Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkInnovar

Print version ISSN 0121-5051

Innovar vol.20 no.37 Bogotá May/Aug. 2010

Jesús García-de-Madariaga* & Fernando Rodríguez-de-Rivera-Cremades**

* Spanish, assistant professor, Marketing Department, Universidad Complutense de Madrid (Spain). PhD in Economics and Business Administration by Universidad Complutense de Madrid. His work focuses on several issues related to corporate social responsibility, customer relationship management and marketing information systems. Refereed international journals have published his research. He is also an active marketing research consultant. E-mail: jesusmadariaga@ccee.ucm.es

** Spanish, Marketing Department, Universidad Complutense de Madrid (Spain). PhD candidate in Economics and Business Administration by Universidad Complutense de Madrid. His research interest lies in customer relationship management. E-mail: fernando.rodriguez.cremades@estumail.ucm.es

RECIBIDO: junio 2008 APROBADO: septiembre 2009

ABSTRACT:

There has been a lot of discussion about corporate social responsibility (CSR) during these last decades. Neoclassical authors support the idea that CSR is not compatible with the objective of profit maximization, and defenders of CSR argue that, in these times of globalization and network economies, the idea of a company managed just to meet shareholders' interests does not support itself. However, beyond this discussion, how can CSR affect firms' market value? If we found a positive relationship between these variables, we could conclude that the two theories are reconcilable and the objective of profit maximization, perhaps, should satisfy not only shareholders' interests, but also stakeholders'. We review previous literature and propose a model to analyze how CSR affects firms' market value.

KEY WORDS:

corporate social responsibility, classical theory of firms, stakeholders and market value.

RESUMEN:

Ha habido mucha discusión acerca de la responsabilidad social empresarial (RSE) durante las últimas décadas. Autores neoclásicos apoyan la idea de que la RSE es incompatible con el objetivo de maximización del beneficio, mientras los defensores de la RSE argumentan que, en estos tiempos de globalización y economías de red, la idea de una compañía manejada únicamente para suplir las necesidades de los accionistas no es sustentable. Más allá de esta discusión, sin embargo, ¿cómo puede la RSE afectar el valor de mercado de la empresa? Si encontráramos una relación positiva entre estas variables, podríamos concluir que las dos teorías no son irreconciliables y que el objetivo de la maximización del beneficio debe quizás satisfacer no solamente los intereses de los accionistas, sino también los de los stakeholders. Revisamos la literatura anterior y proponemos un modelo para analizar cómo la RSE afecta el valor de mercado de la empresa.

PALABRAS CLAVE:

Responsabilidad Social Empresarial, Teoría Clásica de la Empresa, stakeholders y valor de mercado.

RÉSUMÉ:

Un débat important a eu lieu dans les dernières décades sur la Responsabilité Sociale des Entreprises (RSC). Les auteurs néoclassiques appuient l'idée que la RSC est incompatible avec l'objectif de maximisation du bénéfice tandis que les défenseurs de la RSC considèrent qu'à l'époque de la globalisation et des économies de réseaux, l'idée d'une entreprise gérée seulement pour satisfaire les intérêts des actionnaires est insoutenable. Cependant, au-delà du débat, une question se pose : comment la valeur du marché des entreprises est-elle affectée par la RSC ? Si nous trouvions un rapport positif entre ces deux variables, nous pourrions conclure que les deux théories sont réconciliables et que l'objectif de la maximisation du bénéfice pourrait probablement satisfaire non seulement les intérêts des actionnaires mais aussi de tous les stakeholders. Les publications antérieures ont été revues et un modèle est proposé pour analyser comment la RSC affecte la valeur de marché des entreprises.

MOTS-CLEFS:

Responsabilité Sociale Corporative, Théorie Classique de l'Entreprise, stakeholders et valeur du marché.

RESUMO:

Nas últimas décadas tem havido um grande debate sobra a Responsabilidade Social das Empresas (RSC). Os autores Neoclássicos apóiam a idéia de que a RSC não é compatível com o objetivo da maximização do benefício enquanto que os defensores da RSC argumentam que, na era da globalização e as economias de redes, a idéia de uma empresa gerida unicamente para satisfazer os interesses dos acionistas não se sustenta. Sem embargo, mais além do debate, como a RSC afeta o valor de mercado das empresas? Se encontrássemos uma relação positiva entre ambas variáveis, poderíamos concluir que ambas as teorias são reconciliáveis e que o objetivo da maximização do benefício, talvez satisfizesse não só os interesses dos acionistas, mas de todos os stakeholders. Revisamos a literatura anterior e propomos um modelo para analisar como a RSC afeta o valor de mercado das empresas.

PALAVRAS CHAVE:

Responsabilidade Social Corporativa, Teoria Clássica da Empresa, stakeholders e valor de mercado.

INTRODUCTION

On September 13, 1970, Milton Friedman published one of his most famous articles in The New York Times Magazine, entitled "The Social Responsibility of Business is to Increase its Profits." In this article, Friedman argued that the only objective of firms was to increase profits for their shareholders, and they considered any other aim an action aginst owners' interests. like Milton Friedman, most neoclassic theorists have traditionally supported that corporate social responsibility (CSR) is incompatible with the classic principle of profit maximization as the main objective for firms. As Friedman said (1970), there were only two restrictions to achieve that objective: law and ethics.

The situation has changed since Milton Friedman's article. Nowadays, firms face a different business environment. During the seventies and the eighties, companies just tried to carry out exchanges with customers in a stable environment. Concepts such as satisfaction or loyalty began to emerge, and firms more or less controlled the messages that consumers received. Society was not too demanding towards companies and the price was the most important issue to negotiate when firms tried to manage their relationships with their suppliers. Even it was usual to find "one-firm men"-people who started working in a company and retired 40 years later. Stocks exchange only measured economic performances of firms.

By the end of the 20th century, things started to change. Business environment became very turbulent and companies started to outsource, increasing the complexity of their supply chain. Information technology allowed people to be more and more aware of firm activities and nongovernmental organizations (NGOs) to send their messages. Customers became more and more demanding, because competition between firms was harder than ever. Employees wanted something more than a fair wage and indexes like the Dow Jones Sustainability or FTSEE4Good showed that firms which were quoted therein had better results and bore fewer risks than other firms. In such a situation, could a firm that was behind society survive?

Nowadays, the success of firms depends on several agents that interact with them. These agents are called stakeholders, and the way firms manage their relationships with them seems to have become a key point for profitability. Companies are now facing a paradoxical situation. Their economic power is perhaps stronger than ever, but at the same time, they have never been so vulnerable.

CSR could be defined as the set of obligations and lawful and ethical commitments with stakeholders, stemming from the impact of the activities and operations of firms on the social, labor, environmental and human rights fields. CSR implies the recognition and the integration in their operations by companies of social and environmental concerns (Valor et al., 2003, p.11). In other words, in addition to the economic criterion, it means including other criteria -social and environmental- in the management of firms and the way in which companies respond to society's demands.

Beyond those who defend that firms are only responsible to their shareholders and those who include in this responsibility other stakeholders, there is one irrefutable fact: more and more firms are developing policies in the field of CSR. Ninety percent of the firms of Fortune 500 have already set CSR strategies in motion (Kotler et al., 2004). A special article published in Business Week showed the investments of North American firms in this area (Berner, 2005): General Motors spent more than 5 million dollars in several CSR activities, General Mills invested more than 60 million dollars, and Merck used more than 11% of its profit before taxes for this same purpose. In 2006, the BBVA, a Spanish bank, announced its commitment to invest 0.7% of its profits obtained in South America to help the development of this area. Every day, one can read or see something similar about CSR and its introduction into the core business of firms. however, how does CSR affect firms' market value? If there is a positive relationship between CSR and market value, we could conclude that the classical theory of the firm and CSR are reconcilable.

