Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Citado por Google

Citado por Google  Similares em

SciELO

Similares em

SciELO  Similares em Google

Similares em Google

Permalink

Permalink1. Introduction

The focus of leadership theory developed in the 1970s is the relationship that leaders develop with their subordinates (Niemeyer & Cavazotte, 2016). The theory of leadership styles as well as the attitudes and behaviors of individuals in response to leadership style have been developed and tested in the US and other developed countries (Yukl, 1989). The core of their approach is that leadership is a process as a result of interaction between leaders and subordinates. The relationship between the leader and the followers can vary according to the degree of respect, trust and support (Niemeyer & Cavazotte, 2016).

From this perspective, leadership theory assumes that the leader behavior has profound effects on subordinates (Bass, 1990). There is a link between the personality of managers and leaders and the management model of their organizations (Bianchi, Quishida & Foron, 2017). The leader plays an essential role that can encourage subordinates to participate in organizational processes. According to Dunk (1993) and Li, Nan and Mo (2010), without adequate incentives for effective communication, some benefits may not be perceived or missed. Young (1985), Shields and Young (1993) and Kyj and Parker (2008) explain that incentives to participate in the budget should occur only if the subordinate is free to establish a reward estimate without undue pressure or interference from senior management.

The management control procedures frequently used in organizations involve the participation of managers and their subordinates. Of these, the budgetary participation is highlighted (Silva & Gomes, 2010). Budget participation is defined as an administrative process in which a subordinate is involved and has influence over the determination as well as the budgeting (Covaleski, Evans, Luft & Shields, 2006; Shields & Shields, 1998; Milani, 1975).

The budget is one of the widely researched topics in managerial accounting (Luft & Shields, 2003), and budget participation is an emerging theme in the behavioral approach to accounting (Birnberg, Luft & Shields, 2006). According to Covaleski et al. (2006) and Buzzi, dos Santos, Beuren & de Faveri (2014), researchers have noted the importance of the budget and have conducted research related to the topic, but the results have been conflicting. In this context, the purpose of this study is to evaluate the relationship between leadership style, the incentive to budget participation and budgetary participation of controllers with budgetary responsibility in companies operating in Brazil. The problem question that guides the research is: what is the relationship between leadership style, incentive participation and budget participation of controllers?

The basic paradigm to evaluate the history of the use of the participation in the budget is presupposed that all action is triggered by the anticipated accomplishment of the objectives of the entity (Mahlendorf, Schäffer & Skiba, 2015). Understanding leadership is one of the oldest human tasks. For Carvalhal and Muzzio (2015) it was around 2,300 before Christ (BC) that the Egyptians recorded the first writing on the subject. From the nineteenth century, leadership studies were systematically organized. Currently, there are numerous approaches, perspectives, and recurrent definitions of leadership (Azevedo, 2002). Among the pieces of evidence found in research on the subject, there is a consensus among scholars that leadership reveals the influence of the leader over the subordinates (Almada & Policarpo, 2016; Carvalhal & Muzzio, 2015).

The studies on the topic of leadership have been important to organizations (Loiola & Bastos, 2003; Mulki, Caemmerer & Heggde, 2015) since an appropriate leadership style is a decisive strategy for companies to achieve innovation and competitiveness. The leadership style has been investigated as the behavior of the leader in the context of the work capable of being modified in the perspective of training (Azevedo, 2002). The leader is a change agent who strives for a balance in the conduct of his work activities in order to influence the subordinates to reach the established goals.

It is from this perspective that the topic of leadership in this research is addressed, seeking to observe the effects of the leader’s behavior as an antecedent element to the participation of subordinate managers in the budget processes, a convergent approach adopted by Kyj and Parker (2008) and Otley and Pierce (1995). In this way, this study seeks to provide from its results important contributions for organizational behavior and literature on budget participation and leadership style. By perceiving the reasons superiors encourage participation in the budget, it is possible to understand the causes of subordinate participation. In addition, it is possible to verify how participation affects the relationship between superior and subordinate (Kyj & Parker, 2008).

To investigate the proposed relationships, a questionnaire was applied to 316 controllers in Brazilian companies. Structural equations were used to statistically evaluate the hypotheses. In relation to leadership style, incentive budget participation and budget participation, statistical results reveal a positive and significant association between leadership style and the incentive of budget participation, and the incentive of budget participation, in turn, is significantly associated budget participation.

