English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

PermalinkINTRODUCTION

In recent years, several developing countries have started a process in order to be accepted as members of the Organisation for Economic Co-operation and Development (OECD). Some of these economies, for example the Latin American ones, clearly do not fulfil the development standards that have been achieved by traditional OECD members. However, both the organization and the applicants refer to this initiative as an opportunity to revise governance practices and the institutional framework or, more generally, as a possibility to adjust growth and development strategies in middle-income economies.

The process includes the OECD delivering several economic policy recommendations and the candidates adopting benchmarks consistent with patterns already followed by the advanced economies. In regard to tax policy, for example, new members would be expected to have a tax structure less dependent on indirect taxes. While the ratio of indirect taxes to direct taxes was 1.05 in 2016 for OECD economies, that ratio was 2.52 for Non-OECD countries. The literature seems to contain recommendations in favour of more direct taxes and also claims that indirect taxes may limit the scope of after-tax redistribution. Opponents argue that indirect taxes are easier to collect in developing economies and redistribution policies could still occur through expenditure, not only through taxes.

However, in regard to the tax structure, direct redistribution is not the only aspect that should be considered. A tax structure may also affect how economies stabilize their output fluctuations that are often caused by external shocks in the case of developing economies. In fact, it is well known in the literature that (i) the macroeconomic performance in developing economies is volatile and sensitive to external shocks, and (ii) taxes can be automatic stabilizers of output fluctuations (i.e. the role of taxes in the Keynesian multiplier). In the absence of solid social safety nets and consumption-smoothing mechanisms in developing economies (i.e. access to credit), income volatility might lead to deeper asymmetrical welfare effects among "rich" and "poor". Likewise, other phenomena such as unemployment hysteresis might deepen the negative welfare effects of the downturns. Undoubtedly, the role of the tax structure as a macroeconomic stabilizing mechanism is relevant. And, obviously, the motivation for and the importance of this topic go beyond the discussion on OECD membership.

Specifically, this paper attempts to empirically examine if the tax revenue structure (composition), in terms of indirect taxes vis a vis direct taxes, amplifies or mitigates the effect of terms of trade shocks on output fluctuations. Although we recognize the existence of other external shocks (i.e. U.S. interest rates) that can foster capital account flows and cyclical variations of output, our focus on the terms of trade responds to the well-established role of this variable as a key determinant of output fluctuations in developing countries. This will be discussed in more detail in the next section. Our empirical strategy consists of an econometric estimation that the amplifying effect of the tax structure has on the effect of a terms of trade shock on annual growth rates in 51 countries included in the Revenue Statistics Dataset (Organisation for Economic Cooperation and Development (OECD)), which is the largest source of comparable tax revenue data. The baseline regression includes an interaction term composed by an indicator of the terms of trade and a proxy of the tax structure (composition) in order to examine the amplifying/mitigating role of the tax structure.

The following sections succeed this introduction: related literature, data description, econometric strategy, estimates, and conclusions.

RELATED LITERATURE

Many countries have ahigh degree ofmacroeconomic external vulnerability. Macroeconomic shocks, for example, originate in international markets, where open-small economies have negligible market power, or as the consequence of changes in advanced economies' economic policy (e.g. U.S. interest rates). Indeed, these shocks may have both a short and long-term effect by altering the business cycle and economic growth trends (Agénor, McDermott, & Prasad, 2000; Aiolfi, Catão, & Timmermann, 2011; Basu & McLeod, 1991; Hoffmaister & Roldos, 2001; Kose & Riezman; 2013; Osterholm & Zettelmeyer, 2008). Latin America, an example of the developing world, provides evidence that highlights the role of business cycles' external determinants (Hernández, 2018; Osterholm & Zettelmeyer, 2008). Osterholm and Zettelmeyer (2008) show that between fifty and sixty percent of the variation in Latin American annual GDP growth is accounted for by external shocks. Furthermore, Aiolfi, Catão, and Timmermann (2011) observe the commonality of the output fluctuations across Argentina, Brazil, Chile, and Mexico and highlight the importance of external global factors in explaining this common regional cycle.