CLASSICAL THEORY OF FIRMS AND THE OBJECTIVE OF PROFIT MAXIMIZATION

There are three basic institutions in a modern economic system: market, firms, and the State. The first one brings about the following ones. The inefficiencies of the market favor the appearance of firms and the need for the State to set the rules of the game.

According to economic theory, the balance between supply and demand in markets leads to an efficient resource assignation. using Adam Smith's famous idea about the "invisible hand," this balance should maximize market profit, also maximizing the benefit for society. Nevertheless, markets have shortcomings that make them imperfect. In these situations, the balance of markets does not ensure the benefit for all of society. Therefore, the State must participate in markets to guarantee improved efficiency, to set an efficient property rights system, and to supply those goods and services whose provision is not reliable, because of their general interest.

Firms are the replacement of agents in markets. According to Coase (1960), if property rights were perfectly defined, transaction costs were nil, and there was no wealth effect, then the mere operation of the market would suffice to reach an optimum resource assignment. In this hypothetical world, the balance of the market would benefit the entire society and firms would not be necessary. The existence of transaction costs and market imperfections have favored the appearance of companies.

These ideas about the imperfection of markets and the role of firms that participate in them are the main argument for classical theory supporters to state that the only objective for companies is to maximize their profits. A company that maximizes its profit in a perfect market is theoretically guaranteeing the maximization of wealth for society, which will positively affect all agents who are part of it.

The classical vision of firms has been arguing that CSR is practically incompatible with the classical principle of profit maximization. Milton Friedman (1970) even branded CSR as a "fundamentally subversive doctrine" in a free society, adding that

- There is one and only one social responsibility of business-to use it resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.

In other words, for Milton Friedman and his supporters, the only responsibility for businesses is to their shareholders. Companies are not required to carry out any social activity because this kind of actions concern the State and-if society wishes-other social groups (like NGOs) created by it. Friedman only justified social responsibility in one instance- when companies could benefit by some social issue that made them more profitable by paying less tax, obtaining better access to resources, or something similar.

There are several criticisms of the argument about the only objective being profit maximization wielded by neoclassical authors. One of the most obvious is related to the growing complexity of current firms, business environments, and society. Hierarchical organizations were useful for a long time when business environments were stable, economies were constantly growing, and technology changes were foreseeable. In that situation, companies only had to focus on production, because all the rest was under their control.

As mentioned, nowadays firms face a truly different business environment. The 21st century has arrived with a new paradigm. A network economy in which thousand of firms take part, with knowledge as their main asset (Drucker, 1993), has replaced hierarchical organizations. Within this network economy, hierarchy and power have been replaced by relational government mechanisms (Achrol et al., 1999). A few decades ago, for example, Ford even had a farm with a flock of sheep to obtain the wool for its car seats; nowadays Nike has some products on the market, which were not even manufactured by this American company. Network economy has made the success of organizations more difficult because businesses are related to several companies and agents along their value chain, and must deal with competition, which is harder than ever. All these agents, called stakeholders, influence the results of firms, and it is difficult to refer to profit maximization without considering this. In such a situation, can a firm maximize its profit if it is only managed to meet shareholders' interests?

The 21st century has arrived not only with a new business organization paradigm, but also with the way that firms compete. This has gone from a local to a global market with all the consequences. Consumers have more from which to choose and, thanks to information technology, more information to do so properly, and companies adapt constantly to competitive environments that change increasingly faster. The pressure for profit maximization is so strong that some firms even frequently forget the premises pointed out by Milton Friedman-respect for the law and ethics.

This global market and profit pressure have often resulted in the attitude of "anything goes" in the name of profit maximization, with terrible global consequences. The increasing outsourcing of the value chain in developing countries has too often been translated into lack of respect for both workers and human rights. The result is an economic model not linked to human development, although we had our highest economic growth period in the last decades. Strangely, this economic growth period collapsed because of the world scandal of "subprime mortgages" and all related titles, which were swept away by the most important financial institutions of the world. This has made world economies go into recession, which has been translated into an increasing number of unemployed people and thousand of shareholders poorer than before.

Society has also changed. Internet has allowed people to be more aware of everything that occurs, and has opened new alternative communication channels to those used in the past. This has allowed NGOs and diverse lobbies to reach more people with their published denunciations. Therefore, firms are more than ever exposed to reputational risks, and this can affect their market value. Legitimacy and morals play an important role in competition. Companies must assume their responsibility to their shareholders and customers, but also to their workers, suppliers, environment, competitors, and society. These stakeholders must somehow be considered in decision processes at some management level. Only with this focus, organizations can survive at long-term scenario-by their good reputation, the confidence of the market, and, in short, achieving the legitimacy to act, granted by the entire society (Valor and Merino, 2005).

All these arguments make it unfeasible for an economic system to collect and internalize all the agents' possible decisions and so, it cannot be stated that share value maximization, in itself, guarantees the efficiency of the system, and is justified as the only and fundamental principle to apply in firm management.

Another criticism of the notion that the only objective is profit maximization is the imperfection of markets. Markets are far from perfection and they often present externalities. When there are externalities, the balances of the market do not maximize the overall benefit for the entire society.

Nowadays, we are witnessing an intense debate about the participation of governments in economy because of the 2008 crack. Important economists, like Milton Friedman or Keynes, have played a leading role in this debate for decades. The first one defending that States just have to ensure the improvement of market efficiency and let firms compete freely in it, and the latter arguing that governments should take part in markets to solve these externalities.

Milton Friedman's ideas accelerated the liberalization process that took place during the seventies in western countries' economies. The general assumption is that all these policies aimed to increase the presence of market rules in economy have resulted in an improvement of society welfare, but the data now cast a shadow on this. According to Krugman (2008), Amiricans' real income grew much more from 1947 to 1976 (with protectionist governments) than from 1976 to 2005 (with liberalization rules). Moreover, the difference between rich countries and poor ones is greater than ever. This has occurred when firms are stronger and more powerful than ever before. According to the "invisible hand," this should have benefited all the societies in a global economy, not only the rich ones. This is because, as Philips et al. (2003) explain, market theory does not say anything about how to distribute the wealth that profit maximization creates. In addition, information is also imperfect and not available to all agents, which also prevents them to reach the optimum.

Markets are imperfect and, although States take part in them, in a globalized economy like ours, externalities exist and are worldwide. This prevents profitability from being the only indicator of organizations' efficiency (Argandoña 1995). We would need a wealth measure of adequate productivity and an overall measure of the impact of the long-term resources involved to determine the impacto of firms' profits on society.

The last criticism relates to the separation between property and firm management. The complexity of modern companies has resulted in an atomization of shareholders and the consistent separation between ownership and companies' management. The exorbitant growth of firms in the last decades and the growing globalization of economy have favored the emergence of a professionalized ruling class that governs the destiny of organizations without being the owners of them. Although firms hired these managers to defend owners' interests, they also have their own interests, which can come into conflict with those of the shareholders. Owners used to offer an incentive to align managers' interests with their own, falling into "Agency Costs", which prevented shareholders from achieving profit maximization in a strict sense.

