English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

PermalinkINTRODUCTION

Inflation was brought down and sustained at single-digit-levels all over the world. About 30 countries have adopted Inflation Targeting. Despite sharing a common idea, each of these countries resorted to different approaches. Although countries that adopted Inflation Targeting to conduct monetary policy come from different starting points, three scenarios are very common: a) inflation was already low, b) inflation was failing at a slow pace and Inflation Targeting was timidly adopted and later on institutionalized and reinforced, and c) the authorities were searching for a nominal anchor after the collapse of an exchange rate peg.

This paper describes the experience several emerging and less developed economies had with Inflation Targeting. These countries have struggled to control inflation during the adoption phase and have had experiences that start from either a), b), or c). We document the resilience of inflationary expectations during the early days in Israel, Brazil, Guatemala, Mexico, South Africa, and Turkey; the case of New Zealand is also described to provide a benchmark. Finally, the recent case of Argentina is discussed and presented as a case for which Inflation Targeting failed and was abandoned.1

The main lesson is that the "art" of the successful implementation of Inflation Targeting depends a lot on winning the "battle of expectations". Once expected inflation falls and remains inside the bands, it is easier for monetary policy to anchor inflation expectations. There could be occasional departures from the target, but it seems that the private sector considers them "transitory", and lets bygones be bygones.

Small open economies with a relatively open capital account are exposed to sudden stops and maxi depreciations of the domestic currency. But if the "battle of expectations" was already won, the exchange rate pass-through and the degree of liability dollarization will probably be sufficiently low, so the shocks do not compromise the stability of Inflation Targeting. However, if expectations were not anchored, the target may need to be re-adjusted, or worse, the entire regime may be abandoned.

This paper includes a brief discussion of how our case studies faced turmoil in financial markets. The rest of this paper is structured as follows. After this introduction, section 2 presents the literature review. Section 3 presents the "successful" cases, while section 4 explores the failed attempts (Argentina and Turkey) as well as the effects of the subprime crisis on each of the countries studied. Finally, section 5 summarizes the main lessons and implications, and presents the conclusions.

RELATED LITERATURE

Inflation Targeting is described as a scheme that features an explicit commitment to a low and stable rate of inflation, together with an institutional set-up that combines an independent (but accountable) and transparent central bank. The main instrument is a policy determined interest rate, and in the context of a relatively open capital account, it follows that the exchange rate should be allowed to float more or less freely.

Like most policy regimes, Inflation Targeting comes in many forms and adopts different characteristics around the world. Indeed, some authors have argued that some countries have very strict commitment, while some adopted a "flexible" version of the scheme (Carare & Stone, 2003). Finally, there is a "light" version of Inflation Targeting, which features less transparency, less credibility, and low commitment to the target (Carare & Stone, 2003).

Inflation Targeting works as a credible threat by the central bank to blow up the economy if the rate of inflation increases. Due to the commitment and the credibility of the central bank, the public believes that it is not in its own interest to expect rates of inflation above (or below) the target. Thus, Inflation Targeting works mainly by anchoring expectations. When inflation is above the target, a short-term nominal interest is increased, hoping that the real long-term rate of interest will increase. Conversely, when inflation is below the target, the central bank will cut the short-term interest rate.

Changes in real interest rates are assumed to affect aggregate demand, hence altering the rate of inflation. When expectations are anchored by monetary policy, the private sector understands that the central bank will react to keep inflation on target, so changes in output are not even needed. Inflation may deviate from the target, but it is well understood that these departures are temporary and that the central bank controls the long-term rate of inflation by the mere threat of changing its monetary policy rate. Moreover, in absence of supply side shocks, and when there are no frictions in the labour market, stabilizing inflation is equivalent to stabilizing the output gap. This is the "Divine Coincidence" (Blanchard & Galí, 2007).

The literature has identified several prerequisites before adopting Inflation Targeting (Schmidt-Hebbel & Tapia, 2002): 1) to establish the reduction of inflation as an objective of the central bank, while simultaneously making it accountable for its actions and increasing the transparency on communications; 2) to avoid situations where inflation downsizing is subordinate to some other objective, for instance when the central banks need to finance the treasury, assist banks under stress, or to engage in large purchases and sales of FX reserves;2 3) to employ monetary policy instruments aimed at reducing or sustaining a lower inflation rate; and 4) to encourage the presence of a well-developed and stable financial system.

These conditions are not always present in emerging and less developed economies (Laurens et. al., 2015). They are usually violated in the "light" version of Inflation Targeting, and it is often very hard to align expectations with the targets. However, some central banks were able to implement a hybrid system that combines Inflation Targeting with unconventional policies, such as macroprudential regulations, interventions in the foreign exchange market, and even capital controls (Céspedes, Chang, & Velasco, 2014).

The literature distinguishes between varieties of inflationary regimes. "Moderate" or "high" inflations are usually more resilient and stable than "hyperinflation". Some distinguish between "moderate" (roughly 15-30% annual rates) and "high" inflation (above 15-30%, but not "hyperinflation"). A moderate or high rate of inflation induces the introduction of explicit or implicit indexation mechanisms. This is because the adaptation to inflation using indexation reduces transaction costs.

When inflation reaches extremely high levels, the public suffers severe income losses if they index their prices and wages to past inflation. A sudden increase in the rate of inflation will reduce the purchasing power of those whose incomes are indexed, at least until they get a new price or wage increase. As long as inflation remains moderate or high, price setting will remain non-synchronized and the rate of inflation will probably display an inertial behaviour. But any disruptive event, such as a large depreciation or an increase in the price of food or public utility may permanently increase the rate of inflation (Bruno, 1988; Dornbusch & Simonsen, 1987).

A part of the literature has studied stabilization packages designed to deal with high inflation or hyperinflation, but only very few papers have instead focused on the stabilization of moderate inflation (Dornbusch & Fischer, 1993). The take-home point is that stabilizing each type of inflation may require a different approach. The literature distinguishes between monetary-based and exchange rate-based stabilization plans, depending on the instrument that is used as a nominal anchor. Reinhart and Végh (1994) claim that the most important lessons are that exchange rate-based plans usually show boom-bust cycles, while money-based plans work the other way around.

The literature on the effects of Inflation Targeting on macroeconomic performance have paid little attention to the role of Inflation Targeting as a policy to combat moderate or high inflation. The recent Argentinean experience may be described as an Interest-Rate-Based stabilization plan. The inflation target announced by the central bank plays the role of the nominal anchor. This type of stabilization plan is notably difficult to implement if there are credibility problems.

The adoption of Inflation Targeting does not translate into an automatic fall of expected inflation (Bernanke, Laubach, Mishkin, & Posen, 1999; Levin, Natalucci, & Piger, 2004), but, rather, there is some evidence that shows it falls gradually after targets have been announced (Johnson, 2003). This suggests that once inflation targeting has been in place for a while, it does make a difference by anchoring inflation expectations.

