English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

Permalink

1. Introduction

Accounting research in Colombia has been developing because of external pressures to the accounting discipline and profession, which have been largely related to institutional demands and policies associated with processes to strengthen research in Higher Education Institutions (HEI) Patiño, Valero, García, and Díaz, (2016). On the other hand, the calls for measurement of research groups established by the new Ministry of Science, Technology, and Innovation -Minciencias- have directed and determined the formalization of research in the Country. However, the research work has fallen into the complexity of research management, that is, in establishing a series of strategies that guarantee, among many other things: visibility, citation, impact and implicitly funding, leaving research in the background. with social relevance and knowledge of the different members that make up the research community (Machado, Patiño and Cadavid, 2016).

In Colombia, a significant number of studies have been developed around accounting research; however, for this document, research will be understood as the integration of two academic trends, on the one hand, formative research and on the other, research developed by professors (Patiño, Romero, and Jara 2010). Both types of research have in common that they are developed in Higher Education Institutions; formative research is the first step in the training of researchers; it is the raw material of subsequent formal research (Valero and Patiño, 2012). In this work, institutionally formalized research is analysed through groups, lines, research projects, researchers, and publications; that is, to research directly influenced by the guidelines of Minciencias.

Clearly, the approach that has had the most force in the development of formal research in Colombia has been mediated by the technical conception, which has been led and directed by the Administrative Department of Science, Technology, and Innovation, Colciencias, then from the Law 1951 of 2019 is transformed into Minciencias, providing the necessary conditions for advancement in science, among others. In general terms, Minciencias is the one who manages everything related to formal research in the country, also performs categorizations through the Calls for Measurement of Research Groups and Recognition of Researchers, which have been based on the respective Model of Measurement, which has been evolving since its first version in 1991.

In this regard, it is relevant to mention that the group measurement calls have been generating significant pressure on Colombian universities to carry out institutional efforts related to creating, strengthening, and consolidating research groups. On the other hand, criticism of the model and its measurement criteria have been frequent, especially due to increasing demands on publication in Web of Science and Scopus journals found in the Q1, Q2, Q3 and Q4 quartiles. The increase in the level of demand is one of the great challenges for the accounting research community, which has forcibly become familiar with the 126 accounting journals registered in SCImago Journal Rank (SJR), not all specialized in accounting (Macías, 2016).

Regarding researchers, some criticisms are related to the criteria for their recognition and classification into “emeritus”, “senior”, “associate” or “junior”, as has been done since 2015, according to production and trajectory (Departamento Administrativo de Ciencia, Tecnología e Innovación [COLCIENCIAS], 2015, p. 44). The foregoing implies considering a series of specific paths of the Colombian accounting researchers, among which it stands out to be able to internalize the dynamics of the investigation that are interwoven internationally and that are followed by Minciencias in such a way that they can be linked and contribute (Macías, 2016). In this regard, Rueda (2007) envisions interpretive research as a perspective that could empower accounting research in the country to the extent that it responds to social needs.

The main differential aspect of this work is the systematic review of the information registered by the groups in GrupLac, differentiating the accounting groups from those interdisciplinary groups that develop a line of accounting research but are dedicated to disciplines such as economics or management. This article identifies the current state of Colombian accounting research groups and contrasts it with previous studies. In addition, it will be possible to “identify challenges and make an improvement proposal based on Colciencias guidelines” (Macias, 2016, p. 41). The paper does not aim to idealize measurement models since they have various restrictions; however, it is a way of identifying the state of accounting research since there is no other more complete basis on the matter.

The following section presents a literature review, followed by a methodological description, which focused on the document review technique. Subsequently, the research results are presented, including the following categories: research groups, active researchers, research lines and publications of the research groups. Finally, conclusions and discussion are presented.

