Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkPensamiento & Gestión

On-line version ISSN 2145-941X

Pensam. gest. no.37 Barranquilla July/Dec. 2014

An analysis of corporate social responsibility in Brazil: growth, firm size, sector and internal stakeholders involved in policy definition

Un analisis de la responsabilidad social de las empresas en Brasil: el crecimiento, tamano de la empresa, sector y grupos de interes internos que participan en la definicion de politicas

Vicente Lima Crisostomo

vicentelc@gmail.com

Universidade Federal do Ceara

Fatima de Souza Freire

ffreire@unb.br

Profesora de Contabilidad. Universidade de Brasilia(Brasil)

Paulo Henrique Nobre Parente

paulonobreparente@yahoo.com.br

Universidade Federal do Ceara

Fecha de recepciun: 19 de septiembre de 2012

Fecha de aceptacion: Enero de 2014

Abstract

This study aims to analyze Corporate Social Responsibility in Brazil, trying to capture signals that Brazilian firms are integrating CSR into their strategy. We have used a unique database comprising CSR of Brazilian firms, IBASE, which contains CSR data for about ten years. Results show that a growing number of Brazilian companies have adopted CSR and many firms already have internal stakeholders formally involved with CSR policy definition. Such groups have influenced CSR policy. This formal inclusion of stakeholders and the growing number of firms adopting CSR could be an indication that that the Brazilian firms may be integrating CSR into their strategy. Besides, sector, and firm size also seem to interfere on CSR policy. A relevant growth in external and environmental social actions has been documented.

Palabras clave: Corporate Social Responsibility, Brazil, Growth, Firm strategy.

Resumen

Este trabajo tiene como objetivo analizar la Responsabilidad Social Em-presarial en Brasil, intentando captar senales de que la empresa brasilena esta incorporando la RSE en su estrategia. Nosotros hemos utilizado una base de datos unica en Brasil que contiene datos de la RSE para un perfodo aproximado de diez anos. Los resultados muestran que un numero creciente de empresas brasilenas han adoptado la RSE y muchas empresas ya tienen grupos de interes (stakeholders) internos que participan formalmente de la definition de polfticas de RSE. Tales grupos han influido en la polftica de RSE. Esta inclusion formal de los stakeholders y el creciente numero de empresas que adoptan la RSE podrfa ser una indicacion de que de que la empresa brasilena puede estar incorporando la RSE en su estrategia. Ademas, el tamano de la empresa, y el sector de la firma tambien parecen interferir en la polftica de RSC. Un crecimiento relevante en las acciones sociales externas y ambientales se ha documentado.

Keywords: Responsabilidad Social Empresarial, Brasil, crecimiento, estrategia de la empresa.

1. INTRODUCTION

In modern times, the way firms interact with different social groups, as well as with the environment seems to be relevant. Stakeholder theory suggests that companies can be also assessed by their relationship with stakeholders (Donaldson & Preston, 1995; Freeman, 1999; Freeman & Phillips, 2002; Freeman, Wicks, & Parmar, 2004; Jamali, 2008). The strategic process of some companies already take it into account in order to legitimize corporate social activities and improve company's image and reputation (Aguilera Castro, 2012; Cochran, 2007; McWilliams & Siegel, 2001; Prahalad & Hamel, 1994; Tilling & Tilt, 2010).

This study aims to analyze Corporate Social Responsibility in Brazil, a country that faces growing visibility. The evidence that country characteristics moderate CSR motivates specific country studies (Baughn, Bodie, & Mcintosh, 2007). Some research questions can be raised. Were there advances in CSR actions of Brazilian firm since the 1990s when the debate on the subject became more intense? What is the intensity of CSR of the Brazilian company? Are there characteristics of the Brazilian company that contribute to the development of the social action of the Brazilian company? What are the stakeholders involved in CSR policy definition and how they influence it? Are there signs that the Brazilian company could be integrating CSR into its strategy?

Using CSR data of the Brazilian firm for the period 1996-2008 we have assessed the evolution of the intensity of the corporate social action, taking into account some firm characteristics, such as the involvement of internal stakeholders in the definition of firm's CSR policy, firm size, the fact of whether or not a company is listed in the stock market, and firm sector.

Results show that a relevant number of firms already formally involve internal stakeholders in CSR policy definition. During the period of analysis there was an increase in the number of companies that have adopted the practice of CSR and its disclosure, and there was a significant growth of external and environmental social actions. These are important signals that the Brazilian firm is integrating CSR into its business strategy and that CSR may be progressing beyond the field of discourse. Specifically, the groups of internal stakeholders involved also interfere in the intensity of CSR. Besides, CSR of larger companies, and also of those publicly traded, is not superior to CSR of other firms. It was also observed that there is a significant difference in the intensity of CSR among sectors of the economy.

We consider that this work contributes to the research on CSR by using a representative sample of Brazilian companies (1,199 annual observations of 282 firms), composed of listed and non listed companies from several sectors of the economy, while most empirical works deal only with public firms. The growing visibility of emerging markets increases the importance of such researches in these countries.

This work is organized in three sections, besides this introduction. The following section presents literature review and hypotheses. Then, research methodology and findings are exposed and finally, conclusions of the work are presented.

