Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkColombia Internacional

Print version ISSN 0121-5612

colomb.int. no.75 Bogotá Jan./June 2012

El dilema chino: estrategias de desarrollo económico emprendidas por Estados pequeños en Sudamérica

Carol Wise

PhD, es profesora asociada de Relaciones Internacionales en la University of Southern California

RESUMEN

Las tres tendencias predominantes en América del Sur en la década del 2000 han sido 1) la rápida expansión del comercio y los lazos de endeudamiento con China; 2) el colapso de escenarios de negociación comerciales multilaterales y regionales desde el 2006; y 3) la rápida recuperación de la mayoría de los países suramericanos de la crisis financiera global de 2008-2010. Este artículo analiza las formas en las que estas tres tendencias han convergido, y de qué manera han condicionado la escogencia de estrategias de desarrollo en Chile y Perú, quienes tienen los lazos comerciales más importantes con China de toda la región latinoamericana, medidos como porcentaje de su PIB. En efecto, ambos países han buscado forjar sus propios caminos negociando tratados de libre comercio (TLC) bilaterales con China y Estados Unidos. Sin embargo, las implicaciones políticas de estos caminos de desarrollo han resultado más complejas de lo que se esperaba, a pesar de que estas políticas comerciales pueden representar el mecanismo de avance más viable para países con economías pequeñas, mercados emergentes y que han consolidado sus reformas macroeconómicas preparándolos para llevar su estrategia económica al siguiente nivel.

PALABRAS CLAVE

Tratados de Libre Comercio bilaterales • Comercio América Latina y China • Tratados comerciales en Perú y Chile • Tratados de Libre Comercio de EEUU

The China Conundrum: Economic Development Strategies Embraced by Small States in South America1

ABSTRACT

The three most prominent trends in South America in the 2000s have been: 1) the rapid expansion of trade and borrowing ties with China; 2) the collapse of both regional and multilateral trade negotiating venues since 2006; and, 3) the quick recovery of most South American countries from the 2008-10 global financial crisis. This paper analyzes the ways in which these three trends have converged and shaped the choice of development strategy in Chile and Peru, which have the strongest trade ties with China in the entire Latin American region when measured as a percent of GDP. Indeed, both countries have sought to stake out their own paths by negotiating separate bilateral free trade agreements (FTAs) with China and the US. Yet, although making these respective policy choices may well represent the most viable way forward for small emerging market countries which have consolidated macroeconomic reforms and are prepared to take their economic strategy to the next level, the political implications of this development path have already become more complicated than expected.

KEYWORDS

Bilateral Free Trade Agreements • Chinese Latin American trade • Peru and Chile trade agreements • US Free Trade Agreements

Digital Object Identification

http://dx.doi.org/10.7440/colombint75.2012.05

INTRODUCTION

Some thirty years in the making, the phenomenon of China's relatively rapid rise in the international political economy has elicited far more questions than it has answers. The data, for the most part, are unambiguous. Be it China's historically unprecedented growth rate over the past three decades, its amassment of the world's highest level of foreign exchange reserves, or its recent emergence as the largest holder of US Treasury securities, there is little doubt as to the dazzling economic prominence that this country has now attained (Subramanian 2011). However, while these economic advances may seem beyond dispute, any consensual interpretation of the mid- and long-term implications of this structural shift in the global economy remains elusive. This is especially so for Latin America, given its geographic proximity to the US and the longstanding designation of the Western Hemisphere as part of the US "sphere of influence".

Although China's participation in the region is still largely a matter of its rapidly growing trade and lending ties with any number of Latin American countries, the sheer magnitude of these ties has thrown the US presence into relief. For example, since 2000 China has become the first or second most important trading partner for Argentina, Brazil, Chile, Costa Rica and Peru (Barcena and Rosales 2010, 16); moreover, between 2003 and 2011 Chinese foreign direct investment (FDI) in Latin America totaled close to $23 billion, up from basically nothing at the outset of the 2000s. Not only has Chinese demand for South America's natural resources been a motor for high growth in this sub-region in the 2000s, it was this continued demand that at least partially accounted for Latin America's quick rebound from the 2008-10 global financial crisis (Porzecanski 2009; Barcena and Rosales 2010, 9-10). In the wake of this crisis, China has become the second largest economy in the world, after the US, and it has provided the stimulus for global growth as the "Great Recession" in the OECD bloc continues to linger.

A closer examination of the participation of both the US and China in Latin America suggests an emerging division of labor: for better or for worse, the US will continue to promote democracy, market reforms, and rule of law in the region, while China will do the heavy lifting with trade expansion, infrastructure investment, and a range of other development projects. Ever mindful of this being the US sphere of influence (Shixue 2008), and of its own dependence on investing in and exporting to the US market (Lanxin 2008), China has moved cautiously in the Western Hemisphere and its mission in Latin America has largely been developmental in nature (Yang 2009). Still, China is hardly operating under the radar screen. For example, China has now become the major source of demand for soya beans from Argentina and Uruguay, iron ore and soya beans from Brazil, copper and livestock feed from Chile and Peru, and crude oil from Colombia and Ecuador (Barcena and Rosales 2010, 19). Not only has this prompted the longest resource boom and foreign exchange bonanza ever for some countries in the region, the multiplier effects in terms of Chinese development assistance, infrastructure support, and others forms of lending and investment have been an additional windfall.

For large states like Argentina and Brazil, the pattern has been to export raw materials to China and manufactured exports to the region and the rest of the world, except China. For small open economies like Chile and Peru, where the size of the non-resource based manufacturing sector is minor, this is less of an option. In both of these cases the stated goal has been to diversify raw material exports to the region and the rest of the world and to modernize the domestic service sector into a Pacific Rim hub for transport, finance, investment, and all logistics related to trade. Herein lies the decision of both Chile and Peru to negotiate separate bilateral free trade agreements (FTAs) with the US and China. Chile was the first to accomplish this dual feat, with the implementation of the Chile-US FTA in 2004 and the ChileChina FTA in 2006, and Peru followed suit in implementing separate FTAs with the US and China in 2009.

When the Chile-US and Peru-US FTAs are examined, both emerge as highly sophisticated post-industrial accords which reflect the eagerness of US investors in services (e.g. banking, finance, telecom, pharmaceuticals, insurance) to further imprint US regulatory standards and investment codes on the economic structures of these partners. In short, although US producers were anxious to obtain tariff reductions for agricultural and manufactured exports to Chile and Peru, at heart these US agreements pertain mainly to the new trade agenda (the liberalization of services, investment, and intellectual property rights). In essence, and as services and investment have become increasingly interwoven, these two US FTAs have been geared toward the efforts of both Chile and Peru to transform their respective service sectors into competitive Pacific Rim hubs. On the US side, as the relationship between services and investment has become increasingly interwoven (Kotschwar 2009), this has spawned a North-South FTA pattern whereby "[...] concentrated interests in FDI-exporting countries have a strong incentive to lobby for preferential agreements because they confer specific advantages over competitors" (Manger 2009, 19).

In contrast, for both countries the FTA with China centers primarily on the old trade agenda (market access for agriculture and other raw materials, textiles, and labor-intensive manufactured goods), and in particular China's resource-based demands for steady access to raw material imports from both nations (Wise and Quiliconi 2007). Thus, the Chile-China and Peru-China FTAs hark back to the trade patterns which characterized the turn of the last century, whereby old-fashioned comparative advantage fueled the export of ores and other raw materials by these countries to the more developed North and their import of manufactured and basic consumer goods in return (Bulmer-Thomas 1994, 57-60).

In light of the pre- and post-industrial nature of these respective FTAs with China and the US, it appears that these two small open economies with negligible industrial bases and minor weight in negotiating venues at the World Trade Organization (WTO) have basically short-circuited the current standoff within the Doha round negotiations concerning concessions to be made around the old and new trade agendas. While this two-pronged strategy is admittedly incipient, this pursuit of different goals across separate FTAs may well represent a way forward for other small non- or semi-industrial economies which face the challenge of combining comparative advantage based on natural resource exports with the exploitation of a competitive edge based on the modernization of services and investment.

At first glance, this arrangement appears to be quite strategic for all parties concerned. However, what might be the costs for these Latin American countries given the steep asymmetries involved, especially with regard to the hefty liberalization demands of the US concerning the new trade agenda? In Peru, direct political costs have already arisen in the form of violent protests in the northern mining town of Cajamarca against pollution of the local water supply by US and Chinese companies operating within these mining communities (Sanborn and Torres 2009; Romero 2010). Similarly, Chilean civil society has rebelled against the prospect of China's further incursion into that country's mining sector. In both countries, the deterioration of incomes for those working outside of this traditional primary export-led model, and the failure of policymakers in both countries to generate jobs and badly needed human capital investments in education and health, has invoked mass social protests over the past few years. In the following sections of this article I evaluate the agreements themselves and then explore the political implications that are inherent in the choice of this particular development path.

