Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkPensamiento & Gestión

Print version ISSN 1657-6276On-line version ISSN 2145-941X

Pensam. gest. no.40 Barranquilla Jan./June 2016

https://doi.org/10.14482/pege.40.8806

DOI: http://dx.doi.org/10.14482/pege.40.8806

Stock returns, macroeconomic variables and expectations: Evidence from Brazil

Rendimientos de las acciones, las variables de la macroeconomia y expectativas: Evidencia en Brasil

Lucio Linck

luciolinck@yahoo.com.br

Bachelor's Degree in Business Administration. Post graduation in Corporate Finance from Unisinos. Post graduation in controlling from UFRGS. Acting in area of financial management and controlling management.

Roberto Frota Decourt

roberto.decourt@gmail.com

Tenured Professor of the Graduate Program in Accounting and Finance of Unisinos. Postdoctoral fellow at the Universite Pierre-Mendes-France - Grenoble II. Doctor in Business Administration in finance from EA / UFRGS, with sandwich period at the University of Illinois at Urbana-Champaign. Address: Av. Unisinos, 950 - Cristo Rei, Sao Leopoldo - RS, Brazil, 93022-000 - room E07 402

Fecha de recepcion: 15 de febrero de 2016

Fecha de aceptacion: 17 de marzo de 2016

Abstract

There is not general support to explain the correlation among the ma-croeconomic variables and share returns in different countries and time. The unique characteristics of the Brazilian economy have changed deeply over the last years, thus the purpose of this study is to explore the correlation among the macroeconomic variables and share returns in Brazil from 2000 to 2010. The study investigates the causality relationships among real stock returns, basic interest rates, GDP, inflation and the market expectation of future behavior of these macroeconomic variables. The method used to find the correlation among the variables studied was the Stepwise Multiple Regression. The results show that basic interest rates and GDP affect the stock returns, however inflation and market expectation of future behavior of these macroeconomic variables affect stock returns insignificantly.

Keywords: stock returns; capital Market; macroeconomics variables.

Resumen

La relacion entre las variables macroeconomicas y los rendimientos de las acciones tiene resultados diferentes dependiendo de la ubicacion y el tiempo que se estudiaron. Como Brasil tiene en los ultimos anos caracteristicas peculiares, este estudio tiene como objetivo determinar el impacto de las variables y las expectativas sobre el rendimiento de las acciones entre 2000 y 2010. Las tasas de inflacion macroeconomicas fueron probados (IPCA y IGP-M), meta para la tasa Selic y la variacion del PIB actual y tambien la expectativa del mercado para el futuro. El metodo utilizado para identificar la relacion entre las variables y el retorno de las acciones se baso en la estimacion de regresion multiple por pasos. Se identifico que la tasa de interes y el PIB afectan rendimientos de las acciones. La inflacion y las expectativas del comportamiento futuro de las variables no mostraron correlacion significativa con la rentabilidad de las acciones.

Palabras clave: rendimientos de las acciones; los mercados de capitales; Variables macroecomicas.

1. INTRODUCTION

Macroeconomic conditions affect the financial results of companies because their sales and margins are correlated with economic growth, interest rates, inflation, and unemployment in the environment in which they operate. For this reason, macroeconomic indicators are widely used in the fundamentalists' models of pricing stocks. Certain economic sectors are more or less sensitive to those variables, but part of a firm's value depends not only on current performance, but also on the expectation of how those macroeconomic variables will behave in the future.

This expectation concerning the macroeconomic variables' performance in the future is an important point in asset pricing because, for an investor, the important thing to consider when evaluating an investment is how much will potentially be paid in the future balanced against the risk assumed at the time of application (Fama, 1981). Past performances will not necessarily be repeated in the future.

This is why we believe that stock performance is correlated not only with macroeconomic variables (Fama, 1981; Bhattacharya & Mukherjee, 2006; Flannery & Protopapadakis, 2002), but also with the expectation of how those variables will behave in the future.

A strong and efficient capital market gives companies access to investors' resources to invest in their projects; therefore, an efficient capital market is essential for the economic development of a country, as it allows companies to access investors' resources to grow and cultivate a stronger economy.

