Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Enviar articulo por email

Enviar articulo por email Citado por SciELO

Citado por SciELO  Citado por Google

Citado por Google  Similares en

SciELO

Similares en

SciELO  Similares en Google

Similares en Google

Permalink

PermalinkBACKGROUND AND MOTIVATION

For a long time, the international pattern of aggregate savings has puzzled analysts and scholars. For example, since reliable statistics began, Latin America's saving rates (i.e., total savings over GDP) have been consistently below those of countries with similar levels of income (Edwards, 1995; Grigoli, Herman, & Schmidt-Hebbel, 2014; Reinhardt, 2008). This result persists over time and has become an intellectual puzzle as well as a policy challenge. In this article, we revisit the hypothesis of the demonstration effect theories to understand the difference in savings among countries. We take advantage of recently compiled data sets that make it possible for researchers to investigate global patterns including private savings and incomes.

Regarding the policy challenge, while it may be true that savings often seem to follow rather than lead the growth process, it has been shown that, in the long-term, insufficient domestic saving can act as a constraint on growth. Considering lingering uncertainties, various forms of market failure, and the complexities of international policy coordination, it is not too surprising that many investors from the global North choose to invest "close to home" (Bresser-Pereira & Nakano, 2003). This behaviour could explain the high statistical correlation between countries' aggregate investment and domestic saving rates (Apergis & Tsoumas, 2009; Feldstein & Horioka, 1980). At the same time, the observed regularity depicts a global economy where neither net borrower (typically capital-thirsty, investment-constrained developing country governments and companies) nor major global investors get the amounts of funds and levels of returns they and their clients expect.

Just as the "Feldstein-Horioka puzzle" exposes some of those weaknesses of the neoclassical investment theories (with implications for savings-promotion policies), empirical studies of savings variations across countries provide insights into the drivers of consumption. Despite the amount of time that has elapsed and efforts made, the is still no general, encompassing framework (Edwards, 1996; Grigoli et al., 2014; Loayza, López, Schmidt-Hebbel, & Serven 1998b; Loayza, Schmidt-Hebbel, & Serven, 2000, 2001).1 The theory of savings has traditionally been subservient to (i.e., derived from) the theories of consumption. It would not be an overstatement to say that, along with the latter, the theory of savings was at an impasse until the rapid expansion of behavioural economics (BE) over the last two decades (Deaton, 1992, 2009; Thaler & Sunstein, 2008).

For the study of savings, BE has been like a breath of fresh air, as research programmes pursuing the familiar strategy of revisiting old models with a set of new, empirically-grounded assumptions have flourished. In exchange, BE found a trove of questions and puzzles starting to coalesce around key hypotheses. BE has generated numerous insights, including those that could start to address gaps in the theories of consumer behaviour and could also explain savings. In this article, we focus our attention on one crucial deviation from conventional consumption theory: namely, interdependent preferences. Moreover, we focus more narrowly on consumption and savings at the aggregate international level; that is, we mostly investigate countries as the units of analysis.

Interdependent preferences have been studied for quite some time, and some of the key contributors have become prominent due to their determination to challenge established thinking and to work out the implications of their alternative models. As some observers have pointed out, behavioural economics more broadly belongs to a class of research that had its rebellious times and now seems to be converging to be part of a new orthodoxy (Davis, 2008). In other words, diehard "bounded rationality scholars" associated with these could be forgiven for not appreciating the novelty of the emerging consensus since they were making a living by challenging the orthodoxy well before the discipline decided to distinguish them as mavericks rather than fringe scholars.2 Others will more generally embrace the new realities, taking advantage of this "progressive" moment (in terms of Lakatos) to explore grounds opened by the accumulation of refutations afflicting the old programme.

As it befits a "progressive" research programme, BE is at the stage of demonstrating its "encompassing" power, or competing to show that it can answer a broader set of questions than the alternative programmes. New BE models seek to establish regularities from the lab and the field (Bagwell & Bernheim, 1996; Easterlin, 1974, 1995; Frank, 2005; Goodwin, Ackerman, & Kiron, 1996). They aim to derive the implications of partially replacing the foundational neoclassical assumptions about rationality, self-interest, and preference maximization over non-standard objectives (Castilla, 2010; Leibenstein, 1950; Rojas, 2008; Rojas & Jiménez, 2008).

Partly stimulated by the success of current BE stories, we offer a "prequel" to the current wave of paradigm-shifting, which takes us back roughly to the end of the Second World War. Thus, from the variety of behavioural patterns identified by BE, we probe more deeply into the possibility of observing, at a macroeconomic level, empirical regularities that are consistent with the individual/ household patterns of emulative consumption. The latter were most consistently exposed by the likes of Ragnar Nurkse and James Duesenberry, who spoke explicitly about a "demonstration effect" linking individuals' choices through comparisons and consumers' desire to access the living standards of those better off. More specifically, as Nurkse puts it, "When individuals come into contact with superior goods or spending patterns, they are apt to feel a certain tension and restlessness: their propensity to consume is increased." (Nurkse, 1953, p.578) And attributing it to Duesenberry, (citing the latter's Income, Saving and the Theory of Consumer Behavior), Nurkse observes "That (...) individuals' consumption functions are interrelated rather than independent helps to account for certain facts that have seemed puzzling (...) in particular, the choice between consumption and saving." (Nurkse, 1953, pp. 577-78).

