Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkCuadernos de Administración (Universidad del Valle)

Print version ISSN 0120-4645On-line version ISSN 2256-5078

cuad.adm. no.43 Cali Jan./June 2010

Strategic crowding, an illness that erodes sector profitability: case pharmaceutic industry in Colombia

Hacinamiento estratégico, una enfermedad que erosiona la rentabilidad del sector: caso de la industria farmacéutica en Colombia

Hugo A. Rivera Rodríguez*

Natalia Malaver Rojas**

* hugo.rivera@urosario.edu.co Carrera 6 No. 57-44. Apto 504 t1. Chapinero Alto Bogotá -Colombia. Estudiante de Doctorado en Administración de la Universidad de los Andes, Magister en Administración, Universidad Externado, Bogotá. Economista Empresarial Universidad Autónoma, Manizales. Profesor principal e investigador del Grupo de Investigación en Perdurabilidad Empresarial de la Facultad de Administración, Universidad del Rosario, Bogotá - Colombia.

** nathmalaver@gmail.com Carrera 6 No. 57-44. Apto 504 Chapinero Alto Bogotá -Colombia. Magister en Dirección y Gerencia de Empresas, Especialista en Gerencia en Negocios Internacionales Universidad del Rosario. Abogada, Universidad del Rosario. Docente de la Facultad de Administración, Universidad del Rosario, Bogotá - Colombia.

Artículo Tipo 2: de reflexión Según Clasificación Colciencias.

Fecha de recepción: febrero 10 2010 Fecha de corrección: abril 15 2010 Fecha de aprobación: abril 23 2010

ABSTRACT

Firms in the last decade have faced a turbulent environment, characterized by increasing complexity in relationships, changes in the needs of customers, and increased uncertainty in decision making. Some companies respond to this situation using the same strategies of industry leaders, leading to a convergence process, which affects the profitability of the sector. This paper presents a methodology that allows a better way to see what happens in one sector and determine the degree of convergence.

Keywords: strategic crowding, turbulent environments, strategy, pharmaceutical industry, environmental scanning.

RESUMEN

Las organizaciones en la ultima década se han enfrentado a un entorno turbulento, caracterizado por un aumento en la complejidad de las relaciones, cambios en las necesidades de los clientes e incremento de la incertidumbre en la toma de decisiones. Algunas empresas para responder a esta situación utilizan las mismas estrategias de los lideres de la industria, lo que lleva a un proceso de convergencia, que afecta la rentabilidad del sector. Este documento presenta una metodología que permite percibir de una mejor manera lo que ocurre en un sector y determinar el grado de convergencia.

Palabras clave: estrategia, análisis sectorial, hacinamiento, entorno turbulento, industria farmaceutica.

1. Introduction

The field of strategy, since it was consolidated as an independent discipline of economics in the last half century, has sought to explain the motives that drive an enterprise to be better than others, despite living in the same environment. It has been preoccupied with finding the factors of competitive advantage. The pioneers in this subject were Andrews, Cristensen, Gult and Learned, who in the decade of the sixties of the last century proposed the tool known as SWOT, to conduct strategic analysis; years later Porter (1979, 2008) identified the different forces that regulate the competency into an economic sector. Later, he identified the national competitive advantage determinant factors and other tools of sectoral analysis. In recent years Ramos and Ruiz (2004) and Nag, Hambrick and Chen (2008) suggests that environmental scanning is one of the main themes used in the strategy, and the reason is that this can affect the survival of the company.

Other academics have studied the dynamics in economic sectors. For Johnson and Scholes (1999) dynamism implies that an organization can not make future decisions based solely on historical data. Rather it must operate with its current products while anticipating the results of their actions in the future.