Brazil has a recent history of hyperinflation, which was finally controlled in 1994, but despite that apparent stability, the inflation rate is still considered high compared to most other countries. Since 1994, the prime rate, one of the main instruments for controlling inflation in Brazil, has been one of the world's largest, and economic growth fluctuated dramatically during this period, being above the world average in some years and then dropping below that average in others. Still, during this period, the Brazilian capital market showed significant progress, likely as a consequence of higher economic stability and the evolution of corporate governance practices in the country.

Terra (2006) examined the effects of stocks in 14 different countries and found that it is not possible to find an appropriate universal explanation to connect inflation and stock returns. Thus, these characteristics of the Brazilian market motivated us to conduct this study. A more comprehensive understanding of the influence of macroeconomic indicators and their expectations of the Brazilian stock market may be useful to regulators, investors, and researchers.

Contrary to what is expected, the expectations of macroeconomic variables were not relevant in the evaluation of the shares, and only the interest and economic growth were statistically significant in our model. This article presents a brief theory revision on the subject in Chapter 2, the method is outlined in Chapter 3, the results can be found in Chapter 4, and final remarks compose Chapter 5.

2. THEORETICAL REVIEW

Bodie (1976) tested the efficiency of investment in shares as a mechanism of protection against inflation; annual and monthly data over a period of 20 years (1953-1972) was studied, but to the author's surprise, the return of the shares was inversely correlated with inflation.

Fama (1981) argued that the inverse relationship between inflation and stock returns is the result of a spurious relationship, because there is also an inverse correlation between inflation and future economic activity and stock prices tend to anticipate future economic activity. Shares had fallen during times of high inflation, because overall economic activity, in the long run, is impaired by inflation.

Cutler, Poterba, and Summers (1989) analyzed the correlation between stock returns and industrial production growth in the period from 1926 to 1986. Using the full sample, a significant correlation between the two variables was found. However, considering only the period between 1946 and 1985, industrial output growth and stock returns did not present a significant correlation. The authors tested the hypothesis that inflation and interest rates affect longterm stock returns, but were unable to find support for this hypothesis.

Boyd, Jagannathan, and Hu (2005) analyzed the effect of making announcements regarding macroeconomic variables in different economic periods. The authors analyzed the effect of tax advertisements on unexpected unemployment by the stock market and various effects on the S&P 500 for the period of 1948 to 1995. The study concluded that the unexpected hikes in unemployment taxes added value to the stocks during periods of economic growth, but undervalued their shares in periods of economic contraction.

Fama (1990) argued that the stocks reflect the future cash flow of the companies; in this way, variations in stock prices could predict future macroeconomic variables.

Gay (2008) examined the effects of macroeconomic variables of stock prices in emerging markets. The study was conducted in Brazil, China, India, and Russia; it tested the impact of changes in exchange rates and the price of oil share worth. No significant results were found, which led the author to conclude that in emerging markets, domestic factors have a greater influence on stock returns than external factors, such as was evidenced in the study.

In Brazil, Magalhaes (1982) studied the relationship between stock returns and expected and unexpected inflation between 1972 and 1980. Expected inflation was not associated with stock returns, but the author did find a positive correlation for unexpected returns.

Sanvicente, Adrangi, and Chatrath (2002) also studied the relationship between inflation and stock returns in Brazil and found a negative correlation between the variables in a study conducted in the early years of hyperinflation and the stabilization of the Plano Real (1986 to 1997), which correlated macroeconomic variables with the Bovespa Index.

Terra (2006) examined the effect of inflation on stock returns in Brazil and 13 other countries, with a sample composed of seven countries in Latin America and seven industrialized countries. The period covered was not the same for each country, the longest being the one measured in Canada (1970-2000) and the shortest from the sample in Peru (19931999).

For Brazil, the period from 1982 to 1999 was considered. The author suggested that in Brazil there were artificial stock returns because inflation caused the valuation of depreciation and inventories that increased the taxable income of the companies at the expense of the actual return in stocks.