The classical model, then, presents several limitations that relegate it to a utopian framework. If we add the growing importance of stakeholders for firms' management because of network economy and changes in society, we could conclude that we are facing a change of paradigm. The debate about CSR has increased during last decades. Some authors refer to firms' attitudes towards society (navas et al., 1998), others refer to companies' measures to protect society (Certo et al., 1996), and-as mentioned- de la Cuesta et al. (2003) talk about commitments. Beyond the different conceptual meanings, all these authors acknowledge that firms are responsible to society, and CSR seems much more than a new fashion. The question is whether this new paradigm means a cost for firms or just a new way to compete, which can benefit all of society, and thereby, shareholders also. If we could prove this, then CSR and the classical theory of firms would be reconcilable.

CORPORATE SOCIAL RESPONSIBILITY (CSR)

As mentioned above, CSR could be defined as the set of obligations and lawful and ethical commitments with stakeholders, stemming from impacts of activities and operations of firms cause on social, labor, environmental and human rights fields, CSR implies the companies' acknowledgement and integration of social and environmental concerns in their operations (Valor et al., 2003, p. 11). CSR is a relative concept that depends on stakeholders' socials demands and we must not confuse it with ethics.

To find the origin of CSR, we must refer to the stakeholders' theory (ST). The first meaning of stakeholders was proposed at the Stanford Institute, where, in 1963, they were defined as the groups without whose support firms would cease to exist. In 1984, ST achieved its current relevance. In that year, Edward Freeman published Strategic Management: a Stakeholder Approach, in which the growing concern about a better key stakeholder relationship management was expressed.

The main idea that supports ST is based on the existence of other groups besides shareholders that have a stake in firms' activity and their outcome. The claims and objectives demanded by different groups must be considered in a balanced way, permitting managers to increase the efficiency of the organization by responding to external requests (Freeman et al., 1990).

Above all, ST is a management theory, and explicitly ethical. This means that morals and values should be a core part of the firms' management, but always acknowledging that any management theory must fulfill the main objective, which is the subsistence of organizations. For ST to pay attention to shareholders' interests and well-being is compulsory beyond the instrumental and prudential concern of the maximization of share value. ST does not deny the objective of profit maximization as a necessary condition for firms to meet other goals, but this should not be an obstacle to consider aims other tha shareholder's goals.

Stakeholder relationship management is not an easy issue. First, because stakeholders' importance depends on the context of every relationship and industry; second, because stakeholders' relevance may vary over time for each company, but above all, because stakeholders' interests can come into conflict. For example, workers want better wages; customers want lower prices; and shareholders want more profitability. Managers must balance all these interests to maximize firms' value. ST does not propose managing all stakeholders in the same way, but prioritizing them according to their importance and impact on firms. Stakeholders are groups with something in common: their relationship with firms. All of them contribute, voluntarily or involuntarily, to companies' capacity to create wealth and activities; they are the potential beneficiaries and the ones who bear the risks. As firms have limited resources, the determination of stakeholders' importance to achieve strategic goals is a key issue to company management.

Several authors criticize ST, arguing that this theory has paid little attention to shareholders' interests (Heath et al., 2004). Although Hill et al. (1992), Boatright (1994), and Philips et al. (2003) justified the inclusion of stockholders among the rest of the stakeholders, defending that all of them share the same interests and are affected by the success or failure of companies, it cannot be denied that shareholders have special features because they are the owners of firms. Precisely these characteristics are usually recognized by law and by the articles of association of many organizations.

The question is to know whether there is a positive correlation between stakeholder relationship management and shareholders' wealth. ST and CSR are two theories that go together. CSR implies the assumption of ST, but it goes beyond this because it refers not only to ethics in stakeholder relationship management, but also to commitments with these groups.

According to theorists, there are four main justifications for CSR-the moral case, the social case, the economy case and the business case (de la Cuesta, 2004).

The moral case is wielded by those who claim not only the staff's individual ethics, but also that each organization is a body with its own social, economic, and environmental responsibility (de la Cuesta, 2004). These authors assign the same responsibilities to organizations that are demanded from any person, from the three above-mentioned points of view, demanding that firms develop a social and economic model in which collective interest takes priority over the individual one.

The moral case does not analyze the hypothetical profits of CSR for the firms that engage in these kinds of activities, but it points out that some practices, such as child labor, human rights violations, or wasting raw materials are neither moral nor ethic and should be rejected, independently of company profits.

Authors who support that CSR is good for all of society and that the goodwill and voluntarism of firms is insufficient for its development wield the social case. For these authors, governments should promote CSR through legislation.

Supporters of voluntarism argue that CSR means the way firms respond to society's requests and, therefore, society itself should resolve the debate through the public representatives, people's buying decisions, or just as members of social organizations or unions, as employees or as investors, for example. According to voluntarism supporters, the market will press to punish irresponsible firms and to reward CSR companies. However, de la Cuesta (2004) points out that this statement is somewhat fragile:

Firstly, market mechanisms need to deal properly with the existence of perfect information available to all agents to make decisions. There is not enough information about CSR policies, strategies, and results, and, in general, the information offered by firms is usually neither comprehensive nor thorough. Sometimes, it is not even provided regularly. Nowadays, there are many business codes of conduct and standards promoted by diverse public and private institutions that are creating confusion about what CSR is and how to compare it in different firms. The information provided by firms to society must be homogenized in order to verigy it and to perceive firms' positive or negative impact. Just as there are international and national accounting laws, the same should hold for CSR.

Secondly, there is a lack of incentives for firms to incorporate CSR criteria in management. Voluntarism supporters argue that no incentive should be given to firms to promote CSR, but Governments usually give an incentive for Research and Development (R&D), which is as voluntary as CSR. Moreover, both CSR and R&D are assumed good for industries, firms, and society. If R&D is fiscally subsidized, so should CSR.

The last argument for the social case is the common good. There are no more clearly public properties than society and environment. It would be incoherent for the State to dispense with its function of control over the impact of firms beyond these properties. Korten (1996) states that there are several socially responsible managers, but the problem is that they are facing a predatory system which makes their survival difficult. This creates a great dilemma for these managers because they have to choose between changing their viewpoint and running the risk of being expelled from the system, at least at short-term. De la Cuesta (2004) asks for a legal framework to mitigate these effects.

Authors who state that CSR affects both national and world economies brandish the economy case. The increasing international diversification of investment portfolios makes some authors (Monks et al., 1996) consider shareholders universal owners who should be concerned not only with the result of their portfolios one by one, but also with the result of world economy. From this point of view, shareholders would suffer economies' inefficencies and would benefit from improvements in this area.

In economic theory, negative externalities reduce the cost of the firms that generate them, transferring the cost to other companies or citizens. As the overall cost of these externalities is greater than the profits achieved by the firm causing them, universal investors, as the owners of these other companies, end up bearing such costs, obtaining a net loss (de la Cuesta, 2004). If we want to see this entire theory in practice, we just have to observe what has happened during 2008 in the most important stock exchange markets of the world. Subprime mortgages started in the USA but the globalization of economy fostered the infection with toxic assets of international economies. The net loss pointed out by de la Cuesta was not only for Americans, but also for savers and shareholders from almost everywhere. The consequences are well known. Huge rescue plans to avoid bankruptcy of all our entire financial system, enormous increases of public spending to help families and companies, an increasing number of unemployed (see table 1), and most important, an incredible economic recession.

However, there are more arguments that hold in the economy case. The above-mentioned global economy that our society is facing has several implications that should be taken into account. If the value chain of most firms is externalized in several countries, then social and environmental impacts are global and will affect the whole planet. There are, in addition, causes such as global warming or the scarcity of resources that can damage all societies wherever they are. Even more, health, education and the development of working-class people's rights have benefited our wellbeing society, our quality of life, and the improvement of our productive system. The industrial revolution made western coutries' way of living both socially and economically sustainable because economic development was bound to human development. History is full of examples of societies that collapsed because of the inexistence of a middle class and huge differences between higher and lower classes. Nowadays, there is little evidence that our globalization is linked to an improvement of human standard of living in poor countries. If our system is not socially sustainable, our economic system will not be feasible. Firms play an important role in this area. Moreover, they would benefit in a long-term scenario by this improvement of human standard of living and world economies.