1. GOING FOR BROKE? THE RECENT HISTORICAL BACKDROP

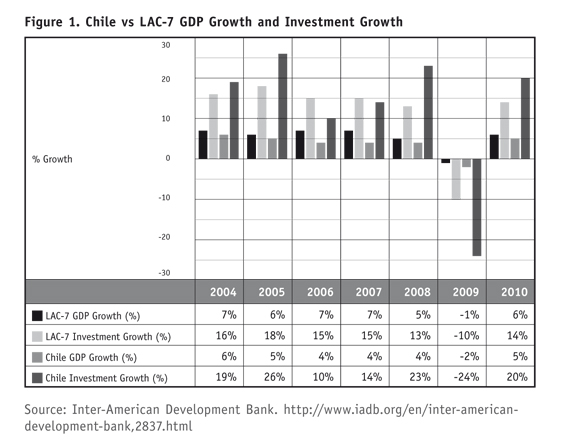

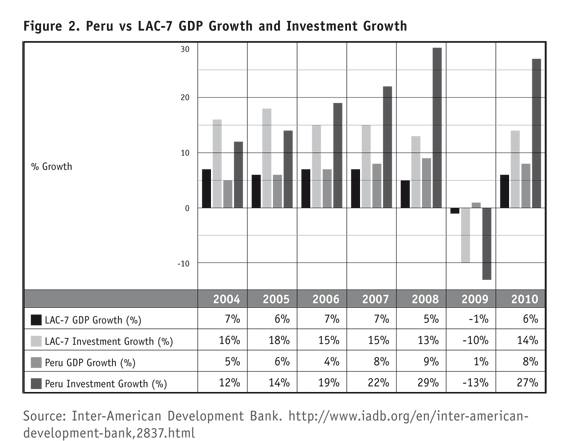

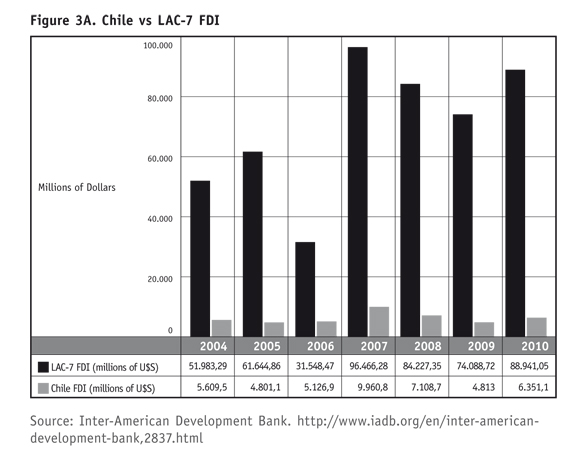

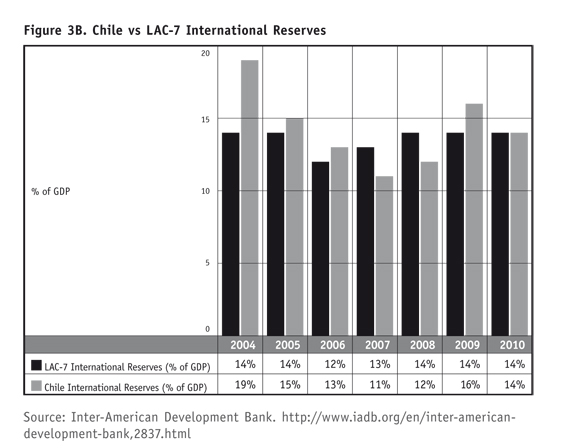

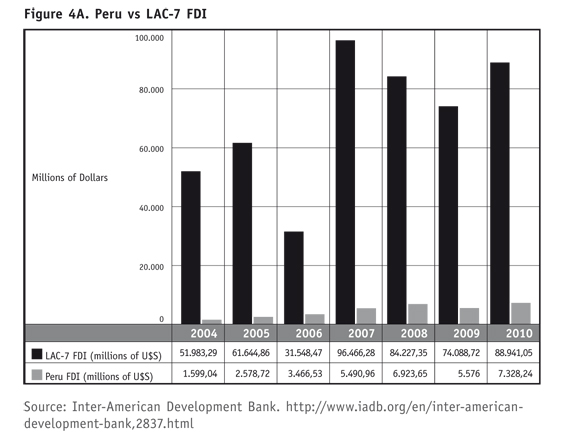

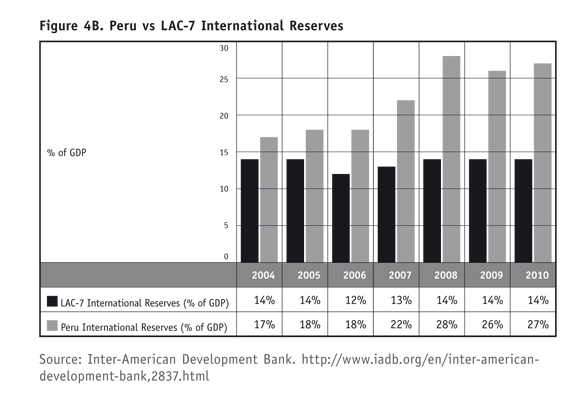

As longstanding members of the Asia Pacific Economic Cooperation forum (APEC), and as two of the top economic performers in Latin America over the past decade, there is little question as to the preparedness of Chile and Peru to literally play both sides of the Pacific in economic and political terms. As figures 1 and 2 show, both countries have grown briskly during the 2000s in terms of the average rate of GDP, and in the case of Peru it is the pace of investment growth that has been especially spectacular. Based on a steady and ongoing process of unilateral liberalization spanning nearly four decades in the case of Chile and two decades in the case of Peru, policymakers in these small open economies have effectively consolidated an export-led model driven by investment and competitive gains. Although both countries took a major hit on the capital account during the 2008-10 global financial crisis (see figures 3 and 4), the previous consolidation of financial sector reforms in both cases enabled policymakers to avoid a full-blown meltdown of the kind that occurred a decade earlier during the 1997 Asian financial crises (Porzecanski 2009).

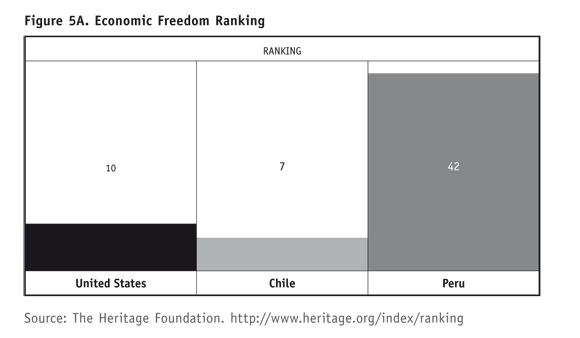

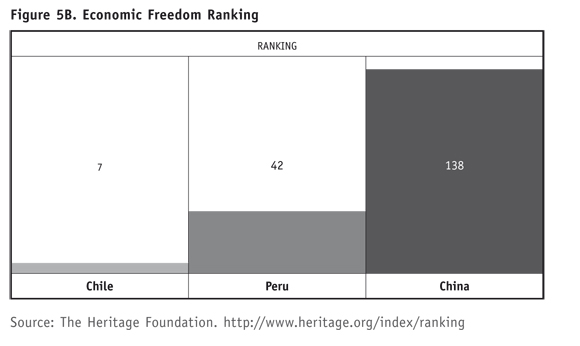

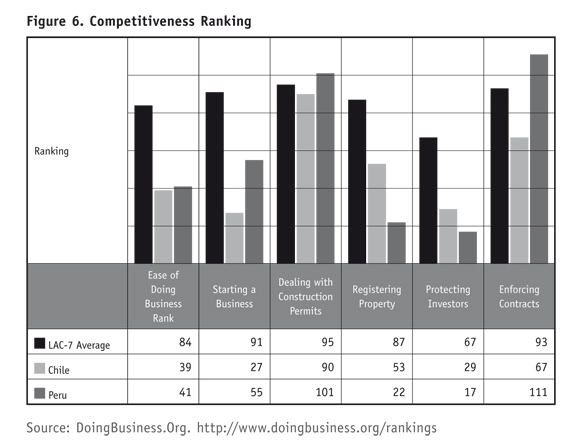

While Chile and Peru are united by geography, endowment factors, and deep-rooted commitment to economic reforms, there are important differences. As figure 5 shows, Chile now ranks ahead of the US and in the top ten on the Heritage Foundation's index of economic freedom, one of the most widely referred to indices of economic competitiveness, whereas Peru clearly has a way to go. Since 2008, however, Peru moved up from 57th to 42ndth place on this index in 2012,2 and it now dominates the top seven Latin American countries (LAC-7) on half of the key competitiveness rankings within the World Bank's Doing Business database (see figure 6);3 Peru can thus be expected to move steadily up in its competitive ranking. China's abysmal ranking on the economic freedom index in figure 5 reflects the extent to which its record-breaking growth relies less on productivity and efficiency gains and more on its sheer size, massive economies of scale and decidedly heterodox development strategy (Naughton 2006; Devlin 2008; Subramanian 2011). In contrast, as small primary exporters with aggregate GDP which totals a mere fraction of China's, the route to success for Chile and Peru lies in increased efficiency and productivity gains, i.e. making the very most of their endowment factors (Bulmer-Thomas 1994). In both cases, the FTA strategy has emerged as an integral part of this quest to promote higher growth, investment, and overall competitiveness.