Nattermann (2000) published an article entitled Best practice does not equal best strategy in which he mentions that strategic crowding is a way to establish the degree of attractiveness of a sector. The author mentions in his paper that companies have an instinct that drives them to move collectively, trying to imitate those companies that stand by a number of characteristics such as type of product, advertising, distribution channels, etc. This destroys value: quickly, the profits of the market leader will be divided among the group of companies that converge in the same space. The companies reaped lower profits in the peaks, resulting from theiro joining the herd. As a result, these sources of revenue are empty, until other companies see an opportunity and seize it. The combination of lost profits for having abandoned the peaks and smaller static gains in the points of agglomeration forces the falling profitability of the industry. This same point is addressed by Markides (1997) in his study about imitation in a simulation environment. Both documents confirm the effect that imitation has in the companys profitability.

Hamel (1996), since the nineties is studying the complexity that occurs in different sectors. In one of his documents he developed the term strategic revolution and states that after the era of progress, companies with very high expenses where every day is worth less tenure, and new business models break all the rules, changes are fast and like retail stores die, old and trusted big companies fall into decay and lose their markets. The marks left by brief and customer acquisition become an art and skill of a few.

The concept of increasing returns also functions and is explained by saying that in areas the rich are becoming richer and the poor poorer, that is that that first win is always first, and highlights sectors that are highly dynamic and require a high degree of innovation. The most successful companies do not become obsessed with their competitors, if not seeking new markets, nor the major companies who are now beginning to lose their markets, their customers and employees who decide to form their own business or enter into capital speculation.

Subsequently, the concept of industrial revolution has been used by Bitar (2003), Tan, Li and Li (2006), Suikki, Tromstedt and Haapasalo (2006), El Sawy and Pavlou (2008), and Pettus and Mahoney (2009) to study the complexity in the economic sectors like a turbulence to explain the turbulence. For them, to deal with turbulent environments, the companies need to obtain dynamic capabilities, to decrease the uncertainty in the decision making process.

As part of this strategy, a school that has become stronger in the last decades, Restrepo y Rivera (2008), and Rivera y Malaver (2008) have proposed mechanisms to ensure the firms longevity with high profitability levels. Among the mechanisms there is a special project called Strategic Analysis of Economic Sectors (SAES). The purpose of SAES is to develop a methodology, which will give tools to investors, entrepreneurs, managers, etc, to make the best possible decision in order to remain with high profitability levels.

The methodology consist of several steps:

1 Strategic convergence, 2 Market forces, 3 Competitive diamond, 4 Competitive panorama, 5 Competency analysis, 6 Agglomeration chart, 7 Barrier and profitability matrix, 8 Macroeconomic studies.

Though the methodology elements are being studied, this paper will be addressed to the Strategic convergence as the first methodology element, and help find answers to these questions:

Why are there economic sectors with higher profitability levels than others, if all of them have the same macroeconomic environment?, What is the level of imitation that shows the sector where my company competes?, Which is the measure of superior performance of the sector?

2. Crowding: measures and Interpretation

2.1. Quantitative Crowding

Strategic crowding is observed in an industrial sectors financial results. Therefore, the quantitative evaluation is basic to determine its presence. To do this, several statistics tests are developed. To determine if there is strategic crowding in a sector, the following tests are done:

1. Profitability performance over time

2. Financial asymmetry determination

3. Kurtosis level

4. Third quartile

5. Income delta vs. Profits delta

2.2. Profitability performance over time

Profitability performance over time is one of the indices that let us know if an industrial sector is crowded or not. According to Nattermann (1999) the sector profitability decreases because of two phenomena, first, the entrance of new competitors that increases the offer into the sector, leading to a drop in prices. The second phenomenon is the imitation of strategies among competitors. As Natermann (1997) observes, this situation increases the rivalry into the sector. After Markides studies (1997), demonstrated that falling profitability is owed in large part to the imitation or strategic convergence rather than the entrance of new competitors. Nattermann (2000) said that the entrance of new competitors erodes profitability by 19%, while the strategic convergence erodes it by 50%.