Caselani and Eid (2008) analyzed the effect of macroeconomic variables on stock prices. To do this, they used composite returns from 35 companies on the Bovespa Index between 1995 and 2003. The authors found a positive relationship between real interest rates and stock returns, but a negative relationship between industrial production and stock returns.

Method

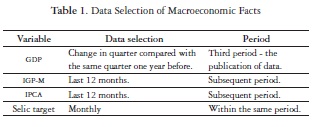

To identify the influence of macroeconomic variables on stock price, the monthly variations of the Bovespa index during the period of 2000 to 2010 is the dependent variable; the macroeconomic indices of inflation (IPCA and IGP-M), SELIC target rates, and the change in GDP are the independent variables. Macroeconomic data was represented by facts or in the actual and selected data, as presented in (Table 1).

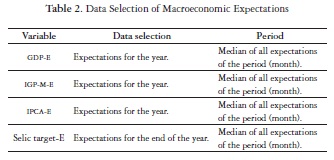

As GDP data is accumulated quarterly, however this research works with monthly variations, thus, for the three months of each quarter was used the same variation in the quarterly GDP. To complete the independent variables, the study also utilized the same systematic indexes, this time represented by the market expectations from the Focus report from the Central Bank of Brazil. In (Table 2), the method of how this data was selected is explained.

The sample of this study considers the ratio between the number of observations in the sample and independent variables, 16.5 to 1, i.e. for each independent variable (macroeconomic), there are 16 observations in the sample, totaling 132 data points to be observed. Hair et al. (2009) argued that this ratio should be at least 5 to 1, while a desired level would be between 15 and 20 observations for each variable.

At the end of each month, from 2000 to 2010, the closing value of the Bovespa Index and IBRX-100 were gathered and subsequently processed by percentage, thus representing the variable dependent multiple regression equation. Both ratios were extracted from the BM & FBOVESPA website.

The method employed for the application of multiple regressions is based on stepwise estimation, where each variable is considered for inclusion before the development of the equation. The independent variable with the largest contribution is added in the equation first, thus selecting variables for inclusion based on their incremental contribution from the variables already in the equation. The research seeks to extend the regression method, applying statistical significance tests to determine the confidence of the regression coefficients over many samples.

As the most appropriate form of analysis and their more reliable results, macroeconomic facts and scores of stock indices were analyzed as variations of absolute indices.

The method of evaluation and interpretation of data is restricted to only four macroeconomic variables, although they are separated from facts and market expectations. Analysts and investors know that the stock market is sensitive to many variables, ranging from a host of other economic indices to the disclosure of fundamentalist information. The effects of an external front, such as the impacts of international news in the Brazilian scenario, are also considered as limiting factors to research. In general, the results of this study are limited only to the variables and partially explain the impact of this information on the variation of stock prices.

3. RESULTS

Initially, Ibovespa scores were collected at the end of each month during the years of 2000 to 2010. Soon after, the facts and the expectations of the Central Bank were extracted in order to determine the macroeconomic variables. Given all the available data, the macroeconomic information was composed of independent variables to the regression equation, while variation from the Bovespa index was considered the dependent variable.

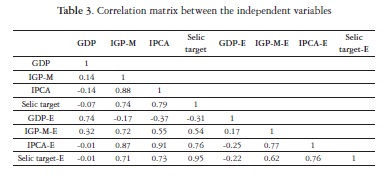

The preferred, most reliable and chosen way for reporting the results of the regression equation was working with the variation of all variables, whether dependent or independent. The absolute independent variables without the percentage changes are strongly correlated, which ultimately indicates the presence of multicollinearity between these variables, where this is harmful to the development of the equation fact. In this case, an independent variable influences another independent variable, which is not appropriate. Thus, one of the correlated variables was discarded from the research. The correlation between variables is shown in (Table 3).