2. Literature review

In the first decade of this century, the research groups attached to the Public Accounting programs began to be formalized in Colciencias. Initially, it went from a single recognized group in 2004 to 11 in 2006 and 33 in 2008. Of these 33 groups recognized and ranked in 2008, 21 (64%) were still in category D, which was the category lowest at that time (Macias, 2016; Macias and Cortés, 2009). In other words, accounting research was beginning to be formalized in Colciencias (today Minciencias), with a concentration of groups in the southwestern part of the country.

In the 2010 Colciencias classification, the number of groups rose to 61, of which 48% had been created between 2002 and 2004 (Valero and Patiño, 2012, p. 188). Of these 61 groups, 34 (56%) were in category D, and an additional 13 (21%) were recognized but not ranked. In other words, progress was being made slowly in the qualification process. The groups that appeared in the highest categories of the ladder were still those formalized in the 2006 and 2008 rankings.

The Colombian accounting tradition, more linked to oral debates than written discussions (Macias and Patiño, 2014, p. 22), has not allowed research groups to achieve the necessary productivity to grow in number and, above all, in level ladder (Macías, 2016). In 2010 there were already 528 researchers linked to the groups, many of them with master’s degree training and a small number with doctoral training. However, this training had a medium (and not high) impact on the productivity of teachers and the groups to which they belong (Valero and Patiño, 2012). In the article by Beltrán and González (2017), Colombian accounting researchers maintained low academic productivity between 2011 and 2015. In other words, the limitations of tradition were compounded by low levels of doctorate training, as well as low contribution to the productivity of the groups.

Fortunately, since 2017 it began to venture into publication in international accounting journals, such as Meditari Accountancy Research (Macias and Farfan-Lievano, 2017), Accounting Education (Sangster, Stoner, and Flood, 2020), Public Money & Management (Arias-Bello, 2020), Journal of Cleaner Production (Serrano-Cinca, Gutiérrez-Nieto, and Reyes, 2016; Correa-García, García-Benau, and García-Meca, 2020), Sustainability (Correa-García, García-Benau, and García-Meca, 2018) and the main accounting history journals: Accounting History (Quintero, 2020) and Accounting History Review (Rico-Bonilla, 2020). This, coupled with a boom in doctoral training during the second decade of the century, led to the fact that participation in this type of publication will multiply (Macias, 2019).

In addition to the contributions of high-level training to productivity, steps have also been taken on formative research. Many works have been published, ranging from analysis in specific academic programs to analysing the phenomenon throughout the country. Among the first, a review of the strategies in the country stands out (Patiño and Santos, 2009), later the analysis in the formative research in a program in the city of Cartagena (Guacarí, Espinel, and Ramos, 2013), in a Public Accounting program at two different universities in the city of Cúcuta (Avendaño, Rueda, and Paz-Montes, 2016; Carvajal, 2016) and at the University of Antioquia (Castaño, 2019). Throughout the country, the presence of formative research in the study plans has been analysed (Patiño, Melgarejo, and Valero, 2017) and the perception that graduates have about their training in research (Patiño, Melgarejo, and Valero, 2019).

Two lines of research have been consolidated in national discussions, and another is emerging in international contributions. At the national level, the main lines have been “accounting theory” and “accounting education”, not only since its declaration within the research groups but it has also been verified in the publications (Macias and Patiño, 2014; Beltrán and González, 2017). At this same level, a line of research in International Financial Reporting Standards (IFRS) is emerging, with the participation of academics from all over the country (Cruz, Roncancio and Camargo, 2020). Most of the publications in high-impact journals follow the line of social and environmental accounting at the international level, emphasizing the non-financial disclosures that large Colombian companies are making (Gómez and Quintanilla, 2012). This line is still emerging in Colombia (Rodríguez and Valdés, 2018), and it is expected to be consolidated through projects.

3. Research Group Measurement Model and Recognition of Researchers - Minciencias

The Model for Measurement of Research, Technological Development or Innovation Groups and Recognition of Researchers from the National System of Science, Technology and Innovation in Colombia arose with the main purpose of:

Identify which are the institutions and people that participate in research and development activities in the country, establishing what they produce; how do they do that; what kind of product they get; what human talent they form; how do they relate to each other; and, in general, what is the dynamics of their activity (Colciencias, 2018, p. 11).