A strategic convergence consequence is the sub-utilization of the available resources into the sector (Markides, 1997). The imitation leads the actors to use the same resources, leaving available resources in other market spaces, which are not perceived by the organizations in their hurry to follow the leader. In this situation, there is depletion of resources. Generating increased bargaining power of suppliers and customers.

2.3. Asymmetry

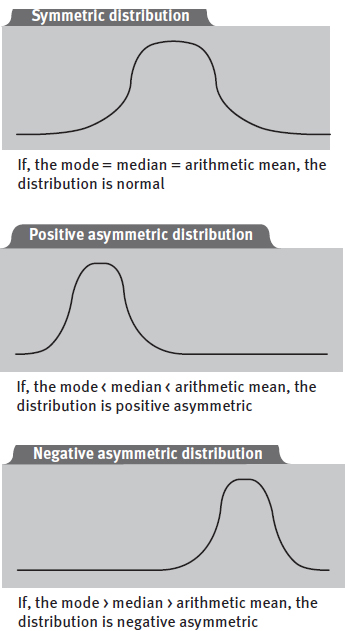

In general, the asymmetry study is developed to analyze how data is distributed around their measures of a central tendency: arithmetic mean, median and mode. Depending on the coefficient of symmetry or asymmetry chosen, this will always make reference to a measure of a central tendency.

It is necessary to determine in an asymmetry study the kind (positive or negative) and the level. The descriptive statistics give different ways to calculate the level as well as the kind.

2.4. Mode, Median, Arithmetic Mean

According to descriptive statistics, there is asymmetry in a set of data when the measures of central tendency (mode, median and arithmetic mean) are different.

In a crowding study, it is hoped that the kind of asymmetry in the set will be positive. As can be seen in the graphic above, most of the data is at the left side of the distribution, leaving the right side with less data. As it is explained further, this represents the highest values in the distribution.

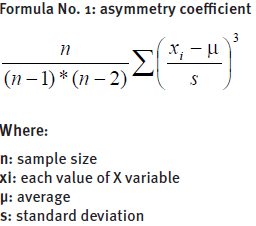

2.5. Asymmetry coefficient

The asymmetr y coefficient indicates the asymmetr y kind and level into a distribution. Depending on the coefficient chosen, the value will be higher, minor or equal to zero. If the coefficient is higher than zero, most of the data will be concentrated at the left side of the distribution (positive asymmetry). On the other hand, if the coefficient is minor than zero, most of the data will be concentrated at the right side of the distribution (negative asymmetry). For this study, the asymmetry coefficient has been calculated with the formula bellow.

As has been mentioned, it can be expected that the asymmetry in the set of profitability will is positive. This means that most of the data will be concentrated at the left side of the set, leaving a small amount of companies at the right side.

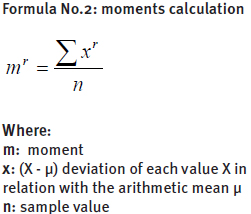

2.6. Kurtosis

The Kurtosis is the other way to measure dispersion in a distribution of data. The difference between each value and the arithmetic mean, determines the dispersion degree. The kurtosis degree is inferred from this analysis. Kurtosis can be measured in different ways; however, one of the most common ways to measure it is through moments. Moments make reference to the standard deviation of each value and the arithmetic mean. The r-esimo moment in relation to the average is defined as follows:

The moment four (a4) is one of the most used ways to measure kurtosis. According to the theory, 3 is the value of a4 for a normal distribution. Therefore, the kurtosis can be expressed as (Shao, 1967):

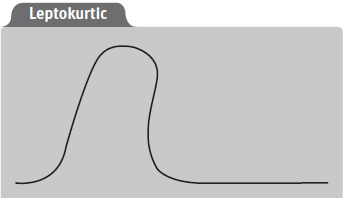

* a4 – 3 = 0 indicates normal distribution, masokurtic.

* a4 – 3 > 0 while higher is the difference of (a4 – 3) above zero, the distribution height is higher, leptokurtic.

