Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Cited by Google

Cited by Google -

Similars in

SciELO

Similars in

SciELO -

Similars in Google

Similars in Google

Share

Permalink

PermalinkAD-minister

Print version ISSN 1692-0279

AD-minister no.28 Medellín Jan./June 2016

https://doi.org/10.17230/ad-minister.28.11

ARTÍCULOS ORIGINALES

DOI: 10.17230/ad-minister.28.11

Mainstreaming Disaster Risk Management for Finance: Application of Real Options Method for Disaster Risk Sensitive Project

Incorporación de la Gestión del Riesgo de Desastres a las Finanzas: Aplicación del Método de Opciones Reales para Proyectos Sensibles al Riesgo de Desastres

KUSDHIANTO SETIAWAN1

1 Ph.D. Faculty of Economics and Business, Universitas Gadjah Mada, Indonesia Email: s.kusdhianto@ugm.ac.id

JEL: G32, M14, Q54

Received: 20/06/2016 Modified: 27/06/2016 Accepted: 30/06/2016

ABSTRACT

This paper discusses the application of real options analysis for a project that is in the process of construction and was affected by a natural disaster. The use of the analytical method has become a way of thinking in making decisions that should be taught to business school students. The case in this paper is based on an MBA thesis at the University of Gadjah Mada that was intended as a showcase for application of real options to address real business problems. It shows one of the strategies in mainstreaming disaster risk management in the business school that also answers the needs of businesses in the disaster-prone country.

KEYWORDS Real options; disaster risk management; business continuity plan; disaster response.

RESUMEN

Este artículo discute la aplicación del análisis de opciones reales a un proyecto en proceso de construcción que se vio afectado por un desastre natural. El uso del método analítico se ha convertido en una manera de pensar cómo la toma de decisiones debe ser enseñada a los estudiantes de escuelas de negocios. El caso de este artículo está basado en una tesis de la Maestría en Administración (MBA) de University of Gadjah Mada, que fue concebida como una plataforma para la aplicación de opciones reales para abordar los problemas de las empresas reales. Este caso muestra una de las estrategias de incorporación de la gestión de riesgo de desastres en las escuelas de negocios que, de igual manera, responde a las necesidades de las empresas en países propensos a desastres.

PALABRAS CLAVE Opciones reales; gestión del riesgo de desastres; plan de continuidad de negocio; respuesta a desastres.

INTRODUCTION

Indonesia is an archipelago country with a population of more than 230 million people, lying on the equator with more than 17,000 (seventeen thousands) islands, and a part of pacific ring of fire with many active volcanos (129). These geographical, geological, hydrological, and demographical characteristics make Indonesia one of the countries most vulnerable to natural disasters such as earthquake, tsunami, volcano eruption, tornado, floods, draughts, wildfire, landslide, etc. Such disasters have caused many casualties and economic damage.

Statistics from the National Disaster Management Authority (BNPB) shows that in January 2016 alone, it recorded 174 disaster events that caused 20 casualties and missing people, 733,650 people have been displaced and 2,931 units of damaged homes. Figure 1 depicts how vulnerable Indonesia is to such disasters, as we can see the area highly affected by disasters (area in red) dominates the map, and the Java island where 70% of population is living, is also the most vulnerable area.

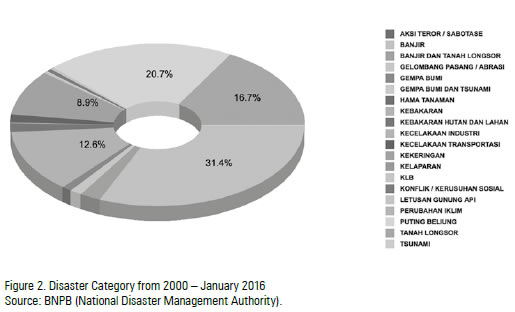

Moreover, despite its potential (rich with natural resources, demography bonus, tourism destinations, etc.), it seems that many kinds of disasters threaten the country. Figure 2 shows the statistics of frequency of disasters from 2000 until January, 2016. It indicates that floods are the most frequent disaster (31.4%), followed by tornados (20.7%), landslides (16.7%), wildfire (12.6%), and draughts (8.9%), with the rest including terrorism, earthquakes, tsunamis, climate change, volcano eruptions, famine, disease outbreaks, etc. All of these disasters undoubtedly cause a vast amount of economic losses, affecting the continuity of businesses and ultimately people's welfare.

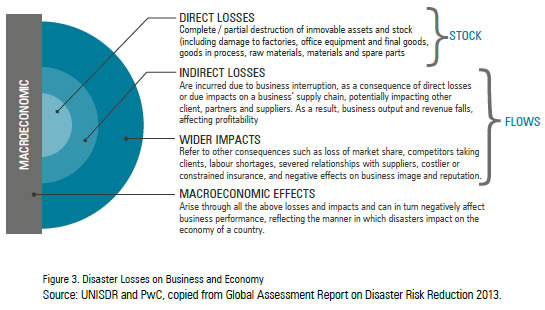

Losses caused by disasters undoubtedly affect business life and the economy. In the UNISDR's Global Assessment Report on Disaster Risk Reduction 2013, disaster losses take many forms; direct losses, indirect losses, wider impacts, and macroeconomic effects.