CSR and business case

Under the theory of business case can be found all the ideas that affirm that CSR is good for shareholders and for other stakeholders also, and even for society (de la Cuesta, 2004). This focus is based on the existence of several (real and potential) links between a quality stakeholder relationship management and firm's profiability (de la Cuesta, 2005).

Some of these links are more or less obvious. For example, eco-efficiencies are improvements related to a better management of resources due to CSR.

Authors like Porter et al. (1995) defend this idea. If firms can produce the same quantity of goods using fewer resources, companies would be saving lots of money. This might be translated into a lower price per customer or even into higher profitability for firms. "First-mover advantage" is another argument for the business case. It is related to the belief that the firms that go beyond their legal obligations will benefit in a long-term scenario because they will occupy a privileged position when diverse pressing issues will be regulated. Eco-efficiencies and first-mover advantage are mainly philosophical arguments. How do they affect firms' market value? Is there any relationship beween CSR and firm's market value?

Empirical data are not conclusive, at least until now. Some authors support the positive link between CSR and firm's market value. Simpson et al. (2002) and Griffin et al. (1997) related CSR to an increase of companies' economic value; Moore (2001) and Orlitzky et al. (2001) related CSR to the reduction of organizational risks; Backhaus et al. (2002), Turban et al. (1997) related CSR to the potential of attracting and keeping employees. Maignan et al. (1999) and Brown et al. (1997) related CSR to an improvement of both corporate image and reputation; Luo et al. (2006) related CSR to market value through customer satisfaction.

However, authors like Omran et al. (2002), Mc Williams et al. (2000), Aupperle et al. (1985), or López et al. (2007) who not only have not found a positive relationship between CSR and firm's market value, but -in some cases- have found a negative one.

This can be explained by two important biases. Firstly, because most investigations that have found negative relationships have attempted to link CSR investments with account statements, which implies a retrospective focus because accounting is a result of past performances. Secondly, CSR is, perhaps, too new to be measured by accounting. Other arguments cast doubt on the appropriateness of using this kind of measurements. CSR is related to environmental and social improvements that can affect global economies, which are not reflected in a balance sheet or in an income statement.

Upon observing what happened during 2008 in the most important stock exchanges of the world, several pieces of evidence of a positive relationship between CSR and market value can be found. Managers of firms such as Lehman Brothers, Merrill Lynch, Fannie Mae, or Freddie Mac, for example, or even several banks among the top ten in the world, seeking short-term profitability without wondering whether it was sustainable, have caused huge losses to thousand of shareholders of the entire world. Perhaps because most practitioners of CSR have forgotten that sustainability also includes an economic perspective, not only social or environmental causes. Even more, CSR implies introducing ethical criteria in companies' management, and also transparency and accountability, precisely the words most coined by politicians in Washington in November 2008. All of this was done in the name of maximizing profits and shareholders' wealth. Where are their profits? Has society benefited, as was assumed in the extrapolation of Adam Smith's ideas carried out by new classical theorists?

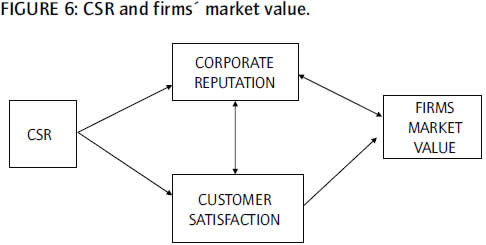

Throughout the literature review, one can find several ways in which CSR can also affect market value. This relationship is not direct, but through other variables such as corporate reputation and customer satisfaction, which affects several stakeholders.

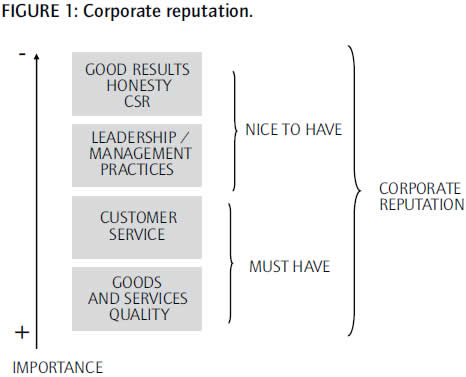

Kantya Consultancy found, with its tool RepTrack, that CSR is a driver of corporate reputation. CSR is considered by RepTrack "nice to have", and other characteristics such as service or quality are considered something that firms "must have" in order to be considered a "Renowned Company," but this result is consistent with the findings of the Foro de Reputación Corporativa in Spain, Maignan et al. (1999) and Brown et al. (1997), which suggest that CSR influences on corporate reputation.

Corporate reputation is based on perceptions, and CSR grants firms a kind of "goodwill reservoir" (Bhattacharya et al., 2004), which could minimize reputational risks and any impact derived from a scandal. Stock market traded firms, for example, are easily damaged by this kind of news. Reputation is based on perceptions, and the way firms are valued is often related to the way companies are seen by different agents who take part in a market. Both good and bad news configure the evaluative context in which organizations are perceived and valued.

CSR strategy might also influence corporate reputation by introducing ethical criteria for management may allow firms to quote in ethical stock indexes or to reduce the chances of incidents along their value chain. Both situations also favor corporate reputation.

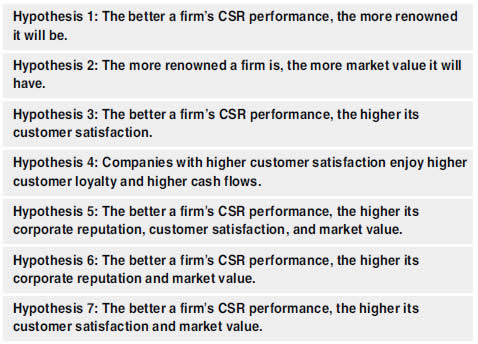

Hypothesis 1: The better the CSR performance is, the more renowned a firm will be (figure 1).

Reputation influence on firms' market value

Several firms, seeking improvements in their corporate reputation, decide to take part in Sustainability or Ethics Indexes such as Dow Jones Sustainability or FTSEE4Good. More and more investors look on CSR as a proper way to manage reputational, corporate governance, and social and environmental risks (de la Cuesta, 2004), and want to invest their capital in these kind of companies. These investors move increasingly large amounts of money that is very appealing to firms and that would not be achievable for organizations if they were not in these indexes.

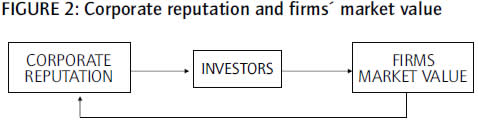

Corporate reputation has an impact on investors' portfolios. Brickley et al. (2002) showed that stock exchange markets are able to value intangible assets such as corporate reputation, influencing investors to invest in one company or another. The higher the demand, the higher the shares' stock value. This increases the overall value of the firm and benefits the shareholders.

As mentioned, corporate reputation is based on perceptions. The incredible bursting of the Spanish real estate bubble have caused all Spanish companies directly or indirectly related to the building industry not only to quote lower than past years in stock markets, but also to obtain a worse score in corporate reputations ranking, according to MERCO 2009. These circumstances do not seem fortuitous. The way firms are perceived influences their market value. Nowadays, who would invest in firms related to real estate industries?