* a4 – 3 < 0 while lesser is the difference bellow zero, the distribution height is less, platikurtic.

The leptokurtic distribution is characterized by its higher height degree. There is a higher concentration of frequencies around the arithmetic mean.

The platikurtic distribution shows a minor concentration of data around the arithmetic mean. This distribution presents an opposite shape to the leptokurtic distribution.

2.7. Income delta vs. Profits delta

As was explained, the financial results are the consequence of the strategy used by companies. If the relation between income and profits is negative, the companies increase their income handing over value (Hamel, 2000). At this point is when companies consider productivity as strategic. Bilocation is not considered as part of the profitability problem. According to Hamel (2000) companies such as Compaq Computer have had income – profits ratios of –7: 3, which means that for each dollar of profits, the company receives an income of –7, 3 dollars. What does it mean? Those profits in Compaq are the result of productivity processes, but not the result of new markets or new customers. An organization that has experimented strategy erosion must show a relation of 5:1, this means that for each dollar of profits the company must produce 5 dollar in income. Bellow this parameter it is considered that the strategy is falling (Hamel, 2000).

2.7. Third quartile calculation

Data distribution is divided in same size quartiles, which represents how the sample is dispersed. The first quartile represents the 25% of the distribution, the second quartile, is the 50%, which is the same median, and the third quartile is the 75% percent of the data in a distribution.

Some academics have considered the third quartile (Hamel, 2000) as an acceptable parameter to determine companies with superior yields. Companies at the right side of the third quartile (25% of the data) could be considered as superior yields companies. Nevertheless, it is important to clarify, that a company has superior yields if through the years, it stays over the third quartile. This study has been determined by a threshold time of nine years.

According to the explanation above the following hypotheses can be stated:

A sector is crowding if:

H1: profitability decreases through the years.

H2: asymmetry is positive

H3: the curve is leptokurtic with a4 > 0

H4: the income – profits ratio is less than 5:1

H5: companies bellow the third quartile are crowding.

If a company fulfills with all the conditions above, it can be stated that it is crowded. The following case is developed whit the pharmaceutical industry

2.8. Practical Case

The exercise explained above is developed with the pharmaceutical industry. The study was made for a time period of nine years (2000-2008). In this period, the methodologies described above are used with the return over assets (ROA)1 as a profitability index. The index chosen indicates the companies ability to generate profits. According to Cadena, Guzman and Rivera (2006) to identify whether there is superior performance, it is important to define one or more indicators that are representative of the financial performance of the strategic sector, and thus determine the level of liquidity, profitability and / or structure indebtedness. The literature on strategy is concerned with the measurement of corporate performance, which can be found in publications such as Strategic Management Journal, uses ROA, which measures the profitability of the shareholders and the actual use or productivity assets of the company.

Continuing with the methodology explained above, the profitability fluctuation is determined through the years studied. Its performance is shown in the graph No.1. In this graph, a first reading can be made about the sector and its capacity to generate profits. In this sector the profitability has fluctuated in the last nine years without showing a clear tendency. It is likely that companies with high profits modify the tendency of the sector, and the performance of crowding companies can not been appreciated.

Based on the total amount of companies analyzed, the third quartile is calculated. (graph 2). This value, the ROA for this research, lets us know the number of companies over and under the 75 percentile. This point allows us to make the first reading about the companies with high yields.

The population is divided in two groups, based on the values depicted in the graph 2. Companies bellow these profits levels are considered crowded. On the other hand, companies above these values are considered as high yields companies. Graph 3 shows companies that are bellow the third quartile. Based on these companies, the analysis through the nine years is developed.

Based on this division, the crowding analysis starts with the number of companies established in graph 3.