For those businesses located in a country that is vulnerable to disasters, investment decision making is becoming more complex. A feasible investment could turn out be unfeasible when an unfavorable event such as a natural disaster occurs. However, it does not necessarily mean that the feasibility study conducted prior to the initiation of the investment project was wrong. A feasibility study of an investment project that used discounted cash flows method (DCF) is assuming that the decision environment is stable and fixed, yet we know that more often than not, that is not true. What is frequently overlooked is to identify the management options also known as real options (to shutdown, to expand, to change price, etc.) to alter the course of the return on investment.

This paper will address the application of the concept of financial reengineering for a disaster-risk-sensitive investment project, namely real options analysis, and specifically, shutdown options. An illustrative business case2 will showcase how to analyze available management options on a project, affected by a disaster during the middle of its life cycle. The management options available in this situation include the shutdown option, where the owner of the project has to decide whether to continue operation of the project until its planned life, or to terminate the project.

In addition, this paper will show the integration of such analysis in a Financial Management Course included in the Master of Management Program (MBA Program-MMUGM), Faculty of Economics and Business, Universitas Gadjah Mada. The case presented in this paper is a joint research project between a student in the study program and the author. A portion of the research was written as a thesis by the student3, demonstrating that the topic of disaster management can be incorporated with financial management concepts.

Universitas Gadjah Mada (UGM), located in Yogyakarta was rocked by an earthquake in 2006 and in 2010 experienced the Merapi Volcano eruption. The area has established some initiatives to help the affected people, which include the establishment of: The Disaster Early Response Unit (DERU-UGM) in 2006, followed by the Disaster Study Center (Pusat Studi Bencana, PSB-UGM), and finally the Master of Disaster Management program which operates under the Postgraduate Program of UGM. A Brief description of one of the initiatives, DERU-UGM, will be discussed.

METHODOLOGY

This paper uses a business case to illustrate the decision making context to identify decision alternatives (management options); to select analysis tools to determine required data to perform the analysis; and to give recommendations on policy.

The business case overviews a company operating a project that was hit by a disaster during the middle of the project's life, requiring changes to the underlying assumptions and estimates used in the feasibility study of the project. Real options analysis using Monte Carlo simulation modelling were performed to select the best decision alternatives that the company's management had to make.

To make a simulation model, we have to understand the decision-making context, such that simulated variables and decision variables are properly incorporated in the model. The best simulation must first predetermine the alternatives in order to determine the best alternative. This results in a policy recommendation, and provides the ability to explain why such a recommendation is given. The reason for using a simulation model to solve such a business case in the MBA program is that it does not require students to be mathematicians nor to have to formulate the complex real problem using mathematical expressions. With the help of simulation software such as Oracle Crystal Ball (an add-in for Microsoft Excel), students should be able to translate the real problems onto a spreadsheet and perform the simulation to analyze each decision alternative.

The integration of DRM into MMUGM's curricula is carried out by several strategies; (1) introducing application of business concepts in core courses such as marketing management, operations management, financial management, and human resource and organization management to deal with disaster-related problems or the impact of a disaster on a business. The application can be introduced by discussing relevant cases or by creating project assignments; (2) master thesis that takes a real disasterrelated business problem as the main theme. Result of the latter is more and more cases can be developed that can be utilized to enrich the first strategy. This paper mainly describes the second strategy implementation.

The author will show the structure of curricula in MM-UGM and identify courses that could be used to disseminate Disaster Risk Management concepts as well as to perform a comparison analysis of curricula in other study program at UGM that specifically deals with disaster management, namely Master of Disaster Management. In addition, the author will describe UGM's initiative to a disaster response; disseminate the disaster awareness, and creating a disaster preparedness program through the establishment of Disaster Early Response Unit (DERU-UGM).

LITERATURE REVIEW

The business case used in this paper is related to a highly sensitive disaster risk investment project. This integrated approach requires understanding not only of financial management concepts but also knowledge such as marketing (to measure market confidence index that leads to demand estimation after the disaster or recovery stage), disaster management (how long the recovery plan will take), and economics (price of the commodity, demand analysis, etc.). The key theme of this case focuses on utilizing financial reengineering techniques to resolve business problems. Investment decision analysis that uses methods such as Net Present Value (NPV), Internal Rate of Return (IRR), and its variation; Modified Internal Rate of Return (MIRR) is often called traditional analysis and is based on the discounted cash flows method (DCF). These are perhaps the oldest methods used in today's modern financial world. The use of these methods always assumes that all factors being considered are fixed and certain; the cost of capital, estimates of cash flows, project investment's life, selling price, cost of inputs, etc.,. are non-stochastic variables. In the real world, these variables are often changing during the project's life. In addition, manager has several options (a right or a privilege, not an obligation) to change the value of the variables, for example terminating the project earlier due to unfavorable outcomes or bad situations. In such a case, the manager alters the project's life; the project's life is no longer a fixed variable that cannot be changed. Such alternatives of decisions are called real options, and the method is called real options analysis (see for example the definitions and examples in the standard financial management textbook of Brigham and Ehrhardt, 2014).

Types of Real Options

There is actually infinite variation of real options. The types of real options listed below are just a list of popular, frequently discussed, and modeled real options.

Investment timing option. It is an option to start immediately or to postpone an investment project. By postponing, one could gather more information that eventually reduces the risk and losses. However, the consequences of the postponement may include higher cost of capital, more expensive inputs (i.e. due to inflation), and momentum loss (demand is vanishing because consumer prefer competitors'/pioneer's product than ours).