Hypothesis 2: The more renowned a firm is, the more market value it will have (figure 2).

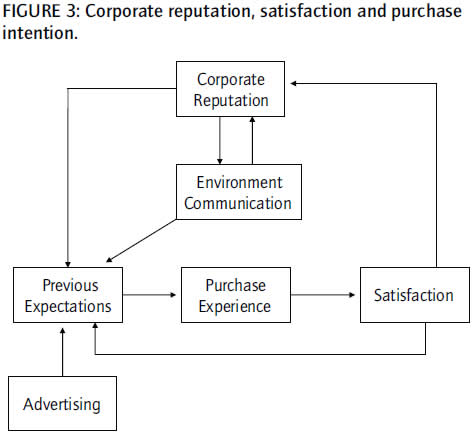

Corporate Reputation also affects customer purchase intention and customer satisfaction through previous expectations. Quality and service are, according to RepTrack, drivers of corporate reputation. Both characteristics are important for customer purchase intention and even for customer satisfaction.

Customer satisfaction depends on the overall evaluation of the buying and consuming experience made by consumers over time (Anderson et al., 2004; Fornell, 1992). In this overall evaluation, a contrast between previous expectations and the result obtained after enjoying the service or product takes place. A previous standard of experience and its confirmation determine satisfaction (Yi, 1990). When the result is at least as good as expected, or even better, then customers feel satisfied.

Santos et al. (2003) stated that previous expectations are a mixture of realistic evaluations and subjective beliefs. The former are usually based on the customer's own experiences; the latter are related to an emotional state. Advertising carried out by suppliers of services and products have an influence on these previous expectations, such as word of mouth, personal needs, and communications with the environment (Parasuraman et al., 1985). These previous expectations and all the variables that configure them are also related to customer purchase intention. The better corporate reputation is, the better previous expectations will be.[1]

CSR has an influence on customer satisfaction and customer purchase intention through corporate reputation. The actions that firms carry out attract the multidimensionality of the customer not only as an economic agent, but also as a member of a community, country, or family (Handelman et al., 1999). People are not only customers, but instead they take part in several stakeholder groups simultaneously, making their satisfaction with products and services more likely when supplied by a socially responsible firm than when supplied by another irresponsible one.

The CSR report may be a way to improve corporate reputation and stakeholders' perceptions. A good CSR report creates a positive context for customers' evaluations and their attitude towards the firm (Brown et al., 1997; Gürhan- Canli et al., 2004; Sen et al., 2001; Luo et al., 2006). Bhattacharya et al. (1995, 2003) insist on the key role that CSR can play for the construction of corporative image because it may lead customers to feel identified with a company, making them more likely to be satisfied with firms' offers. Moreover, people usually identify more with an organization when they perceive their identity as distinctive, and CSR is usually more distinctive than other strategies of the company.

Sen et al. (2001) found that CSR could improve product perceptions under some circumstances-quality, R&D, and price. The coherence between companies, their industry, and the cause supported are also valued. In the cases in which customers perceive that the efforts of firms to be socially responsible affect product quality, CSR may jeopardize corporate reputation. Customers try to understand why a firm is developing a CSR strategy. These attributions determine why customers may react positively or negatively to CSR activities. There are two main factors-corporate reputation and company motivation. In addition, customers usually appraise proactive firms better than reactive ones in CSR activities (Bhattacharya et al., 2004).[2]

Mithas et al. (2005) showed that customer knowledge of a firm affects their satisfaction. Sen et al. (2001) also showed that customers have a better knowledge about the companies that develop CSR initiatives. In 2004, both authors concluded that customers' knowledge of CSR activities is a key requirement for positive consumer reactions to these strategies.

Bhattacharya et al. (2004) stated that customers are an essential stakeholder group because they are especially sensitive to CSR initiatives. Market enquiries point to a positive relationship between company CSR strategies and customers' reaction to the firm and its products. The USA Corporate Citizens poll found that 84% of North American people were likely to switch to a brand associated with a social cause if price and quality were similar to another brand (Bhattacharya et al., 2004). Customers usually have a favorable attitude towards companies that develop CSR strategies. The more renowned a firm is, the better the customers' reaction will be (figure 3).

Brown (1998) and Brown et al. (1997) found that, direct or indirectly, CSR affects customers' responses even more than the product; Berens et al. (2005) found that CSR influences consumers' attitudes before the product does so.

However, CSR does not always have an influence on customer purchase intentions. Enquiries usually have a desirability bias, which makes the individuals who are polled respond with what they think is expected instead of giving their true opinion. Valor (2005) found that customers are likely to buy certain brands that support some causes but they are not willing to make tradeoffs for this purpose. CSR becomes again "nice to have". This can make a difference in some circumstances, but price, quality, and brand dominate purchase intentions (Valor, 2005). There is a positive link between CSR and consumer's purchase intention when customers' support of the main initiative into CSR strategy or when there is high coherence between firms and the cause they support, or when the product is high quality and when customers do not have to make tradeoffs.

Nonetheless, CSR can generate loyalty (Luo et al., 2006), resistance (goodwill reservoir (Bhattacharya et al., 2004), and a good word-of-mouth (Szymansky et al., 2001). All these aspects have an influence on previous expectations.

Bhattacharya et al. (2004) also showed that CSR strategies affect consumers' general sense of well-being. Awareness plays a key role for this because, sometimes, customers have no knowledge of firms' activity in this field. Attributions (causal reasoning when consumers try to understand CSR actions) may also benefit companies under some circumstances- reputation and the alignment of CSR activities and company purpose. Customers also usually have a more positive attitude towards firms that are engaged in CSR strategies (Bhattacharya et al., 2004) and usually identify with companies that support causes that concern their consumers.

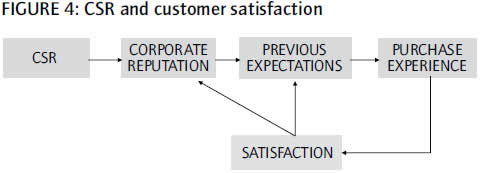

Several multiplier factors can increase the impact of CSR strategies on customers. These factors are marketing global strategy and CSR strategy within this one, the membership to irresponsible perceived industries, and company reputation. When firms distinguish themselves from their competitors through CSR activities, are pioneers or are engaged in several CSR actions, they usually are better perceived (Bhattacharya et al., 2004)(figure 4).

- Hypothesis 3: The better the firms' CSR performance, the higher customer satisfaction will be.

Customer Satisfaction has an influence on firms' market value

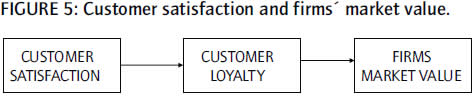

Anderson et al. (2004) argued that customer satisfaction affects firms' market value; Bolton et al. (1991) and Oliver (1980) found that the more satisfied the customers are, the more loyal they will be, and a more positive word-of-mouth will be passed on (Szymansky et al., 2001). Homburg et al. (2005) showed that the more satisfied the customers are, the more willing to pay premium prices they will be. All of these have an influence on firms' increasing market value. There is a broad consensus about the benefits and profits that a loyal customer implies for a company. However, Reinartz et al. (2002) question it, arguing that loyal customers usually expect something in return for their loyalty and are more sensitive to prices, because they are more familiar with the products they are buying (which allows them to establish solid benchmark prices and to value product quality), and usually believe they deserve better prices for their loyalty.

Gruca et al. (2005), Fornell (1992), and Mittal et al. (2005) concluded that the firms with higher satisfaction levels among their customers obtain higher cash flows, also ensuring less volatility on future cash flows (which leads companies to a higher market value) (Anderson et al., 2004; Srivastasa et al., 1998).