Although most of the time Inflation Targeting is adopted when inflation is low, some papers have found that lagged inflation is still an important determinant of current inflation (Caputo & Liendo, 2005). This clearly contrasts with the baseline specification of most models of Inflation Targeting based on the New Keynesian literature, where inflation depends on future inflation. It is not clear whether the statistical significance of past inflation is due to the presence of inertia and in fact backward looking components could be added to the basic model.

CASE STUDIES

In this section, we explore the experience of emerging market economies that adopted Inflation Targeting when inflation was relatively high. The cases analysed are Israel, Brazil, Mexico, South Africa, and Guatemala. The rates of inflation where close to 10%, with the exception of Brazil. However, that country defeated hyperinflation just five years before the adoption of Inflation Targeting in 1999, so there are good reasons to expect that expectations were not necessarily easy to anchor.

Finally, the cases of New Zealand, Argentina, and to a lesser extent, Turkey, are of particular interest. New Zealand was the first country to officially adopt Inflation Targeting and it constitutes the benchmark case. Argentina and Turkey are interesting case studies because they eventually abandoned Inflation Targeting.

A simple conceptual framework can be built to illustrate the mechanics of inflation stabilization. Consider an expectations augmented Phillips Curve:

Where inflation at period t ϖ t depends on expected inflation ϖe t , the output gap y t - y t * , the rate of depreciation E t and some other shocks such as the adjustments of public sector goods, oil, etc., captured by ε t , which is a term with zero mean and constant variance.3

The positive parameters Ø, β, γ and γ measure the ability of the private sector to pass-through from expected inflation to actual inflation (and thus 0 ≤ Ø ≤ 1), the sensibility of inflation with respect to excess demand for goods and/or labour, the pass-through from depreciation to inflation, and the impact of other shocks on the dynamic of inflation. Expected inflation can be further decomposed:

Equation (2) says that expected inflation is a weighted average of the inflation target ϖ T t and past inflation ϖ T t-1 , with 0 ≤ ρ ≤ 1, plus a zero mean and constant variance shock Zt. This shock could also be correlated with other disturbances.

If ρ = 1, there is perfect credibility, while if ρ = 0 there is perfect indexation to past inflation. This equation is also related to the literature on "time inconsistence", which suggests that absence of commitment will lead to a suboptimal equilibrium with some extra inflation (Calvo, 1978, Kydland & Prescott, 1977). Equation (2) can also reflect institutional failures that limit the ability of the central bank to pre-commit to the target. It was suggested that central banks often change the target after they miss it. Instead of adjusting inflation to the target, the target is adjusted to remain closer to observed inflation (Kim & Yim, 2016); this happened, for instance, in Argentina during the end of 2017, and in Brazil during 2003 and 2004.

The weight ρ is a function of country specific characteristics. In countries that start from higher inflation or where credibility and time inconsistency problems are severe, ρ will be relatively closer to 0. The parameter Ø is also closely related to level the level of inflation. In high inflation environments, price setting behaviour will tend to incorporate expectations. The combined parameters ρØ and (1 - ρ)Ø measure how anchored expectations are.

The Inflation Targeting case can be represented assuming a Taylor Rule of the form:

Where the policy determined nominal interest rate i t depends on expected inflation, the deviation of inflation from the target ϖ t - ϖ t T and the output gap. The parameters η 1 and η 2 measure the responsiveness of the target nominal interest rate with respect to each target. They should be positive and large enough to ensure stability. In equilibrium, we should have ϖ t = ϖ t T and y t = y t * , so the expected real interest rate i t - ϖ t e should be equal to the "natural" or "neutral" rate r t * .

In the basic Inflation Targeting framework, it is assumed that the exchange rate is allowed to float in the context of a relatively open capital account, so the expected rate of depreciation should satisfy:

The expected rate of depreciation should be equal to the nominal interest rate differential, plus a risk premium RP t . When the domestic nominal rate i t is higher than the international rate i t * adjusted by risk i t > i t * + RP t , an exchange rate depreciation is expected E e t > 0. Thus, if the central bank increases the policy rate, the exchange rate appreciates on impact, and it is expected to depreciate in the future.

Notice that subtracting expected inflation from equation (4), keeping in mind that foreign inflation is zero, we obtain E e t - ϖ e t = i t - ϖ e t - i * t + RP t . The real rate of depreciation E e t - ϖ e t is a function of the real interest rate differential (adjusted for risk).

Central banks very often intervene in the foreign exchange market, so by adjusting its portfolio, it can influence the risk premium to avoid large undesirable fluctuations in the exchange rate.4 Presumably, the combination of the Taylor Rule with the intervention in the foreign exchange rate will influence the real interest rate and the real exchange rate, which will affect aggregate demand and the output gap. If the pass-through from exchange rates to prices is large or if the shocks are correlated, then monetary and exchange rate policies will influence inflation and expected inflation directly though changes in the exchange rate.

Let the output gap be a function of the deviation of the real interest rate and the real exchange rate from their equilibrium levels and some shock:

Where v t is a shock term, and т 1 and т 2 are positive. Using (3), and assuming that Q t - Q t * is proportional to the difference between the domestic and the foreign real interest rate (adjusted for risk),5 the out-gap becomes:

Where

Equation (6) defines aggregate demand in the output- inflation space. Intuitively, if inflation accelerates, the central bank will increase the real interest rate. Together with an appreciation of the real exchange rate, this will reduce demand. The "Divine Coincidence", implies that stabilizing inflation implies stabilizing the output gap. From (1) and (2):

Equation (6) defines aggregate demand in the output- inflation space. Intuitively, if inflation accelerates, the central bank will increase the real interest rate. Together with an appreciation of the real exchange rate, this will reduce demand. The "Divine Coincidence", implies that stabilizing inflation implies stabilizing the output gap. From (1) and (2):

Inflation will be equal to the target ϖ t = ϖ t T when output is equal to potential output y t = y t * , only if Ø = ρ = 1, the shock terms Z t and ε t are zero, and there is no exchange rate depreciation E t = 0. More precisely, substituting (6) into (7):

We can verify that (8) implies that inflation is equal to the target, provided that the demand shock term v t vanishes. In other words, it is either equal to zero or it is offset by monetary policy.

This feature of our simple set-up helps to explain why inflation needs to fall before a full-fledged Inflation Targeting is adopted. For example, authorities should build "Credibility" or inflation should be reduced and maintained at low levels, in order to let 0p slowly creep towards one. The conditions for the "Divine Coincidence" are probably not satisfied, so in the case studies that we present, it seems likely that there is a trade-off between stabilizing output and stabilizing inflation. Table No. 1 illustrates the international experience. It is clear that by the time of the adoption, none of the countries were experiencing rates of inflation above 10%.