Growth option or expansion option. After a successful investment, frequently firms eager to continue or to expand the existing investment. Examples include: increasing production capacity to take advantage market momentum (higher demand); diversifying existing product lines; expanding the market, etc. The growth option may be considered as a new investment when taking into account the new market size, initial investment to expand, additional cost of capital that might change because of new financing strategy, and so on.

Contracting option. This is a typical investment decision in a new technology or product when there is uncertainty about the product's long term (or short lived) lifecycle. For example: instead of building one's own production facility a less risky alternative is to give the production order to another company.

Flexibility option. Flexibility to change the design of a product or facility, its price, its feature, required inputs to produce it, etc., highlight examples of valuable options that generate a firm's competitive advantage.

Shutdown option or abandonment option. Suppose that in middle of the investment's life, an unfavorable event is taking place (i.e. disaster, disease outbreak, economic crisis, etc.), as a result, demand is falling while cost is increasing. Under such circumstances, a manager has to make a quick yet strategic/long-term decision of whether or not to continue the operation of the business or investment. Careful consideration should be taken in employing this option as shutting down the business also means closing future opportunities.

Many other types of real option and examples of modelling techniques can be found in the literature. See example in Mun (2002) and, Sipp and Carayannis (2013).

Real Options Analysis for Disaster Risk Related Strategic Investment

Sipp and Caravannis (2013) consider the real options analysis in decision making as not only a method or technique, but also as a new paradigm in decision-making. As a new paradigm, the decision making carried out by a manager in an investment decision making is not merely practicing algebra of the DCF method (i.e. go ahead if NPV>0). Additionally he should execute the four-strategic theme outline by Bowman and Hurry (1993), namely sensemaking, resource allocation, strategic positioning, and learning.

- Sensemaking references managers attempt to make sense of and interpret past situations and utilize their intuitive beliefs to inform their future decisions.

- Resource allocation refers to the fact that firms invest in their business to maximize operating eftciencies and build competitive barriers.

- Strategic positioning refers to the fact that firms invest today to create opportunities for tomorrow and thereby attempt to sustain performance across the unforeseeable future.

- Learning refers to the acquisition of knowledge for the future (which should the drive strategy formulation).

In the context of disaster risk related investment, the four-themes of strategic decision making might be exemplified by a manager asking the following questions:

- Sensemaking: do we have experience of unfavorable situations/events in the past that might occur again now and or in the future? Based on our knowledge, can we mitigate, reduce, or even eliminate the risk? How? What is the likelihood of the events? What options do we have now?

- Resource allocation: is the existing investment yield the best rate of return for the firm? Do we have investment alternatives? Should we continue or stop the investment? Are there resources remaining to expand the investment? Should we invest or divest on a project/business/investment?

- Strategic positioning: Is the expected value of future business opportunities worth more than existing investment value? Should we take advantage of future business opportunities or minimizing risk? Maximizing expected return or minimizing risk? What are other non-economic values we should strive for? (Social welfare, safety use of our product, safe working conditions, sustainable improvement of standard of living, etc.).

- Learning: what did we learn from our past failure? Are we ready to cope with a disaster? What should we prepare for? Have we done what we didn't do in the past that could prevent us from experiencing unfavorable outcomes?

The answers to the aforementioned questions could be manifested in variables value that we should take into account in real options analysis.

Learning from the past as outlined above will help us in sensemaking. The sensemaking will guide us to perform strategic resource allocation optimally. Optimal resource allocation is a reflection of our strategic positioning. Thus, the four-strategic theme should not be considered as steps in decision making, but rather as a paradigm in decision making; a way of thinking.

Copeland and Tufano (2004) outlined the use of real options method to analyze an investment decision, which is more often a multistage decision, rather than a onetime decision. According to the authors, they state that compared to financial options, the term 'option' in real option has a clearer meaning that its decision alternatives which have to be decided or chosen by a manager. The binomial models in options valuation such as the famous Black-Scholes-Merton model for financial options is formulated in a complex and unintuitive algebra, while real options can easily be illustrated in a spreadsheet for simulation.

Application of real options analysis for disaster management can be found, for example, in the work of Gaudard and Romerio (2015). The paper highlights the contribution of real options' approach in managing a natural hazard risk, especially in showing how to determine the timing of different types of interventions. By utilizing decision trees, the paper provides a clear and concise presentation of the dynamics of the hazardous events. It also reveals the potential of real options analysis to improve emergency management.

Another example the use of real option to disaster management is a paper Woodward, Gouldby, Kapelan, Khu, and Townend (2011). Woodward et al. identified the sources of flood risk such as climate change and socio economic changes, and then used real options method to help decision making to select the most appropriate long-term flood risk related intervention investment given the future uncertainties.

Andersen in Kreimer, Arnold, and Carlin (2003) also state that real option concept is the vanguard of strategic risk management, and it provides interesting new ways to respond to idiosyncratic non-marketable (firm specific) economic exposures. He adds that new business opportunities planned by economic entities, but not implemented, could be conceived as an options portfolio that gives a country economic flexibility and enhances its development path. Non-marketable economic exposures which are of a competitive advantage typically relate to firm-specific, non-tradable, intangible factors such as knowledge about disaster mitigation strategy that makes a firm less vulnerable to the disaster while reducing income volatility. Having such knowledge also means that future business opportunity could be gained, i.e. making expansion strategy a viable option.