The findings suggest that when superiors encourage budget participation, subordinates are more likely to participate in budgeting; however, when the incentive to budget participation does not occur, subordinate budget participation is mitigated. In this way, budget participation can demonstrate the superior’s leadership style.

This article is structured in five sections: the first comprises the introduction of the research. In the second one, the antecedents and hypotheses of the research are presented. The third section describes the method used. Then, the results of the model tested are demonstrated. Finally, in the fifth section, the conclusion of the study is verified.

2. Theoretical framework

Theorists approach leadership as a collective process. In a group, there is usually one person who has greater influence and carries out some leadership functions (Niemeyer & Cavazotte, 2016). Yukl (1989) emphasizes that some theorists limit the definition of leadership to an exercise of influence of an individual resulting in the commitment of followers.

Leadership theory shows that leader behavior has profound effects on subordinates, even as they relate to their leaders as well as to each other (Bass, 1990). The core of this approach is that leadership is a process, because of interaction between leaders and subordinates. In this way, the relationship between the leader and the followers can become a high level of a partnership through the degree of respect, trust and support exchanged between them (Niemeyer & Cavazotte, 2016).

Brownell (1981) has shown that the superior’s leadership style is directly linked to budget share. According to Milani (1975), budget participation is a concept used to delineate the extent to which a subordinate can define his course of action, and this design may generate certain types of human reactions. Appropriate leadership styles and human resource practices that drive engagement between the superior and the subordinate need to be promoted in organizations to drive managerial performance (Popli & Rizvi, 2016).

Under the budget context, as Kyj and Parker (2008) and Yukl (1989) point out that a leader can use budget participation incentives to accurately and clearly reach the role of his subordinates in the organization. Superiors encourage budget participation for a variety of reasons, among which Kyj and Parker (2008) emphasize motivating open and communicative relationships, and access to private information that is under the power of subordinates. Studies in managerial accounting have examined how the leader’s incentive affects the subordinate’s individual effort (Tuttle & Burton, 1999).

According to Fleishman and Harris (1962, 1998), managers who respect subordinates and develop with these relationships based on trust and open communication are likely to encourage subordinates to participate during the budget process (Kyj & Parker, 2008). Business leaders engage in opportunity-focused activities. Thus, their involvement makes them influence their subordinates, motivating them and encouraging them in management processes and business standards.

Kyj and Parker (2008) and Brownell (1982) propose that leadership style positively influences the subordinate’s incentive to participate in the budget. In this way, the first hypothesis of the research is to verify the influence of the leadership style on the incentive of the subordinates’ budgetary participation:

Budgetary participation provides opportunities to influence the budget, from the time leaders assume more active roles in budget participation (Kren, 2003). For Harrison and Lock (2004), the effect of a superior leadership style on budget participation is an important issue to be considered in managerial accounting.

The results of researches conducted by Popli and Rizvi (2016), Niemeyer and Cavazotte (2016), Otley and Pierce (1995) and Fleishman and Harris (1962), presented significant relationships between leadership style and individuals’ participation in the budget process. The role of the leader and his/her leadership styles are very important to reach goals (Kasiati & Minarsih, 2015), and the participation of subordinates is seen as a key strategy for organizational success (Popli & Rizvi, 2016).

In this research, considering the predominant evidence found in the previous revisited studies, it is suggested that leadership style positively influences budgetary participation. Thus, the second research hypothesis consists of:

Supervisory leadership style is an important variable, according to Brownell (1983), because superiors tend to use budgets as a means of expressing their style of leadership (Argyris, 1952). Kyj & Parker (2008) and Brownell (1983) suggest that leadership style can interact significantly with the design features of the budget system.

According to Magner, Welker and Campbell (1996) subordinates have intimate knowledge of their own work, so such information can result in a budget that is a more accurate representation of future circumstances in the workplace. Budgetary participation allows managers to communicate or disclose some of their private information which can be grouped into budgets (Dunk, 1993). Thus, budget participation strengthens the quality of the budget as it provides subordinates with an opportunity to communicate private and relevant information in budget decisions (Kyj & Parker, 2008; Parker & Kyj, 2006).