Table 1 The International Experience

| Country | Adoption Date | Initial Inflation |

|---|---|---|

| New Zealand | Q11990 | 4.27 |

| Canada | M21991 | 6.22 |

| United Kingdom | M101992 | 2.93 |

| Sweden | M11993 | 4.80 |

| Finland | M21993 | 2.92 |

| Australia | M41993 | 1.84 |

| Spain | M11995 | 4.36 |

| Israel | M61997 | 8.45 |

| Czech Republic | M121997 | 10.09 |

| Poland | M101998 | 10.01 |

| Brazil | M61999 | 3.32 |

| Chile | M91999 | 2.94 |

| Colombia | M91999 | 4.03 |

| South Africa | M22000 | 2.35 |

| Thailand | M52000 | 1.75 |

| South Korea | M12001 | 3.44 |

| Mexico | M12001 | 8.11 |

| Islandia | M32001 | 3.87 |

| Norway | M32001 | 3.74 |

| Hungary | M62001 | 10.50 |

| Peru | M12002 | -0.83 |

| Philippines | M12002 | 3.26 |

| Guatemala | M12005 | 9.20 |

| Slovak | M12005 | 3.19 |

| Indonesia | M72005 | 7.84 |

| Romania | M82005 | 8.79 |

| Turkey | M12006 | 7.93 |

| Serbia | M92006 | 10.75 |

| Ghana | M52007 | 10.50 |

Source: Authors' own elaboration based on BIS and national central banks.

The next sub-sections review a variety of country experiences where inflation was controlled before the adoption of a full-fledged Inflation Targeting regime. In some experiences, widespread indexation in goods and labour and financial markets prevented the authorities from quickly bringing down inflation without large output costs, so baby steps were taken to reduce inflation before the adoption of Inflation Targeting. The increased reputation of central bank policies, the reduction in pass-through and the degree of liability dollarization, and the de-indexation of wages and prices allowed the central bank to pursue a monetary policy oriented by a short-term rate. Importantly, this was accomplished with the aid of unconventional policies, such as capital controls, interventions on the foreign exchange market, prudential regulations, credit growth targets, and even price controls.

Israel

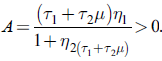

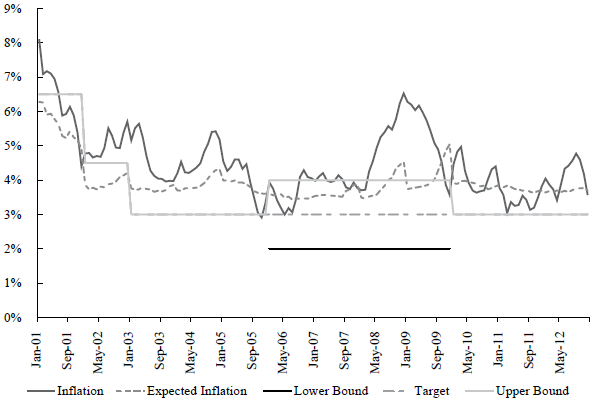

Israel adopted Inflation Targeting in 1997. The transition started in 1992. Previously, Israel suffered from high and persistent inflation. During the early 1970s the economy was on the verge of hyperinflation, with inflation rates lying comfortably at around 300-400% per year. In 2001, the rate of inflation was close to 1%, compared with 17% during 1991. The targets are set with a one-year horizon by the Israeli government. The main target is the consumer price index rate of change. When Inflation Targeting was adopted, expectations were not misaligned.

The introduction of Inflation Targeting in Israel was not a clear and transparent process (Leiderman & Bar-Or, 2000). The central bank was heavily criticized due to the extremely contractionary stance it adopted during the early 1990s and the existence of different anchors for monetary policy, such as an explicit crawling currency band and the inflation target (Leiderman & Bufman, 2000).

During the 1990s, there were episodes where the rate of inflation increased due to the depreciation of the exchange rate. A high pass-through from exchange rate to price was a legacy of Israel's inflationary history. Towards the end of 1994, the exchange rate depreciation led to an increase in inflationary expectations, which climbed to 13% from 7% at the beginning of the year: above the target of 8%. During 1996, expected inflation increased from 9% to 12%. Finally, during the depreciation of 1998, the figures where 3% and 8.6%. However, after 1998, expectations remained anchored by monetary policy.

By mid-1997, the central bank started to gradually increase the width of the crawling band as the mismatch between inflation and expectations begin to disappear. The central bank intervened less frequently in the foreign exchange market.

In 2002 there was another substantial increase in the rate of inflation by around 16% due to a depreciation of the exchange rate with respect to the dollar. This volatility observed in the foreign exchange market during that year was mainly explained by the perception that the Israeli government had eroded the central bank's independence. Moreover, the modification of the economic programme in the previous year, a more contractionary fiscal policy and a more relaxed monetary policy, led to an erosion of authorities' credibility, especially when the fiscal target was not accomplished. Expected inflation increased to 4.4%, but interestingly, it increased by less than actual inflation. Thus, it seemed that the official targets anchored expectations and the central bank's reputation was not severally hampered. During 2003, expected inflation remained well inside the band, and in fact, actual inflation ended-up in the negative domain (-1.9%) due to the sharp appreciation of the domestic currency and a subsequent reduction in aggregate demand.

As we can see in Figure 1, expectations where stable when compared to the first years of Inflation Targeting. Not only was expected inflation less volatile, but it also remained in line with the targets. During 2006-2007, the standard deviation of expected inflation was 0.4%, compared with 1.9% during the first two years.

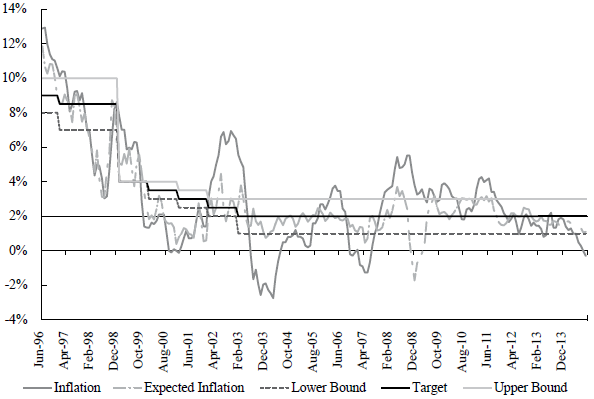

Brazil

Brazil adopted Inflation Targeting in 1999. The scheme seemed to be a reasonable choice after the large depreciation of the domestic currency. In 1994, a stabilization programme was adopted to stop hyperinflation (the so-called "Plan Real"), which was to reduce the rate of inflation from above 2000% to less than 3% in 1998.