Clearly since the first classification the Model has changed significantly. However, adjustments and modifications will be made from the 2015 Model, in which significant changes are made that involved three major phases: the first phase focused on the Construction of the Model between 2010 and 2011, with the respective disclosure between the scientific and academic community during October 2011 and September 2013. The Model was then implemented through Call 640 of 2013 and 693 of 2014. Finally, in the third phase, adjustments were made because of the latest calls and the “Roundtable of Arts, Architecture and Design” (Colciencias - Dirección de Fomento a la Investigación, 2016). However, it is important to clarify that other instances have been defined between the different calls, as is the case of the “Technical Roundtable of Public Research Institutes on the Model of Groups and Researchers”, constituted in the second quarter of 2018 with “representatives from different public research institutes to work on proposals for the incorporation of the institutes’ own CTeI production”(Colciencias, 2018b, p. 2), from which a series of adjustments were made that were evidenced in Call 833 of 2018.

Among the main changes that the Colciencias Measurement Model (2013, 2014, 2015, 2016, 2017, 2018) has reflected in the last decade, it is worth mentioning the redefinition of the research group as a “set of people who interact to investigate and generate knowledge products in one or more topics, by a short, medium or long-term work plan (aimed at solving a problem)” (Colciencias, 2018a, p. 44).

In the same way, the generation of a structure of co-responsibilities of the information contained in the CvLac and the GrupLac goes from the individual to the group and finally to the institution that endorses it. On the other hand, it is established that the validity of the recognition of the groups is annual, as a strategy to keep the information of the groups updated. As of Call 781 of 2017, category D is eliminated from the ranking of the groups, leaving categories A1, A, B and C. Considering the above and taking into account the different conditions that must be met for the measurement process and Recognition, the Colciencias Model “has become a parameter to be met by the various research groups that have been increasingly in less quantity in a sacrifice that shows little correlation with quality” (Machado et al., 2016, p. 75).

The people were classified into researchers, researchers in training and personnel linked to the groups, considering their training, production and trajectory. The researchers were classified as emeritus, senior, associate, or junior. Researchers in training were classified as a doctorate, master, or young researchers. The other members of the groups are undergraduate students or related members. Call 693 of 2014 began to rank investigators. Another change was the inclusion of the ORCID digital identifier in the general data (Mosquera, 2018) and the Scopus ID. In turn, the publication of the H5 index that the researcher has is possible as a way of making visible “the quantity (productivity) and quality (impact) of the author’s scientific production” (Rojas, 2017, p. 5), in the last 5 years. It is not clear if this last aspect will be a new criterion to be included in recognition of the researchers.

Faced with the different versions and from the accounting academy, the Research Group Measurement Model has been the subject of a significant number of observations and objections, among these approaches that Machado et al. (2016), who, in the face of accounting research, state that:

Despite being an evaluation system that tends for quality, it is questionable whether it is measured with criteria imposed based on requirements taken from other geographical and cultural settings, with variable, unstable models. In addition, the model measures short-term results based on the investigative logics of the hard sciences, ignoring the particularities of some disciplines such as accounting and ignoring the processes of construction of the investigative culture (p. 75).

Thus, formal accounting research is increasingly subject to more robust measurement models that inexorably entail greater demands. In this regard, it is important to mention some of the shortcomings identified by Machado et al. (2016) and Patiño et al. (2010): Lack of adequate institutional conditions and structures that promote the design and execution of research in HEIs, difficulty in accessing resources that allow the different research projects to be carried out, the accounting discipline is relegated compared to other forms of knowledge that they are considered strong sciences, in a more direct relationship with Colombian accounting academics. In addition, there are some latent weaknesses such as most do not dominate alternative languages to Spanish, low offer and specialized postgraduate training, low business experience, low time dedication to research and low production of new knowledge in top journals such as those included in the Web of Science and Scopus.