Nurkse (1953), who saw a direct link between consumption patterns and the problem of capital formation, writes about the extrapolation of a plausible model of individual behaviour from the dynamics of macroeconomic aggregates. Research labelled "representative individual" has set off the alerts and prevents us from taking those statements lightly. Writing about the individual level demonstration effect, he declared that "These forces, it seems to me, affect human behaviour to a certain extent in international relations as well" (Nurkse, 1953, p. 578). The emphasis added is about all there is in the article to justify leaping from many individuals to one representative individual. We shall return to these issues below when examining the results of our econometric study.

The study of aggregate private savings is inevitably constrained by the quality of available data. Today, many countries keep up to date national macroeconomic accounts. By taking away current consumption from current income, they get rudimentary savings statistics. Fewer countries are capable of breaking it up into government and private savings; a very small group undertakes surveys of household finances with some frequency. These, which are the accepted international best practices for estimating savings using sound microeconomic data, are available only to a small group of countries, typically those that have functioning oversight institutions in the financial sector. This creates the demand for data and contributes the resources needed to justify and defend the provision of the public good.

The paucity of those surveys is a serious obstacle for those wanting to tackle some the substantial issues of interest. Confronted with such challenges, we adopt a pragmatic approach, exploiting the available data while acknowledging the studies' limitations. Studies such as those undertaken by Cavallo and Serebrisky (2016) are good examples of what should become more widespread: the integration of macro and microdata. In the meantime, while these studies become more prevalent, we maintain that there are still substantive issues that can be analysed with the available data. In this article, we manage to compile a panel from 133 countries between 1990 and 2012.

The rest of the paper is structured as follows: In the next section, we describe some stylized facts about saving across countries and regions based on the available empirical record. In section 3, we discuss alternative explanations ("mechanisms") that may account for demonstration on a country level. Section 4 presents the methodology for our analysis and describes the data and the estimation model based on panel data techniques. Section 5 discusses the main results that nurture our confidence in the interdependence hypothesis as well as the corresponding caveats. We close by summarizing conclusions and providing elements for a future research agenda.

STYLIZED FACTS ABOUT SAVING ACROSS COUNTRIES

Saving rates do vary across countries and time (Edwards, 1995; Grigoli et al. 2014; Loayza et al. 2001). Since the 1960s, there has been a process of divergence among saving rates, in particular among the developing countries: while saving has remained higher in East Asia, it stayed stagnant in Latin America and has not improved that much in Sub-Saharan Africa. For instance, saving rates in East Asia and the Pacific fluctuated around 33.2% of GDP, and Latin America and the Caribbean have experimented historically low domestic saving rates, on average around 21.1% of GDP between 1960 and 2015 (Table 1). Meanwhile, the high-income countries (except the United States) have remained, on average, among those with the highest saving rates, though the mortgages crisis disrupted this and allowed East Asia to improve its figures in relative terms.

Table 1 Gross Domestic Saving As a Percentage of GDP (%) by Regions and Income Levels by Decades (1960-2015)

| Regions | 1960-1970 | 1970-1980 | 1980-1990 | 1990-2000 | 2000-2015 |

|---|---|---|---|---|---|

| East Asia and Pacific | 32.1 | 32.6 | 33.8 | 33.9 | |

| Europe and Central Asia | 27.5 | 25.2 | 22.9 | 23.6 | 23.5 |

| Latin America and Caribbean | 20.4 | 22.1 | 22.7 | 19.4 | 20.9 |

| The Middle East and North Africa | 32.9 | 37.6 | 21.7 | 24.2 | 36.3 |

| North America | 23.7 | 22.8 | 21.7 | 20.3 | 17.6 |

| South Asia | 13.2 | 15.2 | 18.3 | 21.5 | 27.5 |

| Sub-Saharan Africa | 18.8 | 16.9 | 19.2 | ||

| Income levels | |||||

| High income | 26.1 | 24.0 | 23.6 | 22.2 | |

| Low-income | 4.3 | 4.9 | 7.4 | ||

| Middle-income | 26.3 | 27.2 | 28.1 | 31.7 | |

| World | 23.6 | 26.1 | 24.8 | 24.8 | 24. |

Sources: The authors' elaboration based on World Development Indicators from World Bank. https://databank.worldbank.org/source/world-development-indicators

A lot has been written about Latin America's aggregate underperformance, and we do not have the space or scope to add much in that regard; however, a quick look at the savings challenges in the region confirms that inadequate savings can still stall incipient growth despite the combined efforts of local policymakers and international institutions. In the region, it has been argued that, despite the financial reforms of the nineties and the macroeconomic stability achieved by a great number of these countries, in the last decade, savings have stayed quite stable and remained lower than in other regions, especially compared to East Asia (Cavallo & Serebrisky, 2016; Gavin, Hausmann, & Talvi, 1997; Gutiérrez, 2007; Reinhardt, 2008). Empirical research supports the Feldstein and Horioka (1980) hypothesis for most Latin American countries, implying that growth may be constrained by investments that, in turn, are hampered by low domestic savings (Gutiérrez, 2007). This reliance on foreign markets brings more vulnerability to the Latin American economies, which are attached to highly volatile processes.

