English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

Permalink

Introduction

Latin America is a region with high levels of perceived corruption and with significant losses due to fraud and embezzlement by companies and government agencies (ACFE, 2020; Transparency International, 2019). There was identified a large network of corruption between companies and government officials that began in Brazil and spread to other countries such as Argentina, Bolivia, Colombia, Cuba, Ecuador, Guatemala, Mexico, Panama, Peru, Dominican Republic, Venezuela revealed in the wellknown Car Wash operation (BBC, 2018; Época, 2016; Maragno & Borba, 2019; Sallaberry et al., 2020).

Fraud consumes approximately 5% of annual revenues, an important part of organizations (ACFE, 2020). These are resources that hinder the performance of organizations, increasing costs, reducing the competitiveness of the companies involved or consuming public services that should be available to the population.

Whistleblowing is the most efficient mechanism for detecting fraud in Latin America and the Caribbean, higher than the global average (ACFE, 2020). Whistleblower behavior stems from the communication of someone who knows the facts to anyone who can avoid or correct such problem (Near & Miceli, 1985).

Several conventions illustrate international efforts to promote measures to prevent and tackle financial crimes, such as bribery, money laundering and corruption (OECD, 2018; OAS, 2020; Hauser, 2019; UNDOC, 2018). However, the amount of reports of suspicious transactions to Financial Intelligence Units (FIUs) is quite small in some countries (Gomes et al., 2018; Sallaberry & Flach, 2019).

The whistleblower theme is relevant, generating studies in developed countries such as the USA and the United Kingdom, and in emerging economies, such as Africa (De Maria, 2005; Soni et al., 2015), Barbados (Alleyne et al., 2013), China (Zhang et al., 2009), Malaysia (Rachagan & Kupusamy, 2013), and South Korea and Turkey (Park et al., 2008). However, many studies arbitrarily assume direct measures selected or adapted from previous studies, which results in measures with low reliability and underestimation of relationships (Ajzen, 2006). In Latin America, there is a gap in research developed based on local beliefs about reporting financial fraud and financial crimes.

Behavior is an element that has great influence on the moral orientation of the individual and the culture in which he is inserted (Culiberg & Mihelic, 2017; Kim & McKercher, 2011; Rausch, Lindquist, & Steckel, 2014). Countries and regions exhibit different behavior in relation to whistle-blowing behavior (Park et al., 2008; Pillay et al., 2015). That demands the identification of the specific beliefs of individuals in Ibero-America.

The whistleblower strategies of financial crimes applied in the Ibero-American environment more successful prediction depend on the knowledge of the beliefs of local individuals. Considering this, the research aims to identify the behavioral beliefs of Ibero-American individuals about the reporting of suspected financial crimes, segmented in the Brazilian and Hispanic-American contexts.

Understanding the determinants of behavior in the Ibero-American environment, it would be possible to evaluate and intervene to stimulate whistle-blowing behavior. The results can help to understand the influences that Ibero-American individuals receive to make a complaint. Based on the identification and analysis of beliefs, it is possible for regulators to develop more adequate control mechanisms since the reaction of the professional is different from one culture to another (Albrecht, et al., 2012; Lee et al., 2018; Macnab et al., 2007).

The results of the research can make a relevant contribution to society by addressing the main mechanism for identifying financial crimes - the whistleblower (ACFE, 2020). The complaint is even more relevant in Latin America and the Caribbean, being important in the identification of crimes with a financial aspect (Alleyne et al., 2017; Céspedes et al., 2017).

The knowledge of the beliefs of individuals is important for managers in the construction of work team ethics and behavior (Liu & Ren, 2017). Besides, control beliefs are especially useful in modeling control systems that mitigate opportunities for fraud to occur (Gibbs, 2020; Triantoro et al., 2019).

Whistleblower Literature

The whistleblower theme is relevant, generating studies in developed countries and emerging economies (De Maria, 2005; Gundlach et al., 2003; Guthrie & Taylor, 2017; Soni et al., 2015; Alleyne et al., 2013; Zhang et al., 2009; Rachagan & Kupusamy, 2013; Park et al., 2008). The explanation for taking corrective action through a complaint is a relevant gap and needs further analysis (Miceli et al., 2008; Alleyne et al., 2013; Guthrie & Taylor, 2017).