4. Methodological approach

The study is considered from a qualitative perspective, in which social phenomena are interpreted and understood; it is based on the generation of flexible data and analysis from the context (Vasilachis, 2009). The phenomenon studied is formal accounting research in Colombia. The current conditions of research groups, researchers, research lines and some publications made up to 2019 are analysed.

The data was taken from two of the Minciencias platforms: GrupLac and Cvlac. GrupLac is the tool that has the information from the research groups formally registered in Colombia. CvLac has the information from the resumes of formally registered researchers. In these two databases, it was possible to access the information registered by the researchers until 2019. Both are free-use tools to consult the information of research groups and researchers.

To identify the research groups on accounting issues, the presence of the words accounting, accounting, accounting, auditing, tax, costs, auditing, accountability, management accounting and control was used as a criterion (Valero and Patiño, 2012) in group names. Subsequently, the database was supplemented with information on registered research lines, projects, and production to exclude groups that are not countable, despite their name. The consultation process on the Minciencias platform was carried out between February 19 and March 12, 2020, to include the results of the Colciencias 2018 measurement, which is the most recent.

After identifying the groups, the data of the group name, classification, year of creation, department, city, name and gender of the group leader, the institution that provides the endorsement, research lines, members with their category, publications with the main data such as the journal, the year, and the training of the researchers. Those developing research lines such as financial accounting, taxation, control, management accounting, accounting education, and environmental accounting were classified as accounting groups. These lines coincided with those identified in the article by Valero and Patiño (2012) and were added with the emerging lines of accounting research, accounting theory and finance.

Finally, the research groups identified were reduced from 195 to 151 groups by eliminating those that did not have any accounting product. Subsequently, it was observed that there were interdisciplinary groups whose production associated with accounting issues is deficient. Those with accounting products (books, articles, and book chapters) equal to or greater than 30% of their total products were classified as accounting groups. This percentage allows us to include groups that have been considered accounting groups in past studies and exclude interdisciplinary groups with marginal contributions to accounting.

After this analysis, 64 research groups that develop accounting research were identified. Subsequently, 46 interdisciplinary groups were identified that have between 10% and 30% of accounting products. In this article, strictly accounting groups are analysed, and the analysis of interdisciplinary groups that contribute to accounting discussions in Colombia remains for later work.

To determine the products corresponding to each group, those registered in the GrupLAC were taken; they are classified as accounting and those that do not correspond to the discipline (interdisciplinary). The groups were classified into the categories described, and an analysis was carried out by groups, active researchers, research lines and publications.

5. Results

5.1. Research groups

For the year 2019, 110 research groups address accounting issues, which were also active and endorsed by an institution. Of these 110 groups, 64 are accounting groups with accounting products greater than 30%, and 46 groups are interdisciplinary, with accounting products between 10% and 30% of the total. The 64 accounting research groups are presented in Graph 1: year of creation between 1995 and 2019; largest number created between 2007 and 2017; 2016 with the largest number of groups created, among others. In short, in the last 12 years, half of the accounting research groups have been created.

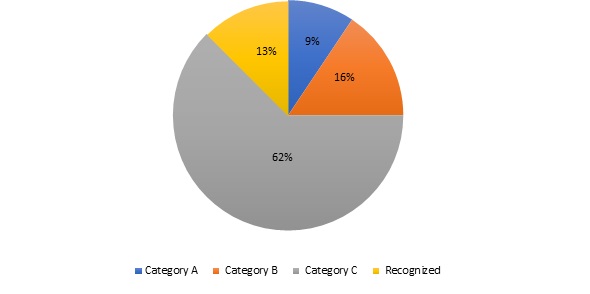

Regarding the categorization of accounting research groups, Graph 2 highlights that the majority are in Category C with 62%, and 40 groups are in the lowest category. There are no groups in Category A1 in this measurement, the highest category in the Colciencias 2018 measurement

Regarding the location, the accounting research groups are in 18 departments of Colombia, according to Table 1. Bogotá stands out with the highest number of groups (37.5%), and adding Valle del Cauca and Antioquia, these three regions represent more than half (56.3%) of the accounting research groups. When reviewing the groups classified in category A, Bogotá has 3, while Antioquia, Cauca, and Atlántico each have one group.

