Serviços Personalizados

Journal

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Citado por Google

Citado por Google -

Similares em

SciELO

Similares em

SciELO -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkEstudios Gerenciales

versão impressa ISSN 0123-5923

estud.gerenc. v.20 n.93 Cali out./dez. 2004

THE EFFECT OF DIVIDEND DISTRIBUTION ON SHARE RETURN IN CHILE

MAURICIO NASH1, DARCY FUENZALIDA

1Universidad Técnica Federico Santa María Department of Industries. Las Nieves 3435 Dept. 116, Vitacura, Santiago, Chile. Tel.: 56-2-2062508. Fax + 56-2-2060134. mauricionash@yahoo.com

Fecha de recepción: 8-3-2004 Fecha de aceptación: 12-7-2004

ABSTRACT

Numerous studies relating to the field of dividends have been carried out over the past twenty-seven years. The objective of this paper is to contrast it with the Barclay study (1987) and to complement the Venkatesh paper (1989).

This piece of research concludes that, contrary to Barclay´s findings, on their postclosure date, share returns in Chile do not fall in the amount of their dividend, owing to the fact that in this country the effect depends on the type of dividend. Finally, and as a complement to the Venkatesh study, it was determined that the average volatility of the twenty-five days prior to closure is lower than that evinced in the twenty-five days after closure.

KEYWORDS

Dividend; Clientele Effect; Cutoff Date; Dividend and Capital Gain.

JEL classification: G10,G12 and G19

INTRODUCTION

Chilean corporations are compelled by law to distribute at least 30% of their liquid profits. This makes it extremely important to measure the impact of dividend distribution on share returns.

Various domestic and international studies have analysed the issue over the past twenty-seven years. The principal objective of this piece of research is to contrast the international evidence provided by the Barclay study (1987) that examines share price behaviour on the day after the closure of the register of shareholders with a right to dividend payments. It was concluded that post-closure share returns fall in an amount that is equal to that of the dividend, in other words investors value dividends and capital gains as a perfect substitute. Another objective is to complement the Venkatesh study (1989), that concludes that the volatility of share returns is lower in the period that follows the announcement of a dividend, which would be explained by a lower uncertainty regarding the conditions of the corporation. So, contrary to what happens in the period that precedes the announcement of a dividend, investors give less importance to unverifiable information or to information based on rumour.

Our main objective is to determine if investors in Chile value dividends and capital gains as a perfect substitute, and our secondary objective is to study the volatility of share returns on the days that follow the closure of the register of shareholders with a right to dividend payments, thus complementing the Venkatesh study, which analysed volatility before and after the announcement. In this study, we will measure this volatility on the date of the closure of the register of shareholders with a right to dividend payments.

Initially we analysed dividend policies and types of dividends in Chile. Section II describes the most important studies carried out in the past twenty-seven years. Section III contains a methodological description. Section IV analyses the outcome of the study, and finally Section V explains our conclusions.

SECTION I

Dividend policy and types of dividends in Chile

As an average, companies in Chile distribute three provisional dividends per year, plus one compulsory minimum dividend, which is only paid when provisional dividends to not reach the minimum amount to be distributed.

Chilean companies are obliged by law to distribute at least 30% of their liquid profits.

Other occasional dividends may be eventual and additional. The following is a description of different types of dividends.

A) Provisional Dividend: The dividend that the board of directors agrees to distribute during the fiscal year, and that is chargeable to the profits for that period. This dividend is payable on a date determined by the board.

B) Definite dividends: These dividends are classified as follows:

B1) Compulsory Minimum dividend: The dividend that the shareholders´ meeting agrees to pay in order to comply with their obligation to distribute a minimum of 30% of their liquid earnings for each fiscal year in the form of a dividend.

B2) Additional Dividend: This dividend is a dividend that shareholders agree to pay over the legal compulsory minimum dividend.

B3) Eventual Dividend: This is a dividend that corresponds to the part of the profits that the shareholders´ meeting has not earmarked for payment in the form of a compulsory minimum dividend or of an additional dividend, and is to be paid during a future fiscal year.