Whistleblowing is widely considered positive and encouraged behavior in the workplace (Park & Blenkinsopp, 2009). The complaint is an action carried out based on a complex psychological process and depends on the confidence or belief that the irregularities will be corrected (Gundlach et al., 2003; Soni et al., 2015). Whistle-blowing channels are mechanisms implemented by organizations and the State to receive reports and assist in the prevention or correction of irregularities (Alleyne et al., 2017).

To modify the behaviour, interventions can be directed to their determinants when individuals have control over behavior (Ajzen, 2006). The psychological literature has several theories useful to explain behavioral determinants, among them the theories of rational action and the theory of planned behavior consolidated in the theory of reasoned goal pursuit.

The rational action theory assumes that people tend to behave rationally and systematically use the information that is made available to them when they decide to act or not (Ajzen & Fishbein, 1980; Fishbein & Ajzen, 1975). Behavioral intentions are determined by the attitude towards behavior and the subjective norm towards behavior, still considered to be the best predictors of intention (Ajzen, & Kruglanski, 2019). The theory of later planned behavior incorporated the perceived control over behavior (Ajzen, 2019). These determinants would be able to explain the behavioral intentions of the individuals and consequently a way to predict the behaviors of a person.

A behavioral belief is the subjective probability that the behavior will produce a certain result. Normative beliefs refer to the behavioral expectations, perceived by the individual from groups of people whose opinion is relevant (Ajzen, 1991). Behavioral control refers to people’s perception of their ability to perform certain behaviors.

Even if a person strongly desires to perform a behavior, he/she may not have the necessary opportunities or resources, such as knowledge, money, skills, information, time, equipment and cooperation from others to actually do it (Kuhl, 1985; Liska, 1984; Sarver, 1983; Triandis, 1977). To improve the predictive capacity of behavior, Ajzen and Kruglanski (2019) incorporated the individual’s goals because the behaviors serve as a means for the individual to achieve their goals.

Attitude Beliefs

Behavioral beliefs link the behavior of interest to the expected results and experiences (Ajzen, 1991). A behavioral belief is the subjective probability that the behavior will produce a certain result or experience. The attitude towards a behavior is therefore the positive or negative feeling about the execution of the target behavior (Ajzen, 2011; Trongmateerut & Sweeney, 2013).

These are beliefs about the likely outcomes of behavior and the assessments of those outcomes, behavioral beliefs (Chang et al., 2017; Park & Blenkinsopp, 2009). Although a person may have many behavioral beliefs in relation to any behavior, only a relatively small number are readily accessible at any given time (Ajzen, 1991).

It is assumed that these accessible beliefs - in combination with the subjective values of the expected results and experiences - determine the predominant attitude towards the behavior. Specifically, the evaluation of each result or experience contributes to the attitude in direct proportion to the person’s subjective probability that the behavior produces the result or experience in question (Ajzen, 2019; Park & Blenkinsopp, 2009).

The attitude towards a behavior is determined by the total set of behavioral beliefs that link the action to a given result or experience. This attitude is the degree to which the performance of the behavior is valued in a positive or negative way. The attitude considers the extent that he agrees or disagrees with a certain behavior, and if the action causes an adverse effect, he will be reluctant to report it (Tarjo et al., 2019).

The strength of each belief is weighted by the evaluation of the result, and the products are aggregated (Ajzen, 1991). In their respective aggregates, behavioral beliefs produce a favorable or unfavorable attitude towards the behavior. To measure an attitude towards the complaint, individual assessment of potential results is measured when reporting the irregular fact, as an example when reporting a theft will avoid losses for the company (Brown et al., 2016).