Employee engagement with the superior’s leadership style can be transformed into a subordinate with commitment to the organization (Wong-On-Wing, Guo & Lui, 2010). In this way, the leadership style will help to coordinate work routines and will cause the exchange of information between superior and subordinate, which demonstrates a positive relationship between superior leadership style and budget participation. Lau, Low and Eggleton (1997) and Brownell (1983) demonstrated in their studies, evidence of positive relationships between leadership style and budget participation. However, the study by Kyj and Parker (2008) did not identify a direct interaction between leadership style and participation in the budget.

The research by Kyj and Parker (2008) revealed a positive and significant association between the incentive to participate in the budget and the participation in the budget. Given the findings of these studies, it is proposed that participation incentives increase attendance levels in the budget process, which suggests a positive relationship between these variables.

Thus, the third research hypothesis investigated seeks to verify the influence of the incentive in the participation of the budget in the process of budgetary participation of subordinates:

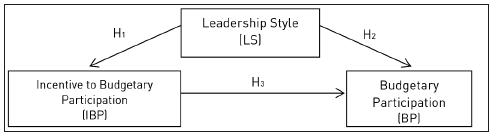

Brownell (1982) points out that participation in the budget is a process that individuals are involved and have influence in regarding the definition of budgets. In this sense, high budget participation includes frequent and comprehensive discussions between the superior and his subordinates over the budget (Milani, 1975). In organizations, Parker and Kyj (2006) and Simons (1995) point out that subordinates who have an interactive dialogue with superiors can reveal important information about strategic uncertainties. The theoretical model analyzed in this research is presented in figure 1, which shows the possible links between the analyzed variables.

3. Methodological procedures

The methodology used in this research is descriptive. For data collection a survey was used. Regarding the approach to the problem, it is a quantitative study. The quantitative approach uses both the quantification of the modalities and data collection applied in the research, as well as the treatment through statistical techniques (Raupp & Beuren, 2006). In this perspective, for the accomplishment of this study, the investigation of the analyzed variables is performed from the technique of modeling by structural equations.

The population that is the object of this research consists of professionals responsible for controlling companies that operate in Brazil with budgetary responsibility in the organizations in which they operate. In a survey carried out with the Linkedin business network, professionals with such characteristics were identified, with functions denominated as controllers, controller managers and controller coordinators. The economic sectors that constituted the sample of the study are of several segments. Thus, the choice of these companies was given in order to comprehensively investigate the behavior of individuals with such a position in the budgetary processes adopted in the Brazilian context.

These procedures are convergent to those adopted in other studies developed under the behavioral approach of accounting, which also analyzed the budget context with companies from different segments (Kren, 1992; Lau et al., 1997; Chong & Chong, 2002; Chong, Eggleton & Leong, 2005; Kyj & Parker, 2008; Zonatto, 2014).

The definition of the population of this research was established from the identification of the companies in operations in the country that have managers with such functions. This population was chosen because the controllers assumed different positions in different companies, which makes them a strategic piece within the organizations, since they are the professional given to have excellence in the information generated in the organizations (Siqueira & Soltelinho, 2001). The sample was defined by individuals with budgetary responsibility and that used Linkedin. For the accomplishment of the research 1985 individuals with budgetary responsibilities were contacted, of these 852 accepted the invitation to answer the research instrument. After accepting the invitation, the questionnaires were sent. Three hundred and sixteen fully completed the research instrument, producing a response rate of 37.08%. 75% of the respondents described themselves as controllers, 12.66% as controllership managers and 12.34% as controllership coordinators. In addition, respondents described themselves with a high level of hierarchy in companies.