During the first year, the rate of inflation was almost 9%, not too serious considering the large depreciation of the currency, but well above the international standard for countries that use that policy regime. Inflation was stabilized around 6-8% during the subsequent years, but due to the election of the left-wing candidate Lula da Silva, another round of depreciation nudged inflation over 17%: well above the official targets. Although the central bank had to change the target, inflation fell towards 5.5%. Another round of inflationary pressures emerged during 2009.

Initially the inflation target was set by an organism that involves the central bank and the Ministry of Finance, which had a tolerance band of 2% and a year-long horizon. Starting in 2002, the targets were set two years in advance, and after 2017, the announcements include the next two years. In Brazil, the central bank targets the rate of growth of the so-called "broad" consumer price index.

When Inflation Targeting was adopted, expected inflation was anchored by the targets, and towards the end of 2000 the public expected an inflation rate of 4.3%. However, in December of 2001 inflation reached 7.6%, which was 1.6% above the upper limit of the target. Thus, the next year's expectations were adjusted upwards, reflecting the development. The central bank explained that the deviation from target was due to the increments in regulated prices and the depreciation of the domestic currency due to the uncertainty associated with the elections. In fact, regulated prices increased by 10.7% during that year, contributing 3.1 p.p. to the rate of inflation.

In October 2002, Lula was elected president, and expected inflation increased significantly in 2003. The market developed concerns regarding the sustainability of the public sector debt. Expected inflation reached 11% towards November 2011, but a new agreement with the IMF was reached in September of 2002, and the central bank managed to modify the targets with drastic effects. For 2003, the new targets were increased from 4% (with a tolerance band of 2%) to 8.5%, and for 2004, from 3.75% to 5.5% (with a tolerance band of 2.5%).

Despite the drastic adjustment, the central bank did not lose control of the financial markets, and it was able to avoid a drastic change in the interest rate, which would probably will not be enough to anchor expectations. The cost of a drastic increase in the interest would probably have undermined the entire structure of Inflation Targeting in Brazil. Over the next years, expected inflation fell inside the bands, and in December 2003 and 2004 they were 5.9%, and 5.8%, respectively. Figure 2 summarises the evolution of inflation and expectations in Brazil.

South Africa

Inflation Targeting was adopted in 2000. From 1997 onwards, a soft version of the regime was in place, but the central bank was targeting the rate of growth for a broad monetary aggregate (M3). Since the financial system was too complex and money demand is extremely unstable, targeting M3 was considered a troublesome task. Inflation was falling in South Africa, from an average of 14.6% during the 1980s to 9.8% during the 1990s. However, that figure was still high when compared to other cases where Inflation Targeting was in place.

One particular feature of Inflation Targeting in South Africa was the creation of a technical committee responsible for evaluating the performance of the central bank. That committee included members from the treasury and the central bank. The time horizon was a calendar year, and the target was the rate of growth of the consumer price index, excluding mortgage payments. However, after 2009, the central bank started to target the entire index.

The targets were usually met, but inflation remained volatile. During the 2000s, inflation averaged 5.9%, which was even below the average for the 1990s. However, each time that inflation fell outside the target, expectations were adjusted accordingly. If inflation was above the target, the public expected higher inflation in the future. Inflation never fell below the targets.

The first critical episode took place during mid 2002 due to the depreciation of the domestic currency and the subsequent increase in the price of food. The depreciation could be explained by the deterioration of the global environment in 2001, which was associated with the Argentinean crisis and led to a fall in capital inflows. Expected inflation increased, from 5.8% during August of 2001, to above 6.8% in 2002 (with a peak of 8.5% during December), a figure just above the target of 3-6%. The rate of inflation increased to 11.4 %.

The second critical episode took place during mid 2007, after the subprime crisis in the United States, which led to a sudden depreciation of the domestic currency by almost 40%. Moreover, during 2008 the price of oil reached a record of USD 132.72 per barrel. Other commodities also sharply increased. Similarly to the previous episode, expected inflation increased but got stuck at 6.1%. This was almost in line with the 3-6% target for 2008.

Expected inflation reached 8.3% in April. As the first impacts of the subprime crisis faded away, inflation also fell, reaching 6.3% in 2009, and 3.5% in 2010: in line with the official targets. However, expectations were slowly realigned, and in 2010 they stood at 6.1% for 2011. The South African experience is summarised in Figure 3.

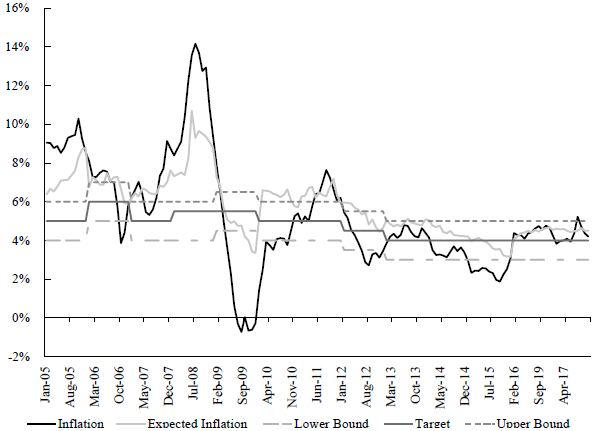

Mexico

In 2001, Mexico adopted Inflation Targeting. In 1994, there was a sharp depreciation of the domestic currency, which led to a very strong inflationary pressure, and in 1995 inflation reached 51.7%. After the crisis, the domestic currency was allowed to consistently float freely.

The Mexican government adopted a stabilization programme to reduce the rate of inflation; meanwhile, the Bank of Mexico took steps to increase transparency and accountability while maintaining inflation under control (Ramos-Francia & García, 2005). When Inflation Targeting was finally adopted, the institutional set-up was already in place. Unlike the other cases discussed so far, the only institution responsible for setting the inflation targets is the Bank of Mexico. They are set on a multi-year basis several years in advance. The target is the growth rate of consumer price index.

During the first years of Inflation Targeting, the central bank experienced some difficulties keeping inflation under control. During 2004, inflation was above the target (5.1% vs. 3%) due to an increase in the international price of commodities and a spike in regulated prices of around 10% (mainly in transport).

Only after 2006 did the inflation rate fall inside the bands (although there was previously no lower bound) for the first time. However, the subprime crisis (which lead to a depreciation of the domestic currency by about 26%), another spike in the price of food (8.65%), and the increase in regulated prices (16.8%) during 2008 put inflation above the target once again.

During January 2001, expected inflation was 6.3%: well above the target for 2002 (4.5%). As time passed, expected inflation was gradually reduced and remained below the upper bound of the band, with the expectation being the end of 2008 and 2009. Hence, the Bank of Mexico had a difficult time anchoring expectations.

After the subprime crisis, the Bank of Mexico's performance significantly improved as the target was met both in 2010 and in 2011. However, expected inflation was still slightly above the official target of 3% as the public expected yet another round of increases in the price of regulated goods (see Figure 4).