Table 1 Classification of accounting research groups by department 2019

| Department | Classification | Accounting Groups | % | |||

|---|---|---|---|---|---|---|

| A | B | C | Recognized | |||

| Bogotá, D. C. | 3 | 4 | 17 | 0 | 24 | 37,5 |

| Valle Del Cauca | 0 | 0 | 6 | 1 | 7 | 10,9 |

| Antioquia | 1 | 2 | 2 | 0 | 5 | 7,8 |

| Boyacá | 0 | 0 | 3 | 1 | 4 | 6,3 |

| Nariño | 0 | 1 | 1 | 1 | 3 | 4,7 |

| Santander | 0 | 1 | 2 | 0 | 3 | 4,7 |

| Cauca | 1 | 0 | 1 | 0 | 2 | 3,1 |

| Norte De Santander | 0 | 0 | 1 | 1 | 2 | 3,1 |

| Quindío | 0 | 0 | 2 | 0 | 2 | 3,1 |

| Caquetá | 0 | 0 | 2 | 0 | 2 | 3,1 |

| La Guajira | 0 | 0 | 1 | 1 | 2 | 3,1 |

| Cesar | 0 | 0 | 2 | 0 | 2 | 3,1 |

| Meta | 0 | 0 | 0 | 1 | 1 | 1,6 |

| Atlántico | 1 | 0 | 0 | 0 | 1 | 1,6 |

| Tolima | 0 | 1 | 0 | 0 | 1 | 1,6 |

| Chocó | 0 | 0 | 0 | 1 | 1 | 1,6 |

| Caldas | 0 | 1 | 0 | 0 | 1 | 1,6 |

| Bolívar | 0 | 0 | 0 | 1 | 1 | 1,6 |

| TOTAL | 6 | 10 | 40 | 8 | 64 | 100,0 |

Source: Own elaboration based on the Colciencias 2018 measurement.

Regarding the groups, it is important to point out that the study carried out in 2010 (Valero and Patiño, 2012) identified 61 groups with products related to the accounting discipline. Now, 64 groups with accounting products greater than 30% have been identified; in addition, 46 other interdisciplinary groups were identified, which have between 10% and 30% of accounting products. There is a significant increase in the groups, although the methodologies are slightly different.

5.2. Active researchers

The 64 accounting research groups have 703 current members, of which 74% are not categorized in Minciencias. It is also found that, of the 15 senior researchers, 12 are linked in accounting groups classified in category A, 1 in B and 2 in C. It is striking that the only emeritus researcher in measurement, Colciencias, is linked to two investigation groups. By detailing his profile, it is found that his investigations correspond to energy and mining issues, so that he has obtained this recognition and category for issues that are not related to accounting.

Concerning associate researchers, 60 people represent 8.5% of the total. Almost half (27) are linked to accounting research groups with category C. Similarly happens with junior researchers (105), who represent 14.9%; still, more than half (59) are linked to accounting research groups in category C, as seen in Table 2.

Table 2 Category of active researchers 2019

| Researcher categories | Accounting research groups categories | Total | % | Group leader | |||

|---|---|---|---|---|---|---|---|

| A | B | C | Recognized | ||||

| Emeritus researcher (ER) | 0 | 0 | 0 | 1 | 1 | 0,1 | 0 |

| Senior researcher (SR) | 12 | 1 | 2 | 0 | 15 | 2,1 | 3 |

| Associate researcher (AR) | 17 | 15 | 27 | 1 | 60 | 8,5 | 13 |

| Junior researcher (JR) | 13 | 29 | 59 | 4 | 105 | 14,9 | 14 |

| Without category | 66 | 75 | 305 | 76 | 522 | 74,3 | 34 |

| TOTAL | 108 | 120 | 393 | 82 | 703 | 100,0 | 64 |

Source: Authors’ own elaboration.