On the other had, in order to design a dividend policy it is necessary to bear the following in mind:

A) Corporate Fund Requirements: Companies should analyse their real capacities to keep up a dividend flow vis-à-vis the distribution of probable future cash flows and their respective positions. This analysis determines probable future residual funds. This is important, as the market values dividend stability because it gives an implicit sign in terms of expectations.

B) Liquidity: Companies should maintain their liquidity in order to have a higher capacity to pay up dividends and face the unforeseen expenses and contingencies that are typical of growth. This is important, as in general, those companies that grow and are profitable may have a low liquidity level because they concentrate their investments on fixed assets and relatively non-liquid assets.

C) Borrowing Capacity: Companies should define their borrowing capacity by establishing their dividend policies with greater accuracy.

D) Nature of shareholders: When a company is strictly controlled, its management can have relatively easy access to its shareholders´ expectations regarding dividends, which facilitates the definition of the latter, and therefore the vast majority of them are subject to high tax rates. Consequently, a low dividend level can be established, but this should always be done on the basis of the existence of real investment opportunities with positive net current value (VAN). Higher dividend levels will be required when ownership is more diluted.

SECTION II

Empirical evidence

We will now describe important national and international studies related to dividend announcements and payment published over the past 27 years, such as the Jensen and Meckling (1976) study that established that agency costs increased according to the increased dilution of ownership. This cost represents the divergence between shareholders and the administrator, because a lower participation of outside shareholders in corporate ownership will result in a reduced possibility of monitoring and disciplining corporate administrators, and this will demand a larger dividend payment so as to ensure that administrators do not make improper use of the resources generated and thus reduce agency costs.

In the area of the factors that determine dividend payment, Rozlef (1982) studied the factors that determined dividend payment: A) External financing transaction costs, B) The financial restriction created by operational leverage and C) Corporate financing and agency costs. His study points out that transaction costs are strictly related to the firm´s level of financial and operational leverage, because its dependence on external financing increases when firm has a relatively high leverage level. Asquith and Mullins´ (1983) study analyses the case of the companies that pay dividends for the first time and states that these present abnormal returns. The results of this study indicate that the beginning of dividend payments and subsequent dividend increases tend to strengthen the wealth of shareholders. Dividends give valuable and unique information, and constitute a sign of the performance of a company and of its projects for the future.

On the other hand Easterbrook (1984) states that agency costs generated by the separation of ownership and control can be brought down by means of dividend policy. His analysis is based on the argument that a greater dispersion generates fewer incentives to control administration stock, because every individual shareholder is forced to bear his own monitoring costs, while they all capture the benefit involved. Therefore, the optimum scenario is that all shareholders monitor their stock as a group, because if this isn´t the case, nobody will achieve control This leads to the appearance of free-riders.

We also have the relevant contrasting work carried out by two important researchers. On the one hand, we have Miller and Rock´s (1985) study regarding the asymmetry of information existing among insiders (administrators) and outsiders (external investors). This problem emerges owing to the fact that as insiders have more and better information on the value of a company, dividend payments would be a signal of current and future earnings that have not been observed by outsiders. On the other hand Jensen´s (1986) study of free cash flow leads him to conclude that dividend payment solves the problem of free cash flow, avoiding the misuse of these cash surpluses, which are the surpluses left after realising all the projects with an 0+ Net Current Value (VAN) and that are discounted from the relevant capital cost rate.

In another important study, Barclay (1987) refers to the way in which individuals value dividends and capital gains the day after the closure of the registers of shareholders with a right to receive dividends. He concluded that the post closure share returns fall in an amount that is equal to the dividend, which means that investors value dividends and capital gain as a perfect substitute.

On the other hand, in their 1989 study, Lang and Litzenburg tried to explain the effect that dividend announcements had on share prices, contrasting the hypotheses of signalling and free cash flow established by Miller and Rock (1985) and Jensen (1986). These authors use Tobin´s Q Ratio, which is a market valuation tool that measures corporate growth opportunities, defined as the market value over the replenishment of the investment, establishing that those companies that present a QSIGNO1 evince over-investment (they invest in projects with a < 0 Net Current Value (VAN) and correspond to a free cash flow hypothesis. They find that in the case of dividend changes, the average return is higher for companies that present Q < 1, in other words, that the market reacts more strongly when the company is over-investing. Therefore, in the case of Q> 1, a dividend increase is a good sign, while in the case of Q< 1, a dividend reduction is a good sign. It is important to mention Vankatesh´s (1989) study when referring to the area of Impact of Dividend Initiation and the information contained in Profit Announcements and Volatility of Returns. This study determined that as an average, there is more information transmitted by profit announcement in the pre-dividend period than in the post dividend period, establishing that in the event of profit announcements, price reactions are lower in the post-dividend period as an average, independently from the fact that the announcement comes before or after the dividend announcement. It also establishes that share return volatility is lower in the postdividend period, which could be explained by reduced uncertainty on the conditions of the company. And, contrary to what happens in the predividend period, investors give less importance to information that is based on rumour, and lacks verifiable sources.