Mainstreaming disaster risk management in the school of management can be carried out by introducing real options concept into courses and thesis. For example, it can be found in the Master of Science in Engineering and Management Thesis at the Massachusetts Institute of Technology. A thesis written by Maseda (2008) discussed expansion design of an emergency department for hospitals. A flexible design of ED was proposed, creating flexibility options for the hospital to cope with demand in excess of their capacity to treat patients, particularly during a disaster event. The thesis identifies, characterizes and quantifies parameters that should be considered in ED expansion projects. Such mainstreaming practices will not only increase understanding and the development of disaster risk management body of knowledge, but also prove useful for institutions that manage the risk (i.e. the hospitals) and provide invaluable benefit for society.

POLICY OPTIONS FOR MAINSTREAMING DRM INTO FINANCIAL COURSES

The Master of Management Program at Universitas Gadjah Mada has carried out several strategies in mainstreaming disaster risk management into its curricula and extra curricula activities, including activities carried out by the Executive Development Program (EDP-MM) that offers non-degree training or an education program for human resources in governmental oftces, corporations, NGOs, as well as conducting community development.

The First Strategy

The first strategy is introducing real business cases into relevant courses. However, bookcases that discuss disaster risk management are quite rare, especially those that already classified such subjects of management as marketing management, operations management, financial management, and human resources and organizational management. Lecturers were asked to look for cases in the form of research papers, white papers, reports from relevant institutions, newspaper/magazine articles, web articles and so on that are suitable for particular topics in the subject. However, the teaching materials are scattered among lecturers so that the delivery of the materials in the class discussions vary or are non-standard.

The lack of papers or cases related to DRM has been coped with via several initiatives, both in the program study level and at the university level. The following initiatives have been carried out in order to gain more updated knowledge about DRM, especially those concerned with investment decisions. Additionally, cases will be developed that will be introduced into class discussions:

Executive Development Program (EDP-MM). It is a non-degree program for executives of firms, employees, and professionals from various industries. The program is managed under the Master of Management, Faculty of Economics and Business, Universitas Gadjah Mada (EDP-MM). The EDP-MM has convened three series of refresher risk management for executives of banks since 2014. Each series has a different theme. Besides the refresher program, EDP-MM is also responsible for business case development by initiating case writing grants for its lecturers.

DISASTER RESPONSE UNIT – UNIVERSITAS GADJAH MADA (DERU-UGM)

DERU-UGM was established as a response to Yogyakarta's earthquake on May 2006. DERU stands for Disaster ''Early'' Response Unit,'' to indicate that this unit is intended to provide early response to a disaster, such as rescue, evacuation, fulfillment of basic needs, protection, management of refugees, and recovery of affected infrastructures. The organization of DERU is under a direct command of the president of the university and is managed by a manager in directorate of research and community service. Its members consist of students, lecturers and professors from 18 Faculties with different expertise, and the university's staff members. Most serve as volunteers when a disaster strikes.

Since 2008, the term ''early'' in the DERU abbreviation was removed, it has evolved into a disaster management unit that not only provides immediate responses and recovery but also has continuous and sustainable programs such as mitigation and preparedness. Recovery programs are carried out after the immediate response program. The purposes are to restore society's public routine that has stopped when the disaster occurs, reconstruction of infrastructures in the post-disaster-regions, and improvement and restorations of every aspect of public service in the post-disaster-regions. The programs are usually synergized with activity Field Work Experience4. Mitigation activities include potential hazard mapping, installation of an Early Warning System, evacuation route planning, and business continuity planning for local businesses (small and micro enterprises) in the affected area. The latter will be further explained as a business case in the next section of this paper. Preparedness programs include training programs for volunteers and the community in order to increase awareness of the disaster, to prepare readiness for disaster response, and to reduce the risk impact.

The programs and activities conducted by DERU-UGM provide invaluable experiences and lessons learned in disaster management. In some cases, the real problems found in the field are brought into class discussions which enrich both students' and lecturers' knowledge about the disaster management.

The Second Strategy

In the MMUGM, the total credits a student must take to pursue an MBA degree is 42, which consists of 11 core courses, three concentration courses, and a master thesis. Students who choose finance as their study concentration will take following courses:

- Financial Management (3 credits)

- Portfolio Management (3 credits)

- Multinational Financial Management (3 credits)

- Financial Risk Management (3 credits)

Other disaster risk management topics are discussed in other study concentrations, such as Business Continuity Plan which is discussed in Operations Management (including topics such as product design, process design, business process reengineering, and supply chain management).

Derivative instrument valuation, i.e. financial options, is taught in Financial Management, Multinational Financial Management, and Financial Risk Management. However, real options as the extension of financial options, is only thought of in Financial Management. Attaining the objective of mainstreaming DRM topics into the curricula, especially topics related to disaster risk sensitive investment analysis, is a challenging task because of the limited number of relevant courses. To cope with this challenge, MMUGM encourages its students who want to deepen their knowledge and to gain experience in performing the analysis to choose a thesis topic that is related to disaster risk sensitive investment analysis. Consequently MMUGM must provide professors and lecturers who are capable of being thesis supervisors. The thesis is an applied research project designed to solve a real business problem. By doing so, students have ample time to study the topic while discussing the methodology with their supervisor. They also explore and cultivate more appropriate methods of analysis, techniques, and managerial implications of their findings. Because the thesis is based on real business problems, the result is not only the thesis itself or the graduate, but also business cases related to disaster risk management that can be used to support the implementation of the first strategy earlier.