As already explained, previous experiences have an impact on expectations before purchasing, playing an important role in loyalty and overall satisfaction.

Hypothesis 4: Companies with higher customer satisfaction enjoy higher customer loyalty and higher cash flows (figure 5).

Influence of CSR on firms' market value through customer satisfaction and corporate reputation

Luo et al. (2006) showed that, under some circumstances, CSR might have a positive influence on firms' market value. These circumstances are quality and ability to innovate (corporative skills). When CSR is linked to corporative skills, firms are more likely to generate favorable attributions and customers' identification with that company. Both aspects will favor loyalty and other positive behaviors. When firms develop strong corporative skills that support CSR, they may win social contracts, institutional loyalty, moral legitimacy, and consumers' support (Handelmand et al., 1999).

Luo and Bhattacharya's are conclusive. The firms that are better perceived because of their CSR initiatives usually have higher customer satisfaction levels, which lead to a higher market value through loyalty, as several authors have shown .

There is only one drawback in the work of these authors. Fortune America's Most Admired Companies Ranking (FAMA) is a measure made up of managers and consumers' opinions, which are, then, perceptions. CSR should be a measure of performance, not of the way that consumers perceive firms. Nevertheless, it seems reasonable that the firms that manage to control all the impacts of their value chains will have more satisfied customers. As mentioned, customers usually have a favorable attitude towards the companies that develop CSR strategies. Moreover, Brown (1998) and Brown et al. (1997) found that, direct or indirectly, CSR affects customers' responses to a product. Berens et al. (2005) found that CSR influences consumers' attitudes towards a product.

Corporate reputation and customer satisfaction provide feedback for each other. As noted, corporate reputation participates in the generation of a customer's expectations before purchasing a product or service. These expectations, which will be compared with the result of the product or service, will be used also to measure the customer's overall satisfaction. Whether or not the customer is satisfied, the purchase experience will have an impact on corporate reputation because it will also affect the way the firm is perceived. Besides, according to with RepTrack, quality- one of the most important drivers of reputation-is also related to customer satisfaction, as a result of the difference between previous expectations and the purchase experience.

Hypothesis 5: The better the firms' CSR performance is, the higher the corporate reputation, customer satisfaction, and the firms' market value

Hypothesis 6: The better the firms' CSR performance is, the higher the corporate reputation, and the firms' market value.

Hypothesis 7: The better the firms' CSR performance, the higher the customer satisfaction and the firms' market value (figure 6).

THE FINAL MODEL

All the relationships that have been developed through literature review could be summarized in a single model that would be like this: (figure 7).

There is also one more proposal that has not been explained because of its obviousness. Loyalty of profitable customers is a driver of purchase intention and, thereby, of sales. The higher the sales, the better the accounting results and the higher the shareholder profitability will be. The higher the shareholder profitability and the better accounting results, the higher the firms' market value will be, which would make investing in these companies more appealing. That is why market value and investor choice have a bidirectional relationship, just like corporate reputation and customer satisfaction.

The following hypotheses would be proposed for this model:

CONCLUSIONS AND LIMITATIONS

CSR and the classical theory of firms could be reconcilable if the proposed model is fulfilled; CSR would lead to higher market value, which would be beneficial also for shareholders, allowing firms to carry out with their main objective, according to Friedman's ideas.

Independently of the results of our model, there are several clear relationships and facts, which should not be forgotten. During the last quarter of 2008 and the first quarter of 2009, we have witnessed with astonishment the fall of some of the biggest world companies. Some of them were saved from bankruptcy by governments but others were not, sweeping away thousand of stakeholders. In the end, whether or not the government intervened, millions of shareholders and all of society have lost. The managers of those firms were not doing anything illegal, but it was immoral.

The first lesson is that law is not sufficient to regulate companies' performance in such a complex world as ours. Managers must go even further to guarantee shareholders' objectives, guaranteeing the sustainability of the companies. The second lesson is that sustainability, from a triple point of view, is actually a keyword for firms' management. the strategies that are no sustainable from an economic, social, and environmental point of view are doomed to fail. The industries most harmed by this crash are those that were developed with the shortest-term vision. The third lesson shows us that the industries and companies that participated in the property bubble are also the ones that were damaged the most by this crisis. This means that the least socially responsible firms were also the least profitable for their shareholders during these last months. The last lesson is that, in a globalized world, economy impacts are also global. World financial markets are interconnected and this is why we are facing a global crisis. From this point of view, it cannot be said that when markets go well, the invisible hand makes all societies improve their standard of living, just some of them. Besides, when markets go wrong, the whole world standard of living worsens considerably. The crisis has not only affected shareholders, but also all stakeholders. In other words, our economic globalization is not linked to human development, and that makes it unsustainable.

We have, then, several arguments in support of the statement that the firms that act irresponsibly are less profitable, but what occurs with the firms that carry out their business properly?

We need to develop the model mathematically, but -in any case- governments and public institutions should help companies make customers aware of what is respectful towards the environment and society, and what is sustainable, also from an economic point of view. Even so, CSR is sometimes just a management tool, forgetting this first premise pointed out by Edward Freeman, and it is just used as a tool for the corporate image. This could cause the model to fail or, at least, lead us to misunderstand the results.

FOOTNOTES

[1] Parasuraman et al. (1985) and Gronröos (1997) defined perceived quality as the result of comparing the service or product received and the service or product hoped. This difference, linked to previous expectations, determines satisfaction.

[2] Fornell et al. (1996) state that perceived value is a precedent for customer satisfaction. Zeithaml (1988) define "perceived value" as the overall valuation of product utility by customers. It is based on perceptions and it is subjective and individual, varying among consumers and even among different moments in time. Perceived quality, perceived price or quality, and company reputation influenced the perceived value (Zeithaml, 1988).

REFERENCES

Abouzeid, K.M. & Weaver, C.N. (1978). Social responsibility in the corporate goal hierarchy. Business Horizons, 21(3), 29-35. [ Links ]

Achrol, R. S. & Kotler, P. (1999). Marketing in the Network Economy. Journal of Marketing, 63(4), 146-163. [ Links ]

Anderson, E. W., Fornell, C. & Mazvancheryl, S. K. (2004). Customer Satisfaction and Shareholder Value. Journal of Marketing, 64(4), 172-185. [ Links ]

Anderson, E. W., Fornell, C. & Lehmann, D. R. (1994). Customer satisfaction, market share and profitability: Findings from Sweden. Journal of Marketing, 58(3), 53-66. [ Links ]

Argandoña, A. (1995). La dimensión ética de las instituciones y los mercados financieros. Madrid: Fundación BBV. [ Links ]

Aupperle, K.E., Carroll, A.B. & Hatfield, J.D. (1985). An empirical examination of the relationship between corporate social responsibility and profitability. Academy of Management Journal, 28(2), 446-463. [ Links ]

Becker-Olsen, K. L., Cudmore, A. B. & Hill, R. P. (2006). The impact of perceived corporate social responsibility on consumer behaviour. Journal of Business Research, 59(1), 46-53. [ Links ]

Berens, G., Van Riel, C.B.M. & Van Bruggen, G.H. (2005). Corporate associations and consumer product responses: The moderating role of corporate brand dominance. Journal of Marketing, 69(3), 35-48. [ Links ]

Berner, R. (2005, November). Smarter corporate giving. Business-Week, 68-76. [ Links ]

Bhattacharya, C.B., Rao, H. & Glynn, M.A. (1995). Understanding the bond of identification: An investigation of its correlates among art museum. Journal of Marketing, 49(4), 46-57. [ Links ]