The set of external shocks that can foster cyclical variations in domestic output is wide; however, our focus on the terms of trade responds to the well-established role of this variable as a key determinant of output fluctuations in developing countries. For instance, Mendoza (1995), provides evidence suggesting that terms of trade shocks may account for between 37% and 56% of the actual variability of the GDP in developing countries. In his intertemporal model, the main mechanism explaining the relationship between terms of trade shocks and output variation is the following: positive terms of trade shocks lead to an increase in the marginal profitability of the exportable sector, followed by an investment boom that accelerates the economy as a whole. The model also allows for a Dutch Disease mechanism: the positive terms of trade shock may be followed by an appreciation of the exchange rate, which has a negative effect on export competitiveness.

Other studies have also estimated the effect of terms of trade shocks (Broda, 2004; Hernández, 2013; Hoffmaister & Roldos, 2001). Hernández (2013), for example, estimates that one third of the variability in the short run output in Colombia is explained by changes in the terms of trade. The econometric estimations of the magnitude of that effect usually depend on the assumption of exogeneity of the terms of trade shocks. Although our empirical strategy in this document does not rely on this assumption, it is worth mentioning since some of the regional sub-samples analysed in this article are more likely to comply with that assumption. In fact, the assumption of exogenous terms of trade in developing economies is certainly reasonable since small economies face an infinitely elastic external demand for their goods and an infinitely elastic supply of imported goods. Despite some well-known exceptions (for example, Broda, 2004), which find a less severe effect of the terms of trade on output fluctuations, especially in countries with flexible exchange regimes, most of the literature suggests a positive effect of terms of trade on output fluctuations in developing countries, at least in the short-term. In the medium or long-term, Dutch Disease mechanisms may revert the initial positive effect.

Another reason to highlight the role of the terms of trade, in contrast to other external variables (i.e. financial variables), as a crucial source of domestic output variation has to do with recent developments in the financial configurations adopted by the monetary policy in developing economies, which have offered these economies additional protection before external financial shocks. Latin America is a clear example of this. After the "lost decade" (the eighties), characterized by particular sensitiveness to external financial shocks, most of the Latin American economies implemented a new financial configuration that includes a flexible exchange rate regime, free capital mobility, and an inflation target framework. According to Aizenman (2008), this setup requires an extremely conservative management of international reserves, which work as a collateral in the financial markets. As mentioned in Ocampo (2009), this conservative management of international reserves has protected Latin America from severe financial crisis spillovers in recent years; however, this has not limited domestic economies' exposure to trade shocks. These shocks are a crucial external element of domestic output fluctuations.

Empirical analyses of the terms of trade effect take into account a generous set of control variables, and some of the econometric techniques decompose the output variability in order to separate the effect of the terms of trade on output from other sources of macroeconomic fluctuations; however, these analyses do not explicitly show that the domestic policy (e.g. fiscal policy) may define a macroeconomic context that might amplify or buffer the external shocks (which is the purpose of this document). There are many contributions that examine the effect of fiscal policy, taxes and spending, and output and optimal tax rates (Arnold, 2008; Auerbach & Gorodnichenko, 2012; Blanchard & Perotti, 2002; Branson, & Lovell, 2001; Engen & Skinner, 1996; Gavin, Haussman, Perotti, & Talvi, 1996; Lee & Gordon, 2005; Jones, Manuelli, & Rossi, 1993; Perotti, 2012). These insights, in combination with studies on automatic stabilizers (for example, Andrés & Doménech, 2006; Auerbach & Feenberg, 2000), motivate an empirical analysis on domestic policy as a transmitter of the terms of trade shocks.

An empirical approach to estimate how much the tax structure amplifies or mitigates terms of trade shocks is particularly important for developing economies. It is well known that these economies are usually very sensitive to external shocks and have a negligible control on the shocks; however, their tax policy might be used as a macroeconomic instrument to stabilize the impact of those external shocks. Even if the fiscal policy is not primarily intended to be used as an automatic stabilizer, policy makers should understand the macroeconomic side effect of changes in the tax structure. Once again, especially in poorer economies, the macroeconomic impacts have a more profound effect on welfare since people are less likely to cushion the windfalls.