Apart from signing a number of bilateral FTAs within Latin America, Chile has finalized similar agreements with Canada, Japan and Korea, has put in place a partial preferential agreement with India, and has Economic Association Agreements with New Zealand, Singapore, and the European Union (EU) (Stallings 2009). While these agreements may signal a chaotic spaghetti bowl pattern of trade and investment integration (World Bank 2005), they also reflect Chile's determination to continue reaping the gains of past liberalization. In particular, Chile's pursuit of FTAs with developed and large emerging market countries distinguishes it from much larger players in its own sub-region, for example, Argentina and Brazil. Chile's separate FTAs with China and the US are a hallmark of this competitive strategy.

While Peruvian policymakers have long voiced admiration and a commitment to launching a Chilean style export-led model, it has taken the past two decades for the country to implement the institutional and economic policy reforms that such a strategy necessitates (Wise 2003). Having crossed a threshold of reform consolidation in the early 2000s, Peru has embraced the Chilean FTA strategy of negotiating with large countries which promise to deliver the most compelling trade and investment gains. On this point, apart from the launching of FTAs with Canada, Chile, Singapore, the US, and China, Peru is in the process of finalizing separate agreements with Japan, Mexico, and the EU. However, in the case of both countries it is their separate but simultaneous negotiation of bilateral FTAs with China and the USthe two countries with which they have the strongest economic tiesas well as the enormous possibilities for realizing dynamic gains and hub production status by virtue of their strategic Pacific Rim location, which represents something entirely new.

2. TRADE LIBERALIZATION À LA CARTE

A number of additional factors account for the success of Chile and Peru on these FTA fronts. It goes without saying that the implementation and consolidation of market reforms, the steady pattern of favorable macroeconomic performance and growth, and the impressive professionalization of the trade policymaking apparatus in both countries, were necessary conditions for the launching of FTA negotiations, as was the unique endowment factors and rich array of natural resources that each brought to the table.

It should be pointed out that two larger trends prompted these small, open economies to engage in a pattern of "trade liberalization a la carte." First, there was the collapse of negotiations for a Free Trade Area of the Americas (FTAA) in 2005, a project launched by the Clinton administration back in 1994 with the intention of negotiating a comprehensive liberalization accord amongst all 34 democratically elected countries in the Western Hemisphere. Second, a year later the Doha round negotiations at the WTO broke down. While the lapse of both sets of negotiations occurred amidst a complicated political and economic backdrop, the deal breaker for both the FTAA and Doha was the inability of all sides to agree on the granting of deeper concessions around the aforementioned items on the old and new trade agendas.

Up until 2000, the FTAA option had been touted by Washington as an interim step that would prepare the Western Hemisphere to enter the next round of multilateral negotiations with a cohesive set of accomplishments and demands on the old and new trade agendas (Cohn 2007). Implicitly, as a brain child of the US policy establishment, the FTAA offered the opportunity to hammer out these differences between North and South on a smaller scale, but in ways meant to favor specific US interests in crafting new investment rules and disciplines within the hemisphere. However, from the Latin American standpoint, the FTAA was also a response to the Uruguay Round (1986-1994), where compromises which had been made on both the old and new trade agendas in order to get the job done, provoked an almost immediate sense of buyer's remorse.

On the old trade agenda, although the Uruguay Round was the eighth set of multilateral negotiations since the launching of the inaugural GATT Geneva Round in 1947-48, it was the first multilateral agreement to cover reductions in tariff and non-tariff barriers for agricultural goods, textiles, and clothing. However, by the mid-2000s, Stiglitz and Charlton (2005, 46) noted that "the average OECD tariff on imports from developing countries is four times higher than on imports originating in the OECD." Moreover, the US and the EU have notoriously been stubborn in resisting sizable cuts in agricultural subsidies. On the new trade agenda, a coalition of developed countries led by the US had finally succeeded in extending WTO coverage to services and trade-related investment and intellectual property. In expectation of their increased market access for agricultural and industrial goods, the developing countries agreed to negotiate new rules and domestic disciplines in these areas. The result was the GATS (General Agreement on Trade in Services) and two agreements on Trade-Related Investment Measures (TRIMS) and Trade-Related Aspects of Intellectual Property Rights (TRIPS) (Kotschwar 2009; Roy, Marchetti and Lim 2009).

The motivation for all parties concerned was the projected welfare gains from the implementation of the Uruguay Round, which ranged wildly from US$50 billion to US$275 billion a year, a large share of which was projected to benefit the developing countries (Stiglitz and Charlton 2005, 46). Yet, five years into the Uruguay Round, the ill preparation and steep costs of complying with these various agreements meant that 90 of the 109 developing country members of the WTO were far behind schedule in implementing those new trade agenda items to which they had signed up earlier (Finger 2000). While the participation of the developing countries in the Uruguay Round had been unprecedented, there was clearly more work to do in realistically reconciling developed and developing country demands and implementation capabilities around the old and new trade agendas. Herein lay the decision to launch the 2001 Doha round and to assign it a specific development mandate (Cohn 2007).

However, with the subsequent collapse of these regional and multilateral negotiating venues, a more recent and bold trend of bilateralism has prevailed, as evidenced by the recently confirmed Colombia-US FTA, the Costa Rica-China FTA and, of course, the China and US FTAs negotiated with Chile and Peru. The bottom line in terms of Chile and Peru is that both countries are seeking to achieve different sets of goals around the old and new trade agendas by simultaneously engaging in FTAs with two of the largest markets in the global economy. Especially with regard to China, it is the rapidity with which its trade ties have grown with Chile and Peru, in both absolute terms and relative to US trade with these countries, which renders this a new chapter in the political economy of Latin American integration.

3. BRIDGING THE OLD AND NEW TRADE AGENDAS

a. The Old Trade Agenda

By the time of the 1996 WTO trade ministerial in Singapore, the 'old' and 'new' issues on the multilateral trade agenda had been clearly demarcated. As mentioned earlier, the new trade agenda issues such as investment, services, and IPRs had been covered in separate mini-accords in the final phases of the Uruguay round. At the Singapore meeting, Japan and the EU called for further negotiations on competition policy, government procurement, and trade facilitation (Cohn 2007, 156-158), which have been incorporated into the new trade agenda. While still contentious, the contours of the new trade agenda are fairly concise. The old trade agenda is less so, mainly because the original GATT clauses dealing with market access and other issues were more generally phrased and thus left open to interpretation.

For the purposes of this analysis, and following the framework put forth by Estevadeordal, Shearer and Suominen (2009, 98-99), negotiations concerning the old trade agenda refer not just to the quest to liberalize agriculture and labor-intensive manufactured goods but also to: the extent of product coverage for liberalized tariff lines; the length of the transition period in reducing tariff and non-tariff barriers; and, the removal or phasing out of those policy instruments deemed to be most detrimental to market access. The latter would include, for example, subsidies, technical barriers, rules of origin, customs procedures, anti-dumping, safeguards and other special regimes. As the following analysis will show, the FTA that Chile and Peru each signed with China stuck closely to the extension of product coverage and to timelines for liberalizing all product lines, whereas the FTA which each negotiated with the US was weighted much more heavily toward the Singapore issues.