During the nineties, several studies focused on the long-term disparities in saving rates, seeking to identify levers for public policy. Some of those studies were outcomes of the World Bank's "Saving across the world" project, which created a database covering over a hundred countries (developing and industrialized), and a time span of over three decades (1960-1994). The studies linked to the database include Schmidt-Hebbel and Servén (1997) and Loayza et al. (1998a, 2000, 2001). Loayza et al. (2001) summarize the main empirical findings of the group of contributions and highlight some stylized facts that stand out for that period. These state that there is a positive correlation found both in longitudinal and in cross-section samples between saving rates and income levels. In addition, this positive correlation is also found between saving rates and income growth (i.e., those economies with higher income growth have higher saving rates) though this relation is stronger for the industrialized countries. This fact has been explained by the virtuous cycles of saving and prosperity, in one case, and by low savings and poverty traps, in the other, evoking Kaldor's contributions on the matter. Another fact that those studies showed was a positive correlation between saving and domestic investment, confirming the Feldstein and Horioka (1980) thesis. In the same vein, Grigoli et al. (2014) present new evidence on the behaviour of saving across the world that confirms some of the previous results and brings new findings. More recently, the Inter-American Development-Bank published a group of studies edited by Cavallo and Serebrisky (2016) that analysed the role of saving for development, and worried about the low saving rates of Latin America and the Caribbean.

Among the empirical studies based on cross-country data, some have focused on national savings, while others go further and disaggregate private and public saving. Loayza et al. (2000) use data on 69 industrialized and developing countries for 1965-1994 to explain national, private, and public saving. Edwards (1996) analysed the determinants on private saving for 36 industrialized and developing countries between 1970-1992. Gutiérrez (2007) focused on national saving in nine Latin America countries for a period after mid-1990, and also, within the private sector, distinguished between household and enterprise savings. Reinhardt (2008) studied the domestic savings among middle-income countries between 1976-2000. Freytag and Voll (2013) used a cross-country sample of 60 developing countries and emerging economies from 1980 to 2007. Grigoli et al. (2014) provide evidence for a large period, 1981-2012, that covers 165 countries. They analyse the determinants of private and national savings and distinguish household and corporate savings. In other papers, these authors focus on Latin America and the Caribbean (Grigoli et al. 2014). Becerra, Cavallo, and Noy (2015) also analysed the Latin American private saving regions, finding evidence that reinforced the low saving pattern characterizing this developing region.

Most of the empirical studies agree on some key determinants to explain the difference between national and private saving rates (Edwards, 1995; Grigoli et al. 2014; Loayza et al., 2000; Reinhardt, 2008). Variables such as economic growth (per capita income growth), income level, and public saving may have important impacts on increasing saving rates, as suggested by both theory and empirical evidence. Such is the case for government savings. According to the Ricardian Equivalence, there is a trade-off between an increase in government saving and a reduction in private saving. This hypothesis is an extension of the permanent income hypothesis and predicts that, as long as some conditions are satisfied, an increase in permanent government consumption is fully offset by lower private consumption (Grigoli et al. 2014). In the life-cycle model, consumption and saving patterns follow an inverted-U. Therefore, we would expect that economically active people will save more and the elderly and the youth will save less. There is no conclusive evidence for this hypothesis: in some cases, the dependency rate appears to be negatively related to savings, but in other studies, the result is not significant. Empirical works do not generally support the effect of macroeconomic uncertainty. There may be some trade-off between external and domestic saving, but it is not complete (Rodrik, 2000).

Finally, the interest rate, the soundness of the financial system and income distribution show ambiguous results. More recently, some authors introduce the effect of institutions on savings in developing and emerging countries, finding a positive relation between saving and the "quality" of institutions suitably defined and measured (Freytag & Voll, 2013)

The literature synthesizes some interesting insights but, as a whole, it still has not reached satisfactory outcomes. Only a few factors consistently appear to be robust determinants of the differences among countries. Advancing in identifying key factors and coherent sets of mechanisms that could account for them is of great importance from policy as well as scientific perspectives.

The meticulous work undertaken by the research teams that have investigated these issues suggests that significant advances in the understanding of savings may not occur by travelling the same beaten paths. In this paper, we propose to recover a hypothesis with a respectable pedigree that has not been so thoroughly examined in recent times and then explore its empirical plausibility. The relative income or demonstration effect theses introduced by Duesenberry (1949) and later extended by Nurkse (1953) becomes a strong candidate framework to shed new light in a field that may be needing it.

THE DEMONSTRATION EFFECT: MECHANISMS

From a development perspective, it is worth exploring the mechanisms that could logically connect demonstration effects with chronic lack of private savings. Filgueira (1981) was among the keen observers who noticed that the Latin American puzzle was not unrelated to the consumption bias of the economic booms of the 1970s. The latter were mostly consumption booms in those countries (as opposed to fundamentally investment-driven booms), and consumer behaviour revealed extraordinarily high discount rates that explained the extended use of credit by households to buy conspicuous durable goods.