2. BACKGROUND AND HYPOTHESES Corporate Social Responsibility in Brazil

According to Dahlsrud (2008), Corporate Social Responsibility (CSR) presents five dimensions: social, environmental, stakeholders, economic and voluntary. Dahlsrud observes that the definition most frequently used is associated with stakeholders and social dimensions, followed by the economic, environmental and voluntary. Stakeholder dimension concerns the way companies interact with their employees, suppliers and customers, for example.

Nowadays, taking into account the wider range of social demands faced by firms, they are trying to incorporate social concerns in their strategy, targeting a closer relationship with society. Integration of social concerns may lead to changes in the organizational management model and, still, interfere in decisions related to the firm strategic policies (Cochran, 2007; McWilliams & Siegel, 2001; Prahalad & Hamel, 1994). In a certain way, the theory of the firm proposed by Jensen & Meckling (1976) could absorb the reflections on a broader set of stakeholders through the enlargement of the concerns about conflicts of interests.

International evidence shows that country characteristics may have a role on firms' CSR (Baughn, Bodie, & Mcintosh, 2007; Gj0lberg, 2009). In Brazil, the first document that bears the denomination "Social Balance Sheet" was made by the company Nitrofertil, in the State of Bahia in 1984 (IBASE, 2008). In the 1990s, CSR has matured with its assimilation by a number of companies that began to promote social action. Some factors have contributed to the advancement of CSR in Brazil: the pressure of international organizations, campaigns of environment protection organizations; the Brazilian Constitution of 1988, which represented a breakthrough in topics related to social and environmental concerns; and the accomplishment of great international events such as the Eco 1992 (IBASE, 2008).

CsR Disclosure

The publication of the activities related to CSR action can be analyzed from the point of view of the theory of legitimacy, which proposes that companies seek to legitimize their actions that are not within a regulatory framework, as is the case of CSR. Although the absence of regulation for CSR disclosure, companies are trying to accomplish and publish such actions. Some motivations for this search of legitimizing attitudes can be considered (Dawkins & Fraas, 2013). First, companies want to report substantial changes regarding their CSR performance. Second, the firm desires to improve the perception their relevant stakeholders have about it. Third, the company tries to divert attention from the relevant problems of the firm, highlighting positive issues. Finally, when the company tries to adjust concepts and views on social values and norms aligning them to their interests. Independently of the nature of the driving motivation, the objective of legitimizing activities is to gain, maintain or repair legitimacy among relevant firm stakeholders. To achieve the desired objective, legitimizing activities of the entity must be presented to society (Dowling & Pfeffer, 1975). Annual reports are a tool used for legitimizing corporate actions - material or symbolic - being an important instrument to enhance the perception of the company or to influence the shift of concepts and opinions about the values and norms of society (Deegan, Rankin, & Tobin, 2002; Deegan, Rankin, & Voght, 2000; Li, Richardson, & Thornton, 1997; Tilling & Tilt, 2010).

The Statement of Value Added (SDA) and the management report are two relevant means to disclose firm CSR. Besides, proposals for CSR reports have been studied in academic researches as well as working groups on regulatory institutions in an attempt to develop models for it (Archel, Husillos, Larrinaga, & Spence, 2009; Freire, Crisostomo, & Rocha, 2006; Gunawan, 2007; Rizk, Dixon, & Woodhead, 2008). The fact that these reports are not standardized can hinder a better analysis of the set of companies' CSR.

The first law establishing a kind of "Social Balance Sheet" was enacted in France in 1977 (Law 77,769), making its disclosure mandatory for companies with over 299 employees, and allowing the checking of firm engagement to CSR (Reis & Medeiros, 2007). Following the initiative of France, the Portuguese government made disclosure of CSR mandatory in 1985 (Law 141) and the government of Belgium in 1996 (Freire & Rebougas, 2001).

Disclosure of CSR in Brazil

In Brazil, CSR disclosure is not mandatory, and there is no formal report form or measures for that. However, there are initiatives to make CSR announcement compulsory. This is the case of the Project of Federal Law 1.305/2003; laws in some states of the country (Mato Grosso - Law 7.987/2002, Rio Grande do Sul - Law 11.440/2000, Amazonas - Law 7.987/2002); and also city laws, as in Londrina/Parana (Law 9.536/2004), in Santo Andre/Sao Paulo (Law 7.672/1998), Porto Alegre/Rio Grande do Sul (Law 8.118/1998 and Law 8.197/1998). In addition to the legislative initiatives, two other important actions must be mentioned: the Brazilian Accounting Standard NBC T 15 - Information of Social and Environmental, and the relevant initiative of the Brazilian Institute of Social and Economic Analysis (IBASE).

With the aim of promoting CSR in Brazil, the Brazilian Institute of Social and Economic Analysis (IBASE) proposed a model of "Social Balance Sheet". The idea was providing the "Social Balance Seal IBASE/Betinho" that would function as a hallmark for the firm that intended to be seen as socially responsible. The hallmark has been granted to firms that have acted responsibly towards society and with relation to the environment.