b. Chile's FTA with China: Market Access Concerns Prevail

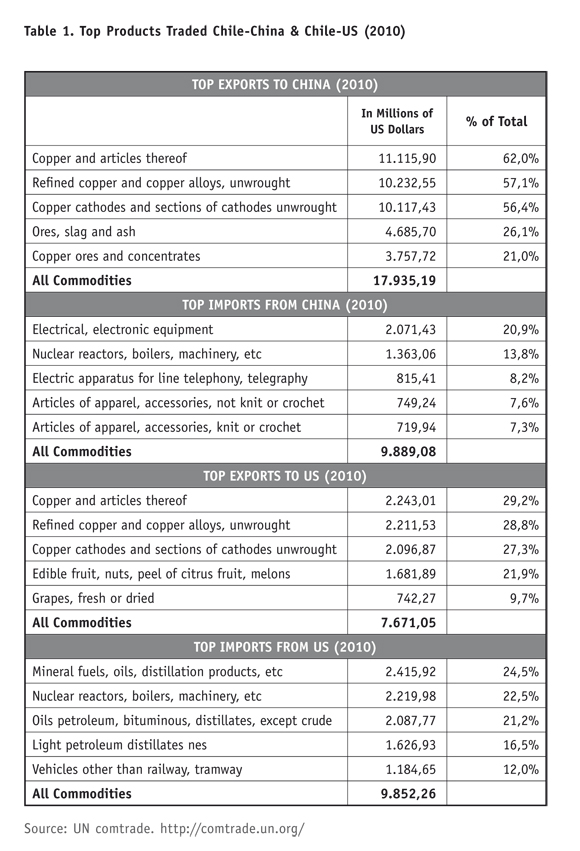

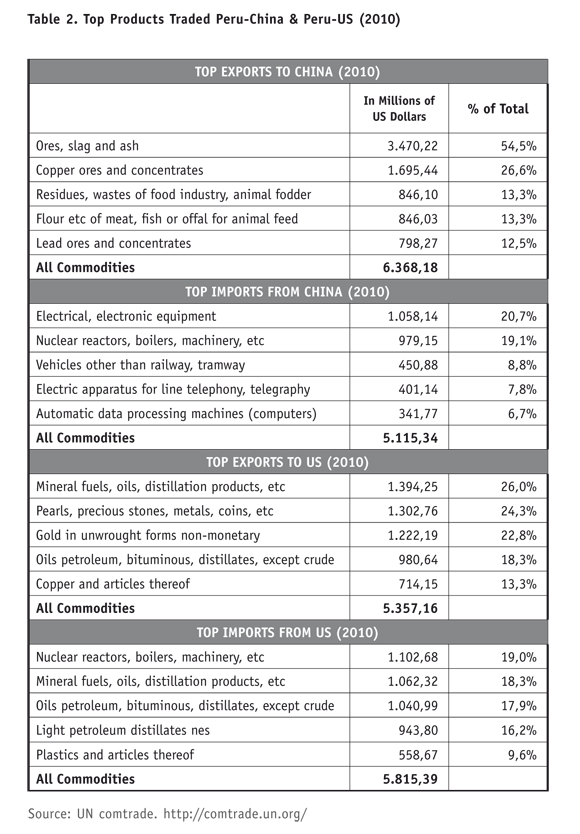

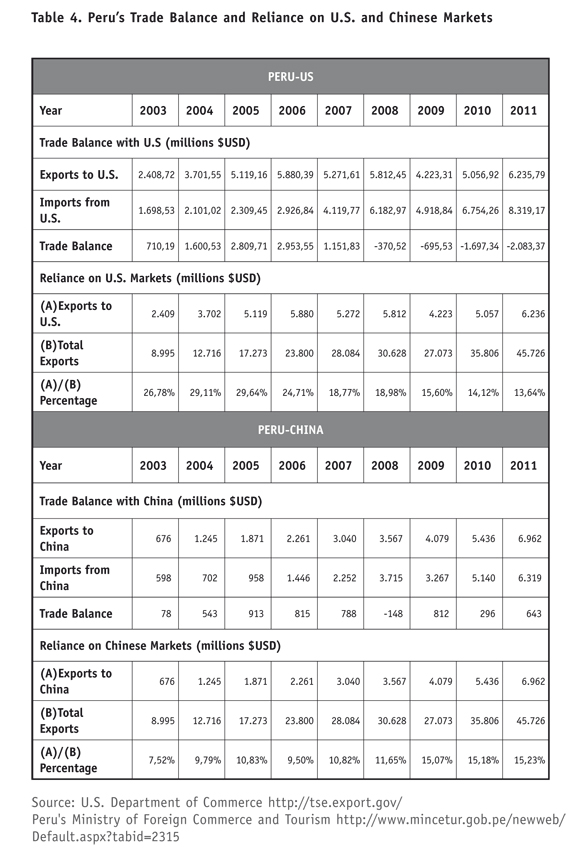

To a certain extent, the trade data in tables 1-4 reflect the triangular dynamic which is emerging in the Chile-China-US economic relationship, on the one hand, and the Peru-China-US relationship, on the other hand. On the export side, both countries are shipping a rich array of raw materials to China (copper, fishmeal) and the US (fruit, frozen seafood, wood, copper, tin and other minerals), while each is primarily importing manufactured goods from China and the US (see tables 1 and 2). The eagerness of both countries to lock in access to the Chinese market for their respective primary goods is a demand-driven phenomenon, as China's voracious appetite for raw materials to fuel its high growth has continued almost unabated.

The Chile-China FTA, China's first Latin American accord, sought the comprehensive reduction of tariff and non-tariff barriers for trade in goods. At the same time, the negotiation of services and investment was referenced as part of a future work program (Kotschwar 2009, 390). In terms of traded goods, this FTA provided immediate duty-free entry for 92 per cent of Chile's exports to China, although some of the country's most successful agro-industrial exports (fruits and fish) were placed on a ten year timeline for accessing the Chinese market (Stallings 2009). On the import side, 50 per cent of Chile's imports from China were granted duty-free access at the outset

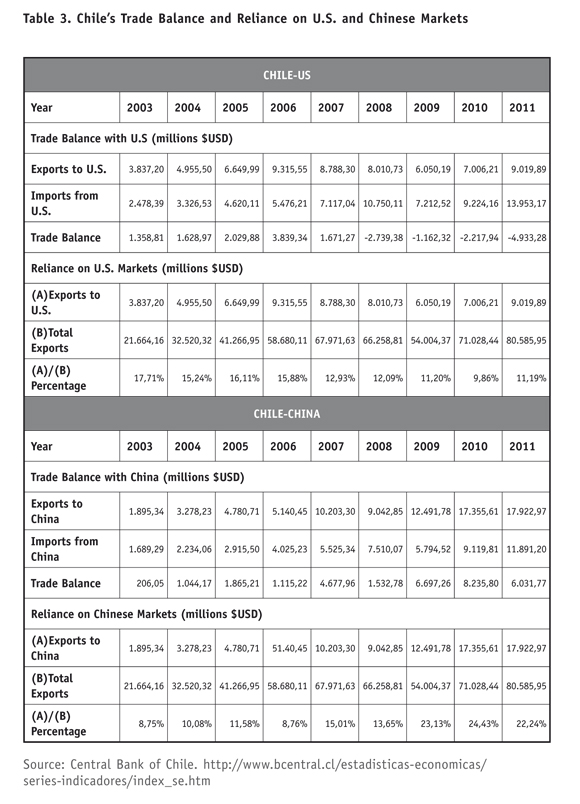

As table 3 shows, Chile's trade with China rose from about 9 per cent of its total trade in 2003 to nearly 14 per cent in 2008, the bulk of it based on copper. For example, copper represented 84 per cent of Chile's exports to China in 2008, with the rest made up mostly of other mineral and wood products. The importance of copper and minerals in this agreement is highlighted by the fact that only six of Chile's agricultural exports are covered by the FTA: apples, grapes, plums, chicken products, cheese, and cherries (Ellis 2009, 38). More than 90 per cent of Chile's imports from China in 2008 were manufactured goods, with over 42 per cent ranking as medium and high-tech (Barton 2009). In both the Chile-China and the Peru-China FTAs, penalties for protectionist measures relating to covered trade were incorporated, including the application of safeguards in response to preferential tariff treatment which could harm an industry of the other party.4

In 2008 the governments of Chile and China signed The Supplementary Agreement on Trade in Services of the Free Trade Agreement. While the negotiation over services is a more recent phenomenon (the 1994 NAFTA and 1995 GATS agreements set important precedents), Chile stands with the US and Singapore as one of the only three countries that are now party to more than five FTAs that include services (Roy, Marchetti and Lim 2009, 318-319). With this 2008 Supplementary Agreement China signaled an increased willingness to tackle the new trade agenda.5 In sum, this agreement covers business services (e.g., engineering, architecture, financial auditing, and advertising), computers and related services (e.g., software implementation, data processing, and hardware installation), real estate, research and development, telecommunications, and manufacturing services.

Of note here are the very few limitations applied by Chile in terms of market access for services and national treatment compared with China's thicker list of restrictions concerning Chile's access to its services market, in particular. With Chinese FDI in Chile currently amounting to less than one per cent of Chile's registered FDI (see figure 1), and Chilean flows of FDI to China were actually declining through the 2000s (Barton 2009, 237), the two governments are currently in the process of negotiating an agreement on investment. Despite Chile's goal of greatly enhancing its services trade and FDI inflows from China, the disproportionate weighting of the Chile-China economic relationship toward trade in goods and the dominance of Chile's copper exports suggests that old trade agenda issues will dominate ChileChina relations for some time to come.

A 2005 agreement signed by Chile's state-owned copper firm, CODELCO, and the Chinese company MinMetals bolsters this insight. By far the strongest FDI link between China and Chile, this agreement established a joint venture in which both companies kicked in US$110 million for capital investments (Barton 2009, 240-241). Through this new joint venture firm, Copper Partners Investment Company Ltd, Chile agreed to sell China copper at a fixed price and China committed to further capital investments to enable Chile to increase output to further meet Chinese demand (Ellis 2009, 37-38). Because this joint venture is registered in the tax haven of Bermuda, it does not appear in the accounting of Chile's FDI inflows (Barton 2009, 242).6 This problem aside, the thrust of the Chile-China partnership is copper, not the promise of new dynamic Chinese investments in services. he importance of copper is such that China's efforts to acquire additional mining assets have met with staunch political resistance on the part of Chilean civil society (Ellis 2009, 37).

c. The Peru-China FTA: Broad but Shallow

Some similar dynamics are underway in Peru-China trade and investment relations. The Peru-China FTA was formally implemented in March 2010 and China has hailed this as the most comprehensive FTA it has yet signed.7 While this is true, the very low levels of Chinese FDI in Peru (see figure 2) and the overwhelming role played by Peru's primary exports in its trade relationship with China also relegate the main action within this FTA to the old trade agenda. Peru's combined mineral and fishmeal products make up 90 per cent of its exports to China (copper at 42 per cent, fishmeal at 20 per cent, with other minerals comprising the remaining 28 per cent), while the bulk of its imports from China are medium-to-high value-added manufactured products (see table 2). At the outset of this FTA, Peru's trade with China accounted for around 12 per cent of its total trade, up from 8 per cent in 2003. By 2007 China had joined step with the US as Peru's most important trading partner (Ellis 2009, 148).