DATA DESCRIPTION

The main component of our empirical strategy is the econometric estimation of the effect of the tax structure as a potential amplifier/mitigator of terms of trade shocks. In order to develop this econometric exercise, we use panel data that includes 51 countries and a time series from 1990 to 2016 (the most recent year that is available with updated information).

The size of the panel is basically determined by available information in the OECD dataset on tax revenues. This dataset is known as the most comprehensive source of tax information that allows comparisons across countries. Our sample includes information for countries that are classiied in different ranges of income (e.g. middle-income economies or high-income economies).

The OECD dataset has 4-digit level information in regard to the different sources of tax revenues; however, we only focus on two main categories: Taxes on Goods and Services (code 5000) and Taxes on Income, Profits, and Capital Gains (code 1000). We use these two codes to construct a proxy for the tax structure that reflects the composition of tax revenues in terms of indirect vis à vis direct taxes. Concretely, TAX (tax structure) corresponds to the ratio between indirect tax revenues (Taxes on Goods and Services) and direct tax revenues (Taxes on Income, Proits and Capital Gains)

Figure 1 shows the TAX histogram for the pooled database. There are a wide range of TAX observations: from 0.13 (Venezuela, 1990) to 18.1 (Bolivia, 1992). The mean (1.75) is close to the median (1.26). TAX is equal to 0.82 in the upper limit of the lowest quartile and is equal to 2.09 in the lower limit of the highest quartile.

Table 1 reports the TAX mean in four arbitrary periods: 1990-1996, 1997-2003, 2004-2009, and 2010-2016. Although the last two periods might be considered as pre- and post-Great Recession time frames, the main purpose of this subsampling is to describe the TAX stability over time in certain selected countries. For period 2010-2016 (the most recent), Table 1 also shows information on other tax revenue indicators that is useful for a more complete characterization: (i) Taxes on Goods and Services as a proportion of Total Tax Revenues, (ii) Taxes on Income, Profits, and Capital Gains as a proportion of Total Tax Revenues, and (iii) Total Tax Revenues as a proportion of Gross Domestic Product (GDP). This descriptive table shows that, for OECD members, the average level of TAX has been quite stable. It was 1.06 in the 1990-1996 period and 1.11 in 2010-2016. Non-OECD economies report a significantly higher level of TAX: 4.48 in 1990-2016 and 2.13 in 20102016. The declining TAX trend in non-OECD economies is worth noting, especially from 1990 to 2009. Nevertheless, in general, lower-income economies rely more on indirect taxes.

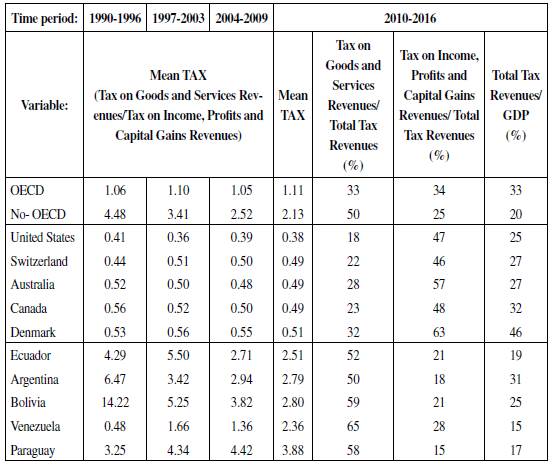

Table 1 Tax structure

Source: Elaborated by the authors, based on the OECD revenue statistics database.

Table 1 also displays information on some selected economies that may provide a clear example of the heterogeneity in tax structures. We chose the five economies with the lowest level of TAX in 2016 and the five economies with the highest level in the same year. Not surprisingly, the first group includes countries such as the United States, Australia, and Denmark. The second group comprises five Latin American countries: Ecuador, Argentina, Bolivia, Venezuela, and Paraguay. These Latin American economies, only with the exception of Venezuela, have experienced a declining TAX trend. Bolivia has a serious fluctuation in TAX from 14.22 in 1990-1996 to 2.80 in 2010-2016 (five times less). It is also worth noticing that tax revenues, as a proportion of the GDP, are on average higher in more advanced economies.