On the other hand, it is important to mention the Loderer and Maurer (1992) study, that refers to the possible relationship between a dividend payment and share issue. This study concludes that there is no relationship whatsoever between dividend payment and the issue of new shares, as these two facts generate different information. Dividends reflect expected cash flows, i.e. current and future profits, while share issue is the reflection of the price elasticity of the company.

Another important study is the Jensen, Solberg, Zorn (1992) paper that looks into common determiners in terms of insider ownership, debt and corporate dividends. In their study "Simultaneous Determination of Insider Ownership, Debt and Dividend Policies" they conclude that the debt, dividend and insider ownership of a firm are not only explained by their specific attributes, but are also directly related to each other. They also show that dividend payments are negatively correlated with the growth and investment opportunities of a firm, with their leverage level and insider ownership, the latter being coherent with the Free Cash Flow Hypothesis. It is also important to refer to the Smith and Watts study (1992), which covers the industrial area, averaging the data of individual companies chosen in each industry. The study concludes that companies with high growth opportunities present low leverage levels, low dividend profitability and high compensation levels. On the other hand, large companies have high dividend returns and high compensation levels. Finally, regulation generates high leverage levels, high dividend profitability, low compensation levels and a low frequency of incentive compensation plan utilisation.

Agrawal and Jayaraman (1994) verify the theory that both dividends and debt interest payments are mechanisms for reducing agency costs between administration and shareholders, because they reduce the free cash flows that the management may use at its discretion for its own pecuniary concumption and for investment in non-profit making projects. This argument is consistent with Jensen´s Free Cash Flow Hypothesis. It is also important to refer to the Yoon and Starks (1995) study, in which they look into the relationship between abnormal returns and Tobin´s Q ratio, considering control variables like changes in dividend payment, dividend performance and company size. Finally, they conclude that this relationship is non-existent, so that their results support the signalling hypothesis of Miller and Rock (1985).

In Chile, Maqueira and Guzmán (1997) investigated a sample of shares traded in the Stock Exchange, concluding the ex dividend share behaviour is determined by tax factors rather than by abnormal returns, and supports the hypotheses of a clientele effect on the domestic market, which is induced by the tax structure that rules local investors. Another important study is the Alaluf and de Río (1999) paper that looks into the effects of the reduction of Telefónica Chile dividend policy by 40% to 30% of its overall profits in 1998, concluding that the dividend cut did not produce significantly negative effects on the company´s share returns prior to the announcement. This study validates the signalling hypothesis developed by Miller and Rock (1985) that states that unexpected changes in dividend payments might lead to a review of expectations, which would mean eventual changes in share prices. The Telefónica Chile case shows that timely and appropriate information prevents the production of unexpected changes in a company´s share returns. Finally, Maqueira and González presented a paper in Chile in 2003 in which they studied 54 Chilean companies belonging to different industrial sectors over the 1996-2003 period. This study establishes the existence of a trend to use dividends as a mechanism for transmitting information to the market, and for transmitting its current and future flow expectations. The study concluded that Chilean administrators and managers behave in a way that is consistent with the signalling hypothesis. On the other hand, they determined that the variables that represent historical performance, as would be the case of past growth and corporate leverage, are consistent with Rozeff´s 1982 study regarding the influence of transaction cost on dividend decisions. This is inversely related to dividends in the sense that higher past growth and/or higher flows allocated to the fulfilment of fixed obligations resulted in the payment of smaller dividends as a way of not resorting to the capital market to satisfy expensive financing needs.