To apply the regression procedure, changes in macroeconomic indicators were determined as factor (y) and the variation of the Bovespa index was factor (x). The independent variables, macroeconomic facts, were determined in the regression table with a lag period, where the data published at a particular time was posted in the next period. Such application data is related to the reading of the market in relation to market indicators. Because the data is published with a certain lag period, the market takes the reading of the information in the subsequent period, characterizing this as the most appropriate way of performing regression calculations in the research and getting the most accurate results. However, the macroeconomic market expectations were not posted in the table with a lag period, but rather in the same reporting period as the market report.

Estimation of Multiple Regression Model First Variable Inclusion

With the regression defined in terms of dependent and independent variables, the sample is considered adequate for research. The next step becomes the estimation of the regression model and the overall model fit.

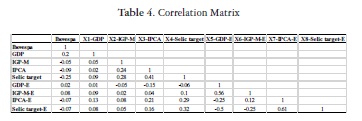

The stepwise estimation procedure was used as a model to perform multiple regression analysis. This procedure aims to maximize the coefficient of determination, R2, through the variable with the highest partial correlation, for each independent variable added to the equation. To define the first variable to be included in the regression model, we considered the macroeconomic indicator of the largest bivariate correlation with the monthly return of Ibovespa.

(Table 4) shows the correlation between the independent variables and the correlation between the Bovespa and all the macroeconomic indicators. According to Table 4, we can identify that variable X4 (Meta Selic - Fact) has the highest bivariate correlation with the dependent variable Bovespa. Thus, this is the first variable to be added to the multiple regression equation, with an acceptable level of significance of 0.05 for the regression coefficients.

The results of the regression between the variable X4 (Meta Selic - Fact) and the Bovespa Index are shown in (Figure 1).

From the results presented in Figure 1, we can draw some conclusions from the model:

R-Multiple: the correlation coefficient for a simple regression (only one dependent variable). At this stage, it is only diagnosing a 24.83% degree of association between Ibovespa and Meta Selic;

R-Square: Indicates the variation explained by the Bovespa index variable X4-Meta Selic, which means that the interest rate explains 6.16% of the variation in the Bovespa index;

Adjusted R-squared: the coefficient with the function of minimizing the equation overfitting. Thus, the adjusted coefficient eliminates certain distortions in R2 when the number of observations in the sample is very close to the dependent variable. In the present study, this coefficient is 5.43%, not much different from the R 2, which partly indicates the lack of overfitting;

Standard Error: this is the square root of the sum of squared errors divided by the number of degrees of freedom, indicating an estimate of the standard deviation of the forecast errors. In our case study, this deviation was 7.61%;

Analysis of variance: the sum of squared errors using only the Y average to make the prediction of the dependent variable. Using the X4 variable, this error is reduced by 6.16% (0.0488/0.7917). This result indicates that by using the sample for estimation, we can demonstrate the variation six times more than by using the average, with an F ratio of 8.4077 at a significance level of 0.044;

Analysis of Variable X4 Introduced into the Equation: a

Meta Selic (fact) was considered statistically significant for the sample (0.0044), with a regression coefficient of -0.4965;

The standard error of the coefficient, estimated as the regression coefficient, can vary in multiple samples (standard deviation of the regression coefficient), and indicated a value of 0.1712.

The statistical collinearity indicator of the correlation between the independent variables (a satisfactory number should be equal or close to 1), was equal to 1, since we were only working with one variable.

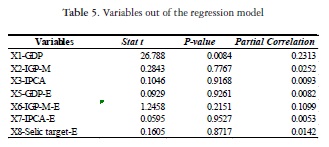

Out of Equation Variables

With the X4 variable (Meta Selic), included in the regression equation, the next step was to evaluate and determine the variable with the greatest potential of being included in the model. To add a second variable into the model, the measurement of assessment was the partial correlation coefficient.

The GDP (fact) was considered the variable with the highest partial correlation coefficient, 0.2313, among all of those who were out of style. This variable was also judged to be statistically significant at a level of 0.0084 and was subsequently added as the second variable in the regression model. The regression results with the inclusion of GDP (fact) in the model are shown in (Figure 2)

With the inclusion of X1 (GDP fact), the R2 increased from 6.16% to 11.18%. The increase of 5.02% in R 2 was the result of multiplying the unexplained variance partial correlation squared, 0.2313 x 0.9384 2. The contribution of the GDP variable in the model, together with the variable X4, helps explain the 11.18% variation in the Bovespa index.