Source: Authors' own elaboration based on data from the Central Bank of Mexico.

Figure 4 Inflation Targeting in Mexico

To summarize, the Bank of Mexico had some difficulties in anchoring expectations during the first years of Inflation Targeting. The main reasons were the pressures emanating from the side of costs due to the increase in regulated prices, the exchange rate shocks, and the increase in the international price of commodities because of the rise of China in world markets.

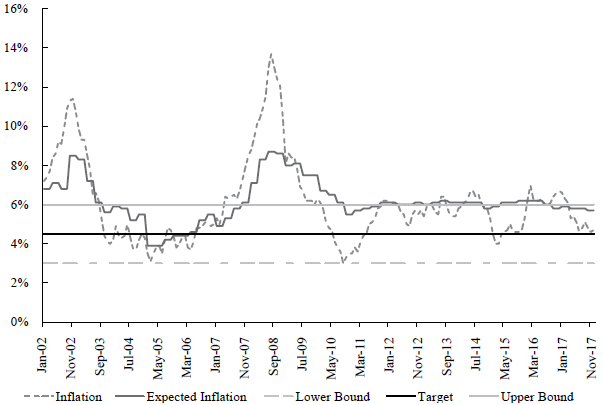

Guatemala

In 2005, Guatemala adopted Inflation Targeting. Previously, a system of ad-hoc targets was in place with no explicit commitment from the central bank and no clear indication about the means to achieve the targets. Since 2000, several reforms were implemented to adjust the institutional framework in preparation for the adoption of Inflation Targeting.

Unlike other countries, Guatemala never experienced chronic inflation or hyperinflation. During the 1990s, the rate of inflation averaged 14.7%, and during the four years before the adoption of Inflation Targeting, it was around 7%. There were no serious macroeconomic imbalances or any previous stabilization attempts.

The inflation targets are set by the Junta Monetaria, which is directed by the president of the Bank of Guatemala. It also includes members from the government, such as the Minister of Finance. The targets are set on an annual basis, and starting in 2013 it was set at 4% ± 1% for the forthcoming years. The Bank of Guatemala targets the rate of growth of the consumer price index.

The rate of inflation was moderate before the adoption of Inflation Targeting (around 9% per year). During the 2000s, the rate of inflation has exhibited considerable volatility from commodity prices as well as from the Subprime Meltdown shock. Then the subprime crisis generated deflationary pressures, and the consumer price index fell by -0.2% during 2009.

In 2005, inflation was 8.6%: above the official target of 6% ± 1%. The next year, expected inflation was 6.3% and in line with the bands. During the next two years, inflation reached 8.7% and 9.4% during 2007 and 2008, and expected inflation increased, clearly falling off the bands. Two main reasons seem to account for this: the increase in the international price of oil and Hurricane Stan. In fact, the peak of inflation and expected inflation coincided with the peak in the price of oil and other commodities (in 2009).

Guatemala was not alone in facing severe supply side shocks emanating from commodity prices, but unlike cases such as Brazil or South Africa, extreme weather is another source of important supply side shocks. Guatemala exports and produces primary commodities, mainly coffee and cotton.

Afterwards, the performance improved significantly: the target was met in 2010, 2011, 2012, and 2013. Consequently, expected inflation fell inside the band.

During 2014, the figure stood at 2.9%, even below the lower bound of the band (then set at 4% ± 1%).

To summarize, it took more than ten years to keep expectations anchored by the target and to bring inflation from around 10% to less than 5%. Supply side shocks seem to be the main culprits. Figure 5 describes the evolution of inflation and expectations in Guatemala.

The Benchmark Case: New Zealand

Analysing the New Zealand experience is a useful way to assess whether the process of adopting Inflation Targeting is easier in more advanced economies. The main difference vis-à-vis the other case studies is that expectations were immediately aligned with the official targets of the Reserve Bank of New Zealand. We should bear in mind that the original targets were set between 0% and 2% during 1992, but inflation one year before the adoption of Inflation Targeting was around 7% (not very different from the 6.9% during the initial year in South Africa and much higher than the 1.65% in Brazil), and it averaged 11% during the two previous decades.

Unlike other emerging market economies, New Zealand did not suffer from significant supply side shocks. The initial target was set with a broad horizon (more than a year), which significantly increased the room for manoeuvre. The only two times that the targets were missed where in 1991 and in 1994. Inflation stood at 2.3% and 2.5%, respectively, not very far from the band. Inflation and expected inflation were much less volatile than in other case studies.

To be concise, the consolidation of Inflation Targeting in emerging economies was slower and much harder. In the first cases, it took between five and six years for expected inflation to fall inside the bands, but it took only one shot for the Reserve Bank of New Zealand. For the few instances where inflation fell outside the band, expected inflation remained firmly anchored by monetary policy.

INFLATION TARGETING UNDER STRESS

Emerging economies are subject to a myriad of supply and demand side shocks, from internal and external origins, and additional problems such as fiscal dominance and financial fragility. These conditions certainly complicate the process of consolidation of Inflation Targeting as the public faith in the ability of the central bank to control inflation is hard to establish. This is clear in those instances where inflation falls outside the bands: expected inflation usually shortly follows.

The evidence suggests that central banks were able to consolidate an Inflation Targeting regime after a struggle with private sector expectations. Nowadays, expected inflation has remained anchored, except in some "pathological" cases (Argentina and Turkey). In some extreme events, unconventional policies are adopted. This section reviews Argentina and Turkey as well as the effects the subprime meltdown had on the case studies.

Failed Cases: Argentina and Turkey

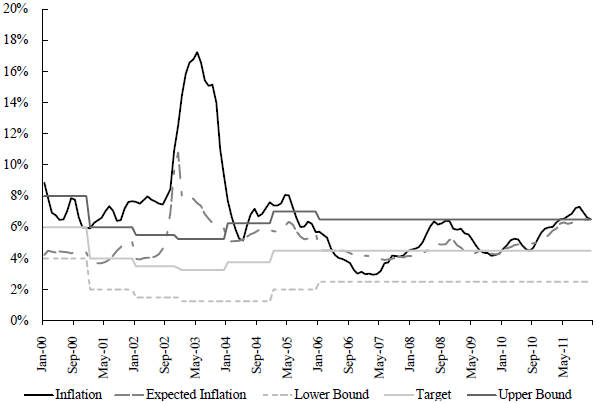

After four years of "implicit inflation targeting", the central bank of Turkey formally adopted Inflation Targeting in 2006. The authorities refused to fully embrace Inflation Targeting due to the presence of inertial inflation, a high degree of exchange rate pass-through, and a high level of public debt. Once these problems where brought under control (or so the authorities thought), and after a monetary reform, Inflation Targeting was formally adopted. Although the central bank was able to deliver a rate of inflation according to the 8% ± 2 target during 2005, inflation never fell below 5%, and expectations reacted accordingly.