SECTION III

Data and methodology applied

A) Methodology: We will use a methodology based on a study of the processes applied in provisional and compulsory minimum definite dividends. We will not study eventual and additional dividends as they appear sporadically in these dividend processes. The objective of this exercise is to measure their impact on share returns in terms of the cut-off date for enrolling in the register of shareholders with a right to dividend payment. We will analyse these effects on compulsory minimum dividends and on provisional dividends, and compare the fall in share returns on the day after the cut-off ate, versus the increase in dividends on the cut-off date itself.

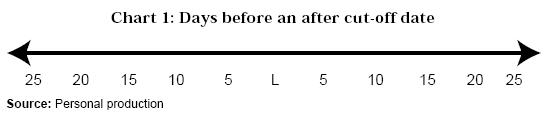

The determination of the 0 cut-off date is important, because after the last transaction carried out on that day it is impossible to gain access to dividend payment. We will furthermore analyse 25 correlative previous transactions, and 25 correlative subsequent transactions, in order to come to a conclusion regarding volatility before and after the cut-off date. (See Chart 1).

B) Description of the study: We will calculate the returns of each share over the entire period of the study, in order to obtain an aggregate graphic analysis for compulsory minimum definite dividends, and for provisional dividends that will give the average for the preceding days, for the cut-off date and for the days that follow the closure of the register of shareholders with a right to receive dividend payment.

We will also make an individual analysis according to company for both compulsory definite dividends and for provisional dividends.

C) Sample:

- The selection will only include dividend payments completed after 1/1/93.

- The selection will only include dividend payments prior to 31/12/03.

- The shares selected will have had a stock market presence of not less that 40%.

- We will select 152 compulsory definite dividend payments.

- We will select 152 provisional dividend payments.

- We will select shares that have evinced 6 or more dividend processes in the period under study.

D) Statistical Models: The following statistical models will be used to measure returns.

- Share returns for the interval that exists between one transaction and another is calculated as:

- We will calculate the average returns for the 152 compulsory definite dividend payments, and for the 152 provisional dividend payments. We will also calculate the average of each payment in the 25 transactions carried out before the cut-off distribution date and of the 25 transactions that followed the cut-off distribution date.

- The increase in the dividend paid per share is calculated on the basis of the last transaction during the closure date, and is the difference between the return (dividend included) and return (dividend excluded). This gives the division between the amount of the dividend and the price on the closure date.

where:

P i,t = The price of asset i in transaction t.

P i,t-1) = The price of asset I in transaction t-l

We will also calculate the average dividend payments for those shares that are contained in the sample of compulsory definite dividend payments and in the sample of provisional dividends. Average return is calculated as follows:

where:

Is the return of the N dividend payments in transaction t.

Is the return of the N dividend payments in transaction t.

N = Is the total number of observations

R i,t = Is the return of asset i in transaction t.

t = Is the transaction, which goes from (-25, 25).

E) Research Hypothesis: This piece of research has the aim of proving the following hypotheses:

- The fall in average share returns on the date after the cut-off date is larger than the average increase of the amounts of the compulsory minimum dividends on the cut-off date.

- It is highly probable that the fall of a company´s average share returns on the day after the cut-off date is higher than the average increase of compulsory minimum dividends on the cut-off date.

- The fall of average share returns on the day after the cut-off date is lower than the average increase in the value of provisional dividends on the cut-off date.

- It is highly probable that the fall of a company´s average share returns on the day after the cut-off date is lower than the average increase in the value of provisional dividends on the cut-off date.

- Volatility on the days that follow the cut-off date is higher than the volatility observed on the days prior to the cut-off date.

- It is highly probable that the volatility ratio betwen the days after the cut-off date/volatility prior to the dividend´s cut-off date is higher for compulsory minimum definite dividends than for provisional dividends.

