structural equation modeling. In G. A. Marcoulides and R. E. Schumacker (Eds.), New developments and techniques in structural equation modeling (pp. 269-296). Mahwah, NJ: Lawrence Erlbaum Associates, Inc. [ Links ]

Banerjee, S. B. (2001). Managerial perceptions of corporate environmentalism: Interpretations from industry and strategic implications for organizations. Journal of Management Studies, 38 (4), 488-513. [ Links ]

Bansal, P. and Roth, K. (2000). Why companies go green: A model of ecological responsiveness. Academy of Management Journal, 43 (4), 717-736. [ Links ]

Bansal, P. and Hunter, T. (2003). Strategic explanations for the early adoption of ISO 14001. Journal of Business Ethics, 46 (3), 289-299. [ Links ]

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17 (1), 99-120. [ Links ]

Baron, R. M. and Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51 (6), 1173-1182. [ Links ]

Barreto, I. (2010). Dynamic capabilities: A review of past research and an agenda for the future. Journal of Management, 36 (1), 256-280. [ Links ]

Bowen, F., Cousins, P., Lamming, R. and Faruk, A. (2006). Horses for courses: Explaining the gap between the theory and practice of green supply. In J. Sarkis (Ed.), Greening the Supply Chain. London: Springer-Verlag. [ Links ]

Boyd, B. (1990). Corporate linkages and organizational environment: A test of the resource dependence model. Strategic Management Journal, 11 (6), 419-430. [ Links ]

Brown, T. A. (2006). Confirmatory Factor Analysis for Applied Research. New York: The Guilford Press. [ Links ]

Burns, T. and Stalker, G. M. (1961). The management of innovation. Oxford: Oxford University Press. [ Links ]

Buysse, K. and Verbeke, A. (2003). Proactive environmental strategies: A stakeholder management perspective. Strategic Management Journal, 24 (5), 453-470. [ Links ]

Chan, R. Y. (2005). Does the natural-resource-based view of the firm apply in an emerging economy? A survey of foreign invested enterprises in China. Journal of Management Studies, 42 (3), 625-672. [ Links ]

Christmann, P. (2000). Effects of "Best Practices" of Environmental Management on Cost Advantage: The Role of Complementary Assets. Academy of Management Journal, 43 (4), 663-680. [ Links ]

Claver-Cortés, E., Molina-Azorín, J. F., Tarí-Guilló, J. J. and López-Gamero, M. D. (2005). Environmental management, quality management and firm performance, a review of empirical studies. In S. Sharma and J. A. Aragón-Correa (Eds.), Corporate environmental strategy and competitive advantage (pp. 157-182). Northampton, MA: Edward Elgar. [ Links ]

Colwell, S. R., and Joshi, A. W. (2013). Corporate ecological responsiveness: Antecedent effects of institutional pressure and top management commitment and their impact on organizational performance. Business Strategy and the Environment, 22 (2), 73-91. [ Links ]

Couper, M. P. (2000). Web surveys: A review of issues and approaches. Public Opinion Quarterly, 64 (4), 464-494. [ Links ]

Dess, G. G. and Beard, D. W. (1984). Dimensions of organizational task environments. Administrative Science Quarterly, 29 (1), 52-73. [ Links ]

Duncan, R. B. (1972). Characteristics of organizational environments and perceived environmental uncertainty. Administrative Science Quarterly, 17 (3), 313-327. [ Links ]

Eisenhardt, K. M. and Martin, J. A. (2000). Dynamic capabilities: What are they? Strategic Management Journal, 21 (10/11), 1105-1105. [ Links ]

Esty, D. and Winston, A. (2006). Green to Gold: How Smart Companies Use Environmental Strategy to Innovate, Create Value, and Build Competitive Advantage. New Haven and London: Yale University Press. [ Links ]

Galdeano-Gómez, E. (2008). Does an endogenous relationship exist between environmental and economic performance? A resource-based view on the horticultural sector. Environmental and Resource Economics, 40 (1), 73-89. [ Links ]

Gavronski, I., Klassen, R. D., Vachon, S. and Nascimento, L. F. (2012). A learning and knowledge approach to sustainable operations. International Journal of Production Economics, 1-10. [ Links ]

Gilley, K. M., Worrell, D. L., Davidson, W. N. and El-Jelly, A. (2000). Corporate environmental initiatives and anticipated firm performance: the differential effects of process-driven versus product-driven greening initiatives. Journal of management, 26 (6), 1199-1216. [ Links ]

Goll, I. and Rasheed, A. A. (2004). The moderating effect of environmental munificence and dynamism on the relationship between discretionary social responsibility and firm performance. Journal of Business Ethics, 49, 41-54. [ Links ]