Bhattacharya, C.B. & Sen, S. (2003). Consumer-company identification: A framework for understanding consumer's relationships with companies. Journal of Marketing, 67(2), 78-88. [ Links ]

Bhattacharya, C.B. & Sen, S. (2004). Doing better at doing good: When, why and how consumers respond to corporate social initiatives. California Management Review, 47(1), 9-24. [ Links ]

Boatright, J. R. (1994). Fiduciary duties and the shareholder-management relation: Or what's so special about shareholders? Business Ethics Quarterly, 4(4), 393-407. [ Links ]

Bolton, R.N. & Drew, J.H. (1991). A multistage model of customers' assessments of service quality and value. Journal of Consumers Research, 17(4), 375-384. [ Links ]

Bolton, R. N. & Drew, J.H. (1991). A longitudinal analysis of the impact of service changes on customer attitudes. Journal of Marketing, 55(1), 1-9. [ Links ]

Brickley, J.A., Smith Jr., C.W. & Zimmerman, J.L. (2002). Business ethics and organizational architecture. Journal of Banking and Finance, 26(9), 1821-1835. [ Links ]

Brown, T.J. & Daci, P.A. (1997). The company and the product: Corporate associations and consumer product responses. Journal of Marketing, 61(1), 68-84. [ Links ]

Brown, T.J. (1998). Corporate associations in marketing: Antecedents and consequences. Corporate Reputation Review, 1(3), 215-233. [ Links ]

Certo, S.C. & Peter, J.P. (1996). Dirección estratégica. Madrid: Irwin. [ Links ]

Coase, R.H. (1960). The problem of social cost. Journal of Law and Economics, 3(1), 1-44. [ Links ]

de la Cuesta González, M. (2004). El porqué de la responsabilidad social corporativa. Boletín Económico del ICE, 2813, 45-58. [ Links ]

de la Cuesta González, M. (2005, October 18). La responsabilidad social corporativa o la responsabilidad social de la empresa. Jornadas de Economía Alternativa y Solidaria. Retrieved from www.hegoa.ehu.es./congreso/bilbo/doku/bat/responsabilidadsocialcorporativa.pdf [ Links ]

de la Cuesta González, M., Valor Martínez, C. & Keisler, I. (2003). Promoción institucional de la responsabilidad social corporativa: iniciativas internacionales y nacionales. Boletín Económico del ICE, 2779, 9-20. [ Links ]

de la Cuesta González, M. (2005). Las inversiones socialmente responsables como palanca de cambio económico y social. Revista Futuros, 11(3), 1-14. [ Links ]

Drucker, P. (1993). Post capitalist society. New York: Harper Collins Publishers. [ Links ]

Eberl, M. & Schwaiger, M. (2005). Corporate reputation: Disentangling the effects on financial performance. European Journal of Marketing, 39(7/8), 838-854. [ Links ]

Freeman, E.R. & Evan, W.M. (1990). Corporate governance: A stakeholder interpretation. Journal of Behavioural Economics, 19(4), 337-360. [ Links ]

Freeman, E.R. & Phillips, R.A. (1996). Efficiency, effectiveness and ethics: a stakeholder view. Human Action in Business, (65-81). Edison: Transaction Books. [ Links ]

FORÉTICA. (2004). Responsabilidad social de las empresas: Situación en España. Informe FORÉTICA. Retrieved from http://www.foretica.es/recursos/doc/Biblioteca/Informes/48383_263263200895842.pdf [ Links ]

FORÉTICA. (2006). Evolución de la Responsabilidad Social de las Empresas en España. Informe FORÉTICA. Retrieved from http://www.foretica.es/recursos/doc/Biblioteca/Informes/6983_263263200895924.pdf [ Links ]

Fornell, C. (1992). A national customer satisfaction barometer: The Swedish experience. Journal of Marketing, 56(1), 6-21. [ Links ]

Fornell, C., Johnson, M.D., Anderson, E.W., Cha, J. & Bryant, B. (1996). The American Customer Satisfaction Index: Description, findings, and implications. Journal of Marketing, 60(4), 7-18. [ Links ]

Freeman, E.R. (1984). Strategic management: A stakeholder approach. Boston: Pitman. [ Links ]

Freeman, E.R. (1999). Response divergent stakeholder theory. Academy of Management Review, 24(2), 233-236. [ Links ]

Freeman, E.R. & Evan, W.M. (1990). Corporate governance: A stakeholder interpretation. Journal of Behavioral Economics, 19(4), 237-255. [ Links ]

Friedman, M. (1970, September 13). The social responsibility of business is to increase its profits. The New York Times Magazine. Retrieved from http://www.colorado.edu/studentgroups/libertarians/issues/friedman-soc-resp-business.html [ Links ]

García de Madariaga, J. & Valor Martínez, C. (2004, September 24). Análisis de la implantación del modelo sostenible entre empresas españolas multinacionales. XVI encuentro de profesores universitarios de Marketing. Retrieved from http://www.epum2004.ua.es/aceptados/296.pdf [ Links ]

García de Madariaga, J. & Valor Martínez, C. (2007). Stakeholders management systems: Empirical insights from relationship marketing and market orientation perspectives. Journal of Business Ethics, 71(4), 425-439. [ Links ]

Griffin, J.J. & Mahon, J.F. (1997). The corporate social performance and financial performance debate: Twenty-five years of incomparable research. Business and Society, 36(1), 5-31. [ Links ]

Gronröos, C. (1997). Value-driven relational marketing: from products to resources and competencies. Journal of Marketing Management, 13(5), 407-419. [ Links ]

Gruca, Thomas S. & Rego, Lopo R. (2005). Customer satisfaction, cash flow and shareholder value. Journal of Marketing, 69(3), 115-130. [ Links ]

Günhar-Canli, R. & Batra, R. (2004). When corporate image affects product evaluations: The moderated role of perceived risk. Journal of Marketing Research, 41(2), 197-205. [ Links ]

Handelman, J.M. & Arnold, S. J. (1999). The role of marketing action with a social dimension: Appeals to institutional environment. Journal of Marketing, 63(3), 33-48. [ Links ]

Harrison, J. S. & Freeman, E. R. (1999). Stakeholders, social responsibility, and performance: empirical evidence and theoretical perspectives. Academy of Management Journal, 42(5), 479-485. [ Links ]

Heath, J. & Norman, W. (2004). Stakeholder theory, corporate governance and public management: What can the history of State-run enterprises teach us in the post-Enron era? Journal of Business Ethics, 53(3), 247-265. [ Links ]

Homburg, C., Koschate, N. & Hoyer, W. (2005). Do satisfied customers really pay more? A study of the relationship between customer satisfaction and willingness to pay. Journal of Marketing, 69(2), 84-97. [ Links ]

Intermon Oxfam. (2004, February). La moda que aprieta. Intermon Oxfam. Retrieved from www.intermonoxfam.org/UniandesInformacion/anexos/3001/0_3001_090204_Moda_que_aprieta.pdf [ Links ]

Intermon Oxfam (2006, May). ¡Fuera de juego! Derechos laborales y producción de ropa deportiva. Intermon Oxfam. Retrieved from http://www.intermonoxfam.org/unidadesinformacion/anexos/7535/060524_fuera_juego_ddll2.pdf [ Links ]

Intermon Oxfam (2006, September). Responsabilidad Social Corporativa: nuestra visión. Intermon Oxfam. Retrieved from http://www.intermonoxfam.org/unidadesinformacion/anexos/7913/061110_Documento_IO_OK.pdf [ Links ]

Kotler, P. & Lee, N. (2004). Corporate social responsibility: Doing the most good for your company and your cause. New York: John Wiley & [ Links ] Sons.