Park and Blenkinsopp (2009) attribute the positive results of a complaint to preventing damage to an organization, controlling corruption, valuing the public interest, functional duty and moral motivation, etc. Brown et al., (2016) reported incentives such as financial and moral, such as ethics. Other prospects may consider to be unfavorable the potential results of social isolation, verbal and physical violence, job monitoring, discomfort, disharmony, demotion, nonpromotion, dismissal, sanctions, reputation damage, other charges and blacklisting (Cassematis & Wortley, 2013; Chang et al., 2013; Chang et al., 2017; Dalton & Radtke, 2013; Mesmer-Magnus & Viswesvaran, 2005; Seifert et al., 2010).

Subjective Norm

Normative beliefs refer to the behavioral expectations, perceived by the individual from important reference groups (Ajzen, 1991). An individual’s attitude towards complaints also depends on his internalization process and identification of related opinions (Lewis et al., 2014). This aspect presupposes that these normative beliefs-in combination with the person’s motivation to fulfill external expectations-determine the current subjective norm. The motivation to fulfill expectations contributes to the subjective norm indirect proportion to the probability of the reference person’s expectation contributing to the realization of a behavior (Ajzen, 1991; Mesmer-Magnus & Viswesvaran 2005).

The subjective norm can be considered as the perceived social pressure to be involved or not in a certain behavior (Park & Blenkinsopp, 2009). They represent the individual interpretation of the opinions of other important people in relation to the behavior in question (Cialdini & Trost, 1998; Trongmateerut & Sweeney, 2013). Being accepted by its referents is an important objective (Tarjo et al., 2019). Specifically, the strength of each normative belief is weighted by the motivation to comply with the corresponding referent, and the products are aggregated.

Individuals trust relevant members of the community to understand and respond effectively to social situations of uncertainty (Cialdini, 2001; Trongmateerut & Sweeney, 2013). An interesting possibility is highlighted by Moan and Rise (2006) who segregated and examined three types of normative influences: injunctive norms (social approval and disapproval of the behavior of other individuals), descriptive norms (behaviors that others are doing) and moral norms (behaviors that are right or wrong). When complaints are accepted in the social environment and by important people, who indicate similar opinions, more individuals tend to report irregularities (Tarjo et al., 2019). Reporting behavior can be influenced when management gives employees an understanding of the importance of reporting an irregularity, in addition to being affected by the opinions of an important referent (Cialdini & Goldstein, 2004; Tarjo et al., 2019).

Important references for a whistleblower are family members, co-workers, immediate supervisor, friends and neighbors (Park & Blenkinsopp, 2009). Brown et al., (2016) included shareholders, senior financial management, company culture, other professionals in the same category and financial regulatory agencies, as the relevant referents.

Perceived Controls

Control beliefs are related to the perceived presence of factors that can facilitate or impede the performance of a behavior. Obstacles or risks to the effectiveness of a behavior are known as control factors, and it is attributed that beliefs are influenced by several other antecedents, such as experiences, third party information about the behavior, among others (Ajzen, 1991; Park & Blenkinsopp, 2009).

Perceived behavioral control refers to people’s perception of their ability to perform certain behaviors by regulating the influence on whistleblower behavior (Chiu, 2003). The perceived control of each factor to prevent or facilitate the performance of the behavior contributes to the perceived behavioral control in direct proportion to the person’s subjective probability of perceiving the presence of that control (Ajzen, 1991).

The strength of each control belief is weighted by the perceived intensity of the control factor, and the products are aggregated. Insofar as this belief is an accurate reflection of real behavioral control, perceived behavioral control can, together with intention, be used to predict behavior (Ajzen, 1991). Perceived behavioral control - as a proxy for real control - moderates the effect of intention on behavior, so that a favorable intention produces behavior only when the perceived behavioral control is strong (Ajzen, 2011).

Organizational support represents an important set of determinants to encourage whistle-blowing behavior (Cho & Song, 2015). Among the factors that can make a complaint difficult are beliefs about the organization making difficult or ignoring reports, difficulties in making the complaint, inability to correct errors and retaliation by the organization (MesmerMagnus & Viswesvaran, 2005; Park & Blenkinsopp, 2009). Beliefs favorable to complaints can be the protection of the whistleblower, supported by company (Chang et al., 2017; Gorta & Forell, 1995).