Demonstration effects have points of contact with related concepts and research programmes that should be acknowledged. In chronological order, Thorstein Veblen's theory of conspicuous consumption (introduced in his 1899 Theory of the leisure class) rests on the observation that goods have a ceremonial or symbolic value in addition to their instrumental value. At any point in time, there is an appropriate level of ceremonial goods, used or consumed, for each group in society, and consumption of those goods would signal one's or a group's rank in society. Veblen's institutionalist theory rejects optimizing rationality, regardless of its broader influence beyond institutionalist circles.

About 50 years later, James Duesenberry found a puzzle in the declining aggregate savings rates that accompanied the growth of income in the U.S. soon after World War II (Duesenberry, 1949). The expectation was that savings and income would move in the same directions, but that was not what the data was showing. He then observed that the emulative consumption hypothesis would solve the puzzle. The upward imitation of relatively poorer consumers, of the patterns of expenditures made by the relatively richer, constitutes an interdependence mechanism that could explain the savings gap. Nurkse argued that the imitation was driven by the aspiration to enjoy experiences previously restricted to the relatively richer. Confronted with incomplete information about the real worth of consumer goods, consumers would be guided by the rich's choices to infer what they should be buying. Nurkse also laid down two features of international demonstration effects that may be taken to be part of "the mechanisms". "One is the size of the gaps in real income and consumption levels. The other is the extent of peoples' awareness of them." And, to leave no doubts, "The leading instance of this effect is at present the widespread imitation of American consumption patterns" (Nurkse, 1953, p. 578).

The research community did not immediately jump to embrace Duesenberry's model: a model that could demonstrate that, under interdependent preferences, progressive income tax rates were Pareto efficient. Duesenberry's model was not a usual feature in microeconomic textbooks until recently. With the Great Recession of 2007-2009, many authors from varied persuasions have given renewed attention to the peculiar syndrome of (i) falling households' savings, (ii) large accumulation of debt, (iii) growing use of debt to finance consumption, and (iv) raising inequality. All of these are apparently connected to the aspiration to "keep up with the Joneses" (Frank, 2005; Frank & Heffetz, 2011; Ray, 2011).

Halfway through this journey, we shall encounter Jeffrey James's (1987) analysis of Veblen's vs. non-Veblenian models of interdependent preferences. He shows that unlike Veblen's framework, Nurkse's and Duesenberry's rest on the information consumers receive about the features of goods consumed and the "restlessness" those consumers experience when they are made aware of the superior qualities of goods purchased by others with a higher status in society. Product variation and the needs "created" by advertising in its "informational" role remain crucial to the work of these mechanisms that have the potential to shape industrial structures, prompt innovation, and-more importantly for our purposes-become determinants of aggregate savings and inequality.

METHODOLOGY

Our empirical approach is based on a cross-countries analysis with the main purpose of identifying the main factors that explain the inter-country variation of private saving rates paying special attention to variables that reflect the presence of emulation patterns affecting saving decisions. A panel data analysis is used which includes cross-section data for countries from all over the world. The panel is unbalanced as not all data are available for every country for every year, so we end up estimating the model for the period 1990-2012 as we have complete information for all the variables included. We use a model based on linear regression with individual effects in the base, and we run panel data estimations, using different alternative specifications (fixed effects, random effects, and dynamic estimators).

Data

The dependent variable is the rate of gross private saving (PS) as a percentage of gross domestic product (GDP). Private saving is computed as the difference between the ratio of gross national saving and government savings (as a percentage of GDP).

The explanatory variable includes two types of effects. We rely on a group of variables that have been widely used in empirical works exploring the effect on the private saving of those factors, which drives directly from the standard theories briefly discussed in the previous section. First, we include the growth rate of per capita GDP as a measure of economic growth and constant GDP per capita (in logs) to evaluate the effect of income levels. The public saving rate (actually, we used the general government saving as a percentage of GDP) allows us to test the partial Ricardian equivalence hypothesis which expects a trade-off between an increase in government saving and a reduction in private saving. The foreign saving rate (measured as the deficit current account balance as a percentage of GDP) is included to look for the trade-off between private and foreign saving. Macroeconomic uncertainty is reflected using the inflation rate as the annual variation of the consumer price index.3 Financial depth is measured as the ratio of money and quasi-money (M2) to GDP. The real interest rate is calculated by adjusting the deposit interest rate by the inflation rate. Income distribution is measured by the GINI coefficient.

The life-cycle hypothesis, which predicts lower savings among the elderly and youths and larger savings among economically active adults, is tested by the introduction of two socio-demographic, dependency indices: the young age dependency rate and the old-age dependency rate. This distinction aims to capture the diverse place of the countries in the demographic transition process, and the corresponding pressures on labour markets and the financing of old age. We calculate the young-age dependency rate as the ratio between those younger than 14 to the people between 14 and 65, and the old-age as the ratio of those older than 65 to those with ages between 14 and 65.