The model of "Social Balance Sheet" proposed by IBASE

The "Social Balance Sheet" model proposed by IBASE includes information of six categories: (1) company's revenue, (2) amount spent in internal social action, (3) amount spent in external social action, (4) amount spent on environmental actions, (5) indicators related to the labor force, and (6) relevant information associated with corporate citizenship. Information in sections 1, 2, 3 and 4 are expressed in monetary values for the current and previous years.

To receive the IBASE hallmark the company must meet certain conditions: (i) IBASE does not grant the seal for tobacco, armament industry, or alcoholic beverages; (ii) the full adoption of the IBASE "Social Balance Sheet" model can't admit omission of information; (iii) publication of the Social Balance in a magazine or newspaper is compulsory; (iv) the distribution of Social Balance to employees and labor unions; (v) the company shall comply with the provisions of Decree 3.298/1999, which regulates Law 7,853/1989, which establishes quotas for people with disabilities (2 to 5% of total number of employees) in companies with more than one hundred employees; finally, (vi) the company must achieve improvements in some indicators, such as education, accidents and environmental actions.

Hypotheses rationale

The context of greater international social pressure on firms, also in developing economies, where social demands are even more relevant, we see as appropriate the proposal of a set of hypotheses about CSR in Brazil.

A first conjecture that we propose is that the initiative of IBASE produced a positive effect towards increasing the social action developed by Brazilian companies. By creating a model of "Social Balance Sheet" with wide diffusion through a credible institution in society and the granting of a hallmark of a socially responsible company for those firms that meet certain levels of social action, IBASE encourages companies to intensify their CSR and awakens society at large to this aspect of the business action. This reasoning leads us to propose the hypothesis that the initiative of IBASE was able to increase the CSR in Brazil.

Hypothesis 1: There was an advance of Corporate Social Responsibility in Brazil leading to expect that CSR indicators have improved the disclosure of CSR with the advent of the IBASE initiative of the "Social Seal IBASE/Betinho".

The intensity of CSR may vary between companies due to different characteristics. The question related to the sector has been highlighted as a factor that must be taken into account, as it seems that there are sectors more likely to perform certain types of social action for different reasons (Aguilera, Rupp, Williams, & Ganapathi, 2007; Crisostomo, Freire, & Soares, 2012; Griffin & Mahon, 1997; Waddock & Graves, 1997). In this work, we propose the hypothesis that, in fact, the intensity of the social action of Brazilian companies is influenced by the sector as detected in other countries.

Hypothesis 2: The intensity of the Corporate Social Responsibility of the company is not independent of Brazilian industry. Based on this proposal, it is expected CSR indicators to be different among sectors.

The size of the company has been considered in the literature as a characteristic that can interfere in the ability of the company to undertake CSR. To the extent the company grows, it becomes more visible and gets more responsibility in relation to a broader spectrum of stakeholders. Besides, larger firms are more likely to have financial slack (slack resources theory) and availability of more infra-structure to support the engagement in CSR. All this tends to ease larger firms to be most active in CSR (Udayasankar, 2008; Waddock & Graves, 1997). Notwithstanding, Udayasankar(2008) and Baumann-Pauly, Wickert, Spence, & Scherer (2013) believe that the motivations for undertaking social action is the same for small and large firms. Although Udayasankar' rationale, the commonsense is that larger firms are more prone to undertake CSR activities. In this line of thought, we propose the hypothesis that there is interdependence between the size and intensity of CSR in the Brazilian company, being the larger companies stronger in CSR activities.

Hypothesis 3: The intensity of Corporate Social Responsibility in Brazil is influenced by the size of the company. Larger companies are more able to undertake CSR and, therefore, have better indicators of CSR.

In the same line of argument related to firm size we propose another hypothesis that public companies also have a higher level of CSR. Such companies usually have higher visibility, and also tend to have easier access to external funds for investment. Besides, public companies tend to be older, larger, and have more operational scale which enables them to be more capable to undertake CSR activities. This group of companies has a tendency to adopt better corporate governance practices that, nowadays, are also linked to corporate sustainability issues which, in certain sense, requires companies to be more active in CSR (Charbaji, 2009; Neal & Cochran, 2008; Petersen & Vredenburg, 2009; Said, Zainuddin, & Haron, 2009).

Hypothesis 4: Corporate Social Responsibility in Brazil is distinct between listed companies and the others, being superior to the first ones.

It is not easy to know exactly whether a firm has integrated CSR in its strategy process. Nonetheless, the formal inclusion of stakeholders in the definition of social projects is an important sign that CSR policy is considered an important concern for that firm.

IBASE requires information relative to which groups of people the firm implies in the definition of CSR policy. The firm may declare among three choices: (i) the participation of all employees, (ii) participation of directors and managers, and (iii) the involvement of firm direction only. Whereas employees may push for their demands at the same time that management wants to give priority to social action that has greater external visibility, it is hypothesized that the dimension of CSR intensity can be influenced by the groups of people involved on CSR policy definition.

Hypothesis 5: CSR policy definition of Brazilian company is influenced by the stakeholders involved in it.

The disclosure of what are the internal stakeholders involved in CSR policy definition indicates that the company has formalized the definition of CSR projects with possible links with business strategy.