SECTION IV

Analysis of results

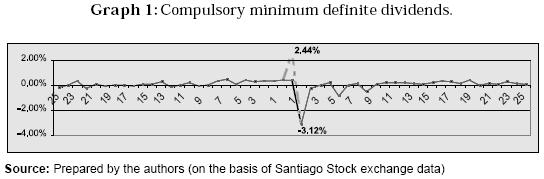

We calculated the returns of each share over the entire period of the study so as to obtain an aggregate graphic analysis containing 51 share returns. Each return is the average of 152 returns, both in terms of compulsory minimum definite dividends and for provisional dividends, and will give the average for the days before the closure of the register, for the closure date and for the days that follow the closure of the register of shareholders with a right to receive dividend payments. On the other hand, graphs of the returns were produced including (green line) and excluding the value of the dividend (blue line) in the last transaction on the closure date. This was carried out in order to see if the value of the dividend is in any way related to the fall of share return (red line).

We also analysed company results for compulsory minimum definite dividends over 10 years, and of the 152 dividend payments included, they affected 19 companies. In the case of provisional dividends, the 152 payments only included 6 companies as in Chile the ratio between provisional dividends and compulsory minimum dividends is 3:1, and would explain the difference in the size of the sample.

The two types of dividends analysed show reduced returns on the day after the closure of the register of shareholders with a right to receive dividend payments. This is caused by the fact that share prices reflect all the information available in the market. In other words, if the share is transferred prior to the closure date, in includes the dividend, while if the transfer occurs after closure, the share price will be lower because the share was transferred on its own, without its dividend, thus reflecting a balanced price.

This paper concludes that in the case of Chile, share returns after the closure of the register of shareholders with a right to receive share payments do not fall in the amount of the dividend, and magnitude will depend on the type of dividend. This is caused by the existence of the Clientele Effect in Chile, and it is caused by the fact that individuals pay different tax rates according to different types of income, capital gains or dividends, and for this reason they select those shares that have flows that enable them to minimise tax payments. Therefore, the existence of personal taxes makes people in the lower income brackets prefer high dividend paying shares.

Chile is a concentrated share market, and its most important feature is a high percentage of shares in the hands of shareholders that pay high tax rates, and who prefer shares that pay low dividends. This is the case of provisional dividends rather than compulsory minimum definite dividends, and can be explained by the fact that investors will maintain portfolios created to maximise return rates after tax. This leads investors to pay high tax rates per dividend, so they will prefer those shares with low dividend returns and higher capital gain returns. As an average, this implies that the market places a different value of flows received a capital gains and dividends.

Chart 1 shows that the average of the 152 10 year dividend processes corresponds to the distribution of compulsory minimum definite dividends. This proves one of the hypotheses of this paper, which is "Average share returns fall -3.12% on the day after the cut-off date. This is higher than the 2.44% average increase of compulsory minimum definite dividends at the cut-off date". This occurs because investors place a different market value on flows received as capital gain and as dividends. The reason for this is that the Chilean stock market has a high concentration of ownership that produces a higher percentage of shares in the hands of shareholders that pay high tax rates per dividend because they are in the higher tax brackets. These prefer shares that pay lower dividends (provisional dividends) rather than the high amounts involved in compulsory minimum dividends, which therefore produce an excess offer of shares, which leads to a fall of average share returns, which is higher than the average value of compulsory minimum definite dividends, as can be seen in Graph 1.

On the other hand, Graph 1 shows volatility and fulfils other hypotheses of this paper. On the days the follow the cut-off date, dividend volatility reaches 0.69%. This is higher than the 0.21% dividend volatility on the days prior to the cut-off date. This is caused by an excess offer the day after cut-off which makes prices plummet.

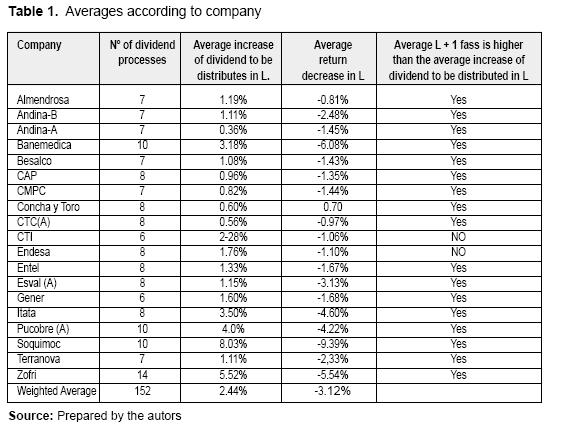

Table 1 shows averages according to company, and proves one of our hypotheses "It is highly probable that the fall of a company´s average share returns on the day after the cut-off date is higher than the average increase of compulsory minimum dividends on the cut-off date". We see that in the case of 17 companies, 89.5% of total average share return falls on the day after the cut-off date is higher than the fall of a company´s average share returns the date following the cut-off date.