Regarding other Latin American countries, Chile and Mexico, which have been OECD members since 2010 and 1994, respectively, are among the economies that have lower reductions in TAX. This pattern might be explained by the fact that these two countries changed their tax structure before other Latin American countries did. In 1990-1996, both in Chile and Mexico, TAX was already below the region's average. For a more general picture on the potential role of being an OECD member, Figure 2 shows the time series for TAX in ten countries that were recently accepted as OECD members (the vertical line shows the year when membership was granted). Except in the case of Estonia, recent members had TAX ratios below two when they joined the organization. In some cases, TAX increased after membership was granted; Hungary, for example, reached a ratio of 2.5 in 2011. However, in general, for these recent members, TAX stayed at relatively low levels. Figure 2, which shows Chile and Mexico, indicates that their entry into the OECD was preceded by reductions of the size of indirect tax revenues in relation to direct tax revenues.

Source: Elaborated by the authors.

Figure 2 TAX (ratio Indirect Tax Revenues over Direct Tax Revenues). Countries that were accepted as OECD members after 1990. The vertical lines show the years in which the countries were accepted as OECD members

In regard to the key external macroeconomic shock, the introduction already mentioned that we would focus on the terms of trade. Terms of trade (TOT) series were obtained from the World Development Indicators (WDI) for OECD economies and from The Economic Commission for Latin America and the Caribbean (ECLAC) for Latin American economies. Figure 3 displays the TOT histogram. The distribution is centred at around one hundred (TOT is an index). One standard deviation is twenty points. The histogram clearly shows that most of the observations are in the range of the mean plus/minus two standard deviations.

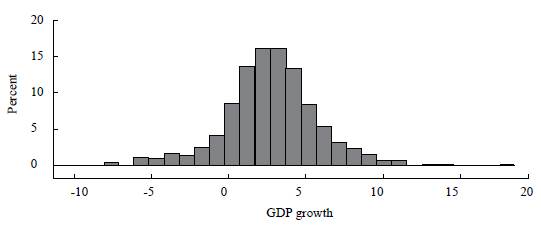

Since we evaluate the role of TAX before TOT shocks on output fluctuations, we use the GDP annual growth rates (World Development indicators) as a proxy of short-run output variations. This variable is named GRGDP. Figure 4 shows the GRGDP histogram. GRGDP observations range from -6.5 percent to 25.6 percent. GRGDP is centred around the mean (3 percent), the median is 3.1 percent.

Finally, besides our key variables, our panel data includes information on Domestic Credit as a Percentage of GDP (DOMCRED), Savings as a percentage of GDP (SAV_GDP), Trade balance as a Percentage of GDP (TB_GDP), Total Tax Revenues as a Percentage of GDP (TTR_GDP), and Government Spending as a Percentage of GDP (GOV_GDP). Some of these proxies correspond to other potential sources of external shocks that are different from the terms of trade; other variables characterize the general macroeconomic performance of the economy. For instance, Total Tax Revenues (as a proportion of GDP) might be especially important to test the robustness of the effect of the tax structure after controlling for the size of total revenues. It is possible that the tax structure is associated with the level of tax revenues as a proportion of GDP. Since this level may also be correlated with the annual growth rates, our coefficient associated with TAX might be biased if Total Tax Revenues were omitted. Likewise, Government Spending may react to the business cycle. Fiscal policy, in general, may be conditioned to the macroeconomic context (Kaminsky, 2010; Vegh & Vuletin, 2015). Data for these control variables were obtained from the World Development Indicators. Table 2 summarises all the variables, definitions, sources, and coverage of the entire data-set described in this section as well as some groups of countries that will be considered in the following empirical strategy.