Korten, D. (1996). When companies rule the world. London: Earthscan. [ Links ]

Krugman, P. (2008). ¿Quién era Milton Friedman? Negocios, 1198, El País, October 19, pp. 10-16. [ Links ]

López, M., García, A. & Rodríguez, L. (2007). Sustainable development and corporate performance: A study based on the Dow Jones Sustainability Index. Journal of Business Ethics, 75(3), 285-300. [ Links ]

Luo, X. & Bhattacharya, C.B. (2006). Corporate social responsibility, customer market satisfaction, and market value. Journal of Marketing, 70(4), 1-18. [ Links ]

Maignan, I. & Ferrell, O.C. (2005). Corporate citizenship: Cultural antecedents and business benefits. Journal of the Academy Management Science, 27(4), 455-469. [ Links ]

Maignan, I., Ferrell, O.C. & Ferrell, L. (2005). A stakeholder model for implementing social responsibility in marketing. European Journal of Marketing, 39(9/10), 956-977. [ Links ]

McWilliams, A. & Siegel, D. (2000). Corporate social responsibility and financial performance: Correlation or misspecification? Strategic Management Journal, 21(5), 603-609. [ Links ]

Méndez Picazo, M.T. (2005). Ética y responsabilidad social corporativa. Ética y Economía, ICE, 823, 141-150. [ Links ]

Mithas, S., Krishnan, M.S. & Fornell, C. (2005). Why do customer relationship management applications affect customer satisfaction? Journal of Marketing, 69(4), 201-209. [ Links ]

Monitor Empresarial de Reputación Corporativa (MERCO) (2009). MERCO 2009. Retrieved from http://www.merco.info/es [ Links ]

Mittal, V., Anderson, E.W., Sayrak, A. & Tadikamalla, P. (2005). Dual emphasis and the long term financial impact of customer satisfaction. Marketing Science, 24(4), 544-555. [ Links ]

Monks, R. & Minow, N. (1996). Watching the watchers: Corporate governance in the 21st Century. Cambridge: Blackwell. [ Links ]

Moore, G. (2001). Corporate social and financial performance: An investigation in the U.K. Supermarket Industry. Journal of Business Ethics, 34(3/4), 299-315. [ Links ]

Navas López, J.E. & Guerras Martín, L.A. (1998). La dirección estratégica de la empresa: teoría y aplicaciones. Madrid: Civitas. [ Links ]

Oliver, R.L. (1980). A cognitive model of the antecedents and consequences of satisfaction decisions. Journal of Marketing Research, 17(4), 460-469. [ Links ]

Omram, M., Atrill, P. & Pointon, J. (2002). Shareholders versus stakeholders: corporate mission, statements and investor returns. Business Ethics: A European Review, 11(4), 318-326. [ Links ]

Orlitzky, M. & Benjamin, J.D. (2001). Corporate social performance and firm risk: A meta-analytic review. Business and Society, 40(4), 369-396. [ Links ]

Parasuraman, A., Zeithaml, V. & Berry, L.L. (1985). A conceptual model of service quality and its implication for future research. Journal of Marketing, 49(4), 41-50. [ Links ]

Philips, R., Freeman, E.R. & Wicks, A.C. (2003). What stakeholder theory is not. Business Ethics Quarterly, 13(4), 479-502. [ Links ]

Porter, M.E. & Van der Linde, C. (1995). Green and competitive: Ending the stalemate. Harvard Business Review, 73(5), 120-134. [ Links ]

Porter, M.E. & Kramer, M. (2002). The competitive advantage of corporate philanthropy. Harvard Business Review, 80(12), 57-68. [ Links ]

Raavald, A. & Gronröos, C. (1996). The value concept and relationship marketing. European Journal of Marketing, 30(2), 19-30. [ Links ]

Reinartz, W. & Kumar, V. (2002). The mismanagement of customer loyalty. Harvard Business Review, 80(7), 86-94. [ Links ]

Reynolds, S.J., Schultz, F.C. & Hekman, D.R. (2006). Stakeholder theory and managerial decision-making: Constraints and implications of balancing stakeholder interests. Journal of Business Ethics, 64(3), 285-301. [ Links ]

Roddick, A. (1992). Cuerpo y alma. Barcelona: Ediciones B. [ Links ]

Santos, J. & Boote, J. (2003). A theoretical exploration and model of consumer expectations, post purchase affective states and affective behaviour. Journal of Consumer Behaviour, 3(2), 142-156. [ Links ]

Sen, S. & Bhattacharya, C.B. (2001). Does doing good always lead to doing better? Journal of Marketing Research, 38(2), 225-243. [ Links ]

Simpson, W. G. & Kohers, T. (2002). The link between corporate social responsibility and financial performance: Evidence from the banking industry. Journal of Business Ethics, 35(2), 97-109. [ Links ]

Srivastava, R., Shervani, T. & Fahey, L. (1998). Market-based assets and shareholder value: A framework for analysis. Journal of Marketing, 62(1), 2-18. [ Links ]

Suchman, M.C. (2005). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review, 20(3), 571- 610. [ Links ]

Szymansky, D.M. and David, H. (2001). Customer satisfaction: A metaanalysis of the empirical evidence. Journal of the Academy of Marketing Science, 29(Winter), 16-35. [ Links ]

Turban, D.B. & Greening, D.W. (1997). Corporate social performance and organizational attractiveness to prospective employees. Academy of Management Journal, 40(3), 658-672. [ Links ]

Valor Martínez, C. & Merino de Diego, A. (2005, November). La relación ONG-empresa en el marco de la responsabilidad social de la empresa. Centro de Estudios de Cooperación al Desarrollo (CECOD). Retrieved from http://www.cecod.net/Informe%20ONG-Empresas.pdf [ Links ]

Valor Martínez, C. (2005). Consumers' responses to corporate philanthropy: Are they willing to make trade-offs? International Journal of Business and Society, 6(1), 1-26. [ Links ]

Valor Martínez, C. & Palomo Zurdo, R. (2003). Inversiones socialmente responsables: coherencia con la doctrina social de la Iglesia. Desafíos Globales: La doctrina social de la Iglesia hoy, 1, 775-788. [ Links ]

Valor Martínez, C. (2001). El contexto: de la responsabilidad social al marketing de relaciones. Papeles de ética, economía y dirección, 6, 4-16. [ Links ]

Valor Martínez, C. (2006). What if all trade was fair trade? The potential of a social clause to achieve the goals of fair trade. Journal of Strategic Marketing, 14(3), 263-275. [ Links ]

Valor Martínez, C. (2006). Cláusulas sociales: análisis de la afinidad de objetivos con el movimiento por el comercio justo. Boletín Económico del ICE, 2882, 39-53. [ Links ]

Valor Martínez, C. & de la Cuesta González, M. (2003). Responsabilidad social de la empresa: concepto, medición y desarrollo en España. Boletín Económico del ICE, 2755, 7-20. [ Links ]

Varadarajan, R.P. & Menon, A. (1988). Cause-related marketing: A coalignment of marketing strategy and corporate philanthropy. Journal of Marketing, 52(3), 58-74. [ Links ]

Yi, Y. (1990). Cognitive and affective priming effects of the contexts for print advertisements. Journal of Advertising, 19(2), 40-48. [ Links ]

Zeithaml, V. (1988). Consumer perceptions of price, quality, and value: A means-end model and synthesis of evidence. Journal of Marketing, 52(3), 2-22. [ Links ]