At the same time, we need a variable, which reflects the mechanism of the demonstration effect. Bases on theory (e.g., Duesenberry, 1949; Nurkse, 1953; Frank, 2005; James, 1987; Schor, 1998) we expect that the richer and more abundant the information consumers receive about superior goods purchased by others with a higher status, the greater the stimulus they receive to obtain more desirable goods. More and better information about the consumption patterns of the rich(er) individuals, and nations, will influence the consumer's choices to acquire more. This emulation behaviour will result in a reduction of savings. To see this, dia-grammatically, we can state the following causal chain:

Greater media penetration of → Greater exposure to info about better goods - Stimulus to buy more than before → Smaller savings ratios

Based on the theoretical definition of the demonstration effect, as explained by Nurkse (1953), and the study of consumers' behaviour pioneered by Galbraith (James & Liste, 1980; Schor, 1998), to mention a few, are most visible when we use two communication media (TV and internet) the penetration of which peaked at different times in the sample period. One traditional mechanism in which these different types of media affect the behaviour of consumers is through advertising some products. We can understand advertising according to James and Lister's (1980) definition: "(...) it constitutes merely a part of the general cultural environment and flows of information to which people are exposed" (p. 91).

Advertising influences consumer behaviour, and, in some case, may shape the relatively poorer both directly and via the effect it has on the desires of the rich (James & Lister, 1980).

First, we use the number of TV sets per 100 inhabitants. An example of the effect of this communication media is Schor (1998) who used a Veblen-inspired study of the individual decisions on spending and found that those who watched TV more saved less, conditionally on the other regressors (Oh, Park, & Bowles, 2012). We also used another indicator (internet users) to measure the exposure to other consumption patterns. This variable is defined as the percentage of the population with access to the worldwide network.

An important advantage of this type of information is that it is available to cover the sample and the period under study. The information on TV sets is available since the beginning of the period, and for most of the countries, the series covers all the period. As for the number of internet users, the database has more information from 2000, although there are some sporadic figures for some countries for previous years. Using these two variables alternatively, we aim to capture the demonstration effect along the whole period under study. The characteristics of these two communication mediums are different if we think about the product lifecycle. TV infrastructure and home equipment have had a widespread telecommunication presence since the 1980s, but the internet is a relatively new network communication medium. In our empirical exercises, we will expect a negative statistical association between the number of TV or internet users (as measures of media penetration) and the saving rates. This is one plausible outcome of the empirical study carried out, but it is not exempt from the implications of the aggregation issues.

In general, we used several sources to build the database: World Economic Outlook Database of the International Monetary Fund (WEO-IMF); the World Development Indicators published by the World Bank (WDI-WB); International Telecommunication Union of the United Nations (ITU-UN), and other national organisms when specific data for some countries was missing. Further details on the sources and definitions of the variables can be found in the Appendix (Table A1).

Method

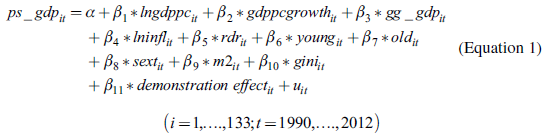

The base equation explaining private saving as a percentage of GDP (ps _ gdp) might be expressed as (Equation 1):

µ it = µ i +λ t +v it

Where i refers to countries (the cross-section dimension, t denoting years (time-series dimension), α is a constant and u it is the error term. Then we have a group of explanatory variables with their respective parameters, β 1 to β 11, where:

Ingdppc is the logarithm of real GDP per capita, adjusted by purchasing power parity (expressed in 2005 international U.S. dollars).

gdppcgrowth is the annual growth of GDP per capita (in percentage)

gg-gdp is the general government saving (as a percentage of GDP)

Ininfl logarithm of the inflation rate (in percentage)

rdr is the real interest rate (in percentage)

young is the young age dependency rate

old is the old-age dependency rate

sext is the external saving rate (as a percentage of GDP)

m2 is the financial depth (as a percentage of GDP)

gini is the GINI index

demonstration effect is the demonstration effect

The error term µ it includes a country-specific effect, µ it , which is unobservable, as well as the disturbance v it . The individual effect is time-invariant and accounts for any country-specific effect that is not included in the regression. In some of the models, we include time-dummies, λ t individual-invariant to account for timespecific effect that is not included in the regression. For instance, these time variables may control for those external shocks that may affect all the countries.

Depending on the assumptions we make about the behaviour of the country effects, there are different model specifications. On the one hand, the fixed effects model (FE) assumed that the explanatory variables are independent of the disturbance for all units and over time but are correlated with the country effect µ i .. The disturbances stochastic v it is independent and identically distributed IID (O, σ 2 v ), and the individual effects are considered as a group of N additional coefficients that are estimated together with β coefficients. This model relies exclusively on the time variation within the units. For this reason, the estimator is named the within estimator (Baltagi, 2012).

On the other hand, in the random effect model (RE), the country effect µ i are assumed as a random constant term over time and independent of the disturbance v it and the explanatory variables x it . In this case, the individual effect becomes part of the error component, and, therefore, these models are also called random error component models.

The problem we face is whether to compare private rates that differ between countries and vary over time within countries. Therefore, we run the panel data using alternatively fixed effects and random effects. The basic difference between both models is the hypothesis of no correlation between the regressors and the individual effects (Baltagi, 2012). The RE model assumes exogeneity of all the regressors with the random individual effects, while the FE allows for the endogeneity of all the regressors with these individual effects. We test this hypothesis using the Hausman test, which is based on the difference between fixed and random estimators.