ECONOMETRIC STRATEGY

Our econometric strategy relies on the following econometric specification:

In addition to those variables already defined in section 3, TAX*TOT is an interaction term between the tax structure proxy (TAX) and terms of trade (TOT), Z is the set of control variables (DOMCRED, SAV_GDP, TB_GDP, TTR_GDP, and GOV_GDP), and ε j ,t is the error term.

Using panel data analysis, we estimate φ, γ, β, ρ, and δ and pay particular attention to the coefficient associated with TAX*TOT (ρ), which relates to the role of the tax structure as an amplifying/mitigating mechanism of terms of trade shocks

We use a Generalized Method of Moments (GMM) estimator instead of an Ordinary Least Square (OLS) estimator. An OLS estimator may lead to biased estimates for several reasons; we are particularly concerned about the potential endogeneity resulting from the fact that right-hand side variables might simultaneously be determined by the annual growth rates. Were that the case, the error term ε j ,t would be correlated with right hand side variables in equation (1). Although terms of trade (TOT) are usually assumed as an exogenous variable in some developing economies, characterized as price takers in international markets, this may not be the case in our full sample including high-income countries. Several of these economies, representing a big part of world's gross domestic product, depart from the assumption of perfectly elastic demand of their exports or perfectly elastic supply of their imports. The endogeneity problem is perhaps more pervasive in the case of our proxy for the tax structure (TAX). In fact, it would be unreasonable to assume that the tax revenue composition is neutral to the business cycle. Not only the tax base but also the tax rate, for both indirect and direct taxes, may react to output shocks. In particular, developing economies tend to display a pro-cyclical fiscal policy in booms and an a-cyclical fiscal policy in non-severe downturns (Kaminsky, 2010). Therefore, governments facing political pressure to maintain the spending level during the windfalls certainly use taxes while they are restricted by international financial markets to issue new debt. It is true that, to some extent, policy makers internalize the political and economic effects of these new taxes on the business cycles; however, they may prefer to focus on the objective related to collecting more revenues. This aspect is crucial in the discussions on tax reforms.

Once it is decided to increase tax revenues, "direct or indirect taxes?" becomes the key question. Both represent benefits and costs for the government, facing inside and outside lags in the implementation of the tax increase. For example, in spite of the fact that indirect taxes might lead to undesired income and wealth redistribution, since they are usually regressive, these types of taxes, at least in developing economies, are easier to collect than direct tax revenues. Perhaps, due to the severe inequality in income, wealth, and political power, tax evasion seems to be more pervasive in the case of direct taxes. To conclude this line of analysis, governments might favour indirect taxes over direct taxes during windfalls. As a conclusion, the tax revenue composition would change depending on the stage of the business cycle. On the other hand, since OECD members have lower levels of TAX than the non-OECD economies, countries attempting to be part of this organization are encouraged to reduce the dependence on indirect taxes.

We use the Arellano-Bover GMM estimator to deal with the potential endogeneity. Instruments are lagged with the dependent and independent variables in equation (1). The GMM estimator controls for two possibilities: (i) the possibility of non-orthogonal error terms due to the inclusion of the lagged dependent variable on the right-hand side of the regression: lags of the dependent variable lead to a dynamic/autoregressive model, and these lags may be correlated with the unobserved individual-level effect, (ii) the possibility for non-strictly exogenous explanatory variables. This GMM estimator is undoubtedly more robust than the OLS estimator in our empirical strategy, even for cases where panels have dimensions N > T (Roodman, 2006). It is well known that the Arellano-Bond estimator removes the unobserved effect after taking the first difference of equation (1); however, by construction, differences in the lags of the dependent variables will be correlated with the error term's differences (ε j ,t ). Therefore, the Arellano-Bond dynamic panel estimator uses higher order lags of the dependent variable besides the lags of the right-hand side variables to instrument TAX or TOT as well as the lags of the dependent variable.

The validity of the instruments is tested by the Sargan-test of over-identifying restrictions. Following Roodman (2006), if the model is over-identified, given the rank condition, a Wald test can be used to test the joint validity of the moment conditions. Similarly, following Arellano and Bond (1991), we also implement a serial correlation test on the residuals. First-order correlation is expected by construction; nevertheless, there must not be serial correlation in the order 2 error terms.