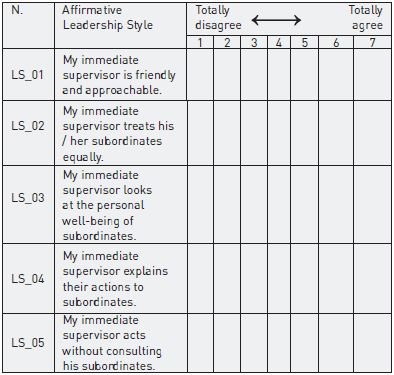

For data collection, a questionnaire (see annexes) was developed with questions about the leadership style variable that was measured using an adapted version of the Leader Behavior Description Questionnaire (LBDQ, Form XII) developed by Stogdill (1963). The LBDQ has ten items that measure the superior’s consideration of subordinates. The version used for the research instrument was adapted from the study by Kyj and Parker (2008), which contain five indicators. The LBDQ represents one of the most used measures of leadership style in the organizational behavior literature (Kyj & Parker, 2008). The instrument used establishes that an attentive, inclusive style of leadership capable of promoting subordinate participation in management processes is capable of positively influencing the behavior of individuals in the organization.

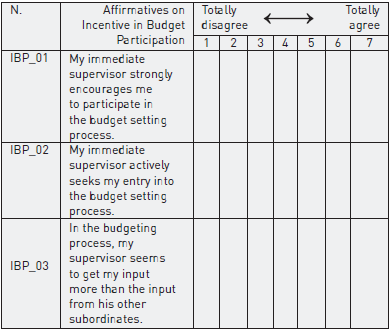

The variable of incentive to subordinate participation in the budget process measures how superiors seek to encourage subordinates to participate in the budget process. This instrument was adapted from the study by Kyj and Parker (2008) and was measured with a scale of three items.

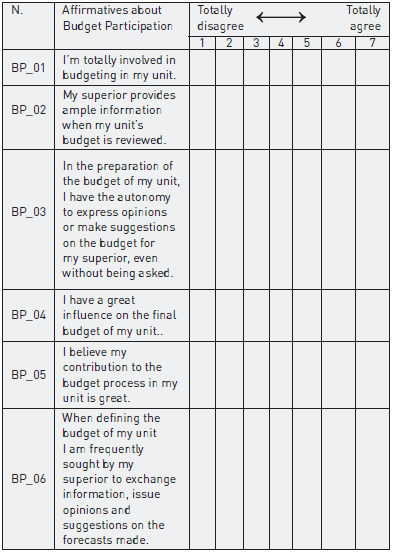

To identify the variable budget participation, the instrument of six items of Milani (1975) was adapted, which tries to evaluate the involvement and influence that an individual has in the budget process. This instrument has been widely used in the behavioral area of accounting, as in Mia (1988), Dunk (1993), Lau and Lim (2002), Chong and Chong (2002), Chong et al. (2005), Parker and Kyj (2006) and Zonatto (2014).

Since the level of analysis in this research focuses on individuals, from the definition of the minimum number of controllers participating in the study, the use of structural equation modeling was adopted to evaluate the theoretical relations observed. Hair Jr., Anderson, Tatham and Black (2005) present that for the use of structural equations a number of five respondents is necessary per indicator analyzed in the model. This minimum number of respondents was observed in this study. The results are presented below.

4. Analysis of results

For the descriptive analysis of the results found, the real interval (minimum and maximum), mean, standard deviation, variance, asymmetry and kurtosis were initially evaluated. Then, individual analysis of each construct was carried out from the results of the Exploratory Factor Analysis, so that the grouping of the indicators of each construct in its respective measurement construct could be evaluated, which contributes to evaluating its predictive capacity of measurement. The Kaiser-Meyer-Olkin (KMO) sample adequacy measure, Bartlett’s sphericity test, total variance explained, factorial load, and commonalities were evaluated in this stage of the research. The reliability of each construct was investigated by Cronbach’s alpha coefficient. Table 1 presents a summary of the results of the descriptive statistical analysis and exploratory factorial analysis of the theoretical construct of leadership style.

Table 1 Descriptive statistics and constructive exploratory factor analysis style of leadership