Whereas Chile was the first Latin American country to negotiate a comprehensive FTA with China for the elimination of tariffs on trade in goods, Peru was the first to actually incorporate items on the old and new trade agendas into an FTA with China. Yet despite Peru's success in negotiating the broadest agreement so far with China, those portions of the Peru-China FTA which cover the new trade agenda are nowhere near as detailed, for example, as the Chile-China 2008 Supplementary Agreement on Trade in Services. On this count, the Peru-China FTA is rather light. The treatment of labor and environmental issues in both the Chile-China and Peru-China FTAs is another case in point. In both FTAs these issues are addressed under the umbrella of a separate chapter on 'Cooperation'. However, these are little more than bullet points which make reference to previously existing letters of agreement between China and these countries on labor and environmental issues.

On the old trade agenda Peru was quite proactive in reducing tariffs on 99 per cent of its exports to China, 83.5 per cent of which entered the Chinese market duty free at the outset of the agreement (González Vigil 2009). In return, 68 per cent of China's exports to Peru were granted immediate market access. At the same time, Peru altogether excluded some 592 "sensitive products" in the textile, garment, shoes, and metal mechanics industries, which amounted to around 10 per cent of the value of China's exports to Peru. For its part, China excluded wood, paper, and some agricultural products (e.g., coffee, wheat, rice, corn, sugar, and vegetable oils) from the FTA, which reflected just 1 per cent of the value of Peru's exports.8

On the new trade issues, separate chapters on services and investment commit both sides to uphold national treatment, greater transparency, and the use of dispute settlement mechanisms in the event of a conflict. The services chapter explicitly covers tourism (China has designated Peru as an official tourist destination), postal express services, transfer payments, and a range of professional services (e.g., translation, consulting, cross-border data transmission). The investment chapter basically reaffirms The Agreement for the Promotion and Protection of Investment that both countries signed back in 1994. Like Chile, Peru is anxious to attract Chinese FDI and services trade as a result of this FTA. In support of these goals, Peru's Grupo Interbank opened a branch office in China in 2007, and China Development Bank established a strategic partnership with Peru's Banco de la Nacion in 2008 to facilitate microfinance lending in Peru (Ellis 2009, 155). Still, this is not where the action lies in China-Peru economic relations.

Like Chile, China's FDI presence in Peru is concentrated in mining (iron and copper), with some minor commitments in oil and natural gas. In addition, perhaps even more so than in Chile, China's investment in Peru's mining sector has at times provoked civic unrest, especially with regard to China's labor practices and its weak record in the safe disposal of environmental waste (Romero 2010). Although China's FDI in Peruvian mining has been widely reported, the routing of these investments through tax havens like Bermuda or the Cayman Islands has led to a similar, albeit legal, pattern of under-reporting as has occurred in Chile. Thus, some spectacular investments, like China's Aluminum Corporation purchase of Peru's share in the Canadian mining company Peru Copper for US$792 million in 2007 (Ellis 2009, 151), fail to appear in the data. Yet, and akin to Chile, the ties that bind Peru and China are central to the old trade agenda and offer little in the way of new dynamic Chinese investments in services.

d. The New Trade Agenda and Deeper liberalization: Chile's and Peru's FTAs with the US

With the Latin American region long regarded as part of the US sphere of influence, the historical timeline on trade and investment between the US and these countries is of course much longer. For the purposes of this discussion, the relevant starting point for Peru was its entry into the Andean Trade and Preference Act (ATPA) in 1991 and for Chile its ultimately thwarted invitation to join NAFTA in 1994. Additional factors shedding light on why the FTAs which each negotiated with the US in the 2000s were weighted heavily toward the new trade agenda, include the longstanding membership of each in the GATT, the concomitant lowering of Most Favored Nation (MFN) tariffs under the GATT/WTO,9 and the deep process of unilateral liberalization underway in each country. There was also the firm realization by policymakers and private actors in both Chile and Peru that the modernization of services and investment was a necessary condition for achieving higher levels of efficiency, productivity, and competitiveness.

As for the antecedents to the Peru-US FTA, in 1991 the US Congress passed the ATPA with an eye toward lessening the reliance of the Andean countries (Bolivia, Colombia, Ecuador, and Peru) on the proceeds from drug production and transshipment. So as to encourage the diversification of crops and exports away from the drug trade, the US offered significant aid and generous market access for goods exported from these countries. By 2004, when FTA negotiations between Peru and the US were started, ATPA-covered trade accounted for roughly 20 per cent of Peru's exports to the US market, all of which consisted of agriculture and other raw materials (see table 2).10 In mounting their lobbying effort for the passage of this agreement, Peruvian policymakers and the various pro-FTA business chambers argued that ATPA-covered exports from Peru to the US market accounted for more than a million jobs in Peru (USTR 2009, 45). There was, moreover, the uncertainty of how much longer the US Congress would continue to approve these ATPA trade preferences, given that Bolivia had abdicated in 2008 and Ecuador was continuing to waver in its compliance.

Thus, Peruvian policymakers and export-oriented producers were eager to lock in ATPA preferences with the negotiation of the Peru-US FTA (De la Flor 2010), as the US Congress had failed to renew this bill in 200102, and the trade and investment hit suffered by the Peruvian private sector had been palpable.11 In achieving their goal of completing a bilateral FTA with the US, Peruvian negotiators secured some additional, although minor, concessions for exports covered by ATPA (De la Flor 2010, 66).12 In exchange, the US made significant inroads with the liberalization of Peruvian agriculture, manufacturing, and the aforementioned items on the new trade agenda (USTR 2007). On this latter point, both the Peru-US and the Chile-US FTAs are modeled closely after NAFTA, which is considered to be the most comprehensive and detailed of all FTAs (Estevadeordal, Shearer and Suominen 2009, 137).

The nature of the Chile-US FTA was shaped by Chile's designation as the first new adherent to NAFTA, as announced by the US and its NAFTA partners at the 1994 Miami Summit of the Americas. It was envisioned that NAFTA would be incorporated into the FTAA, which would embrace WTO-plus rules and norms which surpassed the achievements of the Uruguay Round. However, the ability of the US to negotiate the FTAA, or for that matter the accession of Chile to NAFTA, was hampered by the systematic veto of the fast-track negotiating legislation by the US Congress until the passage of the Bipartisan Trade Promotion Authority Act of 2002 (TPA).13 By this time, Chile's bilateral trade strategy was highly developed. Apart from negotiating separate FTAs with Canada and Mexico in anticipation of NAFTA entry, Chile had negotiated bilateral FTAs with nine other Latin American countries in preparation for the FTAA. Simultaneously, Chile embarked on the aforementioned negotiation of FTAs with much larger global partners, including the EU, South Korea, Japan, China, and India.

With Trade Promotion Authority finally in hand, the first point of business for the Office of the US Trade Representative (USTR) was the completion of the Chile-US FTA, which enabled the Bush administration to showcase its newly articulated "competitive liberalization" strategy of rewarding neoliberal reformers and achieving WTO-plus results in these bilateral deals (Quiliconi and Wise 2009). However, in the case of Chile, the US actually had some catching up to do, as the 2005 Chile-EU agreement had been declared by an EU spokesperson to be "the most innovative and ambitious results ever negotiated by the EU" (Stallings 2009).14 Whereas overall US FDI to Chile had dropped from 37 per cent of the country's total FDI in 1994 to 20 per cent in 2003, Spain, in particular, now represented some 18 per cent of FDI inflows in such Chilean service industries as banking/finance, energy, and telecommunications, all of which had proved quite profitable (Manger 2009, 164).

From the standpoint of the US, competitive liberalization quickly came to denote the goal of establishing a firm toehold in services and FDI, if not 'first mover' status, in the FTAs it negotiated with Chile and subsequently Peru, as well as with other countries in the Western Hemisphere.15 Since the Chile-US and Peru-US FTAs were modeled closely on the NAFTA accord, the old trade agenda items within each concerning the elimination of tariffs and opening up of markets are quite similar. One notable exception lies in agriculture, where Chile negotiated a 12-year transition for the removal of tariffs and elimination of an import price band system on wheat, wheat flour, and sugar.16 Similarly, Peru retained a 17-year liberalization timeline on sensitive agricultural products, while some 60 per cent of US farm exports to Peru became duty-free automatically.17 Otherwise, these two North-South FTAs conformed to an emerging trend, one where the bulk of all tariff lines are liberalized by year 5 and the remainder by year 10 (Estevadeordal, Shearer and Suominen 2009, 126).