3. sample and methodology

sample and Variables

For carrying out this work we used data from the Brazilian Institute of Social and Economic Analyses (IBASE) to compose a unique database with CSR of Brazilian firms, composed of 1,199 annual observations of 282 companies that reported CSR data in the period 1996-2008.

Literature has indicated the problem of CSR measurement and evaluation, leading to a variety of proxies for CSR (Margolis & Walsh, 2003). This difficulty can be even more severe in developing markets, where the issue of CSR has not reached the relevance already achieved in advanced economies. The lack of information on CSR in Brazil makes IBASE database quite unique and relevant. It is worth mentioning the fact that such database comprises data from listed and non listed firms.

This paper calculates a CSR index from IBASE data. There are available data relating to the three aspects of CSR: social action addressed to all employees, external, and environmental action. More funds invested in social action can be considered as an indication that the company is socially responsible (Barnea & Rubin, 2010). Following previous studies, monetary values indicating how much the company has spent on every aspect of social action are divided by the net income in each specific year (Crisostomo, Freire, & Vasconcellos, 2011; Machado, Machado, & Santos, 2010).

The CSR index used in this work takes into account three aspects. CSP-I (Corporate Social Performance Index) corresponds to the total social expenditures over net income. Similarly, for every aspect of corporate social action (CSR directed to employees, external social action, and environmental action) was also calculated a specific index. Each of the three indexes of CSR have been calculated by the ratio between the amount of specific expenditures in social action dimension and net income: index relative to the relationship with employees (ER-I), index relative external social action (ESA-I) and the rate of environmental action (ENV-I).

Methodology

The methodology of this work is based on a descriptive study of CSR indicators throughout the research period and between firm industries. Mean comparison tests have been carried out for CSR indexes, global, and for every aspect of social action, internal, external and environmental. For robustness of results, parametric and non-parametric tests have been used.

4. REsULTs

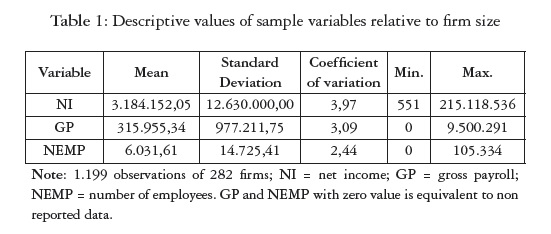

Table 1 shows the descriptive values of variables, allowing an overview of the sample of 282 companies (1,199 firm-year observations) that have reported social action using the model of Social Balance proposed by IBASE. The high variability (standard deviation and coefficient of variation) of the net revenue and the body of employees (total payroll and number of employees) shows that there is a good representation of companies. In fact, small, medium and large firms have disclosed CSR information through IBASE.

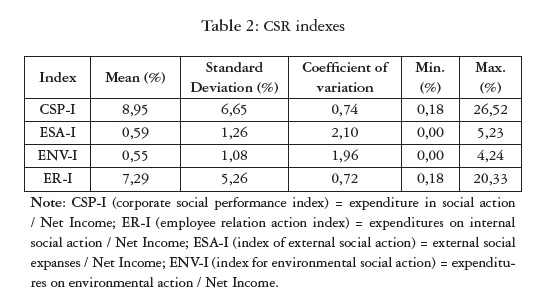

Table 2 allows a general overview of the intensity of CSR of Brazilian companies. The corporate social performance index (CSP-I) shows that the Brazilian company has spent an average of 8.95% of net revenue in CSR. The index related to the employee relations (internal social action) (ER-I) is the main component of CSR, corresponding to 7.29% of net revenue which, in fact, far exceeds the rate of external action (0.59%) and the environmental action (0.55%). The importance of internal social action has been highlighted in the literature calling attention to need for advances in this area in developing countries like Colombia (Jaramillo Naranjo, 2011). This need is also a reality in Brazil. The external and environmental social actions also present greater variation between companies with coefficients of variation of approximately 2.

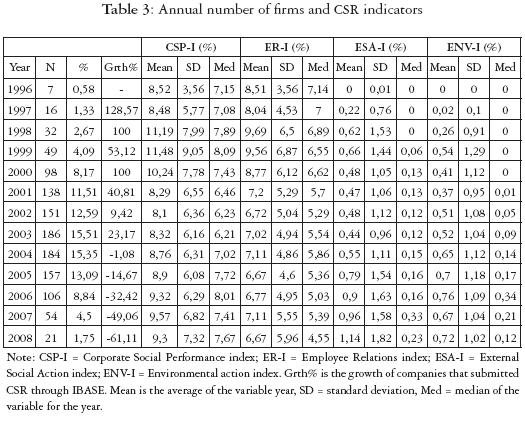

Numbers in Table 3 show that the work of IBASE, aiming to stimulate CSR in Brazil, seems to have been effective, regarding the number of firms disclosing CSR. It can be seen that from the first year of publication (1996) until 2004 there was an increase (% Grth) fairly relevant in the number of companies disclosing CSR. From then on the reduction in the number of companies may have occurred due to emergence of other media outlets with more visibility, like the GRI (Global Reporting Initiative). Table 3 also shows the mean, standard deviation (SD) and median (Med) of each index annually. Note that CSP-I does not present a great variability, ranging between 8 and 11%.The numbers of employee relation (ER-I) also do not show great variance. Differently, external social action (ESA-I) and environmental action (ENV-I) have faced a relevant increase since the first years. For external social action, we can see that both the average and median values have been raised. The same happens to environmental action (ENV-I).