| CA | KMO | TEB | TVE | Ind. | TI | RI | Med. | SD | AS | CT | CF | Com. |

| Leadership Style (LS) | ||||||||||||

| 0.84 | 0.84 | 946.3 (0.00) | 66.26 | LS01 | 1-7 | 1-7 | 5.69 | 1.58 | 1.37 | 1.28 | 0.87 | 0.76 |

| LS02 | 1-7 | 1-7 | 5.19 | 1.85 | 0.93 | 0.19 | 0.89 | 0.80 | ||||

| LS03 | 1-7 | 1-7 | 5.14 | 1.79 | 0.84 | 0.29 | 0.90 | 0.82 | ||||

| LS04 | 1-7 | 1-7 | 4.79 | 1.80 | 0.59 | 0.63 | 0.88 | 0.79 | ||||

| LS05 | 1-7 | 1-7 | 3.51 | 1.91 | 0.285 | 1.02 | 0.35 | 0.12 | ||||

| Incentive to Budget Participation (IBP) | ||||||||||||

| 0.85 | 0.64 | 614.1 (0.00) | 79.08 | IBP01 | 1-7 | 1-7 | 6.09 | 1.28 | -1.73 | 2.95 | 0.92 | 0.85 |

| IBP02 | 1-7 | 1-7 | 6.11 | 1.26 | -1.78 | 3.25 | 0.94 | 0.89 | ||||

| IBP03 | 1-7 | 1-7 | 5.50 | 1.57 | -1.02 | 0.49 | 0.79 | 0.62 | ||||

| Budgetary Participation (OP) | ||||||||||||

| 0.85 | 0.83 | 865.2 (0.00) | 60.06 | BP01 | 1 - 7 | 1 - 7 | 6.49 | 1.07 | -2.78 | 8.71 | 0.81 | 0.66 |

| BP02 | 1 - 7 | 1 - 7 | 5.75 | 1.43 | -1.20 | 1.05 | 0.61 | 0.37 | ||||

| BP03 | 1 - 7 | 1 - 7 | 6.44 | 0.99 | -2.50 | 7.92 | 0.79 | 0.63 | ||||

| BP04 | 1 - 7 | 1 - 7 | 6.10 | 1.24 | -1.72 | 3.20 | 0.80 | 0.64 | ||||

| BP05 | 1 - 7 | 1 - 7 | 6.42 | 0.97 | -2.58 | 8.91 | 0.83 | 0.69 | ||||

| BP06 | 1 - 7 | 1 - 7 | 5.97 | 1.31 | -1.63 | 2.63 | 0.76 | 0.58 | ||||

Legend: AC. Cronbach’s Alpha; KMO: Kaiser-Meyer-Olkin; TEB. Bartlett’s Sphericity Test; TVE. Total Variance Explained; Ind. Indicator; TI. Theoretical Interval; RI. Real Interval; MED: Medium. SD. Standard Deviation; AS Asymmetry; CT. Curtose; CF. Factorial load; Com. Communality.

Source: own elaboration.

The established KMO value is 0.50 and the leadership style variable presented a value higher than that (0.848). The Bartlett’s Sphericity Test showed statistical significance of (p <0.05). The commonalities of the indicators demonstrated the achievement of the minimum criteria established, with the exception of LS05, which indicates that this indicator may be a candidate for exclusion at the stage of the confirmatory factor analysis of this construct. At this stage of the research, we opted to keep the variable in the analysis in the face of the results achieved in the other tests performed.

The results evidenced in the statistical descriptive analysis for the leadership style construct show differences between the leadership styles of the controllers’ superiors. This highlights the opportunity to analyze leadership style as a precedent to participation in the budget context.

In this context, superior leadership style is an important variable because, as Argyris (1952) pointed out, superiors tend to use budgets as a means of expressing their leadership style, suggesting that leadership style can interact in the characteristics of design of the budgetary system. Based on leadership theory, Kyj and Parker (2008) propose that some superiors encourage participation by demonstrating their leadership style. Fleishman and Harris (1998) emphasize that superiors encourage participation to build a relationship with their subordinates with characteristics of trust, respect and support. Likewise, as Kyj and Parker (2008) explain, superiors can foster budget participation to create an atmosphere of equality.

Regarding the results of the exploratory factorial analysis for the incentive construct for the budget participation, it was verified that the Cronbach alpha as well as the KMO reached values higher than the one recommended by Hair Jr. et al. (2005). Bartlett’s Sphericity Test showed a significance of 0.05 and total explained variance of 79.08%. Regarding the factorial load of the constructs, all the indicators remained, since in addition to grouping in their factor, they presented loads superior to the recommended minimum ones.