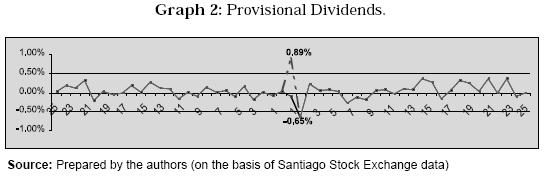

Graph 2 shows that the average of the 152 10 year dividend processes correspond to the distribution of provisional dividends. This proves one of the hypotheses presented in this paper. The fall of average share returns on the day after the cut-off date is -0.65%lower than the average 0,89% increase of provisional dividends on the cut-off date. This is caused by the fact that investors place a different value on flows received as capital gains and as dividends, because the Chilean stock market has a high concentration of ownership that producers a higher percentage of shares in the hands of shareholders that pay high tax rates per dividend because they are in the higher tax brackets and prefer shares that pay low dividends (provisional dividends) rather than shares that pay higher dividends (compulsory minimum dividends). The latter are preferred by shareholders that pay low tax rates and own fewer shares.

As provisional dividends result in a lower dividend, shareholders that have higher share percentages tend to prefer these dividends that have lower amounts than compulsory minimum definite dividends. The consequence of this is that the fall of average share returns is lower that the average increase in compulsory minimum definite dividends.

On the other hand, Graph 2 proves the volatility hypothesis presented in this paper. Provisional dividend volatility is 0.22% on the days that follow the cut-off date. This is higher than the 0.14% volatility rate seen on the days prior to the cut-off date, and is the result of an increase in transactions after cut-off date. On the other hand, when we compare the ratio: Volatility in the days that follow the cut-off date/volatility on the days that precede the cut-off date in the case of both kinds of dividends, we see that in compulsory minimum definite dividends the volatility ratio for the days after cut-off date/days prior to the cut off date is 3.28 higher than in provisional dividends, which have a ratio of 1.57, because in the case of compulsory minimum definite dividends there is an excess offer on the day after the cut-off date, which provokes a strong fall in share returns.

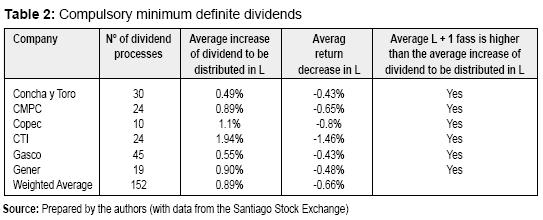

Finally, Table 2 shows the average per company in terms of provisional dividends, and we see that it proves our hypothesis "It is highly probable that the fall of a company´s average share returns on the day after the cutoff date is higher than the average increase of compulsory minimum dividends on the cut-off date". We see that in the six companies studied, the fall of average share returns on the day after the cut-off date is higher than the average increase of provisional dividends on the cut-off date.

SECTION V

Conclusions

The results of this study generate different conclusions regarding the effects that different dividends have on share returns. There is no doubt whatsoever that the high volatility seen around the cut-off date is valid evidence of the existence of the Clientele Effect in Chile, which is reflected in the fact that investors change their stance, according to their tax preferences, and provoke a different effect on share returns for provisional dividends or for compulsory minimum definite dividends.

Chile is a concentrated share market, and in the past 10 years its most important feature is a high percentage of shares in the hands of shareholders that pay high tax rates, and who prefer shares that pay low dividends. This is the case of provisional dividends rather than compulsory minimum definite dividends, and can be explained by the fact that investors will maintain portfolios created to maximise return rates after tax. This leads investors to pay high tax rates per dividend, so they will prefer those shares with low dividend returns and higher capital gain returns. As an average, this implies that the market places a different value on flows received as capital gains and as dividends.

On the other hand, the market considers that the distribution of provisional dividends on the part of companies to be positive, because the company is capable of generating positive profits and will later be able to produce the definite dividend established by law, which amounts to 30% of its liquid profits.