2.9. Profitability fluctuation over time

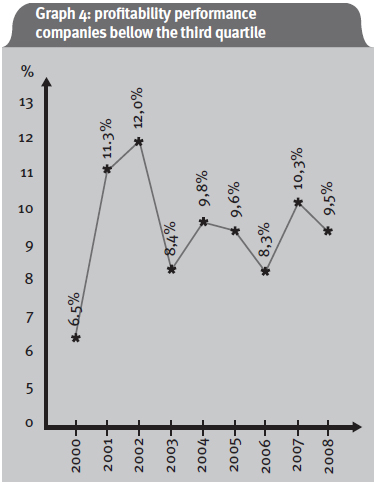

The profitability performance is depicted in graph 4 for the pharmaceutical industry. The analysis is made for companies bellow the third quartile.

During the nine years studied the profitability has fluctuated, specially between 2003- 2006, reaching its lowest point during these years. From 2003, the sample profitability has remained down. Based on this first diagnostic, it can be inferred that during the last three years companies have increased their crowding level, due to the profitability drop.

2.10. Asymmetry analysis

The selected sample lacks of mode. Thus the analysis will be developed based on the median and arithmetic mean. According to the explanation given in the number three, the median must be less than the arithmetic mean (Median < Arithmetic mean), so it can be stated that the asymmetry is positive and crowding can be found in the sector. In the graph 5 the relationship between the median and the arithmetic mean is shown.

According to graph 5, the relationship between median and arithmetic mean shows a minimal difference between these two measures of central tendency. Part of the analysis developed above, shows positive asymmetry. Thus, the median < arithmetic mean. In some cases they are equals. Based on these data, a first reading indicates that the studied sample tends to have a normal distribution.

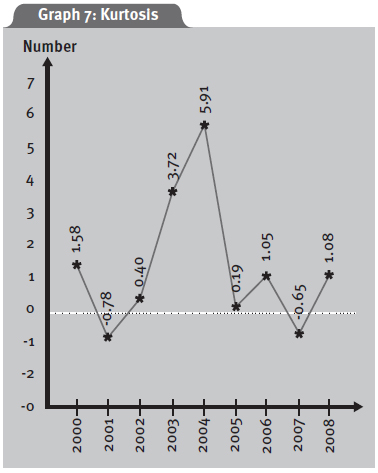

If to the analysis we add the asymmetry coefficient (graph 6), it can be concluded that most of the years show a positive asymmetry but 1995, is a year in which the coefficient is negative. This indicates that most of the data stays at the right side of the distribution. This can be confronted in the graph 7, in which the average profitability through the years is higher in 1995, the year in which the asymmetry is negative.

In the rest of the years the asymmetry is positive. Nevertheless in very low levels, in most of the cases one is not even reached. As a first diagnosis of the crowding level in this sector, it can be said that, even though the profitability in the latter years has fallen, the asymmetry analysis shows a distribution that trends to normal. This means that the data trend is homogenous.

2.11. Kurtosis

In the studied sector it is seen (graph 7) that the sample kurtosis is negative, which means that the curve is platikurtic. The data have a higher degree of dispersion bellow the curve, making the data dispersed. Based on this analysis, it can be inferred that the media is not a good measure for this sample, due to the dispersion degree.

Even though it is a researchers choice to determine if the measure is representative for the sample, in this study, it was determined that there is a big dispersion in the analyzed data, therefore the arithmetic mean can not be considered as a representative measure. In most of the cases the range between the minor and the higher value is above of 5%. In figure 9, the trend between the arithmetic mean and the standard deviation is shown. In this graph, is not hard to conclude that the values of the standard deviation through the years confirm the kurtosis analysis.

2.12. Income delta vs. profits delta

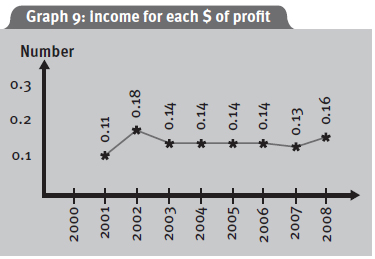

According to the explanation given in number three, the relationship between income and profits must be 5:1. So it can be stated that the strategy has not been eroded. In the graph No.9 the relationship between income and profits can be seen. None of the years show a negative relationship, however, the relationship does not show that the companies increase their profits as a result of strategy strength.