The budget participation construct presented a chrombach alpha of 0.853. The total variance explained resulted in 60.06%, indicating a reliability as indicated by Hair Jr. et al. (2005). All the indicators presented an appropriate factorial load for the maintenance of these in the construct of budgetary participation. The indicators reached minimum and maximum responses on the scale used. These results reveal that, although being considered high, in most cases, the hierarchical level of the controllers participating in the study, the levels of budgetary participation differ in their organizations.

In this construct, it was observed from the descriptive statistical analysis that the levels of budgetary participation differ among the participants of the research, which suggests that in some organizations the controllers do not perceive their influence in the budgetary process of the organization in which it is inserted. These results reinforce the pertinence of observing the theoretical relations investigated in the research, since different levels of budgetary participation help in understanding the different effects of these levels analyzed on the managerial performance.

The results evidenced for asymmetry and kurtosis show that the distribution of data is normal. Table 2 presents the reliability indices of the measurement constructs and the analysis of their discriminant validity.

Table 2 Reliability indicators of measurement constructs

| Constructs | Cronbach Alpha (CA) | Compound Validity (CV) | Extracted Variance (AVE) |

|---|---|---|---|

| Minimum Expected Values => | > 0.70 | > 0.50 | > 0.50 |

| Leadership Style (LS) | 0.84 | 0.92 | 0.74 |

| Incentive to Budget Participation (IBP) | 0.85 | 0.88 | 0.72 |

| Budgetary Participation (BP) | 0.85 | 0.87 | 0.52 |

| Discriminant validity by the criterion of Fornell and Larcker (1981) | |||

| LS | IBP | BP | |

| LS | 0.74 | ||

| IBP | 0.15 | 0.72 | |

| BP | 0.07 | 0.62 | 0.52 |

Source: own elaboration.

The results show that the reliability indicators are higher than the recommended minimum values, which indicates the validation of the constructs. The discriminant validity analysis, developed on the basis of the Fornell and Larcker (1981) analysis model, established that the variances extracted from the measurement constructs, when compared to the shared variance (Eberle, Milan & de Matos, 2016), are greater, which confirms the discriminant validity of the measurement constructs.

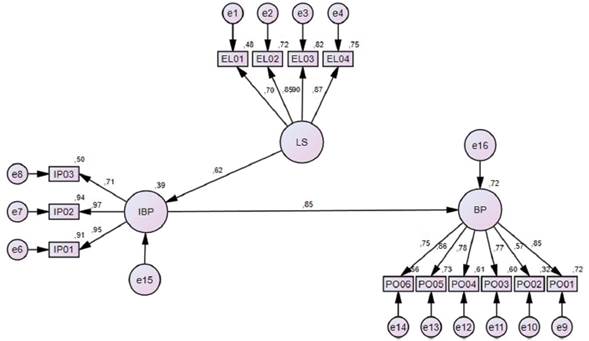

This validation then sought to investigate the relationship between the constructs that seek to respond to the objective of this study, consisting of identifying the relationship between leadership style, incentive to budget participation and budget participation of controllers with budgetary responsibility in companies that operate in Brazil. Figure 2 presents the results of the path estimates of the final measurement model found in the analysis of such relationships.

In the initial measurement model, leadership style (LS) was composed of five indicators. The indicator that evaluates whether the immediate supervisor acts without consulting the subordinates (LS_5) was excluded from the initial measurement model since its factorial load was only 0.24. Thus, the final model of measurement of this construct is represented by four indicators. The other initial models of construct measurement, incentive to budget participation (IBP) and budgetary participation (BP) remained unchanged, being composed respectively by three and six indicators. The values evidenced from the confirmatory factorial analysis show that all the remaining indicators in this structural model reached factor loads higher than 0.5, these being statistically significant. The results of the adjustment indexes of the final version of the first structural model used in the research are presented in table 3.

Table 3 Measurement model adjustment indices

| Indicator | Expected Value | Purified Final Model |

|---|---|---|

| Qui2 | - | 345,80 |

| Degree of Freedom (GL) | - | 64 |

| Qui2/ Degree of Freedom (GL) | <5 | 5 |

| Statistical significance (P) | p < 0.05 | 0,000 |

| Comparative Fit Index - CFI | > 0.90 | 0,897 |

| Tucker-Lewis Index-TLI | > 0.90 | 0,875 |

| Normed Fit Index - NFI | > 0.90 | 0,877 |

| Goodness of fit Index- GFI | > 0.90 | 0,850 |

| Goodness of fit Quality - AGFI | > 0.90 | 0,787 |

| Root Mean Square Error of Approximation - RMSEA | < 0.10 | 0,118 |

Source: own elaboration.