Brown et al., (2016) highlight the support of the internal control system, prevention of financial losses, retention of the integrity of the accounting profession, job retention and maintenance of positive career direction. Other important elements for whistleblower behavior can be included, such as: knowledge of the behavior; the experiences of other people; the existence of resources; the perceived intentionality of the offender; the magnitude; the severity; the amount of evidence of complaints; the institutional policies; whistle-blowing legislation; reporting channels; and the presence of compelling evidence (Brown et al., 2016; Dworkin & Baucus, 1998; King, 2001; Near & Miceli, 1985; Keenan, 2000; Tarjo et al., 2019; VandekerckHove & Lewis, 2012).

Objectives and Goals

Behavior serves as a means to achieve the individual’s goals in the light of alternative options (goals when not the behavior itself) and in the context of the individual’s current active goals (Ajzen & Kruglanski, 2019). Objectives constitute a result or state in which people want to achieve and remain through their actions (Kruglanski, 1996).

Each goal has a magnitude that reflects its convenience, the degree to which it is desired, and also the likelihood that its achievement is within reach, and so goals are the central motivators of behavior (Kruglanski et al., 2014). The motivational context must be considered to understand and predict the occurrence of a behavior.

Some moral characteristics can be confused between desired goals, with behavioral results and as conditions for behavioral control, since high or ‘pure’ moral statuses can be a condition and purpose of the whistle-blowing behavior (Brown et al., 2016; Callahan & Dworkin, 2000; Dozier & Miceli, 1985; MacGregor & Stuebs, 2014; Oliver, 2003). Other considerations such as organizational loyalty and silence, severity of consequences, also have the capacity to influence the complaint (Miceli et al., 2009; Near et al., 2004; Hassink et al., 2007).

The whistle-blowing context includes people’s active goals and their perception of the degree to which contemplated behavior (in comparison with other possible actions) is likely to promote those goals. When more than one behavioral option can achieve an active set of goals, the alternative associated with the strongest intention is selected (Ajzen & Kruglanski, 2019).

The whistle-blowing behavior is encouraged in the organizational environment of high ethical values, but that is not always triggered at any time, due to beliefs of lesser magnitude. Another rationalized option could be remaining silent permanently or temporarily until certain conditions are reached (Brown et al., 2016).

Research Method

The survey employed interview procedures and content analysis to identify whistleblower beliefs of business professionals. The sample choice of business professionals is relevant because these professionals work daily with financial and patrimonial resources, the main input for white-collar crimes.

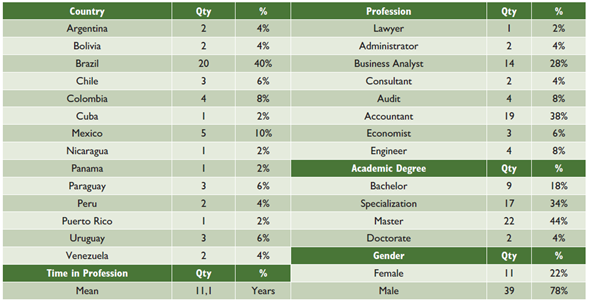

Self-reported social norms are more effective than organizational rules to influence the intention to report (Feldman & Lobel, 2008; Trongmateerut & Sweeney, 2013). This strategy allows exploring more options, alternatives, and perceptions than the closed The survey of the data occurred from structured interviews with business professionals from Latin America, sent by electronic form. These professionals were selected randomly in professional networks intentionally due to their area of expertise and training, obtaining 50 responses, detailed in Table 1. For access to respondents, search was carried out on the professional network LinkedIn by professionals in the business area, based on the criteria of the selected countries, with professional ties on researcher of first and second degree.

After the first connections, applying the snowball strategy to acquire legitimacy with potential respondents, new professionals were invited. For the 240 invitations for connections sent, 130 professionals accepted the connection and for the 95 (39.5%) first professionals who accepted to receive the questionnaire, and 50 (52.6%) complete answers with internal validity were obtained. As the last five responses did not add new subcategories of behavioral beliefs, we considered that the collection reached a saturation level and therefore we stopped sending new questionnaires to other connected professionals.