The main problem was a depreciation of the Turkish Lira (around 20%), which increased the price of tradable goods, and consequently, the entire price level. Shortly afterwards, an increase in the price of oil aggravated the problem. Inflation reached 11.6% during July 2006, and expected inflation reacted quickly and moved in an upward direction. This adverse scenario forced the Central Bank of the Republic of Turkey to consequently act and rise its policy rate. Despite the central bank's efforts, inflation reached 9.6% at the end of the year, and the target was missed. Eventually, the target was revised for 2007, but the central bank could not achieve the 4% ± 2 target as yearly inflation was 8.3%.

For 2008, inflation and expected inflation displayed a similar dynamic. Both fell slightly due to the presence of supply side shocks. As the Subprime crisis developed, the price of commodities slumped, and despite a currency depreciation, according to the central bank's estimations, the pass-through was significantly lower. Civcir and Akçaglayan (2010) found similar results regarding the exchange rate pass-through under Inflation Targeting in Turkey. Additionally, the central bank implemented a monetary tightening procedure, which was its policy rate during the May-July period. Even though the weakness in the domestic demand seemed to have reduced, the financial turmoil around the globe forced the central bank to remain cautious and, therefore, monetary policy remained tightened. Unfortunately, this was not enough, and inflation reached 10%: also above the 4% ± 2 target.

During 2009 and 2010 the central bank finally met the targets (7.5% ± 2 and 6.5% ± 2) as inflation reached 6.5% and 6.4%, respectively. However, expected inflation never fell below the floor of 6%. Moreover, the central bank made significant cuts in the policy rates in order to alleviate the impact of the global financial crisis by providing the credit markets with more liquidity.

During the period between September 2008 and October 2009, the interest rate dropped 1000 basis points. This might have been a considerable part of explaining why inflation expectations remained stagnant. Inflation accelerated again during 2011, reaching 10.5%, so the target of 5.5% ± 2 was not met. A depreciation of 14% of the Turkish Lira triggered by the Eurozone crisis was the main culprit. However, the monetary authority did not react as it did in previous episodes of exogenous shocks. As a matter of fact, the central bank marginally increased its policy rate, but it raised the reserve requirements ratio.

Since 2010, the Turkish central bank has made some modifications in its monetary policy framework by considering macroeconomic financial risks. In order to achieve the goal, additional policy instruments were implemented such as the reserve requirement ratio. The central bank introduced a substantial modification in its regime, which consisted in implementing a wide corridor system in which more than one interest rate was used as a policy instrument. 2012 was the last year when the central bank reached the 5% ± 2 target, and inflation stood at 6.2%. In addition to this, the monetary policy took a more hawkish stance by the beginning of 2012 and, as expectations developed positively, the CBRT adopted a more accommodative stance during the second half of that year. Expected inflation fell a little during December 2012, right in the middle of the band. According to Cobham's (2018) de facto classification, Turkey "informally" abandoned Inflation Targeting in 2014.

To summarize, the case of Turkey illustrates emerging markets' struggle to implement Inflation Targeting. Inflation and expected inflation were volatile, and the target was repeatedly missed. While inflation significantly declined from between 50-60%, the target was missed during 2006-2008, and has consistently been missed from 2012. According to Genc and Balcilar (2012) a crucial issue in understanding why Turkey failed to bring inflation under control is the fact the central bank failed to achieve its original promise regarding its inflation targets on several opportunities, which made it less credible as an institution. Figure 6 illustrates the Turkish case.

Source: Authors' own elaboration based on data from the Central Bank of Turkey.

Figure 6 Inflation Targeting in Turkey

We will now briefly consider the Argentinean case. From 2008 to 2015, the average annual inflation rate was around 27%; it peaked at 37% after a 20% devaluation at the beginning of 2014. The real exchange rate continuously appreciated since 2009, and capital controls were imposed in October 2011 to prevent capital flight creating a parallel market. Regulated prices such as public services and transport where almost frozen since 2003. The fiscal stance was clearly negative as there was a 5.1% of GDP fiscal deficit in 2015.6 External debt was also in pseudo-default because an adverse court ruling with bondholders after a series of restructuration attempts. Due to the favourable terms of trade during most of the 2000s, the economy was running short on foreign exchange.

The new government elected towards the end of 2015 had very few options other than stabilization. However, there was some room for choosing the type of stabilization plan. Shortly after the new government took the office, a new debt restructuration attempt was implemented and capital controls were removed. A more flexible exchange rate regime was also adopted. The liberalization of the capital account caused an important devaluation of about 36% in December 2015, which accelerated inflation (reaching an annual rate of 38.6% in 2016).

The government also signalled its intentions to cut the fiscal deficit, re-establishing a coherent system of public service tariffs. Unfortunately, this also accelerated the inflation rate. While writing this paper in 2019, Argentina has experienced 11 years in a row with an annual rate of inflation above 15%. Table 2 provides some statistics.

Table 2. Argentina Descriptive Statistics

| Year | Inflation | REER* | Fiscal Deficit** | GDP growth | Current Account** | Debt | |||

|---|---|---|---|---|---|---|---|---|---|

| Total** | External** | In Foreign Currency*** | In Foreign Currency**** | ||||||

| 2003 | 0.15 | 95.97 | 0.06 | 1.39 | 0.79 | 9.60 | 3.93 | ||

| 2004 | 0.04 | 100.26 | 0.02 | 0.02 | 1.18 | 0.69 | 7.36 | 3.63 | |

| 2005 | 0.10 | 102.20 | 0.02 | 0.09 | 0.03 | 0.68 | 0.32 | 2.37 | 1.41 |

| 2006 | 0.11 | 104.78 | 0.01 | 0.08 | 0.03 | 0.59 | 0.24 | 2.22 | 1.31 |

| 2007 | 0.17 | 101.53 | 0.01 | 0.09 | 0.02 | 0.51 | 0.22 | 1.65 | 1.15 |

| 2008 | 0.27 | 92.21 | 0.01 | 0.04 | 0.01 | 0.44 | 0.17 | 1.65 | 0.94 |

| 2009 | 0.15 | 91.05 | -0.01 | -0.06 | 0.02 | 0.46 | 0.17 | 1.66 | 1.20 |

| 2010 | 0.24 | 82.43 | -0.01 | 0.10 | 0.00 | 0.40 | 0.15 | 1.85 | 1.19 |

| 2011 | 0.27 | 77.00 | -0.02 | 0.06 | -0.01 | 0.36 | 0.12 | 2.32 | 1.10 |

| 2012 | 0.25 | 65.95 | -0.02 | -0.01 | 0.00 | 0.37 | 0.11 | 2.69 | 1.23 |

| 2013 | 0.24 | 63.56 | -0.03 | 0.02 | -0.02 | 0.40 | 0.12 | 4.10 | 1.40 |

| 2014 | 0.37 | 67.00 | -0.04 | -0.03 | -0.02 | 0.41 | 0.13 | 4.58 | 1.76 |

| 2015 | 0.27 | 52.56 | -0.05 | 0.03 | -0.03 | 0.49 | 0.14 | 5.82 | 2.13 |

| 2016 | 0.39 | 59.80 | -0.07 | -0.02 | -0.03 | 0.52 | 0.18 | 4.64 | 2.54 |

| 2017 | 0.26 | 56.03 | -0.06 | 0.03 | -0.05 | 0.53 | 0.19 | 4.20 | 2.93 |

*(Dec-2003=100), **(% GDP), ***(% International Reserves), ****(% exports)

Source: Authors' own elaboration from Ministry of Finance, INDEC and Central Bank of Argentina.