The standard error fell slightly, revealing an improvement in the forecasts. Similarly, the analysis of variance showed an improvement in overall model fit, reducing the level of statistical significance of the F ratio

to 0.0005.

The two variables included in the model were diagnosed as significant and the standard error of the coefficient X4 was lowered to 0.1679. The statistical collinearity for both variables was satisfactorily close to the desired Level 1, thereby indicating that there was no self-correlation between these two variables.

The next step was to identify the next potential variable to be included in the multiple regression model. The rate of partial correlation was also referenced to find this next variable.

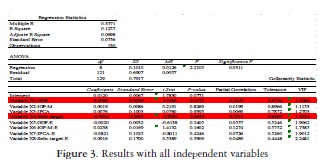

We can see in (Table 6) that none of the macroeconomic indicators have statistical significance. Consequently, none of them can be added to the model and cannot be generalized in terms of population. This test allows us to conclude that research, taking the Bovespa index benchmark as a reference point, and evaluates only two of the eight variables diagnosed, revealing a degree of explanation of 11.18%. To confirm this statement, we decided to include all eight variables in the multiple regression model. This way, we could try and confirm the results found with the inclusion of more variables, which had previously been six. The regression results with all of the variables are shown in (Figure 3).

Even with the addition of all the variables in the equation, only X1 and X4 remain significant variables that are valid for the research. The coefficient of determination, R2, increased very little with the addition of six variables, only climbing by 1.57%. This represents four times the number as compared to the number of variables with very little added to the coefficient of determination, further reinforcing the strength of Meta Selic and GDP in explaining the variation in the Bovespa index as a reference index. Variables, X4 and X1, continued to have the highest rates of partial correlation, 0.2515 and 0.2247, respectively.

A second alternative to validate the results found in the sample of the Bovespa index as a reference was to use data from another confirmatory model. This time, the confirmation was made from a second sample, IBRX-100, another index of BM & FBovespa, whose results are presented in (Figure 4). The objective of this process was to ensure that the results were generalizable to the population and not specific to the samples used in that specific estimation.

With the use of IBRX-100, the R-squared showed a slight improvement, being raised to 0.1522. The F ratio remained at a satisfactory level of significance: 0.0087. The explanatory variables considered for the Bovespa index as reference, GDP Selic apparel and apparel, also remained significant and are part of the final model in the analysis of the second sample. Both variables also had the best indicators of partial correlation. This finding was of great relevance to the research results, revealing that these two macroeconomic indicators are partially responsible for the changes in stock market shares, which provides strength to the results found in the first sample. It is also important to note that the R2, in terms of GDP and Selic, was very close to the previous sample at 11.59%.

Just as in the first sample, the X6 IGP-M variable expectation recorded the third largest partial correlation. In the previous sample, this variable did not show a significant index of a satisfactory level (0.10 / 0.05), which already indicated that the data could be relevant to the study below. However, in the second sample, the IGP-M expected statistical significance at recommended levels. That being said, regarding the interpretation of the variable X6, two interpretations can be made. The first and most relevant, which disqualifies the variable of the model, is the fact that this variable identified a positive correlation with stock indices (8% with the Bovespa Index and 12% with IBRX-100), an opposite motion that is considered normal. When market forecasts for inflation rates indicate positive change, the stock tends to fall. With a negative inflation projection, the market has a tendency to interpret this event in a positive way, and the stock market value grows. The second hypothesis, perhaps of less importance, is the fact that the market may interpret future inflation as a consequence of the growth or growing economy in the present, functioning as positive information to the market and valuing stock. In this way, the stock market moves in the same direction as the inflation index.

The results indicate, in both samples, that X4 - Meta Selic (fact) is the variable with the greatest explanatory power for the variation of the stock indices. The regression coefficients for the interest rate always had a negative sign, confirming that an increase or reduction in the Selic rate by the Central Bank reflects positively or negatively on the performance of the shares of Bovespa index as a reference and IBRX-100.