ESTIMATES

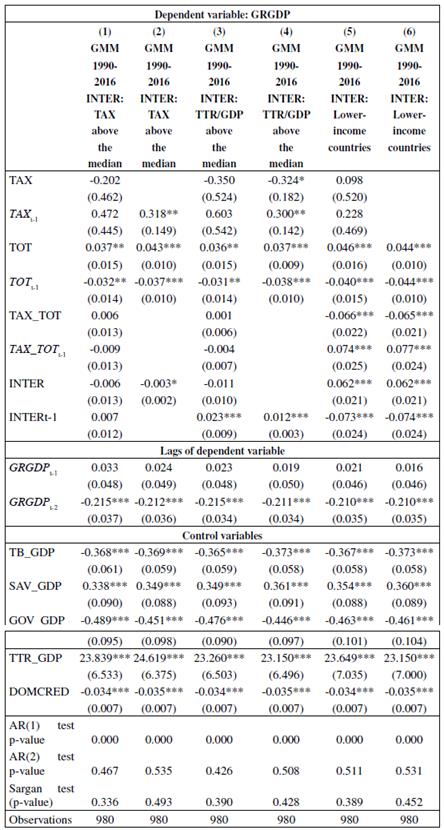

Table 3 summarizes the results obtained from our baseline regression. Column (1) reports the GMM estimates for the general econometric specification. This regression takes into account the set of control variables. The main result from this regression is the positive effect of TOT and the negative effect of lagged TOT on the annual growth rates of the GDP (GRGDP). The estimate associated with contemporaneous TOT (0.038) means that one standard deviation of TOT translates into 0.74 additional percentage points for the GRGDP. This effect is important. It corresponds to 22 percent of a GRGDP one standard deviation. This contemporaneous effect is reversed in the next year, given the negative estimate associated with the first TOT lag (-0.037). These estimates are consistent with a Dutch Disease effect following the positive contemporaneous effect of TOT. As mentioned in the literature review, the positive terms of trade shocks may lead to the appreciation of the exchange rate, which may then affect export competitiveness. Column (2) reports the results of a specific regression that is obtained after removing the right-hand side variables one by one that are not statistically significant in column (1). The purpose of this new regression is to examine a more parsimonious specification that avoids, to some degree, the variance inflation caused by many variables that could be correlated on the right-hand side. Column (2) confirms the interpretation provided in column (1).

Table 3 Estimates. Baseline regression

(t-statistic), *p < 0.10, **p < 0.05, ***p < 0.01.

Source: Elaborated by the authors.

Finally, in columns (3) and (4), Table 3 shows the estimates of the econometric specification applied to a subsample of countries in our dataset that were previously defined in Broda (2004) as economies facing exogenous terms of trade: Austria, Chile, Germany, Denmark, Hungary, Ireland, Italy, Netherlands, New Zealand, Poland, the Slovak Republic, the United States, Brazil, Costa Rica, Guatemala, and Nicaragua. This group of economies is quite heterogeneous in relation to the level of economic development. We decided to examine if the coefficients estimated in columns (1) and (2) were similar to those obtained in (3) and (4). Interestingly, the estimates are similar in magnitude and statistical significance. We see these results as potential evidence that favours the assumption of exogenous terms of trade although we are controlling for potential endogeneity with the GMM estimator. With regards to our key variable (TAX*TOT), estimates in columns (1) to (4) show an estimate that is not statistically significant at the 10 percent level.