During the 2008-2015 period, the rate of inflation oscillated between 15-40%. Although these figures may look small considering Argentina's historical record, they are clearly above those of all of its main trade partners and international standards. The struggle and the failure to control inflation are the Achilles' heels of Argentina's stabilization policies.

In September 2016, the central bank formally announced the implementation of Inflation Targeting. The inflation target was set between 12% and 17% for 2017, 8% and 12% for 2018, and between 3.5% and 6% for 2019. Since inflation in 2016 was 39% (on average), the rate of disinflation was required to meet the higher bound targeted in 2017, which was around 5.4% during each quarter. The annual average inflation rate of 2017 was 25.7%, and the authorities decided to change the target to 15% in 2018.

After the removal of the controls during the end of 2015, the authorities claimed that the exchange rate was allowed to float, and that monetary policy would follow a strict Inflation Targeting approach. In Argentina, the instrument used is the rate associated with central bank short-term instruments, first the so-called "Lebacs" (Letras del Banco Central) and then the "Leliqs" (Letras de Liquidez).

Despite the efforts made, the central bank had a hard time convincing the public that disinflation would happen quickly. Public expectations and professional forecasting of inflation kept it at least 5 percentage points higher than the inflation target during 2017 and the beginning of 2018, which reflected a combination of inertia and imperfect credibility.7

In order to ease monetary policy, during the end of 2017 the inflation target for 2018 was revised upward from 8% - 12% to 15%. However, during the first part of 2018, a sharp real exchange rate depreciation forced the abandonment of Inflation Targeting and the replacement of the interest rate rule with monetary targeting. There are not enough data points to show a full chart, but Table 3 describes the evolution of inflation and expectations in Argentina.

Table 3 Selected Indicators (Argentina)

| Date | Interest Rate | Inflation | Public Expectations | Professional Forecast | Official Target |

|---|---|---|---|---|---|

| Dec-17 | 25% | 25% | 25% | 20% | 12% - 17% |

| Dec-18 | 29% | 47.6% | 20% | 17.40% | 8% - 12% |

| Jan-19 | 28% | 49.30% | 20% | 18.60% | 15% |

Source: Authors' own elaboration based on data from the Central Bank of Argentina.

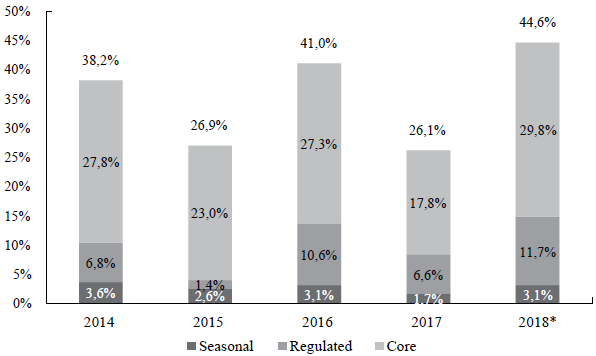

Figure 7 illustrates the dynamics of the consumer price index and core inflation during 2017 and the first eight months of 2018. In Argentina, core inflation excludes goods that have heavily regulated prices or include many of taxes (such as transportation, cigars, gas, electricity, and water) and goods affected by seasonal patterns (for instance fruits, vegetables, tourism, and clothing); this accounts for about 70% of the consumer price index basket.

Source: Authors' own elaboration based on the Bureau of Census and Statistics from the City of Buenos Aires. *January-October.

Figure 7 CPI by Components (Autonomous City of Buenos Aires)

Inflation decreased slowly during 2017, even if we exclude goods with excessive volatile components and elements that do not depend on market conditions. It fell significantly when compared to 2016, which included the effects of the large exchange rate depreciation after the removal of the controls. Compared to 2015, 2016 was less than one percentage point below. Moreover, inflation accelerated once again in 2018 due to the sudden-stop and the new depreciation of the peso.

Considering Figure 8, we can see that during 2017, there was a slight decline after the first three months, but inflation never fell below the 1.2%-1.5% range, which implied an annual rate of about 26%-30% and was clearly inconsistent with an original inflation target of 12%-17%. The small but noticeable recovery of the economy during 2017 combined with the adjustment of relative prices and a sluggish adjustment of expected inflation are the main culprits.

Source: Authors' own elaboration based on data from INDEC (The National Bureau of Statistics and Censuses from Argentina).

Figure 8 Core CPI and CPI Inflation (monthly rates)

To summarize, the authorities where committed to attempting an interest rate-based stabilization plan using Inflation Targeting. The Argentinean case shows that a policy of targeting the domestic interest rate in the context of a fully open capital account and a flexible exchange rate regime may fail to anchor expectations. This is an important lesson for countries that aim to reduce their relatively high levels of inflation. The relatively high domestic interest rate may induce capital inflows that lead to strong pressures on real exchange rate appreciation, which have little effects on inflation. The central bank's credibility may be undermined, the external imbalances may lead to an accumulation of external indebtedness, and the domestic economy may become too exposed to a sudden-stop.

The Subprime Melt-Down

The purpose of this section is to assess the performance of Inflation Targeting when under the presence of severe shortages of international liquidity. A "sudden stop", which implies a reversal of capital flows creates enormous tension on the foreign exchange market, implying additional inflationary pressures through depreciation. The central bank is often forced to increase the target even if output contracts.

Not all the emerging economies are equally exposed to drastic reversals of capital flows. Liability dollarization and large current account deficit seem to increase the exposure (Calvo, Izquierdo, & Mejia, 2004). A monetary policy subjected to external dominance, clearly less prevalent in less dollarized and surplus economies, makes the central bank's task much harder, and the chances that it will fail to fulfil its commitments increase.

In this section we look into the relation between expectations and inflation during the Subprime Meltdown. Although the crisis originated in the U.S., there were clear repercussions in global capital markets. According to our previous findings, large shock may require the implementation of unconventional policies, but it would not treat the stability for the inflation targeting regime.