FINDINGS

Results of the First Strategy Implementation

EDP-MM Activities and Results

The first series of the refresher risk management program was held in May 2014, in Amsterdam, Rotterdam, and Brussels. The event was held in collaboration with the Rotterdam School of Management (RSM) at Erasmus University. The main theme was property bubbles and the impact of Greece's economic turmoil on emerging markets. The speakers were not only academicians or economists, but also professionals in the financial industry. One such speaker was from AXA Financials who explained about risk management of new financial instruments and a new asset class (i.e. property) in emerging markets, which also includes the transmission of economic turmoil in Euro economies on emerging market economies such as Indonesia. There was further discussion about global disaster i.e. SARS outbreaks and swine flu and their impact on the economy and financial sectors.

The second series was held in May 2015, in Tokyo-Japan, in collaboration with the International University of Japan (IUJ). The main theme of this series, specific and typical of Japanese expertise was Business Continuity Management (BCM). Participants included 15 top executives of leading banks in Indonesia who had a chance to learn and to discuss with experts in the field of BCM from an insurance company (especially about disaster risk transfer). Other topics included learning innovation in disaster intervention technologies in the NEC Innovation Center, and best practices of BCM in Mizuho Bank.

In late 2015, because of uncertainties in the US Fed's rate as rumor indicated that quantitative easing would be ended, the Indonesian rupiah (IDR) had depreciated significantly against the US Dollar. MMUGM was then exposed to exchange rate risk, which was an unprecedented event in the program. Its international refresher risk management program that was usually held abroad was no longer feasible to run, given that the design of the program was deemed too expensive and demand participation would be challenging in the local currency. To cope with this situation, the management of MMUGM then looked for options and tried to change the program design. Finally, the program series was held in Jakarta, featuring the topic that had become the main interest of the current situation: ''Global Economic Slowdown and Its Impact on the Indonesian Banking Sector''. The main target of participants remained the same: top executives of financial companies. The event was held in a luxurious hotel in Jakarta. An invited international speaker from RSM, a professional international banker from Deutsche Bank, and an economist of UGM were featured. This processes which we have passed through is a simple example of real options analysis, mainly the flexibility options.

The results of the lessons learned from the programs and experts in the field of risk management allowed participants to gain the latest knowledge and to be exposed to the latest technologies designed to address and to mitigate the impact of a disaster. This achieved our stated goal related to the purpose of teaching and mainstreaming disaster risk management in MMUGM, namely in the form of cases provided those companies who practice it.

DERU-UGM ACTIVITIES AND RESULTS

Since the establishment of the unit, it has contributed to providing immediate responses to disasters such as the earthquake in Padang (2009), volcano Merapi eruption in Yogyakarta (2010), floods in Jakarta (2013), volcano Sinabung eruption (2014), floods in Kudus (2014), floods in Bekasi (2014), volcano Kelud eruption (2014), landslide in Banjarnegara (2014), and many other disasters in Indonesia. Involvement of students and lecturers from different expertise areas has helped to bring about such missions successfully. Moreover, since DERU-UGM is no longer just an early response unit, but as a disaster management unit, it has started some continuous and sustainable programs, looking for best alternatives of mitigation and business continuity planning for the small and local business community, and preparedness programming.

Regarding the BCP, it is also provided an example as a simple real options analysis for identifying the most cost-effective strategy in disaster risk reduction. For example, in the case of the Merapi volcano eruption in 2010, DERU-UGM in collaboration with BNPB and local government, has successfully designed and carried out a program that enabled affected people to continue their business after the disaster. The business of the affected people is a dairy farm. DERU-UGM saved about 10,000 dairy cows that in normal days could produce 15 L/cow, generating revenue of IDR 4,000/L. That is about a business value of IDR 600 million (USD 50,000) per day or USD 18 million in a year. On average, every family has 3-5 dairy cows, so the program saved about 2,000 families' economy. This is an example of a business case that is developed from what DERU-UGM has experienced in. The business case covers topics ranging from operations management (supply chain management and location strategy) and financial management (feasibility study of the BCP and real options analysis).

Results of the Second Strategy Implementation

The second strategy is focusing on thesis writing for students who are interested in deepening their knowledge on disaster risk reduction analysis, and to be more specific, on disaster-risk-sensitive investment analysis. During 2015, the author advised three students of MMUGM who chose this topic as their main thesis theme. Not all of the theses take natural disaster as the underlying problems. Economic turmoil and uncertainties such as the fall of commodity prices of more than 70% recently became a disastrous event for firms, causing previously feasible investment projects to becoming infeasible, should management take no intervention to alter the situation. The latter issue is recently becoming more interesting as a major thesis topic in finance. However, there are more similarities than differences on the impact caused by both types of disasters, so determining how to analyze the problems and how to find the solutions are also similar. In most cases, because we have to find or choose the best alternative for strategies on a multistage decision making process, real option analysis is found to be an appropriate methodology to tackle such issues.