We then explored potential heterogeneous effects in different sets (Table 4). Beginning with the baseline specification, we included the interaction between TAX and TOT (TAX*TOT)-our key variable to explore the potential magnifying/mitigation effect of the tax structure-and a dummy that is equal to 1 depending on the following characteristics: (i) when the country has a level of TAX that is above the median of the full sample in 2016, (ii) when observations are above the median of the level of total tax revenues as a proportion of the GDP, and (iii) for observations corresponding to lower-income countries (when the level of income is below the median of the full sample). Columns (2) and (4), which are the more parsimonious versions of the regressions in columns (1) and (3), try to capture the heterogeneous effects of TAX above the median and high-tax revenue countries, respectively. Results show significant estimates for the new interaction terms. The signs of these estimates are opposed to the signs of the estimates of TOT and the first lag of TOT. This econometric evidence suggests that in countries with a higher level of TAX or a higher level of tax revenues (as a proportion of GDP) a tax structure more oriented to indirect taxes tends to better mitigate the effect of terms of trade shocks.

Table 4 Estimates. Regressions with the interaction term INTER (TAX or TTR/GDP above the median, and Lower-income countries)

(t-statistic), *p < 0.10, **p < 0.05, ***p < 0.01.

Source: Elaborated by the authors.

The clearest analysis in order to evaluate the effect of the tax structure in developing economies can be obtained from columns (5) and (6), which report the specification that includes an interaction term to evaluate the role of TAX as an amplifying/mitigating mechanism in lower-income countries. It is worth mentioning that the distribution of TAX is described by a higher mean and variance in lower-income economies than in higher-income economies. The mean in the sample of lower-income economies is 2.58 and the standard deviation is 1.99: three and five times greater than the mean and the standard deviation of TAX in higher-income economies, respectively. The analysis for lower income economies contributes to alleviate the potential problem of endogeneity resulting from terms of trade variation caused by output fluctuations. In comparison to high income economies, developing economies may be characterized as primary commodity exporters with very low international market power. The results show that both the coefficient associated with the new interaction term and the estimate related to TAX*TOT are statistically significant.

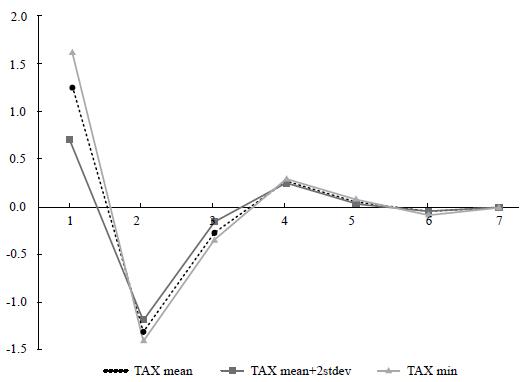

In order to provide a clearer picture of the dynamic effect of the terms of trade on the annual growth rates and the role of the tax structure, we used the estimates in column (5) to simulate the dynamic effect of a one standard deviation shock of the terms of trade on the annual growth rates. This simulation compares the effect in three scenarios that depend on the level of TAX: (i) for TAX at the mean of the sample for lower-income economies, (ii) for TAX at the mean plus two standard deviations of the sample for lower-income economies, and (iii) for TAX at the minimum level of the sample for lower-income economies. The mean plus two standard deviations (3.97) of TAX is 6.55 and TAX in the 75th percentile is 2.96. We did not use, for the last scenario, the mean minus two standard deviations, because that level is below the minimum value of the distribution. Figure 5 shows the results of the simulation. First, a tax structure more oriented toward indirect taxes better mitigates the volatility caused by a terms of trade shocks. For TAX in the level of the mean plus two standard deviations, after a 1 standard deviation shock in TOT, the additional annual growth rate in the first period would be almost 1 percentage point less than the annual growth rate if TAX were at the minimum level. In the second and the third period, since TOT leads to reductions in the annual growth rate, the higher TAX buffers the reductions. As mentioned before, this result is particularly important in developing economies where macro-economic volatility has deeper welfare effects on low-income or low-wealth citizens than in advanced economies. This evidence describes a potential cost that has not been explored when changes in tax structures favouring direct taxes are recommended.

Source: Elaborated by the authors.