Analyzing the results shown in table 3, one can observe that the index of adjustment of the model presented an index of 5, being significant at p <0.000. The Comparative Fit Index - CFI (0.897) presented a value close to that expected (0.90), as well as the Tucker-Lewis (TLI) (0.875), Normed Fit Index (NFI) (0,877) and RMSEA (0.118).

In this way, it can be verified from the analysis of the adjustment indices of the final version of this structural model, that the constructs leadership style (LS), incentive participation (IBP) and budget participation (BP) can be confirmed, which allows the evaluation of the relations observed in it. Table 4 presents the standardized coefficients and significance of the relationships found in the final analysis model of such relationships.

Table 4 Standardized coefficients and significance of the relationships of the model tested

| Structural Pathways | Estimate | E.P | t - values | p | Coef. Standardized | R2 | ||

|---|---|---|---|---|---|---|---|---|

| IBP | ← | LS | 1 | - | - | - | 0,647 | 0,418 |

| BP | ← | LS | - | - | - | - | - | - |

| BP | ← | IBP | 0,546 | 0,02 | 18,62 | 0,000 | 0,859 | 0,738 |

Note 1: results of the purified model. Path between LS and BP excluded (not significant).

Note 2: path between IBP and LS fixed and t-values not calculated.

Source: own elaboration.

In order for the relationships investigated to be accepted, from the hypothesis test the results found for the t-values must be greater than 1.96, a tolerable acceptance value, (Hair Jr et al., 2005). Table 4 shows the relationship between the IBP ← LS path that had its values set at 1.00, thus the t-values were not calculated. In the relation between the BP ← LS path, the t-values found in the first evaluated model presented a value lower than 1.96. Thus, it can be inferred that the relationship between these variables did not present statistical significance. The relation between BP ← IBP presented t-values higher than the recommended one, which shows the existence of a significant relation between these constructs.

It table 4 it can be seen that there is no statistically significant positive relationship between leadership style factors and the subordinate’s participation in the budget. The path between the leadership style and the incentive to budget participation presented a positive and statistically significant relationship of λ = 0.647 to ρ <0.000. The incentive to budget participation is the variable that exerts influence among the determinants of budgetary participation. The path between participation incentive and budget participation showed λ = 0.859 and a R2 coefficient of <0.738.

By verifying the influence of the antecedents of the budgetary participation, leadership style and incentive to the budgetary participation, the evidence found in the literature is proven. In this way, it is possible to affirm that leaders with an attentive style of leadership are able to promote the participation of the subordinates in the tasks related to the budget, which confirms the first investigated hypothesis: H1: the style of leadership is positively associated to the incentive to budget participation.

Kyj and Parker (2008) demonstrate a direct relationship between leadership style and budget incentive participation. The superiors encourage the budgetary participation of the subordinates to promote open relations and have access to information maintained by the subordinate (Kyj & Parker, 2008).

The findings indicated that the leader’s style does not directly influence the subordinate’s participation in the company budget, which does not confirm the second research hypothesis: H2: leadership style is positively associated with budget participation. The results of this stage of the research demonstrated that the incentive of subordinate budget participation influences the participation in the budget, which confirms the third hypothesis investigated in the study H3: the incentive in participation is positively associated with the budgetary participation. Likewise, they indicate that leadership style indirectly influences budget participation by encouraging participation.

In this research, leadership style did not directly influence the participation of the subordinate in the elaboration of the budget. The findings of Kyj and Parker (2008) are similar to the results of this research. For Wong-On-Wing et al. (2010), Kren (2003), Lau et al. (1997), Brownell (1983) and Argyris (1952) budget participation generates opportunities for individuals to influence the budget, as leaders take on more active roles in the organization. However, Milani (1975) points out that the superior, in selecting his own actions, determines how this will influence the relationship with the subordinate’s participation in the company’s budget process.