AN EXAMPLE OF BUSINESS CASE: SHUTDOWN OPTIONS ANALYSIS

GasFactory (GF) is a state owned company that is assigned by the Government to provide gas (compressed natural gas/CNG) supply to industry such as with fertilizer, cement, and an electricity power plant. In carrying out the assignment, GF was seeking a buyer, and finally collaborated with ElectricPower (EP), an Independent Power Producer (IPP) that also owns a strategic business unit (SBU), namely Fertilizer Co. (FC) that needed gas supply and electric power to fire up the machineries for its production. The gas purchased by EP distributed from the gas plant is not only intended to supply its SBU, but also other industries in the area (an industrial estate). The gas plant also functions as a gas storage and regasification terminal. In case of an excess production from the gas wells/terminals, the gas will flow into the storage plant, and will flow (after the regasification process) to the IPP when it operates on a peak load. The business agreement between GF and EP stated that EP will buy at least 10 BBTUD (Billion British Thermal Unit per Day) at price of USD 3 per MMBTU (Million British Thermal Unit), and if the purchase is less than that amount, EP has to pay 75% of 10 BBTUD (75% x 10000 MMBTU x USD 3 = USD 22,500/day), no matter how much gas is actually consumed. Such agreement is known as a Take-or-Pay (ToP) clause.

In order to supply a sustainable and stable gas to the plant (EP), GF had to build a gas plant facility located near its clients' facilities. This was a huge investment made by GF, worth USD 43 million. The project's life was expected to be 15 years since the commencement of operation. However, the ToP clause only effectively provided that the gas flows from the gas terminal of GF to the gas plant was at least 30 BBTUD, otherwise the buyer, EP, only pays as much as its actual consumption. The investment was made in 2012 and completed in 2013.

The business investment that GF made is very risky. Financial risk is assumed to be under the control of the Government as it provided project financing at a subsidized rate, which was below the commercial market rate. Because it was fully financed by debt and secured by the Government (in contrast to corporate financing which optimal capital structure and limited debt capacity will inhibit the company to fully finance its project by debt, project financing can do so), the cost of capital was equal to the cost of debt, at a fixed rate of 8%.

Unfortunately, since the start of operation of the gas plant, the gas flow from gas field was not as much as expected. It was less than the ToP terms such that the clause of the agreement could not be implemented; at max the flow could only reach 25 BBTUD. The main problem on the supply side (from the gas producer) of the natural gas is that there was uncertainty regarding the regulation so that new investment needed to develop the gas field was postponed. As a result, the production rate was insuftcient to supply the gas plant. Moreover, the world natural gas price has fallen significantly recently, making the gas producer demotivated to increase its investment in developing the gas field. This is another reason for the steady declining gas production rate. This situation has been persisting until now. Because the area was a developing area, not many industries were relocated to the industrial estate yet, so that the demand for gas was still lower than 20 BBTUD (on average the actual demand was only 5 BBTUD). The result is that the Take-or-Pay clause in the agreement between GF and EP could not be implemented. It was expected that the demand would grow at a higher rate in the following years, as more and more industries began operating in the area. Yet, one year after the operations, the area near where the gas plant is located, was hit by a flash flood causing tens of people killed, hundreds were evacuated, infrastructures were damaged, and many businesses collapsed. Since the planning and construction design stages of the gas plant, GF has implemented Business Continuity Plan (BCP) such as selecting location of the gas plant at the hilly side area so that tsunami could not damage the facility. Also, a disaster recovery plan was executed by creating system redundancy: a dual backup operations (on-site backup and off-site backup oftce operations), and so, the facility is safe from the disaster. Even though the gas plant was unaffected by the disaster, the demand for gas from EP dropped significantly. However, EP believes that soon after the disaster, relief had been distributed, and the recovery and reconstruction plan had been carried out. The demand also will recover and grow even higher.

The Management Options

Operating costs mostly consist of fixed costs, because the cost is more related to the production capacity than the production rate. On average, with the current capacity, total annual operating cost is USD 2.5 million, with 3% increase every year, and an overhaul cost of 6% of initial investment cost every 6 years. This situation has led to a dilemma for both GF and EP. On GF's side, continuing the operation would only generate more losses if the reconstruction process is slower than its expected. Yet stopping the operation means closing the opportunity to recover the sunk cost, and losses assume that the reconstruction, running more smoothly and quickly so that the demand from EP could be even larger than it was in the past. Moreover, because the project is an assignment from the Government that GF must do, the management also has to consider the negative multiplier effect if the project is stopped (i.e. unemployment, slower regional economic growth, etc.). If management of GF decided to shutdown, the question is when? Now? In the the next 3 years? 10 years? Never?

On the other side, EP is also facing a situation dilemma. If GF decided to shut down its operation and the market recovery worked well, then it could not take advantage of business opportunities in the future. Therefore, management of EP is thinking about acquiring the gas plant facility from GF. The question is how much it cost?

As explained above, both GF and EP have the choice of decision alternatives. The alternatives are management options that have economic value; the management on each side has to select an alternative decision that would maximize its corporate value. Such options are known as real options, and therefore to answer the business problems, we have to value each option and then choose the best one.

Analysis

The standard tool for analyzing the project feasibility is capital budgeting analysis, such as net present value (NPV), internal rate of return (IRR), and modified internal rate of return (MIRR). However, these tools are only well suited in the early stage of the project plan (before the project started). The aforementioned identified problems are problems that arose in the middle of the project's life. Real options analysis, especially the shutdown options, provide a strategic path of thinking as outlined by Bowman and Hurry (1993).