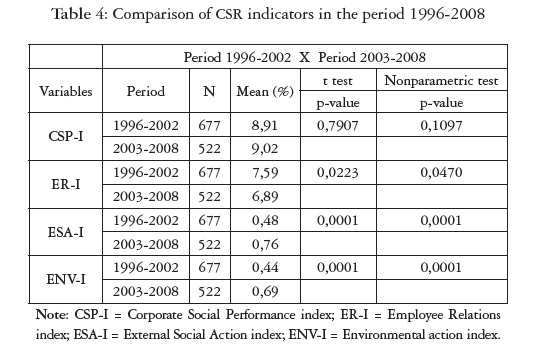

It is difficult to evaluate whether the work of IBASE, which aimed to stimulate CSR in Brazil, has managed to actually increase CSR of Brazilian companies. The numbers in Table 3 show that there appears to be large differences in the intensity of the CSR throughout the period of research. However, we advance in search of a difference as proposed in Hypothesis 1 that there was an increase in CSR. We performed a comparative study between the first half of the period, 1996-2002, and the second phase of the study period, 2003-2008 (Table 4). No significant differences were observed in the CSR indicator (CSP-I) between the two periods. However, there is significant higher average value for external social action (ESA-I) and environmental (ENV-I) in the second stage of the research period. This indicates that there appears to have been a significant increase in these two dimensions of CSR. However, the evidence concerning the internal social action (ER-I) goes in the opposite direction as the observed mean for the second period is significantly lower. Were firms prioritizing social actions with more external visibility? In fact, the internal social action seems to have a smaller impact in terms of visibility and association with the image of the company, compared to external and environmental actions that are seen as more prone to promote firm image. For robustness of results we proceeded to the comparison using parametric (t-test) and nonparametric tests. Results were the same.

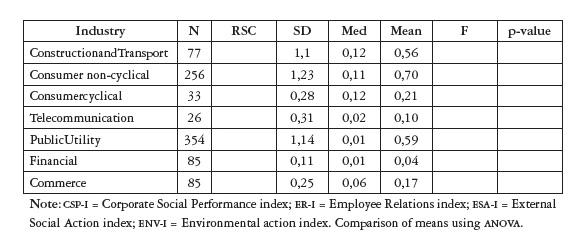

It is important to note that companies are well representative of the Brazilian economy, as they are distributed in ten sectors, according to BM&FBOVESPA industry classification (Table 5). The average index of corporate social performance (CSP-I) by industry ranges from 4,02% to 11,35%.

Extrapolating the descriptive analysis, we carried out a comparison of CSR indexes among sectors using ANOVA. There is no significant difference in the level of social action among sectors (Table 5). This difference is significant for the overall index of social action (CSP-I). This means that some industries, indeed, are more active in CSR, such as in the financial and non-cyclical consumer (foods, tobacco, cleaning and sanitation) CSP-I which exceeds 11%, compared with less-intensive sectors in CSR such as Gas and Biofuels, with 4.02%, and 5.58% of telecommunications. Importantly, there is a significant difference for each of the three areas of social action (ER-I, ESA-I and ENV-I). This resulted in the sector's importance for CSR is consistent with the literature (Machado, Machado, & Santos, 2010; Waddock & Graves, 1997).

Internal social action (ER-I) also shows significant differences between sectors, with the highest in the financial sector, 10.34%, and the lowest in the Oil, Gas and Biofuels, reaching 2.79%. The external social and environmental actions are much lower than internal action. External social action (ESA-I) is prioritized in the public utility sector (electricity, water supply and sewerage services) (1.07%), in contrast to the rate of 0.11% for the Oil, Gas and Biofuels and Industrial Products (transport material, equipment and electrical and industrial machinery). Moreover, the basic materials sector (mining, steel and metallurgy, chemicals, pulp and paper, packaging and miscellaneous equipment) is quite intense in environmental action (ENV-I), with an index of 1.01%, which is significantly higher. These higher rates may be explained by the fact that companies in these sectors must give excessive attention to environmental concerns as their activities tend to have major impacts on environment. That places them in the normative scope forcing them to pay more attention to environmental aspects.

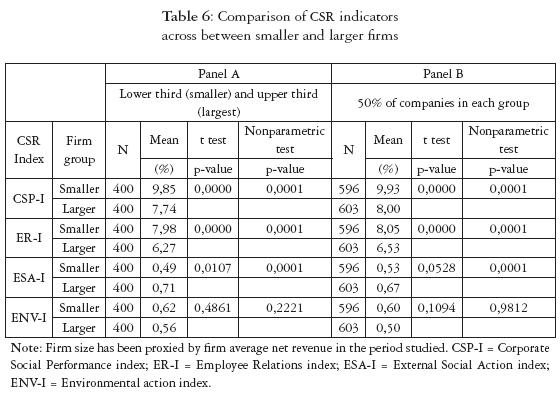

Additionally to the comparative analysis of means in all sectors, other firm characteristics also seem to influence the intensity of CSR in Brazil. Company size is generally regarded as a characteristic that could interfere in CSR as predicted in Hypothesis 3 that proposes the existence of a positive effect of size on CSR. Average firm net revenue has been used as a proxy for firm size. CSR indexes of larger and smaller firms have been compared. Looking for robust results, two sample division strategies have been adopted. First, the upper third (larger firms) of the whole sample has been compared with the lower third (smaller firms) (Table 6, Panel A). Then, sample split has been done by the median value of firm size, i.e., the upper 50% (larger firms) of the whole sample has been compared with the lower 50% (smaller firms) (Table 6, Panel B).