The analysis of the effects of antecedents to budget participation was investigated in this study by variables, leadership style and incentive to budget participation. The findings of this research demonstrate that leadership style does not directly influence the participation of controllers in the budget process of the organizations in which they operate. Leadership style influences positively and significantly the incentive for controllers to participate in the budget process. As a consequence, the incentive to participate has a positive and significant influence on the effective participation of these professionals in the budgetary processes of their organizations.

These findings reveal that by supporting controllers in their management activities by encouraging them to participate in the budgeting processes of the firms in which they operate, their superiors contribute to the creation of conditions for greater participation of controllers in the budget process. Thus, these professionals are more likely to share relevant information with the budget process, qualifying the established forecasts. In this way, by perceiving their influence on the budgeting of their unit, controllers tend to be more involved with the organization, being willing to undertake greater effort to reach the established objectives.

Thus, under the behavioral perspective of leadership theory, the effects of the leader’s actions on the behavior of the subordinate managers are confirmed. As advocated by Yukl (1989), by being considerate and approachable, treating his subordinates equally, as well as verifying the well-being of his subordinates by providing information and adequately explaining his actions, the leader tends to captivate and influence the actions of their subordinates.

In this research, this influence occurs when the leadership style has a profile that strongly encourages the participation of controllers in the process of budget definition and actively seeks the input of the subordinate in the budget process. Therefore, the incentives made by the leader to his subordinates are the most influential factor for the controllers to participate actively in the budget processes.

5. Final considerations

This study aimed to evaluate the relationship between leadership style, the incentive to participation and budget participation of controllers working in Brazil. In order to respond to the objective, a descriptive research was carried out by means of a survey and a quantitative approach to data analysis. The research sample consists of 316 respondents with budgetary responsibility in Brazilian companies. The individuals participating in the study act as controller, manager controller or controllership coordinator.

The theoretical relations investigated in this research were tested using the modeling technique of structural equations. The antecedents of the budgetary participation were evaluated by the leadership style constructs and incentive in the budgetary participation. The results show a strong relationship between the leadership style and the incentive to participate in the budget. However, there was no direct relationship between leadership style and budget participation. A positive and statistically significant relationship was found between incentive participation and participation in the budget.

These results reveal that most survey participants perceive the supervisor as accessible, who treats their subordinates equally, caring about the personal well-being of subordinates. Likewise, they act to explain their actions and act by consulting their employees, including them in the management processes. As a consequence, they adopt a posture of encouraging the participation of these individuals in the budgetary processes of their organizations. Under these conditions, these subordinate managers tend to feel part of the budget processes of the organization in which they operate and perceive their influence on the organization’s budget processes. This participation allows the adjustment of budgetary objectives and targets, as well as the adequate allocation of resources, in order to enable the development of the activities of each unit of work, in order to ensure the achievement of better performance.

Based on the findings of this research, it is noticed that the more companies encourage their subordinates to participate in the budget activities, the better the participation of the individual in this process, since subordinates will have a greater influence in the definition of budgets. Similar results were identified in the study by Brownell (1982), demonstrating a positive relationship between the incentive to participation and the budgetary participation of subordinates in the organization.

The findings of this research contribute to the advancement of existing knowledge on the topics addressed. The evidence found revealed the previous effects of budget participation (leadership style and incentive participation) as determinant attributes for a better participation of the controllers of companies operating in Brazil in the budgetary processes of their organizations. These results corroborate with the evidence on the effects of the leader’s actions on the behavior of his subordinates in the budget context.

From this study, it was possible to verify some opportunities for the accomplishment of different research under the behavioral approach in the area of accounting. From the perspective of leadership, these results reveal the specific effects of the leader’s actions as a history of budgetary participation, as well as the consequent effects of their decisions on whether or not to encourage the participation of controllers in budget processes. Hence, understanding its effects on controller attitudes and behaviors in this context also constitutes an opportunity for research.

The reflexes of these actions on occupational stress can also be investigated, in order to infer about the conditions in which their action creates a favorable environment reducing the negative effects of stress at work. The observance of the leaders’ personality traits can indicate the preferences of users of the budget, at the same time its effects in the relationship between participation and performance, as well as in relation to other intervening variables present in this process.