Such a statement can be based on the fact that an increase in the benchmark interest rate inhibits investments, thereby generating an economic downturn and an increase in systemic risk and the loss of market value of companies as a direct consequence. Conversely, a decline in interest rates encourages investment and consumption, in addition to the borrowing costs of companies becoming smaller, causing an increase in the earning potential of the business; this increase is reflected in the prices of its shares, which will similarly increase.

Another strong influence of this variable is associated with the fact that high interest rates are one component of the monetary policy to fight inflation, revealing an inherent foundation of instability in the economic and stock market. At this point, the investor may prefer to be more cautious, risk less with the volatility of the stock, and apply their fixed income investments (e.g. DI funds or government securities), effectively taking advantage of the better profitability offered by high interest rates.

The transfer of the equity investors to fixed income somewhat emptied the stock market, causing a decline in prices due to a lack of handling money. Normally, if interest rates fall, investors seek new ways to achieve profitability and end up migrating to the income variable, moving to buy more shares, which cause a rise in stock prices.

The second variable X1 - GDP (fact) increased 5.02% in the explanation of the Bovespa index change, which confirms that improvements or declines in economic growth help explain, together with interest rates, 11.18% of the Bovespa index volatility. This means that if GDP growth increases, the market partially follows Brazil's best growth performance. Contrarily, if the indicator of variation is lower, then the stock market has a greater likelihood of falling. One of the consequences of economic growth is the increasing demand for products and services favoring performance and producing increased profits for companies listed on stock exchanges. Economic growth is also reflective of an economy that is maintaining a certain number of activities at full capacity, boosting business investment and therefore improving the value of shares.

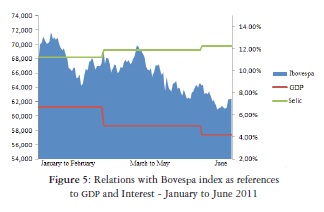

An example of the influence of interest rates and GDP variation in the stock market can be best viewed in the Bovespa index performance from the first half of 2011 as shown in (Figure 5)..

From January to February 2011, the only market information available was GDP growth from 3 quarters of 2010 (6.70%), because the disclosure of GDP occurs on average 60 days after the fact. The Selic rate for this period was fixed at 11.25%. Over the following four months, the market showed a variation of GDP that was always less than the previous transmission of 5% and 4.20%, along with an interest rate on the rise at 11.88% and 12.25% in March and April, respectively. Figure 8 leaves no doubt that the rise in interest rates and lower economic growth negatively influenced the Bovespa index score.

Inflation indicators, IGP-M and IPCA fact, were not considered as relevant to the model, revealing interference variation of stock indices. Fluctuations in the inflationary scenario are used by Central Bank to define the range of the bands of the inflation targeting. The main instrument of the central bank to pursue their policy goals is the interest rate. This makes it the most sensitive to changes in market interest rates, thus defining this instrument as a consequence of the inflationary scenario indicating an indirect influence of inflation on the stock market, i.e. by an increase or decrease of interest rates.

This same theory applies for the expectations of inflation rates, which also failed to provide a significant degree of explanation for the model. For GDP and Selic, both expectations also showed no influence on the exchange, thus demonstrating that these two variables are noticeable to investors by properly publicized facts and not by the expectation of economists.

The degree of explanation found for the variation of the market was around 11%, and can be considered as a satisfactory result, considering that the stock market is exposed to numerous variables and based on the information available. Fundamental indicators, other domestic macroeconomic variables (rates of unemployment, for example), and information on international economic scenarios are some examples of facts that may raise or drop the rates of stock shares.

4. CONCLUSIONS

This study tested the relationship between the main macroeconomic variables and the price of the shares in the Bovespa index from 2000 to 2010. This research seeks to extend the macroeconomic variables in realized facts and market expectations.