For those models, we use FE, and we perform the F-test to test whether the country effects are zero. A rejection of this hypothesis means that the fixed effects are not zero, which is not equal across countries. We use RE for those models, and we perform the Breusch-Pagan significance test. Finally, in all the cases, we use robust standard errors when estimating the coefficients.

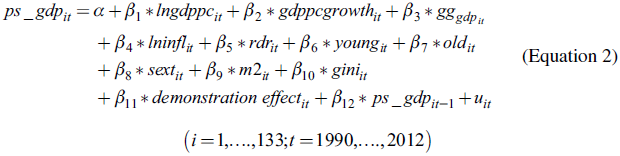

In addition, other problems arose when working with economic relationships. These relationships turn out to be dynamic. In our model, it is plausible that there are some effects of past saving behaviour on the actual rates of saving, which converts the static model in a dynamic one (Edwards, 1996; Grigoli et al. 2014; Loayza et al., 2000; Reinhardt, 2008). This dynamic relationship is characterized by the presence of a lagged dependent variable among the regressors (Baltagi, 2012, p. 147) (Equation 2):

To estimate the dynamic panel (Equation 2), we used the methods proposed by Arellano and Bond (1991), which was generalized and extended by Arellano and Bover (1995). To implement the Generalized Method of Moment's estimators (GMM) suggested by these authors, we ran the xtabond2 command for Stata programmed by Roodman (2009). Two lists of variables are needed for this estimation.4 A group of endogenous variables that include income level, economic growth, inflation, real deposit rate, is instrumented with GMM-style instruments. In this case, we use the second lag values of the variables in levels. The second group of explanatory variables includes all the strictly exogenous ones, and we assume the public saving, external saving, demonstration effect (TV and internet), old dependency rates and Gini index. Therefore, for these variables, the programme will use them as their own instruments. We could also use the Arellano-Bond difference GMM or the system GMM. The system GMM is a better method when the lagged values of the regressors are poor instruments for the first-differenced regressors. The system GMM estimator uses the level equation to obtain a system of two equations: one differenced and one in levels, and it usually increases efficiency.

Three additional tests are offered with the command xtabond2. Two diagnostics are computed using Arellano and Bond GMM procedure to test for first-order and second-order serial correlation of the residuals. One should reject the null of the absence of first-order serial correlation, and not reject the absence of second-order serial correlation. A special feature of dynamic panel data GMM estimation is that, if T is large, the number of moment conditions increases. Therefore, the Sargan test is performed to test the over-identification restrictions. Too many moment conditions introduce bias while increasing efficiency. Stata reports the Hansen J statistic, instead, but it keeps the same null hypothesis that the instruments as a group are exogenous, and, therefore, we expect not to reject it.