Contrary to the expectations, the results indicate that CSP-I of smaller companies has been significantly higher. Viewing the three dimensions of corporate social action, it is observed that the main component of CSR, internal social action, was also higher for smaller companies, which probably influenced the outcome of CSP-I. The negative relationship between firm size and CSR has been documented previously in USA and Brazil (Barnea & Rubin, 2010; Crisostomo, Freire, & Vasconcellos, 2011). Noteworthy studies have questioned the linear and positive relationship between firm size and CSR (Baumann-Pauly, Wickert, Spence, & Scherer, 2013; Udayasankar, 2008).

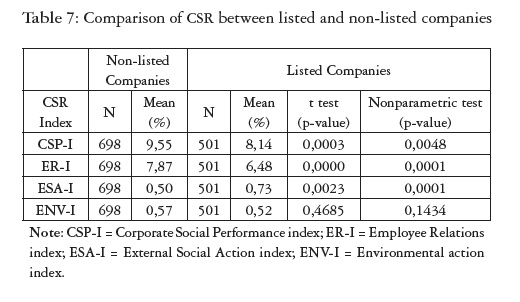

Results similar to those obtained with respect to firm size have been obtained splitting the sample by a dummy variable indicating whether the firm is listed in stock exchange market or not. Results show that listed companies have inferior internal social action (ER-I) and corporate social performance index (CSP-I) than non-listed companies (Table 7). These findings, in a certain way, are in the same direction of those obtained considering firm size, since listed companies are, in principle, larger. Moreover, it is interesting to note that publicly traded companies present significantly higher external social action index (ESA-I) than others. This may be an indication that listed firms may prioritize external social actions, which tend to have more visibility than internal actions.

About the stakeholders involved in the definition of firm CSR policy, 58.8% of the firms declared this information. Most of the firms (47.46%) have CSR policy definition in hands of firm direction and managers, 5.17% that put CSR policy definition under firm direction responsibility only, and 6.17% of firms have declared to involve all employees. This data is a good signal that Brazilian firm is highlighting CSR importance and integrating it into firm strategy.

Besides, the signaling of stakeholders responsibility in CSR, it is worth assessing whether such stakeholders involved in CSR policy definition interfere in such policy as proposed in Hypothesis 5.

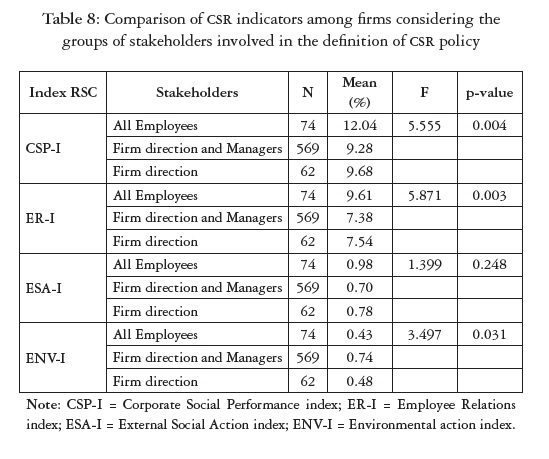

To test Hypothesis 5 that proposes the possible influence of stakeholders in CSR policy definition we have carried out a mean comparison of CSR indexes among the three groups of stakeholders, using analysis of variance (ANOVA). The mean comparison of CSR indexes by ANOVA showed that, indeed, stakeholders seem to affect the intensity of social action.

The global CSR index (CSP-I) is significantly different for companies according to the stakeholders involved in CSR policy definition. Companies in which all employees are involved in CSR policy definition have average firm social action (CSP-I = 12.04%) significantly higher than others

(Table 8). Looking at each dimension of social action, the participation of all employees in CSR policy definition appears to lead companies to be more intense in internal social action (ER-I) since ER-I index is significantly higher (9.61%) for this group of companies. On the other hand, employee participation does not appear to be able to promote external social action (ESA-I) as well as environmental (ENV-I). On the contrary, environmental action (ENV-I) is significantly higher (0.74%) for companies where only firm direction and managers are responsible for CSR policy definition.

The afore presented set of results seem to be a good signal that Brazilian firm is integrating CSR in its strategy, mainly for the fact that more than 50% have published the stakeholders formally involved in CSR policy definition.

5. conclusions

The importance of Corporate Social Responsibility has grown internationally, in developed markets and also in markets with less advanced economies. The existence of a certain pressure for more CSR from a wide range of interested parties (stakeholders) is a reality.