In the main case studies reviewed, there was no evidence of a large and persistent misalignment of expectations from the bands. Israel is a very interesting example. During early 2009, expected inflation fell below the low limit of the band (1%) into a negative domain despite an inflation spike above the upper limit (3%); this was most likely due to the depreciation of the Shekel: Israel faced deflation.

On the other hand, in almost all the other cases inflation and expected inflation surpassed the upper bound of the bands, with Guatemala being the sole exception, which was severely hit by the contraction of the U.S. economy. In this case, inflation fell from 14% to 0% from early 2008 towards mid 2009. In Mexico and South Africa, expectations dramatically increased after the shock, and their central banks faced difficulties in bringing inflation back in line. In these cases, expected inflation was very close to the upper bound of the bands just before the shock.

According to the experiences reviewed, it seems unclear whether all central banks from the emerging economies where able to fully anchor expectations during the Subprime Meltdown. The sole exception seems to be Israel, which experienced deflation.

ASSESSMENT AND CONCLUSIONS

Our main argument is that Inflation Targeting works, but only when inflation is already low. All the existing experiences, except for Argentina, started from low or moderate rates of inflation, usually below the 10% level.

Table 4 and 5 include some summary statics for inflation and the deviations from the target. The variable "deviations" takes a value of zero when yearly inflation in a given month was inside the target, it takes a positive value equal to the deviation from the upper bound (when yearly inflation was above the upper bound), and it takes a negative value equal to the deviation from the lower bound (when yearly inflation was below the lower bound).

Table 4 Inflation. Summary Statistics

| Country | Observations | Mean | SD / Mean | Min / Max |

|---|---|---|---|---|

| Argentina | 30 | 27.75% | 5.38% | 18.57% / 37.20% |

| Brazil | 227 | 6.58% | 2.69% | 2.46% / 17.24% |

| Guatemala | 159 | 5.09% | 2.66% | '-0.74% / 13.24% |

| Israel | 251 | 2.14% | 2.52% | -2.74% / 9.26% |

| Mexico | 209 | 4.35% | 1.12% | 2.13% / 8.11% |

| New Zealand | 339 | 2.15% | 1.43% | -0.51% / 7.62% |

| South Africa | 220 | 5.74% | 2.43% | 0.17% / 13.02% |

| Turkey | 149 | 8.57% | 1.85% | 3.99% / 12.98% |

Source: Authors' own elaboration based on data from the central banks.

Table 5 Deviations from the Target

| Country | Deviations > 0 | Deviations < 0 | ||

|---|---|---|---|---|

| Observations / Share | Mean | Observations / Share | Mean | |

| Argentina | 27 / 90.00% | 9.39% | 0 / 0.00% | - |

| Brazil | 75 / 33.04% | 2.25% | 17 / 7.49% | 0.43% |

| Guatemala | 49 / 30.83% | 2.16% | 37 / 23.27% | 1.47% |

| Israel | 65 / 25.90% | 1.46% | 120 / 47.82% | 1.51% |

| Mexico | 107 / 51.20% | 1.10% | 17 / 8.13% | 0.62% |

| New Zealand | 87 / 25.66% | 1.44% | 48 / 14.16% | 0.41% |

| South Africa | 77 / 35.00% | 2.01% | 16 / 7.27% | 1.74% |

| Turkey | 96 / 64.43% | 2.06% | 8 / 5.37% | 0.55% |

Source: Authors' own elaboration based on data from the central banks.

The Tables show that Argentina, Brazil, Guatemala, and Turkey have, on average, the highest rates of inflation. Additionally, most of the deviations have a positive sign, so inflation is more often above the upper bound than below the lower bound (except in Israel). The countries with the highest inflation rate are also those where inflation is outside the targets. This is shown in the column that includes the "shares" (observations where inflation deviates divided by total number of months where the country has an official target). This is much more obvious in Argentina, where the target was missed nine out of ten months, and in Turkey, where this figure is six out of ten months.

A formal test is shown in Table 6, which includes different specification of a baseline regression where the variable the captures the extent to which the variable that measures deviations is correlated with different controls and the average rate of inflation.8 The latter is statistically significant at 1%, and the coefficient ranges from about 0.22% to 0.38%, which means that an extra percentage point of inflation increases the deviation by about a fifth and almost a half percentage point deviation from the target. Thus, if we move from low inflation (Israel), let us say from an average inflation rate of around 2%, to high inflation (Argentina at 28%), then deviation will increase between 5% and 10%.

Table 6 Effects of Average Inflation on Deviations from the Target

| Dependent | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Variables | Deviation | Deviation | Deviation | Deviation | Deviation |

| Inflation | 0.305*** | 0.372*** | 0.326*** | 0.326*** | 0.218*** |

| (0.0109) | (0.0141) | (0.0104) | (0.0104) | (0.0169) | |

| Constant | -0.880*** | -1.571*** | 3 424*** | 3.361*** | 3.587*** |

| (0.0686) | (0.168) | (0.407) | (0.427) | (0.387) | |

| Observations | 1,473 | 1,473 | 1,473 | 1,473 | 1,444 |

| R-squared | 0.345 | 0.384 | 0.520 | 0.521 | 0.349 |

Standard errors in parentheses / *** p < 0.01, ** p < 0.05, * p < 0.1

1: OLS; 2: OLS + Country Fixed Effects; 3: OLS + Country & Year Fixed Effects; 4: OLS + Country & Year & Month Fixed Effects; 5: OLS + Country & Year & Month Fixed Effects (without Argentina).

Source: Authors' own elaboration based on data from the central banks.

The case studies reviewed also highlight the role of previous stabilization programmes before a full-fledged Inflation Targeting regime has been adopted. During the previous disinflation phase, some countries officially declared to operate under an Inflation Targeting scheme, but others did not. Chile and Colombia were often described as Inflation Targeting countries during the early 1990s. Despite this, their policies were unconventional by most standards. For example, a system of exchange rate bands was in place until 1999 through which the central banks started to float more or less freely.

In the experiences reviewed, the disinflation phase was gradual, presumably due to the inertia of inflation and the overlapping of contracts, or the fact that a stabilization package based on an exchange rate peg (that was previously in place to control inflation) was abandoned. Thus, Inflation Targeting emerged as a reasonable nominal anchor.

While some economies successfully de-dollarized the financial contracts and managed to reduce the pass-through from exchange rate to prices, others adopted full-fledged Inflation Targeting although they seemed to pay close attention to the evolution of the exchange rate (for instance Turkey, Peru, and Uruguay). Despite some evidence of mixed success, inflation seems to remain under control, and, thus, despite its failure in Argentina and to a lesser extent in Turkey, Inflation Targeting does seem to work as a "lock-in strategy".