On the new trade agenda, the Chile-US FTA set the precedent of incorporating labor and environmental standards within the agreement, rather than the side accord format adopted under NAFTA, and Peru followed suit in its FTA with the US.18 Of particular note are the chapters within both FTAs on investment, cross-border trade in services, financial services, telecommunication, electronic commerce, and intellectual property. The negative-list approach is used in both agreements, which means that everything is liberalized unless otherwise marked. In all respects, both FTAS are considered to be WTO/GATS-plus, "the aim being to achieve greater coherence between services and investment disciplines so as to avoid discrepancies in the treatment of investment in goods and services or in the treatment of trade in services under different modes of supply' (Roy, Marchetti and Lim 2009, 320-321). Alternatively, to put this in GATS/WTO parlance, both the Chile-US and the Peru-US FTAs made giant leaps in terms of higher levels of commitment and enhanced sector coverage within both mode 1 (cross-border supply, or service flows from one WTO member country to another) and mode 3 (commercial presence, whereby a service supplier from one WTO member country establishes a territorial presence in another to provide services via ownership or leasing provisions) under the GATS (Kotschwar 2009, 370; Roy, Marchetti and Lim 2009, 334-35).

In both Chile and Peru, the US won extensive access to professional services (e.g. engineering, accounting, architecture), the local telecommunications market, the supply of financial services across the border, and the right of US insurance companies to establish local branches. In both counties, for example, US insurers were allowed to offer marine, aviation, and transport insurance for the first time; in financial services, asset management companies were allowed to offer new instruments, including mutual funds and voluntary savings plans (Roy, Marchetti and Lim 2009, 346-350);19 and in telecom, US suppliers were granted local access in the provision of basic services. However, given the previously mentioned differences between the two countries in terms of the overall level of development, the US addressed this discrepancy by providing Peru with about $58 million in trade capacity building assistance during the negotiating period between 2004 and 2006.

Moreover, although the Peru-US FTA had been approved by the congress of both countries in 2007, the Bush administration held up the formal implementation of that agreement until it had received the green light from the USTR with regard to the Peruvian Congress's ratification of a core package of regulatory measures which conformed with those of the US.20 From the standpoint of Peruvian policymakers the change of administration in the US in January 2009, at the very moment of the launching of the Peru-US FTA, has left some doubt as to US follow-through on trade capacity building, but little ambiguity in terms of US expectations for deep regulatory reform to uphold Peru's commitments to implementing the new trade agenda (De la Flor 2010, 75). The USTR has, in fact, closely monitored Peru's compliance, which has been the source of some tension between the two governments.21

4. THE POTENTIAL COSTS AND BENEFITS

Given the steep asymmetries inherent in these parallel North-South FTAs, it is little wonder that they have invoked the wrath of anti-globalization activists and fair trade proponents, especially with regard to the lesser developed country, Peru. In the case of each country's FTA with China, it was this same reliance on raw material exports and manufactured/industrial imports that gave rise to the theory of "unequal exchange" in Latin America back in the 1950s (Bulmer-Thomas 1994, 298-299; Jenkins 2009, 60). In other words, this heightened dependence of Chile and Peru on a primary export model riddled with possibilities for adverse terms of trade and comparative disadvantage suggests valid cause for concern. At the same time, the clear intention of the US to stake its claim within lucrative sub-sectors of each country's telecom, insurance and financial services market has raised old 1960s-style dependency hackles concerning imperialism and exploitation (Weiss, Thurbon and Mathews 2004). In a more tempered vein, there is also the longstanding concern as to whether these agreements are trade-creating or trade-diverting and whether they promise Pareto-optimal welfare gains (Balassa 1961). The question which has been raised here is: can these pitfalls inherent in the old and new trade agendas be mitigated via the "ä la carte" strategy that Chile and Peru have pursued through parallel FTAs with China and the US?

Despite the challenges, this strategy does offer some promising prospects. Any concerns over possible trade diversion as a result of these FTAs can be dispensed with rather quickly. As the data in Tables 3 and 4 shows, the US percentage share of total Chilean trade has declined over the six-year lifetime of the Chile-US FTA, and the drop in this similar indicator for Peru-US trade has been even more precipitous since the onset of negotiations for the Peru-US FTA in 2004. In contrast to Colombia and Mexico, where well over 50 percent of exports are destined for the US market, both Chile and Peru have now reduced their percentage dependence on the US market down to 10 percent. While some of this declining trade with the US can be accounted for by the growth of each country's trade ties with China, the latter has occurred in tandem with a brisker pace of growth in both Chile's and Peru's trade with the rest of the world.

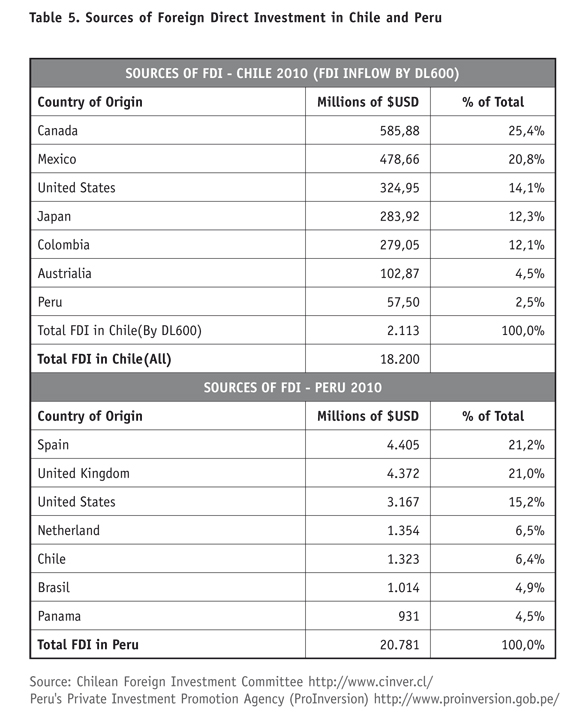

What about the possibilities for investment diversion, given the heavy emphasis of the US FTAs on the new trade agenda? In fact, as table 5 shows, the US ranks a distant third in its FDI flows in both countries, accounting for just 14 per cent of total FDI in Chile in 2010 (versus 25 per cent for Canada and 20 per cent for Mexico) and 15 per cent of total FDI in Peru (versus 21 per cent for Spain and 21 per cent for Great Britain). Whereas US FDI in Chile declined in the 2000s, in Peru it has more or less stagnated over the same time period (see figures 1 and 2).

The trade and FDI portrait that emerges between the US with these two South American countries is decidedly different from that of other US FTA partners in the region, such as Mexico or CAFTA-DR. Under NAFTA, for example, Mexico's trade dependence on the US has fluctuated between 80-88 percent of its total trade since the launching of NAFTA in 1994,22 and in 2008 the US percentage share of FDI in Mexico, although on the decline, still towered over distant competitors at 41 per cent.23 Since the launching of FTA negotiations with CAFTA-DR in 2004-05, US exports to this bloc have expanded by 44 per cent and US FDI has more than doubled; in Costa Rica, alone, US FDI accounted for 63 per cent of that country's total in 2008.24 In North and Central America, then, concerns over trade and investment diversion, as well as an over-dependence on the US market, may well be justified. However, the data for Chile and Peru suggest a more defensive posture on the part of the US, one where US service investors are lagging behind their competitors, and US policymakers are anxious to stay in the game, rather than calling the shots.

What about the very legitimate claim concerning the risks of asymmetrical integration with the US with regard to items on the new trade agenda (Weiss, Thurbon and Mathews, 2004)? Since the advent of NAFTA, the entry into a bilateral FTA with the US has been prized by capital-scarce developing countries as the most expedient way to signal to foreign investors that their commitment to deep economic reform is authentic. The trade-off, of course, has been the willingness of these US FTA partners in Latin America to sign on to the new trade agenda and to the adoption of US regulatory codes and disciplines. Yet while an FTA with the US may still be the ultimate signal for potential investors, both Chile and Peru have managed to leverage investment from multiple sources even prior to implementing an FTA with the US. By liberalizing unilaterally and covering some 90 per cent of their respective trade in FTAs with more developed and competitive partners, these countries have succeeded in diversifying and strengthening their economic ties in ways that have eluded their northern neighbors in the region.

This is not to say that Chile and Peru have avoided the costs of entering into an FTA with the US, but they have certainly managed to spread the risks. Furthermore, for both countries, the China FTA has been another way of hedging. Firstly, as secured access for exports to the US and Chinese markets are a main priority for producers in these countries, as is the attraction of FDI inflows from these mega-economies, the prospect of dynamic gains and lower opportunity costs enabled political leaders in Chile and Peru to finesse the usual collective action standoff over negotiations around the new trade agenda. Secondly, the pursuit of old and new trade issues across the two FTAs transformed the political incentives for public support of these accords, as the perceived net benefits now appeared to credibly exceed the overall costs.

On the upside, in contrast with the revenue losses associated with a reduction of tariffs on trade in goods, the reduction of barriers in new trade agenda sectors does not lead to a loss of revenue. Moreover, the nature of services liberalization is such that the removal of barriers for suppliers from one country (e.g., the US or Spain) makes it more likely that this increased access will be applied to suppliers from other countries (Roy, Marchetti and Lim 2009, 353-54). Equally important, under the impulse of unilateral and bilateral liberalization across the old and new trade agendas, both Chile and Peru are quickly advancing their own respective positions within the international political economy. For example, on the World Bank's 2011 Doing Business competitive rankings,25 out of 183 countries, Chile now stands at number 39 and Peru at number 41, versus scores of 114 for Uruguay, 118 for Argentina, and 130 for Brazil.