González-Benito, J. and González-Benito, Ó. (2005). Environmental proactivity and business performance: An empirical analysis. Omega, 33 (1), 1-15. [ Links ]

Gosling, S. D., Vazire, S., Srivastava, S. and John, O. P. (2004). Should we trust web-based studies? A comparative analysis of six preconceptions about internet questionnaires. American Psychologist, 59 (2), 93-104. [ Links ]

Hair, J. F., Black, W. C., Babin, B. J. and Anderson, R. E. (2010). Multivariate data analysis (7th ed.). Upper Saddle River, NJ: Prentice Hall. [ Links ]

Hamschmidt, J. and Dyllick, T. (2001). ISO 14001 profitable? Yes! But is it eco-effective? Greener Management International, 34, 43-54. [ Links ]

Harrington, D. R., Khanna, M. and Deltas, G. (2008). Striving to be green: The adoption of total quality environmental management. Applied Economics, 40 (23), 2995-3007. [ Links ]

Hart, S. L. (1995). A natural-resource-based view of the firm. Academy of Management Review, 20 (4), 986-1014. [ Links ]

Hart, S. L. and Dowell, G. (2011). A natural-resource-based view of the firm: Fifteen years after. Journal of Management, 37 (5), 1464-1479. [ Links ]

Hayduk, L. A. (1988). Structural equation modeling with LISREL: Essentials and advances. Baltimore: John Hopkins University Press. [ Links ]

Helfat, C. E., Finkelstein, S., Mitchell, W., Peteraf, M., Singh, H., Teece, D. and Winter, S. G. (2009). Dynamic capabilities: Understanding strategic change in organizations. London: Blackwell. [ Links ]

Hunt, C. B. and Auster, E. R. (1990). Proactive environmental management: avoiding the toxic trap. Sloan Management Review, 31 (2), 718. [ Links ]

Jabnoun, N., Khalifah, A. and Yusuf, A. (2003). Environmental uncertainty, strategic orientation, and quality management: a contingency model. Quality Management Journal, 10 (4), 17-31. [ Links ]

Johnson, D. R. and Creech, J. C. (1983). Ordinal measures in multiple indicator models: A simulation study of categorization error. American Sociological Review, 48, 398-407. [ Links ]

Jöreskog, K., Sörbom, D., du Toit, S. and du Toit, M. (2001). LISREL 8: New Statistical Features. Lincolnwood, IL: Scientific Software International, Inc. [ Links ]

Judge, J. R. and Douglas, T. J. (1998). Performance implications of incorporating natural environmental issues into the strategic planning process: an empirical assessment. Journal of Management Studies, 35 (2), 241-262. [ Links ]

Judge, W. Q. and Elenkov, D. (2005). Organizational capacity for change and environmental performance: an empirical assessment of Bulgarian firms. Journal of Business Research, 58 (7), 893-901. [ Links ]

Karagozoglu, N. and Lindell, M. (2000). Environmental management: Testing the win-win model. Journal of Environmental Planning and Management, 43 (6), 817-829. [ Links ]

Kemp, R. (1998). The diffusion of biological wastewater treatment plants in the Dutch food and beverage industry. Environmental and Resource Economics, 12 (1), 113-136. [ Links ]

King, A. A. and Lenox, M. J. (2001). Lean and green? An empirical examination of the relationship between lean production and environmental performance. Production and Operations Management, 10 (3), 244-256. [ Links ]

Klassen, R. D. and Whybark, D. C. (1999). The impact of environmental technologies on manufacturing performance. Academy of Management Journal, 42 (6), 599-615. [ Links ]

Lawrence, P. and Lorsch, J. (1967). Organization and environment: Managing differentiation and integration. Boston: Harvard University Graduate School of Business Administration Division of Research. [ Links ]

Lewis, G. J. and Harvey, B. (2001). Perceived environmental uncertainty: The extension of Miller's scale to the natural environment. Journal of Management Studies, 38 (2), 200-233. [ Links ]

Linton, J. D., Klassen, R. and Jayaraman, V. (2007). Sustainable supply chains: An introduction. Journal of Operations Management, 25 (6), 1075-1082. [ Links ]

Little, T. D., Cunningham, W. A., Shahar, G. and Widaman, K. F. (2002). To parcel or not to parcel: Exploring the question, weighing the merits. Structural Equation Modeling, 9 (2), 151-173. [ Links ]

Lo, C. K., Yeung, A. C. and Cheng, T. C. E. (2012). The impact of environmental management systems on financial performance in fashion and textiles industries. International Journal of Production Economics, 135 (2), 561-567. [ Links ]

López-Gamero, M. D., Claver-Cortés, E. and Molina-Azorín, J. F. (2011a). Environmental perception, management, and competitive opportunity in Spanish hotels. Cornell Hospitality Quarterly, 52 (4), 480-500. [ Links ]