This paper provides an analysis of CSR in Brazil starting from CSR information evidenced by "Social Balance Sheet" proposed by IBASE in the period 1996-2008. A better knowledge of the set of Brazilian companies that have adopted the practice of social action is important when research on CSR is growing in the country. In this context, this work has verified some characteristics of the Brazilian company that seem to interfere in the intensity of CSR: firm size, sector, being a listed firm or not, and the stakeholders involved in CSR policy definition.

The findings indicate that large and small firms have undertaken CSR projects in Brazil. The majority of the companies that have used the IBASE's "Social Balance Sheet" proposal as a means of dissemination of CSR are not listed in the stock exchange, which may be an indication that a growing number of medium and small companies are integrating CSR in their activities.

Internal social action, that is, social action directed to firm' workforce has received more attention from the Brazilian company. The proposal that Brazilian firm social action has increased as a result of IBASE action cannot be fully confirmed. In fact, there has been observed that during the second half of the research period external social action and environmental action indexes have been higher. Conversely, internal social action has been reduced. This inversion may signal the possibility of a priority of conflict in Brazilian firm considering CSR policy.

CSR of the Brazilian company does not seem to be positively influenced by firm size, contrary to expectations. In fact, the mean global CSR index of Brazilian firm is higher for smaller firms. Similar result is the one indicating that non-listed firms are more intense in CSR. It is worth mentioning that internal social action is higher for non-listed firms while listed firms are more intense in external social responsibility. That signals that larger and listed firms may be more interested in external social action motivated for more visibility and reputational concerns.

An important data is the fact that a huge number of firms have declared the stakeholders involved in CSR policy definition with the majority of these having CSR in hands of firm direction and managers. Going deeper in the stakeholders performance related to CSR, evidence has been found that the stakeholders involved seem to influence firm CSR. The participation of all employees in the company CSR policy definition is associated with greater internal social action, while firms with CSR policy definition restricted to firm direction and management have a superior environmental action. That indicates that firm workforce seem to be effective in protecting their interests whereas firm direction has a trend to emphasize environmental action.

We see this work as contribution to CSR literature by providing some characteristics of CSR from an emerging market with important international visibility. CSR of Brazilian firm is not restricted to large firms or listed firms, a growing number of firms is formally involving internal stakeholders in CSR policy definition.

References

Aguilera Castro, A. (2012). Crecimiento empresarial basado en la Responsabili-dad Social. Pensamiento & Gestion(32), 1-26. [ Links ]

Aguilera, R. V., Rupp, D. E., Williams, C. A., & Ganapathi, J. (2007). Putting the S back in corporate social responsibility: a multilevel theory of social change in organizations. Academy of Management Review, 32(3), 836-863. [ Links ]

Archel, P., Husillos, J., Larrinaga, C., & Spence, C. (2009). Social disclosure, legitimacy theory and the role of the state. Accounting, Auditing & Accountability Journal, 22(8), 1284-1307. [ Links ]

Barnea, A., & Rubin, A. (2010). Corporate Social Responsibility as a Conflict Between Shareholders. Journal of Business Ethics, 97(1), 71-86. [ Links ]

Baughn, C. C., Bodie, N. L. D., & McIntosh, J. C. (2007). Corporate Social and Environmental Responsibility in Asian Countries and Other Geographical Regions. Corporate Social Responsibility and Environmental Management, 14(4), 189-205. [ Links ]

Baumann-Pauly, D., Wickert, C., Spence, L. J., & Scherer, A. G. (2013). Organizing Corporate Social Responsibility in Small and Large Firms: Size Matters. Journal of Business Ethics, 115(4), 693-705. [ Links ]

Charbaji, A. (2009). The effect of globalization on commitment to ethical corporate governance and corporate social responsibility in Lebanon. Social Responsibility Journal, 5(3), 376-387. [ Links ]

Cochran, P. L. (2007). The evolution of corporate social responsibility. Business Horizons, 50(6), 449-454. [ Links ]

Crisostomo, V. L., Freire, F. S., & Soares, P. M. (2012). Uma Analise comparativa da Responsabilidade Social Corporativa entre o Setor Bancario e outros no Brasil. Contabilidade Vista & Revista, 23(4), 103-128. [ Links ]

Crisostomo, V. L., Freire, F. S., & Vasconcellos, F. C. (2011). Corporate Social Responsibility, Firm Value and Financial Performance in Brazil. Social Responsibility Journal, 7(2), 295-309. [ Links ]

Dahlsrud, A. (2008). How corporate social responsibility is defined: an analysis of 37 definitions. Corporate Social Responsibility and Environmental Management, 15(1), 1-13. [ Links ]

Dawkins, C. E., & Fraas, J. W. (2013). An Exploratory Analysis of Corporate Social Performance and Disclosure. Business & Society, 52, 245-281. [ Links ]

Deegan, C., Rankin, M., & Tobin, J. (2002). An examination of the corporate social and environmental disclosures of BHP from 1983-1997: A test of legitimacy theory. Accounting, Auditing & Accountability Journal, 15 (3), 312-343. [ Links ]

Deegan, C., Rankin, M., & Voght, P. (2000). Firms' disclosure reactions to major social incidents: Australian evidence. Accounting Forum, 24, 101-130. [ Links ]