2.13. Results

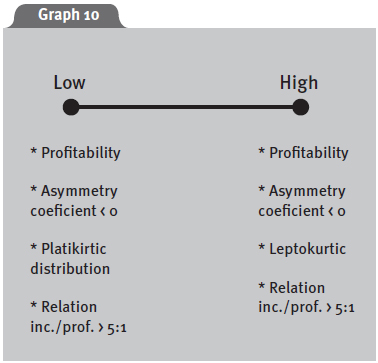

Into the threshold that heaping can have in a sector; it can be completely heaped. In this situation the sector is characterized by: a) decreasing profitability tendency; b) having positive asymmetry coefficient; c) being leptokurtic: d) having a relationship between income and profits lower that 5:1. On the other hand, an non-crowded sector presents:

a) increasing profitability through the years

b) negative asymmetry coefficient

c) platikurtic distribution

d) relation between income and profits higher that 5:1. In the graph No.10 these characteristics are depicted

To measure the degree of crowding in an industrial sector in a more objective way, an exit table has been developed. This table allows making a first diagnosis of the sector (table No.1). This tool summarizes the above analysis in four variables: profitability, asymmetry coefficient, kurtosis level and the relation between income/profits. These variables show the same weighting degree among themselves. Nevertheless, the entire quantitative analysis represents the 50% and the qualitative analysis represents the 50%. Adding these two measures gives as a total result the total crowding level of a sector.

In the table No. 1, four variables are tested; profitability, asymmetry coefficient, kurtosis and the relation income-profits. Each variable has in each cell a 0,25 qualification. The degree of crowding can be determined with this tool. Adding the cells in a column it can be determined if the sector is crowded if the addition trends to 1. Thus, when the column that indicates a high crowding degree (H), is 1, it can be stated that the sector is highly crowded. On the other hand, if the addition of the cells in the column L is 1, the sector is not crowded. According to this, it can be inferred that the pharmaceutical industry has a medium low crowding degree, having as the only crowding symptom the relation income over profits, in which it can be seen that the companies present erosion in their strategies.

3. Conclusion

The academy of management has been concerned for years in seeking answers to the question why some companies are better than others?, concluding that the managers that better understood the environment obtained better results. To achieve take command of the sector, the business manager should analyze the market and identify the signals it gives us constantly, as in the case of companies that disappear, or entering, the decline in market share caused by price wars, or the appearance of products with new features. It is important to recognize these signs and take appropriate measures to prevent the companys profits eroding and therefore contribute to the decrease of the profits in the sector.

In this paper, we showed the strategic crowding proposal. With the crowding analysis we attempt to measure the potential financial symmetries, in which case you could see how much similarity exists in the performance of the sector and thus to end on a quantitative level of imitation. The financial results for homogeneous, low, plus a significant strategic convergence are the property of a crowded sector characterized by imitation. In these sectors, and this is hypothesized, they would not generate enough jobs to support policies that will assist in providing decent and productive work. If true, and once our research progresses, we may conclude that the sectors are overcrowded, in essence, generating productive and decent employment.

With regard to the questions presented in the introduction: Why are there economic sectors with higher profitability levels than others, if all of them have the same macroeconomic environment? What is the level of imitation that shows the sector where my company competes? What is the measure of superior performance of the sector? We have found that implementing the proposed methodology, companies realize greater profitability as a result of implementing business models aimed at innovation, which identify and meet needs not supplied or exploitable weaknesses by competitors, and in other cases pursuing a strategy of rupture. Regarding the question on the level of imitation of the sector, the methodology for identifying differences and similarities between firms using financial information, the more similar are the strategies, and the generation of superior performance will become something more improbable. Finally, regarding the concern for superior performance measurement, we conclude that using the mean of profitability does not identify differences in the sector, thereby separating the third quartile firms who achieved superior performance over the others.