Figure 5 Effect of a terms of trade (TOT) shock in Lower-income economies. Effect of TOT on the annual growth rates (GRGDP) for three scenarios: (i) TAX at the mean, (ii) TAX at the mean plus two standard deviations, and (iii) TAX at the minimum level in the sample of lower-income economies

Nevertheless, our results present a more complex dynamic effect. The buffering effect of TAX with regards to terms of trade shocks is not the only element to be highlighted from the simulation. Once the aggregate effect of a terms of trade shock on growth is calculated (for a 5-year period), we observe that a one standard deviation variation in TOT ends up at the same GDP level (before the shock) after 5 years, when TAX is at the mean level. If TAX was at the mean plus two standard deviations (6.54), the GDP would be 0.07 percent below its level before the shock. When TAX is at the minimum (0.13), the GDP level would be higher 0.04 percentage points. Therefore, a higher TAX stabilizes the volatility caused by the terms of trade shocks by further mitigating the positive effects of TOT on growth (rather than its negative effects). This less obvious effect should also be considered in potential analyses on the welfare effects of different tax structures in lower-income economies.

CONCLUSIONS

Developing economies have permanently been exposed to external shocks that determine their output fluctuations and, with a few exceptions, these countries resemble the assumptions of a small and open economy. Although these external shocks have originated from multiple sources, recent vulnerability to external shocks have mainly been associated with terms of trade. In the nineties, Latin America, for example, followed a new plan for its financial configuration based on flexible exchange rates, inflation targeting, and free capital mobility; the sustainability of this required a large international reserve hoarding. These reserves, in the framework of a conservative monetary policy, limited the possibility of a financial crisis in the region. Therefore, this configuration left the terms of trade as the key source of external shocks. In fact, part of the recent Latin American macroeconomic performance has been determined by the commodity price boom that started in 2003 and the deterioration of the terms of trade as a consequence of the Great Recession.

The exposure to external shocks in developing economies has been vastly covered in the economic literature. However, as far as we know, less attention has been paid to how the tax structure operates as a propagation mechanism of these terms of trade shocks. Since it is well-known that the Keynesian multiplier may be affected by taxes, it is reasonable to empirically explore if the tax revenue structure matters as an amplifier of these shocks to small and open economies.

The main purpose of this paper was to develop an empirical analysis of the role of the tax structure before terms of trade variations. In spite of the fact that this analysis includes high-income economies, we highlighted our result for lower-income economies, where terms of trade are more likely to be exogenous and the incidence of terms of trade shocks are relatively more important. Specifically, we found that a tax revenue composition more oriented toward indirect taxes buffers the propagation of terms of trade shocks on output fluctuations. When TAX is at the level of the mean plus two standard deviations, a one standard deviation shock in TOT leads to an additional annual growth rate in the first period that is almost 1 percentage point less than the annual growth rate if TAX were at the minimum level. Then, in the next periods (second and third), since TOT leads to reductions in the annual growth rate, the higher TAX buffers the reductions. The aggregate effect of a terms of trade shock on growth shows that a one standard deviation variation in TOT ends up with more growth after five years when TAX is lower. A higher level of TAX stabilizes the volatility caused by the terms of trade shocks by mitigating more the positive effects of TOT on growth rather than the negative effects. This effect should also be considered in potential analyses on the welfare effects of different tax structures in lower-income economies.

Econometric results in this document provide a clear policy implication in relation to recommendations of changing the tax structure to reduce the share of indirect taxes. Although it is well known that a tax structure favouring indirect taxes in developing economies creates the advantage of an easier tax collection, it also gen erates the cost associated with regressive taxes on the poor and the middle class, especially if this tax policy is not accompanied by fiscal spending oriented toward redistribution. In this regard, the OECD might be right in favouring a tax composition less dependent on indirect taxes. However, the effects of the tax structure as an amplifier of output fluctuations cannot be neglected. Our empirical strategy offers a result for our group of lower-income countries that is not obvious: changes in the type of tax revenue in favour of direct taxes bring higher macroeconomic volatility. Contrary to high-income economies, lower-income countries are characterized by incomplete credit markets and weak social safety nets. Therefore, the action of consumption-smoothing mechanisms is limited, and these developing economies face adverse welfare effects derived from macroeconomic volatility.