Donaldson, T., & Preston, L. E. (1995). The stakeholder theory of the corporation: Concepts, evidence, and implications. The Academy of Management Review, 20(1), 65-91. [ Links ]

Dowling, J. B., & Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior. Pacific Sociological Review, 18(1), 122-136. [ Links ]

Freeman, R. E. (1999). Divergent stakeholder theory. Academy of Management Review, 24(2), 233-236. [ Links ]

Freeman, R. E., & Phillips, R. A. (2002). Stakeholder Theory: A Libertarian Defense. Business Ethics Quarterly, 12(3), 331-349. [ Links ]

Freeman, R. E., Wicks, A. C., & Parmar, B. (2004). Stakeholder Theory and "The Corporate Objective Revisited". Organization Science, 15(3), 364-369. [ Links ]

Freire, F. D. S., Crisostomo, V. L., & Rocha, E. S. (2006). Proposta de Modelo de Balanjo Ambiental. UnB Contabil, 9(1), 33-57. [ Links ]

Freire, F. d. S., & Rebougas, T. R. S. (2001). Uma descrigao sucinta do Balango Social Frances, Portugues, Belga e Brasileiro. In C. A. T. Silva & F. d. S. Freire (Eds.), Balango Social: teoria eprdtica (Vol. 1, pp. 69-114). Sao Paulo: Atlas. [ Links ]

Gj0lberg, M. (2009). Measuring the immeasurable?: Constructing an index of CSR practices and CSR performance in 20 countries. Scandinavian Journal of Management, 25(1), 10-22. [ Links ]

Griffin, J. J., & Mahon, J. F. (1997). The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Business and Society Review, 36(1), 5-31. [ Links ]

Gunawan, J. (2007). Corporate Social Disclosures by Indonesian Listed Companies: A Pilot Study. Social Responsibility Journal, 3(3), 26-34. [ Links ]

IBASE. (2008). Balango social, dez anos: o desafio da transparencia. Rio de Janeiro: Instituto Brasileiro de Analises Sociais e Economicas (Brazilian Institute of Social and Economic Analysis). [ Links ]

Jamali, D. (2008). A Stakeholder Approach to Corporate Social Responsibility: A Fresh Perspective into Theory and Practice. Journal of Business Ethics, 82, 213-231. [ Links ]

Jaramillo Naranjo, O. L. (2011). La dimension interna de la responsabilidad social en las micro, pequenas y medianas empresas del programa expopyme de la Universidad del Norte. Pensamiento & Gesti6n(31), 167-195. [ Links ]

Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behavior, Agency Cost and Ownership Structure. Journal of Financial Economics, 3(4), 305-360. [ Links ]

Li, Y., Richardson, G., & Thornton, D. (1997). Corporate disclosure of environmental liability information: theory and evidence. Contemporary Accounting Research, 14, 435-474. [ Links ]

Machado, M. R., Machado, M. A. V., & Santos, A. d. (2010). A relagao entre o setor economico e investimentos sociais e ambientais. Contabilidade, Gestao e Governanga, 13(3), 102-115. [ Links ]

Margolis, J. D., & Walsh, J. P. (2003). Misery Loves Companies: Rethinking Social Initiatives by Business. Administrative Science Quarterly, 48(2), 268-305. [ Links ]

McWilliams, A., & Siegel, D. S. (2001). Corporate social responsibility: A theory of the firm perspective. The Academy of Management Review, 26(1), 117-127. [ Links ]

Neal, R., & Cochran, P. L. (2008). Corporate social responsibility, corporate governance, and financial performance: Lessons from finance. Business Horizons, 51(6), 535-540. [ Links ]

Petersen, H., & Vredenburg, H. (2009). Corporate governance, social responsibility and capital markets: exploring the institutional investor mental model. Corporate Governance, 9(5), 610-622. [ Links ]

Prahalad, C. K., & Hamel, G. (1994). Strategy as a field of study: Why search for a new paradigm? Strategic Management Journal, 15, 5-16. [ Links ]

Reis, C. N. d., & Medeiros, L. E. (2007). Responsabilidade Social das Empresas e Balanco Social: meios propulsores do desenvolvimento econdmico e social. Sao Paulo: Atlas. [ Links ]

Rizk, R., Dixon, R., & Woodhead, A. (2008). Corporate social and environmental reporting: a survey of disclosure practices in Egypt. Social Responsibility Journal, 4(3), 306-323. [ Links ]

Said, R., Zainuddin, Y H., & Haron, H. (2009). The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Social Responsibility Journal, 5(2), 212-226. [ Links ]

Tilling, M. V., & Tilt, C. A. (2010). The edge of legitimacy: voluntary social and environmental reporting in Rothmans' 1956-1999 annual reports. Accounting, Auditing & Accountability Journal, 23, 55-81. [ Links ]

Udayasankar, K. (2008). Corporate Social Responsibility and Firm Size. Journal of Business Ethics, 83, 167-175. [ Links ]

Waddock, S. A., & Graves, S. B. (1997). The corporate social performance-financial performance link. Strategic Management Journal, 18(4), 303-319. [ Links ]