To finish, we can say that the implementation of the methodology provides important elements for the decision maker to enable him/ her to answer the question why one company is better than another.

NOTA AL PIE

1. The information of this study is taken from the data published by the Superintendencia de Sociedades. www.supersociedades.gov.co

4. References

1. Bitar, J. (2003). Strategy in Turbulent Environment Continuous Innovation and Generic Dynamic Capabilities. Montreal: HEC. [ Links ]

2. Cadena, J.; Guzman, A. y Rivera, H. (2006) ¿Es posible medir la perdurabilidad empresarial? Revista Científica de UCES. 10(1), 47-69. [ Links ]

3. Christensen, R.; Andrews, K.; Guth, W. & Learned, E. (1965). Business Policy: Text and Cases. Honewood, Illinois. [ Links ]

4. El Sawy, O. & C Pavlou, P. (2008). IT-Enabled Business capabilities for Turbulent Environments. MIS Quarterly Executive, 7 (3), 139-150. [ Links ]

5. Hamel, G. (2000). Liderando la revolution (primera ed.). Bogotá: editorial Norma S.A [ Links ]

6. Johnson, G. & Scholes, K. (1999). Exploring Corporate Strategy: Text and Cases. Harlow, England: Prentice Hall. [ Links ]

7. Markides, C. (1997). Strategic Innovation. Sloan Management Review, 38 (3), 9-23. [ Links ]

8. Markides, C.; Larsen, E. & Shayne, G. (2003), Firm-level imitation and the evolution of industry profitability: a simulation study. London Business School (working paper) [ Links ]

9. Nag, R.; Hambrick, D. & Chen, M. (2007). What is Strategic Management Really Inductive Derivation of a Consensus Definition of The Field? Strategic Management Journal, 935-955. [ Links ]

10. Nattermann, P. (2000), Best Practice does not Equal Best Strategy, The McKinsey Quarterly, 2, 22-31. [ Links ]

11. Nattermann, P. (1999). Estimating firm conduct: A study on the German Cellular Telephone Market, Unpublished doctoral dissertation, Georgetown University. [ Links ]

12. Nattermann, P. (1997). New entry, Strategy Convergence and the Erosion of Industry Profitability. Cass Business School (Paper). [ Links ]

13. Pettus, M.; Kor, Y. & Mahoney, J. (2009). A Theory of Change in Turbulent Environments: The Sequencing of Dynamics Capabilities Following Industry Deregulation. The International Journal of Strategic Change Management, 1 (3), 186-211. [ Links ]

14. Porter, M. (1996). Estrategia Competitiva. Mexico: Compañía editorial continental. [ Links ]

15. Porter, M. (2000). El camino que conduce a la diferenciacion. Gestion 5 (1), 146-152. [ Links ]

16. Porter, M. (2008). The Five Competitive Forces That Shape Strategy. Harvard Business Review, 78-93. [ Links ]

17. Ramos, A. & Ruiz, J. (2004), Changes in the Intellectual Structure of Strategic Management Research: A Bibliometric Study of the Strategic Management Journal, 1980-2000. Strategic Management Journal 25, 981-1004. [ Links ]

18. Restrepo, L. & Rivera, H. (2008). Analisis estructural de sectores estratégicos. Segunda edición. Fondo editorial Universidad del Rosario. Bogotá. [ Links ]

19. Rivera, H. & Malaver, M. (2008). Longevidad Empresarial. Universidad del Rosario; Documento de Investigación No 43. [ Links ]

20. Tan, J.; Li, S. & Li, W. (2006). Building Core Competences in a turbulent Environment: An Exploratory Study of Firm Resources and Capabilities in Chinese Transitional Economy. Managing Global Transitions, 4 (3), 197-214. [ Links ]