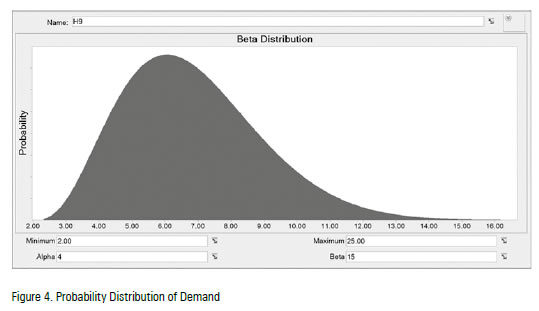

Sensemaking. The fall of commodity prices as well as the disaster had caused unfavorable outcomes, yet the events are unprecedented ones for the industry. The management has no historical data as to how fast the recovery will be or the economic losses. However, judging from the experiences of the country in responding to such disasters (Aceh's tsunami and Yogyakarta's earthquake), the recovery could take about 1-2 years, considering that the recent disasters that hit the business area were relatively small compared to the other two giant disasters. The implementation of BCP saved valuable assets, so that there was no serious damage to the production facilities. Assuming that the low commodity price will last during the project's life, management could not expect the take-or-pay clause in the agreement will go into effect. However, what management should concern itself with is the expected future demand of gas. This depends on the recovery of the affected businesses. Based on estimation, the demand for gas will remain low, at about 5 BBTUD. However, there is a chance that as soon as the affected area recovered from the disaster, the demand could reach 25 BBTUD, yet this is very unlikely. The most likely demand is about 6 BBTUD which is based on the initial feasibility study which will yield a positive NPV. The following graph shows the probability distribution of possible quantity of demand.From Figure 4, we can see that the probability that the demand will be more than 6 BBTUD is greater than the demand will be less than 6 BBTUD. It indicates that there is still a chance that this investment project would remain feasible.

Resource Allocation. From the GF's point of view, the current situation indicates that the existing investment project is not feasible as the revenue is not sufficient to cover the initial investment and operating cost. With the sales quantity of just 5 BBTUD, the NPV is –USD 3.23 million provided that the sales will remain constant until the end of the project's life. GF's management has several options,

(1) to continue the operation until the end of the project's life, (2) to terminate the operation in order to cut losses or, (3) postponing the decision in terminating the project's life at year 7 (three years from now). The assets are depreciated on a straight-line basis so that the salvage value when the project is terminated would be equal to the initial investment value subtracted by the cumulative depreciation. The manager has to decide which option would maximize the NPV by taking into account future business opportunities.

Strategic Positioning. If GF's management decided to terminate the project, either at year 4 (now) or at year 7, it would lose the opportunity to gain more revenue in the future provided that the recovery from disaster runs successfully. Moreover, by terminating the project, there would be no economic multiplier effect as this project is not only about maximizing GF's profit but also for the sake of social welfare. Therefore, decision option (1) to continue the operation, should remain on the table, even though the current situation is unfavorable.

Learning. Since the event is an unprecedented one for both companies, they have to learn from other companies, countries, histories, and the experiences of others. For example, to determine the probability distribution of demand, we have to take into account the disaster management, the mitigation plan, and the recovery plan, as well as the preparedness of the affected people. Moreover, options for not terminating the project would give management the opportunity to gather more information while avoiding having to close the future business opportunities too early.

Results

The complete spreadsheet of the Monte Carlo simulation of the real options analysis is available on the following hyperlink:

https://www.dropbox.com/s/nbh9x0t1czyey1i/Real%20Option%20with%20Crystal%20Ball.xlsx?dl=0

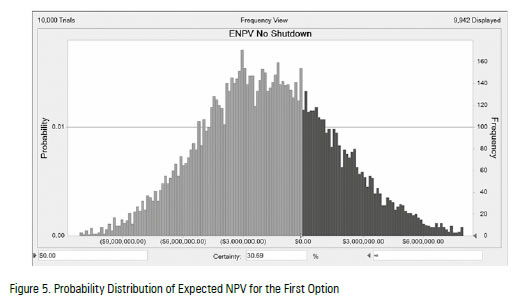

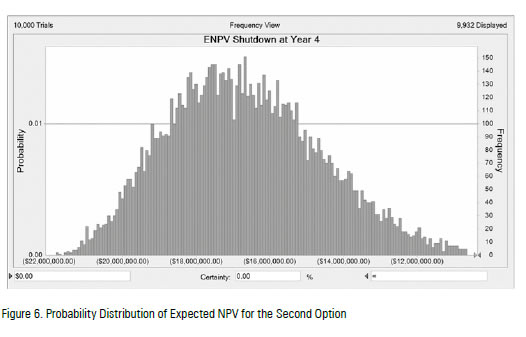

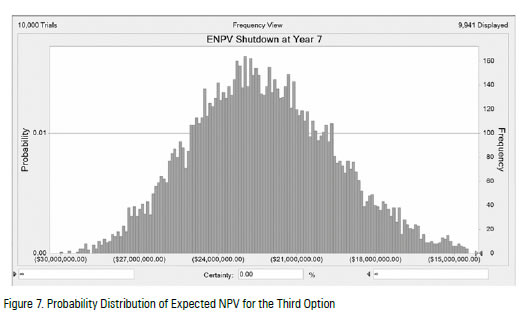

The results of the options analysis are shown on Figure 5, 6, and 7 for real option 1, 2, and 3 respectively. Figure 5 shows the result of the first option analysis (to continue the operation until the end of the project's life), and tells us that continuing the operation will give a chance to gain positive NPV (the probability of achieving positive NPV is 30%) with the maximum losses of about USD 9 million. Comparing the first option with the others, we can observe that it is the best in terms of probability of achieving NPV>0, and also maximum possible losses. The recommendation based on the results is that the management of GasFactory should continue its operation, and when new updated information is available in the future, the distribution probability of demand should be updated to reflect the latest development of the recovery.