The sample of 50 respondents was intentionally obtained from business professionals in the Ibero American, of which 60% were from Hispanic countries and 40% were Brazilian respondents. Respondents showed a diversity of specializations in accounting, administration, finance, compliance, economics, compliance, forensics, auditing, money laundering, continuous improvement, ethics.

Individuals demonstrate knowledge and skill from an average experience of over 11 years and 82% of respondents with a specialist or higher education level. Gender diversity was found to be concentrated in the male gender with 78% of respondents, although invitations were sent to similar proportions.

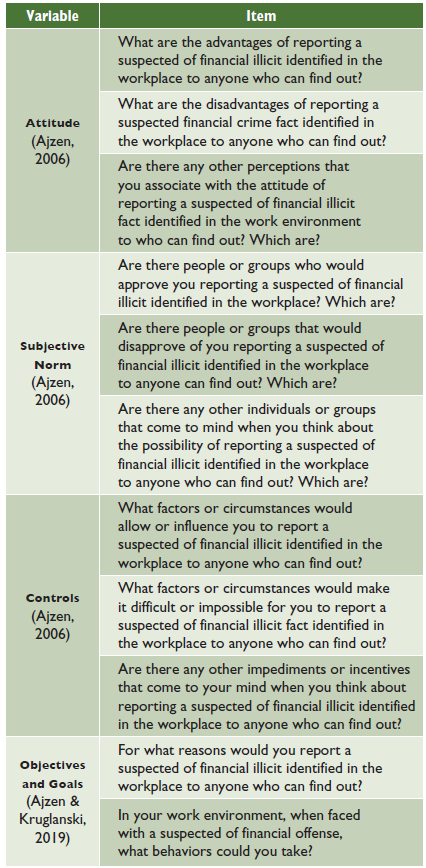

The instrument sought to capture the characteristics of the respondent professionals and the determining elements of the reporting behavior. Three questions were established for each of the three traditional variables (Attitude, Subjective Norm and Controls), goals and motivations, as well as the perceptions of suspicious or illicit facts and the recipients of complaints.

The instrument’s structure follows the protocol established by Fishbein and Ajzen (2010), through the initial proposal of the investigated behavior as “Report of suspected financial illicit identified in the work environment to anyone who can find out”, which characterizes the whistleblower. Before applying the research instrument, the questionnaires were translated into local languages, Spanish and Portuguese, with the adoption of back-translation procedures and analysis by a local specialist, in addition to a pre-test for external validation (Brislin, 1980; Yin, 1994).

Respondents were asked to respond to immediate thoughts restricted to the personal opinions of these professionals, using the instrument shown in Table 2.

The content analysis technique allows a phenomenological perspective for interpretative data analysis (Bardin, 2016). In the categorization process, under the premise of deriving from a single principle of classification, the set of established categories derives from the behavioral determinants segregated previously in the structuring of the interview form.

Subsequently, subcategories of beliefs, referents, objectives, and controls are collected from the interviews by codifications developed from the responses. The content analysis of the responses of the instrument results in lists of salient modal results, referring to the various relevant positive and negative aspects. Due to the methodological choice to face limitations of space, we chose to present the summary of results in tables for all beliefs, which are discussed in light of the evidence that already exists in the literature in other environments. Considering the possibility that one of the great cultural influences existing in the American continent is its exploration and colonization, this distinction is represented quite clearly in the colonial language: Portuguese America and Spanish or Hispanic America.

Analysis

The initial analysis started from the survey of the items of the categories and subcategories of the research, segmented by the main geographic regions, Hispanic America and Brazil. Subsequently, these elements were analyzed individually and discussed in light of the theoretical referential.

The number of countries in Latin America made it impossible to analyze them together, as there are many socio-cultural differences between countries. We apply one of the main characteristics of segregation of this sample set, that is the cultural orientation that stems from its historical and colonial formation, whose Hispanic countries were strongly influenced by Spain, while Brazil by Portugal. This segregation divides the sample into a reasonable proportion of population and territorial size. Furthermore, cultural aspects exert a significant influence on the development of personal beliefs.