However, as Rodrik (1992) reminds us, there are always winners and losers from these arrangements and any semblance of success will require that the losers be compensated. As regional leaders in terms of high growth, low inflation, and rock solid macroeconomic management in the 2000s (Porzecanski 2009), and by virtue of having implemented these parallel FTAs, both Chile and Peru have indeed projected the image of dynamic Pacific Rim hubs. Still, there is a downside. On the new trade agenda, although the removal of costly domestic restrictions can lead to lower domestic prices and to the extension of market access to country suppliers from outside the FTA, as a first-mover in some of these markets the US is at a distinct advantage. Hence, there is a strong need for sound regulatory oversight and transparency with regard to anti-trust and decision-making practices on licensing applications (Roy, Marchetti and Lim 2009, 353-54). This is especially urgent for Peru, which is still in the process of implementing many of these laws as a result of the aforementioned US demands around the harmonization of codes, disciplines, and business practices.

The effect of these FTAs on old trade agenda sectors represents another distinct downside, as both have placed considerable pressure on small agricultural concerns and local manufacturing industries in Chile and Peru. This includes, for example, Peru's textile producers or Chile's mid and high-tech industrial enterprises. In the agricultural sector, the setting of prolonged liberalization timelines and the offering of structural adjustment support has provided somewhat of a cushion from the US FTA, in particular (De la Flor 2010, 70). In the manufacturing sector, given the ferocity with which China has conquered these markets worldwide over the past decade (Gallagher and Porzecanski, 2010), the disruption of these sectors in Chile and Peru is a foregone conclusion with or without an FTA with China. In the Chilean case, the articulated goal is to move more quickly up the innovation curve, including large investments in the kinds of high-tech infrastructure and scientific human capital that would enable the country to fully emerge as a competitive Pacific Rim transport and logistics hub (Barton 2009, 235; Ellis 2009, 42). The pace of Chile's advances in this realm has been slower than promised by government policy makers. The strongest evidence of the public's dissatisfaction is the year-long university protests that paralyzed the public universities for most of 2011-12. At heart, Chilean university students are calling for affordable and relevant courses which will enable them to acquire the skills needed to absorb their labor into this strategy of combining comparative advantage based on natural resource exports with competitive edge based on the liberalization and modernization of services, and investment is both credible and tenable.

If the Chilean strategy lacks credibility in the eyes of the electorate, Peru is much further behind in this respect. As the country's 2011 Presidential election showed, the 50 percent or so of Peruvians who perceived themselves as excluded from the gains of trade and buoyant growth over the past decade succeeded in electing a candidate who offered the equivalent of a massive human capital shock. Without the exponentially higher investment in human capital and small businesses promised by newly elected President Ollanta Humala, these two recent FTAs will mean little without a more compelling public policy framework to bolster and complement them.26 Although the country is clearly reaping the benefits of sound macroeconomic reforms and deep liberalization since the early 1990s, it still lacks the necessary micro-economic policies to bring these reforms to full fruition (Wise 2003; De La Flor 2010, 81-2). Taking a page from Chile's lesson book, this would include: more targeted and vigorous investment in human capital; the equivalent of an investment shock in infrastructure and productive capacities; and an explicit strategy which promotes ties between R&D, private initiative and the adaption of efficiency-enhancing technology, especially within small and medium-sized firms. Should Peruvian policymakers lose focus and mistake the implementation of these FTAs as a substitute for continued reform, they will quickly confront the reality that FTAs cannot substitute for the hard work of microeconomic restructuring, institutional renewal and policy innovation.

CONCLUSION

The pattern that has been analyzed here, whereby the respective US bilateral FTAs with Chile and Peru target the new trade agenda, and the respective Chinese FTAs with each country focus closely on the old trade agenda, represents an important breakthrough; these two small open developing countries have managed to overcome the collective action standoff which has stalled the Doha round at the WTO since 2006. Although a multilateral route to trade and investment liberalization would probably offer longer liberalization timelines and more flexible terms for small open developing countries, the foreclosing of this venue for the time being has rendered bilateralism a second-best option. The ability of Chile and Peru to successfully engage in this bilateral strategy of liberalization a la carte may well represent the more viable path forward for other small developing countries which have consolidated macroeconomic reforms and are prepared to take their development strategy to the next level of modernization and competitiveness.

Finally, although I have basically applauded this pattern of pragmatic bilateralism from the Latin American standpoint, I conclude with a note of caution. Both Peru and Chile have set their sights on becoming dynamic Pacific Rim hubs. The launching of these bilateral FTAs with the US and China represents an impressive effort to combine a strategy based on comparative advantage and natural resource exports with one based on promoting competitive edge via the liberalization and modernization of services and investment. However, the success of these FTAs will rest crucially on the design and implementation of a more pro-active competition policy, one that invests vigorously in human capital, spurs productive investments, increases ties between R&D and private initiative, and promotes the adaption of efficiency-enhancing technology. For Peru more so than Chile, the negotiation of these path breaking FTAs could mean little without a more compelling political commitment and public policy framework to bolster and complement them.

Comentarios

1 The author thanks Kimberly Burtnyk, Javier Colato, Mariana González Insua, Daniel Paly, Victor Paredes-Colonia, Dawn Powell, Chengxi Shi, Vijeta Tandon, and Becky Turner for their excellent assistance in completing the research and compiling the database for this paper.

2 See Heritage Foundation, 2012 Index of Economic Freedom, Country Rankings, www.heritage.org/Index/Ranking.aspx (accessed 4/24/12)

3 See World Bank, Doing Business: Measuring Business Regulations, http://www.doingbusiness.org/ (accessed 4/24/12)

4 "Free Trade Agreement Between the People's Republic of China and the Government of the Republic of Chile," Articles 44 and 45, Foreign Trade Information System, Organization of American States, http://www.sice.oas.org/Trade/CHL_CHN/CHL_CHN_e/Text_e.asp#Sec1 (accessed 4/24/12)

5 For a summary of this supplementary agreement on services go to Ministry of Commerce of the People's Republic of China, http://fta.mofcom.gov.cn/topic/enchile.shtml (accessed 4/24/12)

6 There are wild discrepancies in the Chinese data that report FDI flows to Chile and in Chile's reporting on this same indicator. The difficulty in gauging these numbers is that Chinese FDI is frequently channeled through tax havens in Bermuda or the Cayman Islands and tends to show up under 'services' in Chile's national accounts (Barton 2009, 238). In fact, the bulk of these funds are invested in mining and in mining-related endeavors.

7 See Ministry of Commerce of the People's Republic of China, http://fta.mofcom.gov.cn/topic/enperu.shtml (accessed 4/24/12)

8 For more detail go to Ministry of Commerce of the People's Republic of China, http://fta.mofcom.gov.cn/topic/enperu.shtml (accessed 4/24/12)

9 According to Article 1 of the GATT, member countries must offer market access on par with the 'most favored nation' amongst their trading partners; the formation of an FTA, the criteria for which are defined in GATT Article 24, is one way of circumventing the mandate that each signatory to the GATT/WTO charge trade duties on an MFN, or non-discriminatory, basis.

10 Copper cathodes dominated this list of APTA-covered goods, which included apparel, fresh asparagus, mangoes, grapes, paprika, and molybdenum ore (USTR 2009, 11).

11 Author's interview with Eduardo Ferreyros, Vice-Minister of Foreign Trade, Ministry of Foreign Trade and Tourism, Lima, Peru, September 2, 2008.

12 When renewed in 2002 the ATPA was renamed the 'Andean Trade Preference and Drug Eradication Act' (ATPDEA).

13 Fast-track/TPA stipulates that the US Congress can vote up or down on a trade agreement submitted by the executive branch, but amendments are prohibited once the final bill is sent to Congress.

14 The Chile-EU accord covered goods, services, government procurement, the liberalization of investment and capital flows, the protection of intellectual property rights (IPRs), and a binding dispute settlement mechanism (Stallings 2009).

15 Including the US-Central American-Dominican Republic FTA, or CAFTA-DR, and separate FTAs with Panama and Colombia that have yet to be ratified.

16 See Office of the United States Trade Representative, United States - Chile Free Trade Agreement, Final Text, Article 3.16. http://www.ustr.gov/trade-agreements/free-trade-agreements/chile-fta/final-text (accessed 4/24/12),

17 Office of the United States Trade Representative, United States - Peru Trade Promotion Agreement, Final Text. http://www.ustr.gov/trade-agreements/free-trade-agreements/peru-tpa/final-text . (accessed 4/24/12)

18 However, the labor and environmental commitments made by Chile and Peru in these separate FTAs with the US are no more binding that those within NAFTA. In all three agreements, each signatory has pledged to uphold their own domestic laws on these non-trade issues which, in the case of NAFTA, have undermined compliance.