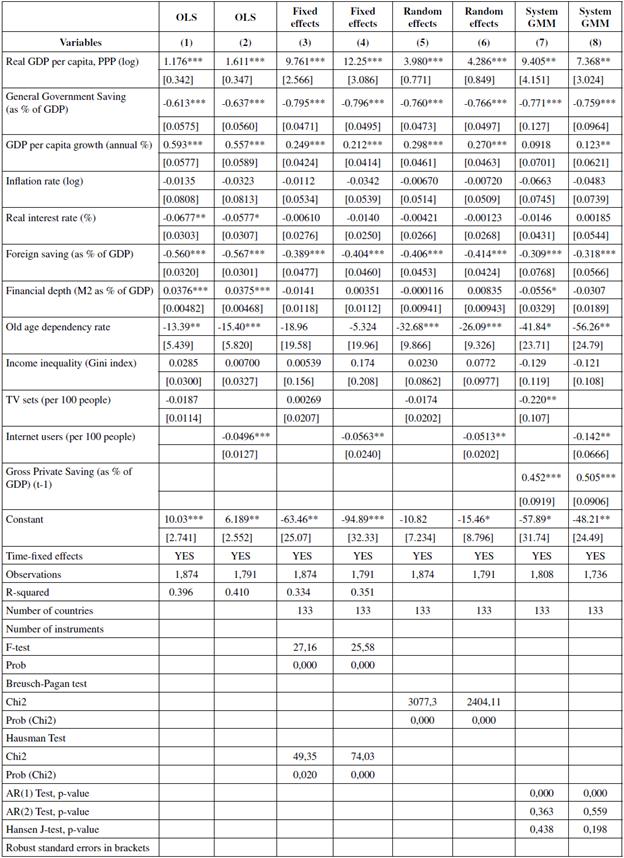

Empirical Results

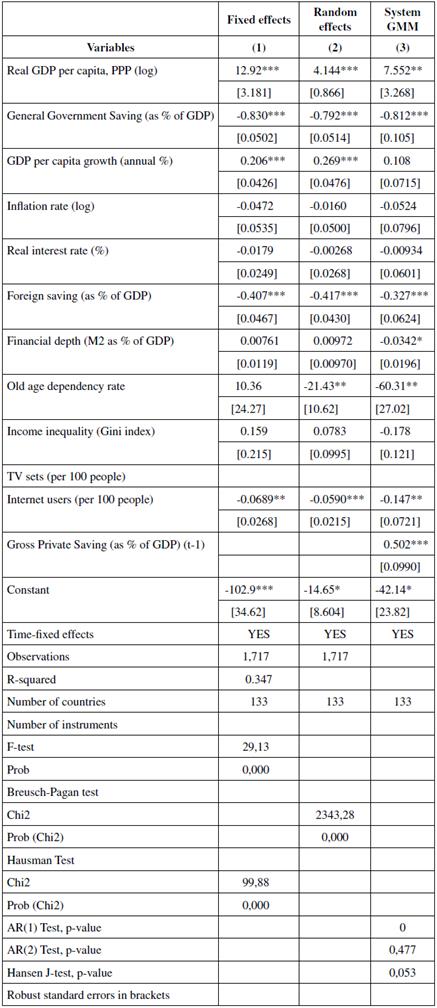

The results of the econometric estimations are presented in Table 2. We run several estimations exercises. The baseline model is the one we run for the world sample between 1990-2012. We alternatively use two measures of the demonstration effect: TV sets (per 100 people) and internet users (per 100 people). The coverage of these two variables is different. The information on TV sets has very good coverage in our database. For the internet, the data has been available in the surveys since 1990 although the data is better after 1995.

Table 2 Estimation Results of the Panel Data (1990-2012). Dependent Variable: Private Saving (As a Percentage of GDP)

For each model, we run ordinary least squares (OLS, columns 1 and 2), fixed effects (FE, columns 3 and 4), and random effects (RE, columns 5 and 6). For all cases, we use robust standard errors. We compare the levels and significance of the coefficients, and we chose the better specification, following the result of the Hausman test. A rejection of the null hypothesis of a correlation between the individual effects and the regressors was interpreted as the adoption of fixed effects, and we adopt random effects when there is no rejection of the hypothesis. We include time-dummies variables for all cases.

For the dynamic model, we use the system GMM estimator, which allows us to control for unobserved country-specific effects and potential endogeneity of the regressors. In general, the results obtained with GMM system estimator are similar to those obtained with the other estimation techniques. There are some exceptions which we will comment upon.

We summarize the key findings and the story that could be told about Nurkse's type of international demonstration effects that influence private savings in the aggregate.

As previously stated, we address the research question using two alternative indicators for the demonstration effect: the number of TV sets and the number of internet users. In the case of the models with fixed effects (Columns 3 and 4) and system GMM (Columns 7 and 8), the following paragraphs show the main findings.

Measured by internet users, the demonstration effect has a negative effect on saving (with a significant level of 5%). This result is independent of whether we use fixed effects (Column 4) or System GMM (Column 8). When we include TV sets, we find a negative and significant coefficient in the dynamic model (Column 7). However, we do not find a significant effect on the fixed effects regression (Column 3).

The coefficients of per capita income (in logarithms) and income growth are positive and significant at 1% or 5% for most of the cases. As outlined by Loayza et al. (2000) the positive effect of income on private saving implies that economic policies promoting growth are an indirect but effective channel to increase saving. Considering that part of the increase in saving becomes the financial support of domestic investment (following the evidence from Feldstein & Horioka, 1980), successful growth policies may result in a virtuous cycle of saving, capital accumulation, and growth. The exception is that income growth seems to lack statistical significance when we run the GMM system and include the TV sets. The financial factors measured by the real interest rate and the financial depth (M2/ GDP) appear to have no statistically significant effects on private saving in most of the cases. The only model in which financial depth shows a significant negative effect is in the dynamic model (System GMM), although with a 10% level of significance. This relatively weak result poses some doubts about the effectiveness of the financial reforms to promote saving. The proxy of macroeconomic uncertainty, inflation rate, appears to have a negative but not significant effect on private savings. Fiscal policy influences private saving. The government saving ratio shows a statistically significant and negative effect on private saving rate, a result in line with the literature review: i.e., there is partial Ricardian equivalence. The result of foreign saving is in line with some empirical works. We find a negative and statistically significant effect on private saving.

The demographic variable included -old dependency rate- has a statistically significant negative effect on the dynamic models -with a 5% and 10% level of significance- except in the fixed effects regressions. This result means that there is some evidence to support the life-cycle hypothesis. Income distribution (measured using the GINI index) seems to not be significant in explaining private saving.

Finally, the outcome of the system GMM models shows a persistence effect of past private saving on the present rates, based on the positive and significant effect -with 1% significance- of the lagged value of the saving rate.