Attitude Beliefs

Beliefs are relevant to the individual because they represent the results expected by the individual for a given behavior (Ajzen, 2019). The intention is predicted by the importance that the individual attributes to this result in a considered way.

It is unlikely that an individual will make a complaint if the individual does not believe that this behavior will generate the expected result (Park & Blenkinsopp, 2009). These beliefs tend to reflect environmental conditions, such as the culture and maturity of organizations. Although fraud and financial crimes are misconduct that occur globally, strategies and preferences are often different (Park & Blenkinsopp, 2009).

The results considered by the individual resulting from a complaint may be favorable or unfavorable to the complainant, influencing the decision to conduct the behavior. To extract the individuals’ beliefs, the analysis subcategories were analyzed: favorable and unfavorable results.

The elements favorable to a whistle-blowing behavior were asked to the interviewees by questioning what the advantages of would be reporting a suspected financial illicit fact. In the different regions, the results obtained showed small distinctions, as shown in Table 3.

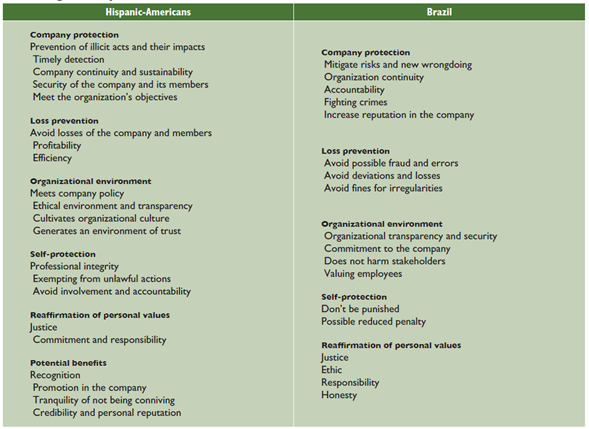

From the analysis of the elements, they were classified into variables of advantages for the Hispanic American interviewees resulting from complaints about the protection of the company, the prevention of losses, the organizational environment, self-protection, the reaffirmation of personal values and other potential benefits for the whistleblower. In macrostructures, it would be possible to characterize them as advantages for the organization and for the individual.

Company protection is one of the most recurrent variables for individuals and it is reported that the complaint results in procedures and investigations that prevent the occurrence of fraud and illicit occurrences as well as pedagogically inhibit the occurrence of new deviations. These actions add security to the company and its members since the criminal environment tends to attract other agents and related crimes, impairing the achievement of the organization’s main objectives. The complaint is pointed out as a strategy for the timely detection of deviations corroborating the whistleblower literature (ACFE, 2020), in addition to allowing the continuity and sustainability of the business in the long term, which could be shaken due to the aggravation of fraud and crimes.

The complaint mitigates criminal conduct but also its consequences, mainly due to the financial losses of the facts and their potential punishments. Hispanic-American respondents report the impact on the organization’s profitability and efficiency.

The reduction in profitability can result from the deviations of the company itself or from the payment of fines and indemnities, in addition criminal practices can reduce the operational efficiency of companies participating in cartels, which naturally reduce the effects of market efficiency, since they do not demand competition for price and quality.

In the different contexts, the advantages for the organizational environment reported were similar, since complaints of illicit and resulting suspicions usually meet the organization’s policies and codes of ethics. Individuals report whistleblower behavior as an element of encouraging transparency and organizational culture, creating an environment of trust between colleagues and procedures.

Respondents claim that the complaint results in the reaffirmation of personal values such as justice, commitment, and responsibility. Notwithstanding moral values, they also address the need for self-protection of individuals since reporting a suspicious or unlawful fact can exempt the whistleblower and avoid liability. Reporting can be a way of protecting the reputation and integrity of the reporting professional, hence the relevance of the self-protection dimension.

E20: “It is the proper conduct, the advantages can be: avoiding the illegality to continue, preventing other people from being harmed, investigating the facts and holding those responsible.”