The following are the specific results of this paper, which prove its hypotheses:

- Average share returns fall -3.12% on the day after the cut-off date. This is higher than the 2.44% average increase of compulsory minimum definite dividends at the cut-off date.

- In 89% of the cases analysed, the fall of average corporate share returns the day after cut-off date is higher than the average increase of compulsory minimum definite dividends on the cut-off date.

- The fall of average share returns the day after the cut-off date is - 0.56% lower than the average 0.89% increase in the amounts of provisional dividends at the cutoff date.

- 100% of the fall of a company´s average share returns on the day after the cut-off date is lower than the average increase in provisional dividends on the cut-off date.

- 25 days after the cut-off rate, compulsory minimum definite dividends have a volatility of 0.69%, which is higher than the 0.21% volatility rate during the 25 days before the cut-off date.

- 25 days after the cut-off rate, provisional dividends have a volatility of 0.22%, which is higher than the 0.14% volatility rate during the 25 days before the cut-off date.

- The following is the ratio for compulsory minimum definite dividends: volatility after the cut-off date/volatility prior to the cut-off date is 3.28% higher than in provisional dividends, which show 1.57%, This results from the fact that compulsory minimum definite dividends produce an excess offer the day after the cut-off date, which make share returns plummet.

Finally, it is important to note that the existence of the clientele effect on a determined market does not mean that this should become similarly apparent in other markets, because tax structures vary according to countries, making results completely different from one country to another.

For this reason, it would be interesting to undertake a similar study in another country so as to contrast results.

BIBLIOGRAPHY

Asquith, P. & Mullins, D. (1983) "The impact of initiating dividend payment on shareholders´ wealth" Journal of Business 56 (1): 77-96. [ Links ]

Barclay, M. (1987). "Dividends, taxes and common stock prices; The ex dividend day behaviour of common stock prices before income tax". Journal of Finance 31-44. [ Links ]

Copeland, T., Koller, T. & Murrin, J. (2000) Valuation: Measuring and Managing the value of companies. New York: John Wiley & Sons. [ Links ]

Gaver, J. & Gaver, K. (1993). "Additional evidence of the association between the investment opportunity set and corporate financing dividend, and compensation policies".Journal of Accounting & Economics 16:125:129. [ Links ]

Guzmán, J.P. y Maqueira, C. (1997). "Presencia del Efecto Clientela en el mercado chileno". MA Thesis in Finance. Santiago de Chile: University of Chile. [ Links ]

Jensen M.C., & Meckling, W. (1976). "Theory of the firm Managerial Behaviour,agency costs and ownership structure", Journal of Financial Economics 3. 305-360. [ Links ]

Jensen, M.C. (1986) "Agency costs of free cash flow, corporate financial and takeovers". The American Economics Review 76 (2): 323-329. [ Links ]

Lang, L. & Litzenberger, R. (1989). "The effect of personal takes and dividend on capital asset prices", Journal of Financial Economics 24 (1): 181-191. [ Links ]

Litzenbergerr, R. & Ramaswamy, K. (1979). "The effect of personal takes and dividend on capital asset prices", Journal of Financial Economics 7: 163-194. [ Links ]

Lease, Ronald, C. (2001). "Política de dividendos y sus efectos en el valor de la firma". Boston: Harvard Business School Press. [ Links ]

Maqueira, C. & Fuentes, O. (1997). "Política de dividendo en Chile, 1993 y 1994". Estudios de Administración, Volumen 4 Número 1: 79-112. [ Links ]

Miller, M. & Rock, K. (1985). "Dividend Policy under Asymmetric Information" Journal of Finance 40: 1031- 1051. [ Links ]

Moncayo, E. (2003). "Factores que inciden en la política de dividendo en Chile". MA Thesis in Finance, Santiago de Chile: University of Chile. [ Links ]

Venkatech, P. (1989). "The impact of dividend initiation on the information content of earnings announcements and return volatility". Journal of Business 62 (2): 175-197. [ Links ]

Ross, Stephen, A. (2002). "Finanzas Corporativas" Sexta Edición. México: Irwin McGraw-Hill. [ Links ]

Yoon, P. & Starks, L. (1995) "Signalling, investment opportunities, and dividend announcements", The Review of Financial Studies 8 (4): 995- 1018. [ Links ]