López-Gamero, M. D., Molina-Azorín, J. F. and Claver-Cortés, E. (2009). The whole relationship between environmental variables and firm performance: Competitive advantage and firm resources as mediator variables. Journal of Environmental Management, 90 (10), 3110-3121. [ Links ]

López-Gamero, M. D., Molina-Azorín, J. F. and Claver-Cortés, E. (2011b). Environmental uncertainty and environmental management perception: A multiple case study. Journal of Business Research, 64 (4), 427-435. [ Links ]

Maas, S., Schuster, T. and Hartmann, E. (2012). Pollution prevention and service stewardship strategies in the third-party logistics industry: effects on firm differentiation and the moderating role of environmental communication. Business Strategy and the Environment. [ Links ]

Makadok, R. (2001). Toward a synthesis of the resource-based and dynamic-capability views of rent creation. Strategic Management Journal, 22 (5), 387-401. [ Links ]

Marsh, H. W., Wen, Z. and Hau, K.-T. (2006). Structural equation models of latent interaction and quadratic effects. In G. R. Hancock and R. O. Mueller (Eds.), Structural Equation Modeling: A Second Course (pp. 225-265). Charlotte, NC: Information Age Publishing. [ Links ]

Marsh, H. W., Wen, Z., Nagengast, B. and Hau, K.-T. (2012). Structural equation models of latent interaction. In R. H. Hoyle (Ed.), Handbook of structural equation modeling (pp. 436-458). New York: The Guilford Press. [ Links ]

McArthur, A. W. and Nystrom, P. C. (1991). Environmental dynamism, complexity, and munificence as moderators of strategy-performance relationships. Journal of Business Research, 23 (4), 349-361. [ Links ]

Menguc, B., Auh, S. and Ozanne, L. (2010). The interactive effect of internal and external factors on a proactive environmental strategy and its influence on a firm's performance. Journal of Business Ethics, 94 (2), 279-298. [ Links ]

Milliken, F. J. (1987). Three types of perceived uncertainty about the environment: State, effect, and response uncertainty. Academy of Management Review, 12 (1), 133-143. [ Links ]

Mir, D. F. and Feitelson, E. (2007). Factors affecting environmental behavior in micro-enterprises: Laundry and motor vehicle repair firms in Jerusalem. International Small Business Journal, 25 (4), 383-415. [ Links ]

Moreno-Mantilla, C. E., Romero-Larrahondo, P. A. and Reyes-Rodríguez, J. F. (2013). Driving product stewardship: an empirical evaluation of the association between some form of LCA implementation and environmental strategy choice in Colombian firms. Paper presented at the Vth International Conference on Life Cycle Assessment, CILCA2013, Mendoza, Argentina. [ Links ]

Parker, C. M., Redmond, J. and Simpson, M. (2009). A review of interventions to encourage SMEs to make environmental improvements. Environment and Planning C: Government and Policy, 27, 279-301. [ Links ]

Popp, D. (2005). Uncertain R&D and the Porter Hypothesis. Contributions to Economic Analysis & Policy, 4 (1), 1-14. [ Links ]

Prescott, J. E. (1986). Environments as moderators of the relationship between strategy and performance. Academy of Management Journal, 29 (2), 329-346. [ Links ]

Reinhardt, F. (1999). Market failure and the environmental policies of firms: Economic rationales for 'beyond compliance' behavior. J. Ind. Ecol, 3 (1), 9-21. [ Links ]

Reinhardt, F. L. (1998). Environmental product differentiation: Implications for corporate strategy. California Management Review, 40 (4), 43-ss. [ Links ]

Rondinelli, D. and Vastag, G. (2000). Panacea, Common Sense, or Just a Label? The Value of ISO 14001 Environmental management systems. European Management Journal, 18 (5), 499-510. [ Links ]

Roome, N. (1992). Developing environmental management strategies. Business Strategy and the Environment, 1 (1), 11-24. [ Links ]

Rothenberg, S., Pil, F. K. and Maxwell, J. (2001). Lean, green, and the quest for superior environmental performance. Production and Operations Management, 10 (3), 228-243. [ Links ]

Rueda-Manzanares, A., Aragon-Correa, J. A. and Sharma, S. (2008). The influence of stakeholders on the environmental strategy of service firms: The moderating effects of complexity, uncertainty and munificence. British Journal of Management, 19 (2), 185-203. [ Links ]

Russo, M. V. (2009). Explaining the Impact of ISO 14001 on Emission Performance: a Dynamic Capabilities Perspective on Process and Learning. Business Strategy and the Environment, 18 (5), 307-319. [ Links ]

Russo, M. V. and Fouts, P. A. (1997). A resource-based perspective on corporate environmental performance and profitability. Academy of Management Journal, 40 (3), 534-559. [ Links ]