19 Also see Office of the United States Trade Representative, United States - Peru Trade Promotion Agreement, Final Text. http://www.ustr.gov/trade-agreements/free-trade-agreements/peru-tpa/final-text. (accessed 4/24/12)

20 This statement is based on my confidential communication with policymakers at the Office of the United States Trade Representative, Washington, DC, September, 2008.

21 See "EE. UU. constatará posible falta a acuerdo commercial con Perú". http://www.bilaterals.org/spip.php?article17949 (accessed 4/24/12)

22 Mexico's trade statistics are published by the Secretariat of the Economy at: www.economia.gob.mx/comunidad-negocios/comercio-exterior/informacion-estadistica-y-arancelaria (accessed 4/24/12)m

23 Mexico's statistics on FDI are published by the Secretariat of the Economy at: www.economia.gob.mx/comunidad-negocios/inversion-extranjera-directa/estadistica-oficial-de-ied-en-mexico (accessed 4/24/12)

24 For these export figures go to U.S. Department of Commerce, Bureau of Economic Analysis, http://www.bea.gov/newsreleases/international/trade/2012/pdf/info0212.pdf. (accessed 4/24/12). For the FDI data go to U.S. Department of Commerce, Bureau of Economic Analysis, International Economic Accounts, http://www.bea.gov/internatio-nal/ii_web/timeseries7-2.cfm (accessed 4/24/12)

25 See World Bank, Doing Business: Measuring Business Regulations, http://www.doingbusiness.org/ (accessed 4/24/12)

26 "UNDP: Regional Inequities Persist in Peru Despite Economic Growth," Peruvian Times, 23 April 2010.http://www.peruviantimes.com/undp-regional-inequities-persist-in-peru-despite-economic-growth/235865 (accessed 4/24/12)

REFERENCES

1. Balassa, Bela. 1961. Towards a theory of economic integration. Kyklos 14 (1): 1-17. [ Links ]

2. Barcena, Alicia and Osvaldo Rosales. 2010. The People's Republic of China and Latin America and the Caribbean: Towards a strategic partnership. Santiago, Chile: Economic Commission for Latin America and the Caribbean. [ Links ]

3. Barton, Jonathan R. 2009. The Chilean case. In China and Latin America: Economic relations in the twenty-first century, eds. Rhys Jenkins and Enrique Dussel Peters, 227 - 277. Bonn: German Development Institute. [ Links ]

4- Bulmer-Thomas, Victor. 1994. The economic history of Latin America since independence. New York: Cambridge University Press. [ Links ]

5. Cohn, Theodore H. 2007. Te Doha round: Problems, challenges, and prospects. In Requiem or Revival? Te Promise of North American Integration, eds. Isabel Studer and Carol Wise, 147 - 165, Washington, DC: Brookings Institution Press. [ Links ]

6. De la Flor, Pablo. 2010. El TLC Perú-Estados Unidos: riesgos y oportunidades. In La economía política del Tratado de Libre Comercio entre Perú y Estados Unidos, eds. José Raúl Perales and Eduardo Morón 61 - 84, Washington, DC: Latin American Program, Woo-drow Wilson International Center for Scholars. [ Links ]

7. Devlin, Robert. 2008. China's economic rise. In China's expansion into the western hemisphere, eds. Riordan Roett and Guadalupe Paz, 111 - 147 Washington, DC: Brookings Institution Press. [ Links ]

8. Ellis, Evan R. 2009. China in Latin America: The whats & wherefores. Boulder and London: Lynne Rienner Publishers. [ Links ]

9. Estevadeordal, Antoni, Matthew Shearer, and Kati Suominen. 2009. Market Access Provisions in Regional Trade Agreements. In Regional rules in the global trading system, Antoni Es-tevadeordal, Kati Suominen and Robert Teh, 96 - 165. New York: Cambridge University Press. [ Links ]

10. Finger, Michael. 2000. Te WTO's special burden on less developed countries. Cato Journal 19: 425-37. [ Links ]

11. Gallagher, Kevin and Roberto Porzecanski. 2010. Te dragon in the room: China and the future of Latin American industrialization. Palo Alto: Stanford University Press, forthcoming. [ Links ]

12. González Vigil, Fernando. 2009. El TLC China-Perú: una negociación ejemplar. Punto de Equilibrio http://www.puntodeequilibrio.com.pe/punto_equilibrio/01i.php?pantalla=noticia&id=15789bolnum_key=29&serv_key=2100 . julio. (accessed 7/24/2010) [ Links ]

13. Jenkins, Rhys. 2009. Te Latin American case. In China and Latin America: Economic Relations in the Twenty-first Century, eds. Rhys Jenkins and Enrique Dussel Peters, 21 - 63. Bonn: German Development Institute. [ Links ]

14. Kotschwar, Barbara. 2009. Mapping investment provisions in regional trade agreements. In Regional rules in the global trading system, eds. Antoni Estevadeordal, Kati Suominen and Robert Teh, 365 - 417 New York: Cambridge University Press. [ Links ]

15. Lanxin, Xiang. 2008. An alternative Chinese view. In China's expansion into the western hemisphere, eds. Riordan Roett and Guadalupe Paz, 44 - 58.Washington, DC: Brookings Institution Press. [ Links ]

16. Manger, Mark. 2009. Investing in protection: Te politics of preferential trade agreements between north and south. Cambridge: Cambridge University Press. [ Links ]

17. Naughton, Barry. 2006. The Chinese economy: Transitions and growth. Cambridge, MA: The MIT Press. [ Links ]

18. Porzecanski, Arturo. 2009. Latin America: The missing financial crisis. Washington, DC: Economic Commission on Latin America and the Caribbean (ECLAC), Studies and Perspectives Series No. 6. [ Links ]

19. Quiliconi, Cintía and Carol Wise. 2009. The US as a bilateral player. In Competitive regionalism: FTA diffusion in the Pacific rim, eds. Mireya Solís, Barbara Stallings, and Saori Katada 97 - 117, Basingstoke, UK: Palgrave Macmillan. [ Links ]

20. Rodrik, Dani. 1992. Why the Rush to Free Trade in the Developing World: Why So Late? Why Now? Will it Last? Working Paper no. 3947, National Bureau of Economic Research, Cambridge, MA, January. [ Links ]

21. Romero, Simon. 2010. Tensions over Chinese mining venture in Peru. New York Times, 14 August. http://www.nytimes.com/2010/08/15/world/americas/15chinaperu.html?_r=1&emc=eta1 (accessed 8/15/10) [ Links ]

22. Roy, Martin, Juan Marchetti and Hoe Lim. 2009. Services liberalization in the new generation of preferential trade agreements: How much further than the GATS? In Regional rules in the global trading system, eds. Antoni Estevadeordal, Kati Suominen, and Robert Teh, 316 - 364, New York: Cambridge University Press. [ Links ]

23. Sanborn, Cynthia and Víctor Torres. 2009. La economía china y las industrias extractivas: desafíos para el Perú. Lima: Universidad del Pacífico, Centro de Investigación. [ Links ]

24. Shixue, Jiang. 2008. Te Chinese foreign policy perspective. In China's expansion into the western hemisphere, eds. Riordan Roett and Guadalupe Paz, 27 - 43. Washington, DC: Brookings Institution Press. [ Links ]

25. Stallings, Barbara. 2009. Chile: A pioneer in trade policy. In Competitive regionalism: FTA diffusion in the Pacific rim, eds. Mireya Solís, Barbara Stallings, and Saori Katada, Faltan páginas Basingstoke, UK: Palgrave Macmillan. [ Links ]

26. Stiglitz, Joseph E. and Andrew Charlton. 2005. Fair trade for all: How trade can promote economic development. New York: Oxford University Press. [ Links ]

27. Subramanian, Arvind. 2011. Eclipse: Living in the shadow of China's economic dominance. Washington, DC: Peterson Institute for International Economics. [ Links ]

28. United States Trade Representative (USTR). 2007. Free Trade with Peru: Summary of the United States-Peru Trade Promotion Agreement. June 7. Washington, DC. [ Links ]

29. United States Trade Representative (USTR). 2009 Fourth report to the Congress on the operation of the Andean Trade and Preference Act as amended. April 30. http://www.ustr.gov/sites/default/files/USTR 2009 ATPA Report Final.pdf [ Links ]

30. Weiss, Linda, Elizabeth Thurbon, and John Mathews. 2004. How to kill a country: Australia's devastating trade deal with the United States. Melbourne: Allen and Unwin Academic. [ Links ]

31. Wise, Carol. 2003. Reinventing the state: Economic strategy and institutional change in Peru. Ann Arbor: University of Michigan Press. [ Links ]

32. Wise, Carol and Cintía Quiliconi. 2007. China's surge in Latin American markets: Policy challenges and responses. Politics & Policy 35 (3): 410-438. [ Links ]

33. World Bank. 2005. Global Economic Prospects: Trade, Regionalism, and Development. Washington, DC: Te World Bank [ Links ]

34. Yang, Jian. 2009. China's competitive FTA strategy: Realism on a liberal slide. In Competitive regionalism: FTA diffusion in the Pacific rim, eds. Mireya Solís, Barbara Stallings, and Saori Katada, 216 - 235.Basingstoke, UK: Palgrave Macmillan. [ Links ]