E44: “Depending on the place that the person occupies within the organization chart, I could receive some kind of acknowledgment, the tenure in care to occupy the highest responsibility within the organization.”

Hispanic-American respondents, unlike Brazilian sample, indicated that reporting can generate potential benefits for whistleblowers, such as personal recognition for suitability and even promotion by demonstrating loyalty to the organization. In reinforcement of personal values, but still as a benefit directly to the whistleblower, tranquility is reported for not being complicit with such acts and improving credibility and personal reputation. The elements with results that are unfavorable or whose results of a denouncing behavior are undesirable were asked to the interviewees by asking what the disadvantages of would be reporting a suspected financial illicit fact in the work environment. In the different regions, the results obtained showed similarities, with few exceptions, as shown in Table 4.

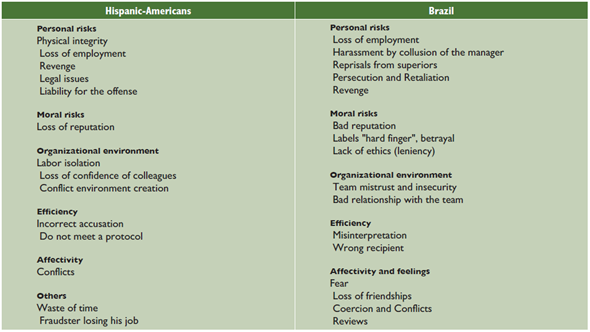

The disadvantages reported by the individuals were initially categorized into personal and moral risks variables, related to the organizational environment, the effectiveness of the complaint, the affectivity of the individual and others. The report in the Spanish-American environment highlights the report of risks on the physical integrity of the whistleblower, among the personal risks, which besides being differential can be considered the risk of greatest impact-the life of the whistleblower or its referents.

Other Personal Risks were reported with recurrence by individuals as the possible loss of job, persecution and revenge of other members of the organization, which corroborate the evidence of Sallaberry and Flach (2021) in the Latin American environment. The personal risks indicated also consider potential legal problems of litigation and possible liability for the offense, since in some cases, the accused could be pursued and involved by managers and colleagues regarding acts that occurred prior to the complaint.

E79: “Persecution, revenge, disagreements”.

The interviewees pointed out Reputation Risks resulting from a wrong or even correct report, when they do not have the approval of the other teammates. This risk is related to other problems that can happen in the organizational environment, mainly the job isolation of the whistleblower, since colleagues may fear being reported. In the Brazilian context, these perceived moral risks include the risk of having labels of betrayal attributed by their colleagues, or even a lack of ethics lenient to colleagues.

The organizational environment offers other challenges to an individual’s intention to report. The loss of confidence of colleagues, an environment of conflict with colleagues, mistrust, insecurity and poor relationship between the team of the accused and other related persons, all these possible results are unfavorable for making a complaint.

E49: “Co-workers can isolate or block their work, so that the performance is not adequate. Or worse yet, they can attempt against your life, indirectly (they send other people to harm you).”

The unfavorable category of effectiveness considers the possibility of the individual to make mistakes at the time of the complaint, which may occur from an incorrect complaint, which was carried out without enough elements or for not complying with an organization protocol. Since error is inherent in the decision-making process, such results mitigate the interest in making the complaint, given the other undercurrent consequences of this behavior.

In the Hispanic-American environment, the whistleblower’s affectivity is mentioned less frequently, yet the possibility of conflicts is a disturbing and unwanted consequence, so it reduces the possibility of the complaint. In this same context, other factors are reported by the interviewees, such as the loss of time with the complaint and the possible consequences for the accused. The Brazilian respondents pointed out, as unfavorable results of a complaint, some feelings such as loss of friendships, coercion, and conflicts in the workplace, in addition to criticism from colleagues.

E56: “Personal differences, whether they are effective or professional. Ambition among officials from different areas”.