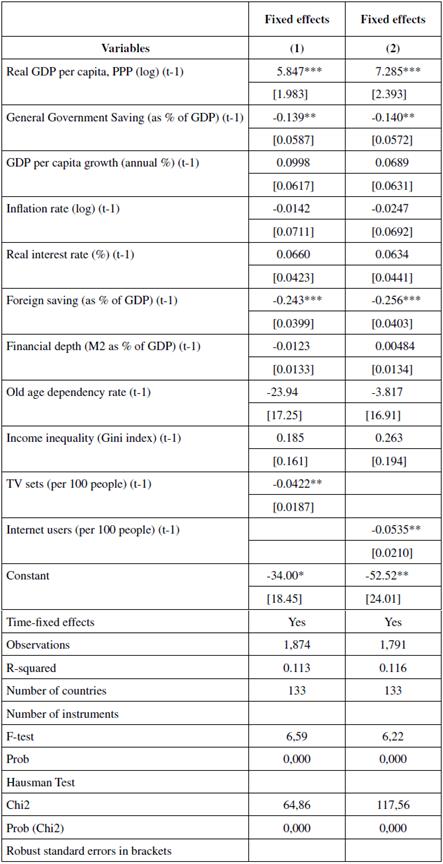

We estimate the models with alternative specifications to test the robustness of our results (see the Appendix with the outputs). First, we check the robustness of the results for a shorter period (1995-2012) for those models in which we include internet, as the data for this variable is better from 1995 onwards (See Table A2). The main results do not change; in particular, the negative impact of the demonstration effect, measured by internet users, on private saving keeps its statistical significance-at 5%. Additionally, income level and growth, foreign saving, and fiscal policy show significant effects on private saving.

Second, another drawback the model may have is that some of the explanatory variables may be endogenous. Some authors use the lagged values of the independent variables to mitigate -but not fully resolve- the presence of endogeneity (Table A3). We use the first lags of the explanatory variables and run the fixed effect models. The exposition variables maintain their negative effect on private saving, and we find a significant coefficient for internet users and for TV sets. As for the case of the other explanatory variables, the main difference with the model without lags is that economic growth is no longer significant.

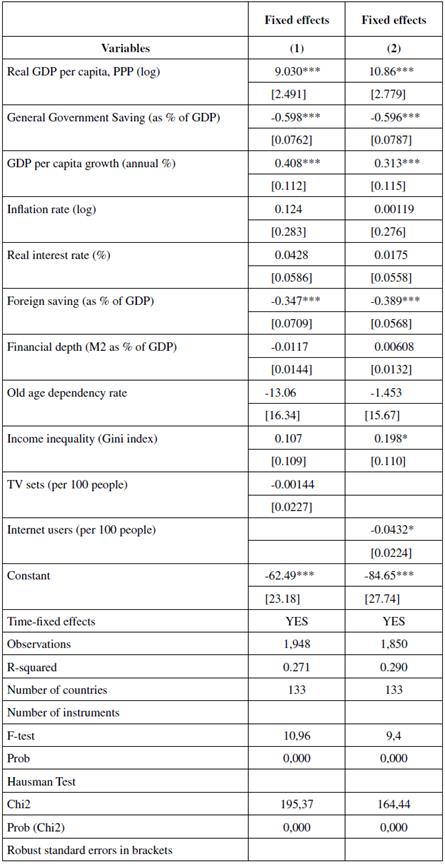

Third, since we are working with several macroeconomic variables that may contain cyclical movements for some periods, we run estimations with five-year moving averages of the variables, and we run the fixed effects estimators (Table A4). Regarding the exposition effect, TV does not appear to be significant, but the internet maintains its negative effect on private savings. The results of the coefficients of the rest of the variables are the same as the models based on annual observations.

In sum, the main control variables have the correct signs and significance levels. We find a negative statistical relationship between the demonstration effect (captured by the TV sets and internet) and the private saving rate.

CONCLUSIONS

Throughout the world, it has been proved that it is hard to find stable regional patterns of private savings. These stylized facts remain intellectual puzzles and development policy challenges. In addition, despite the difficulties discerning causes and effects, it has been shown that, in the long-term, it is not possible to grow sustainably with domestic savings persistently below investments. For these and other scientific considerations, understanding the determinants of savings is an important research objective that has previously raised challenges to analysts who tried to make sense of results from varied, distinct models.

This paper aims to bring together two strands of the literature. On the one hand, several empirical studies have explored the determinants of saving rates across countries, but they are far from conclusive. On the other hand, a growing literature is working with the hypothesis of emulation patterns between consumers and their reference group, moving away from the neoclassical assumption of independent preferences to explain consumption and saving. The main purpose was to study the behavioural patterns of saving to understand the performance of private savings. We provide empirical evidence to discuss the emulation patterns between consumers as a driver of private savings, using a macro approach based on cross-country analysis.

We use panel data techniques to explain the statistical relationship between the emulation patterns and the private saving rate based on data from 133 countries for the period between 1990-2012. We estimate several models (fixed, random, and dynamic models), so we can compare the results and arrive at robust conclusions. We used two media indicators to reflect the effect of societies' changing exposure to foreign cultural and consumption styles of the demonstration effect: TV sets and internet users. After controlling for the standard regressors, we found that the international demonstration effect measured by internet users has a negative effect on private saving and is statistically significant. In addition, these results are robust after estimating different models. When using TV sets, we find a negative and significant effect in the dynamic model but not for the fixed effects.

The discussion on the mechanisms that may account for a demonstration effect, and the empirical evidence we find, provide useful insights in order to understand the differences in private savings across the world. Synthesizing and emphasizing the substantive results, the empirical analysis shows that the global pattern of private savings maintains a strong influence of income level and income growth; government and foreign savings; and old-age dependency ratios. We find evidence of a statistical association between greater exposure to global trends via some global medium and smaller savings rates. The hypothesis of demonstration effects can be a candidate explanation. However, we do not perform any exercise to analyse the causality of this relation. This could be a possible area for future research.