Figure 5 shows the result of the first option analysis (to continue the operation until the end of the project's life), and tells us that continuing the operation will give a chance to gain positive NPV (the probability of achieving positive NPV is 30%) with the maximum losses of about USD 9 million. Comparing the first option with the others, we can observe that the first option is the best in terms of probability of achieving NPV>0, and also maximum possible losses. The recommendation based on the results is that the management of GasFactory should continue its operation, and when new updated information is available in the future, the distribution of probability of demand should be updated to reflect the latest development of the recovery.

RECOMMENDATION

Real options analysis can be very useful in selecting the best alternative of decisions, or choosing the most appropriate intervention in the case of disaster risk management. The method is used not only as a mathematical or statistical tool, but also as a paradigm in decision making. By incorporating the method in analyzing disaster risk sensitive investment or as a project in the financial management course and master thesis, students are expected to be able to practice the four-strategic themes in decision making; sensemaking, resource allocation, strategic positioning, and learning.

In addition, business case development can be further cultivated from extra curricula activities and programs, such as those carried out by the Executive Development Program and DERU-UGM. The business cases should be brought into class discussion and if possible, to be further investigated as a master thesis by MMUGM's students.

CONCLUSION

Master of Management, Universitas Gadjah Mada (MMUGM) will continue its initiatives in developing business cases based on real problems using Indonesian setting. The illustrative case used in this paper is an example of one of the initiatives to incorporate disaster risk management issues into school of business' curricula. The real options analysis is not only a decision making tool but also a paradigm on how to deal with risks or uncertainties, including those man-made or natural disasters. The case also illustrates an example for the needs of businesses in a disaster-prone country like Indonesia, which needs to work in partnership with business schools to find solutions.

Specific business cases with a central theme of disaster risk management are already available from the activities and programs performed by the Executive Development Program (EDP-MMUGM) and Disaster Response Unit (DERU-UGM). Students who are interested in this topic could write a thesis based on recent issues in disaster risk management. The written cases could then be used as a learning process for further discussion and development in response to current real business issues.

2 The business case presented in this paper is fictional (the names, places, numbers, etc.), but it offers real dilemmas and decision making context that is based on real business case.

3 Thanks to Evi Novita Dewi, MBA for her contribution to this business case, and part of the business case is her master thesis in MM-UGM.

4 Field Work Experience (KKN/Kuliah Kerja Nyata as in Indonesian language) is a 3-credit course that all undergraduate students of UGM must take. A community service program requires groups of students to go into area in needs for 1-2 months. Each group usually consists of 30 students from different faculties. Students are required to make an activity plan that utilize their knowledge/area of study, carry out the plan, and to measure the results.

REFERENCES

Brigham, E.F. & Ehrhardt, M.C. (2014). Financial Management: Theory and Practice. Cengage Learning: South-Western. [ Links ]

Mun, J. (2002). Real Options Analysis: Tools and Techniques for Valuing Strategic Investments and Decisions. New Jersey: John Wiley & Sons, Inc. [ Links ]

Sipp, C.M., & Carayannis, E.G. (2013). Real Options and Strategic Technology Venturing. New York: Springer. [ Links ]

Bowman, E.H., Hurry, D. (1993). Strategy through the option lens: an integrated view of resource investments and the incremental-choice process. Academy Management Review, 18(4):760–782. [ Links ]

UNISDR. (2013). Global Assessment Report on Disaster Risk Reduction 2013. UNISDR. Retrieved from http://www.preventionweb.net/english/hyogo/gar/2013/en/home/index.html [ Links ]

Gaudard, L. & Romerio, F. (2013). Natural hazard risk in the case of an emergency: the real options' approach. Natural Hazards, 75(1), 473-488. DOI: 10.1007/s11069-014-1330-1 [ Links ]

Copeland, T. & Tufano, P. (2004). A Real-World Way to Manage Real Options, Harvard Business Review. Retrieved from: https://hbr.org/2004/03/a-real-world-way-to-manage-real-options [ Links ]

Andersen, T.J (2003). Globalization and Natural Disasters: An Integrative Risk Management Approach, in Kreiner A., Arnold, M., and Carlin, A. (Editors), Building Safer Cities: The Future of Disaster Risk, Disaster Risk Management Series No. 3, World Bank. [ Links ]

Maseda, L.J. (2008). Real Options Analysis of Flexibility in a Hospital Emergency Department Expansion Project, a System Approach. Thesis for Master of Science in Engineering and Management, Massachusetts Institute of Technology. [ Links ]

Woodward, M., Gouldby, B., Kapelan, Z., & Khu, S-T. (2011). Real Options in Flood Risk Management Decision Making. Journal of Flood Risk Management, 4(4), 339-349. DOI: 10.1111/j.1753-318X.2011.01119.x [ Links ]