Through the statistical multiple regression model, the variables Meta Selic (apparel) and GDP growth (fact), together offered some explanation, the R2 about 11% to the variation of BM & FBOVESPA. We analyzed eight variables studied, divided between facts and expectations, however only interest rates and economic growth presented statistical significance. The market expectations seems not expressly influence stock indices, maybe the market expectations are also consequence of the observed macro variables

Based on the results presented, it is evident that the market is very sensitive to changes in interest rates, which is a major factor behind the volatility of the stock market. Perhaps more importantly, in a scenario of successive increases in the benchmark interest rate, the investor increases his liability by the risk premium due to the increased profitability of risk-free securities.

However, in an environment of high interest rates and shifts in economic growth in the fall, this scenario may be a great opportunity for future gains for long-term investors, considering that stocks, during negative economic momentum, tend to be undervalued or cheap, signaling index earnings that are below expectations.

With two variables accepted and included in the final regression model, the R2 was able to determine 11% of the variation in the price of shares, totaling eight macroeconomic variables. To deepen and improve the coefficient of determination, R2 would require the inclusion of other systemic variables, such as exchange rates, unemployment rates, and industrial production numbers, thus increasing the explanatory power of the model.

Even so, a large percentage of the explanation is still related to other relevant factors, such as specific companies or the international economy. Because of this, in future research, having some fundamentalist indicators, such as profitability, P/E ratio, and debt, as additional variables in the current regression model, would be something of great relevance and would impact the results significantly, thereby improving investors' confidence and the attitude of market analysts regarding the sources of information for the valuation of assets.

REFERENCES

Bhattacharya, B. E Mukherjee J. (2006). Indian stock price movements and the macroeconomic context - A time-series analysis. Journal of International Business and Economics. 5(1), 88-93. [ Links ]

Bodie, Z. (1976). Common stocks as a hedge against inflation. The journal of finance 31(2), 459-470. DOI: 10.1111/j.1540-6261.1976.tb01899.x [ Links ]

Boyd, J. H.; Hu, J. E & Jagannathan, R. (2005). The stock market>s reaction to unemployment news: Why bad news is usually good for stocks. Journal of Finance, 60(2), 649-672. [ Links ]

Caselani, C. N. & Eid Jr., W. (2008). Fatores microeconomicos e conjunturais e a volatilidade dos retornos das principais agoes negociadas no Brasil. Revista RAC Eletromca, 2(2), 330-350. [ Links ]

Chen, N.; Roll, R. e Ross, S. (1986). Economic forces and the stock market. Journal of Business, 59, 383-403. [ Links ]

Cutler, D. M.; Poterba, J. M. & Summers, L. H. (1989). What moves stock prices? Journal of Portfolio Management, 15(3), 4-12. [ Links ]

Fama, E. F. (1981). Stock returns, real activity, inflation, and money. The American Economic Review, 71(4), 545-565. [ Links ]

Fama, E. F. (1990). Stock returns, expected returns, and real activity. Journal of Finance, 45(4), 1089-108. [ Links ]

Gay, R. D. (2008). Effect of macroeconomic variables on stock market returns for four emerging economies: Brazil, Russia, India, and China. International Business & Economics Research Journal, 7(3), 1-8. [ Links ]

Hair, J. F.; Black, B.; Babin, B.; Andreson, R. E. & Tatham, R. L. (2009). Ana-lise multivariada de dados (6a ed.) Porto Alegre: Bookman. [ Links ]

Flannery, M. J. & Protopapadakis, A. A. (2002). Macroeconomic factors do influence aggregate stock returns. Review of Financial Studies, 15(3), 751-782. [ Links ]

Magalhaes, U. (1982). Retornos de ativos e inflagao. Revista Brasileira de Economia, 36(4), 445-472. [ Links ]

Terra, P. R. S. (2006). Inflagao e retorno do mercado acionario em paises desenvolvidos e emergentes. Revista de Administragao Contemporanea, 10(3), 133158. [ Links ]

Sanvicente, A. Z.; Bahram, A.; Chatrah, A. & Pamplin, R. B. (2002). Inflation, output and stock prices: evidence from Brazil. Journal of Applied Business Research, 18(1), 61-76. [ Links ]