When analysing the 64 leaders of accounting research groups, it is found that 53% do not have a category in Colciencias, 22% are junior, 20% are associates, and only 5% are senior researchers. In other words, of the 15 researchers who belong to this last category, only 3 are leaders in their groups. Likewise, we found that 77% of the leaders are Public Accountants, and 45% are women. Finally, we found that accounting research groups are concentrated in 8 Universities, with 33 groups representing 50% of accounting research groups in the country.

5.3. Research lines and publications of research groups

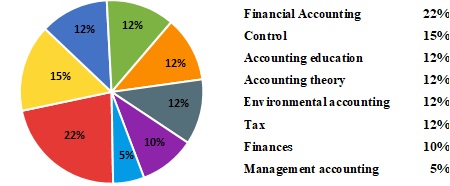

The lines of research are thematic areas of greater importance for the discipline; therefore, they indicate trends in the interests of the research community. Each research group establishes these to correspond to 221 for the total of the 64 accounting groups. Of these, 79% of the lines are related to the accounting discipline and 21% in complementary matters. The research lines were grouped according to the criteria established in the methodology.

It should be noted the theme of the most frequent line of research groups is financial accounting. The others have relatively homogeneous participation, highlighting that the least frequent is management accounting, according to what is presented in Graph 3.

Regarding the production of the accounting groups, it is identified that the most representative is articles (62%), book chapters (22%) and books (16%). Concerning the distribution of the topics of the publications, it is found that in the 64 accounting research groups, 52% of the production is articulated in topics of the accounting discipline and 48% in different areas such as economics or administration.

When reviewing the production of books, chapters, and articles by areas (Table 3), highly variable results are presented between the various topics. The area with the highest participation is financial accounting, which coincides with the most recurrent line of research. It is also appreciated that management accounting has an important participation in the articles, although as a line of research, it is not representative.

Table 3 Distribution by areas of publications 2019

| Area | Articles (%) | Chapters (%) | Books (%) |

|---|---|---|---|

| Financial accounting | 30 | 21 | 27 |

| Accounting theory | 15 | 18 | 16 |

| Management accounting | 12 | 6 | 10 |

| Accounting education | 12 | 22 | 9 |

| Control | 7 | 9 | 15 |

| Accounting research | 7 | 8 | 11 |

| Environmental accounting | 6 | 8 | 5 |

| Taxation | 6 | 8 | 4 |

| Finance | 4 | 1 | 4 |

| Total | 100 | 100 | 100 |

Source: Authors’ own elaboration.

When reviewing the products of the research groups by location, it is evident that the departments with more groups have more products. Each research group has an average of 40 products and publishes 3 per year. Furthermore, Atlántico is the department with the highest average of products per year (8), followed by Antioquia (6) and Caldas (5). Although Bogotá has the largest number of research and product groups, the average value of products by groups would be expected to be high; however, it has a value of 3, within the total average. Not all accounting research groups publish with the same frequency (Table 4).

Table 4 Distribution of products by departments and institutions

| Departments | Groups | Products | Average products per group * | Average products per year ** |

|---|---|---|---|---|

| Bogotá, D. C. | 24 | 898 | 37 | 3 |

| Valle del Cauca | 7 | 501 | 72 | 4 |

| Antioquia | 5 | 429 | 86 | 6 |

| Nariño | 3 | 121 | 40 | 2 |

| Quindío | 2 | 119 | 60 | 4 |

| Cauca | 2 | 117 | 59 | 3 |

| Atlántico | 1 | 99 | 99 | 8 |

| Caquetá | 2 | 87 | 44 | 3 |

| Caldas | 1 | 76 | 76 | 5 |

| Boyacá | 4 | 43 | 11 | 2 |

| Santander | 3 | 34 | 11 | 1 |

| Chocó | 1 | 18 | 18 | 3 |

| Norte De Santander | 2 | 12 | 6 | 2 |

| Bolívar | 1 | 9 | 9 | 1 |

| La Guajira | 2 | 9 | 5 | 1 |

| Cesar | 2 | 8 | 4 | 1 |

| Tolima | 1 | 7 | 7 | 1 |

| Meta | 1 | 3 | 3 | 1 |

| TOTAL | 64 | 2590 | 40 | 3 |

Source: Authors’ own elaboration.

6. Discussion and Conclusions

When approaching this section, there are two important elements about works with similar scopes that link the research groups; these are the methodology to determine groups under study and the measurement criteria reconsidered in the calls of Minciencias. The relationship between these two variables generates dynamism in the results of similar works.

A contribution of this research is to improve the selection criteria and increase the information analysed. It is possible to separate the accounting research groups from interdisciplinary groups with accounting products. Although the results presented in other studies on accounting research groups (Rueda, 2007, Macías and Cortés, 2009, Valero and Patiño, 2012, Macías, 2016) are determined with different methodologies, it is evident that there has been growth in the number of research groups dealing with accounting issues in the last 12 years. The number of groups is low compared to other disciplines (Rueda, 2007), but most were created between 2007 and 2017, increasing soon.

Although in 2004, only one accounting research group was recognized by Colciencias (Macías and Cortés, 2009), 22 accounting research groups had already been created (Graph 1). Macias and Cortés (2009) identified 33 accounting research groups ranked in 2008: 1 group in category A1; 2 groups in category A; 4 groups in B; 5 groups in C and 21 groups in category D. The new methodology identifies 37 research groups in 2008 (Graph 2); the difference may be due to the inclusion of groups not recognized at the time.

Similarly, when crossing the accounting research groups of the Colciencias 2019 call with the 2010 measurement, which identified 61 groups (Valero and Patiño, 2012), only 17 groups have remained (Annex 1), most have been created in the last decade.

Another important finding is that the preferred lines of research have changed in the last decade. In the first place, the most preferred line in 2010 was accounting education, with 21% (Valero and Patiño, 2012). However, the highest publications in accounting journals between 2011 and 2015 were financial accounting (Beltrán and Gonzáles, 2017). Now, the line of environmental accounting has taken on importance (12%), from low participation in previous studies, only 3% (Valero and Patiño, 2012). Only the participation of management accounting is preserved, which is the line of least interest for researchers.

On the other hand, it is necessary to mention that research lines provide thematic guidelines agreed by the groups, but the research products may differ. Thus, when reviewing the thematic areas of the publications, financial accounting is the one that is published the most in articles and books and is second in research chapters, followed by accounting theory. The accounting education line is the preferred line for chapters, and the finance line is the least interesting for research articles, chapters, and books.

Likewise, in the publications of the accounting groups, the majority are articles, followed by chapters and research books. This result is similar that found in Valero and Patiño (2012) work, which indicates that the production strategies have been maintained in recent years, determined by the percentage weights of these products in the measurement model.

Finally, Bogotá continues to be the region with the largest accounting research groups in the country, with 24. However, the department with the highest average of products is Atlántico, followed by Antioquia and Caldas. This shows that the regions that have more research groups do not necessarily have a higher average of products. It is considered that the average number of products per year is a better approximation to the performance of the accounting research groups.

For future research, the study of interdisciplinary groups is proposed and continue with the permanent updating of this study to have inputs in other accounting research studies. On the other hand, based on the results of this article, it is proposed to develop research from a critical or interpretive perspective. Thus, a more in-depth analysis could be achieved that allows to detail the causes of the results and even determine factors of the Minciencias model that can negatively influence university research.