The loss of time is an intricate response in a lenient organizational context with illicit conduct, since the expected result does not meet the objective of a complaint. Finally, the consequence for the reported individual is also perceived as a nuisance to the whistleblower, since it is possible that complaints result from errors or from suspicions that need to be investigated by the control sectors, and a rigid interpretation of the complaint can cause too much consequence to the respondent, greater than acceptable by the complainant. These were not factors pointed out by the Brazilian interviewees.

Subjective Norm

Normative belief attributes the fulfillment of the observed action to the expectation of relevant people (Ajzen, 1991). These beliefs about the expectation of these referents and the respective importance that each referent has for the whistleblower influence the behavior.

For the analysis of whistleblower behavior, the relevant referents tend to be related to the work environment, although not limited, where the action can be perceived (Park & Blenkinsopp, 2009). This subjective norm can be considered as the perceived social pressure to be involved or not in a certain behavior.

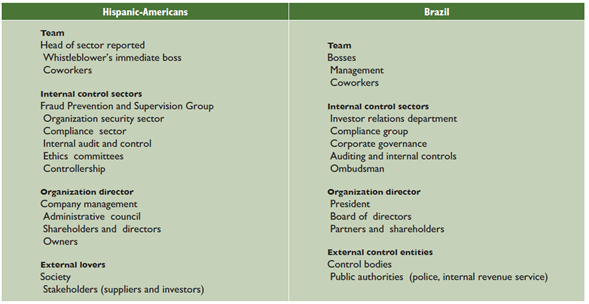

Beliefs about the subjective norm of individuals were collected by questioning which people and groups would approve the individual to report a suspected financial offense. The analysis subcategories were segregated in terms of approval and disapproval of the whistleblower conduct, and then in the variables of team, internal control sectors, organization management and external entities, detailed in Table 5.

Hispanic-American respondents attach importance to the Work Team in deciding whether to report a suspicious fact. Among the referents of the team, we highlight the immediate boss and the head of the unit who reported the fact, who would be the immediate representatives of the organization’s management. This group also includes co-workers who value the established behavior as an ethical conduct.

The Internal Control Sectors, although depersonalized, are considered as relevant references for whistleblower behavior, which is rational since they are units whose technique is an input for the success of their work. These sectors were indicated as the sectors of fraud prevention and supervision, organization security, compliance, audit and internal control, controllership, and ethics committee.

E45: “Yes, Management, Direction, Compliance Officer. The institution”.

E64: “Internal control, compliance. The owner of the company-if he is not the one who commits the act”.

Hispanic-American respondents assign the company’s owners as referents to the organization as much as possible. In broader organizations, the direction of the company, the board of directors, shareholders and directors were indicated. This perception considers the size of the organization in the indication of posts of interest since they would be the most interested in protecting the company’s assets. As companies are smaller, it increases the risk that those involved are closer to the management or the whistleblower.

External Entities are also considered as relevant approval referents for the complaint. For Hispanic-American respondents, the referents indicated were society at large and stakeholders, such as suppliers and investors. The company disapproves of these illegal conducts and therefore the complaint is approved, as well as the suppliers and investors who have credits in the organization and are not interested in the liquidation of the organization.

In the Brazilian context, respondents considered the investor relations department in publicly traded corporations, which in principle has no role in investigating suspicious situations, but which can receive reports from investors and third parties. Outside the company, public bodies with police and tax inspection powers were appointed, whose denunciation is an instrument of work and investigation. In short, the manifestation of important referents tends to make it clear to collaborators the magnitude of approval of the complaint.

The disapproval of referents for the individual can also influence the interest of reporting, as the disapproval of this conduct by a person considered relevant can mitigate the ability to decide. Respondents were asked to indicate which people or groups would disapprove of the report of the suspected financial offense, which were segregated into variables of the Reported and related and of the Work Teams, detailed in Table 6.

The interviewees highlighted as groups that would disapprove of such behavior the criminals reported and their referents, as the denounced and suspects who could naturally feel harmed. It is important to highlight that the investigated behavior of whistleblower was indicated as suspicious of illicit facts, not necessarily a proven fact, which depends on a formal investigation.

In the Hispanic-American environment, interest groups were reported as friends of the accused and people with emotional ties. Due to the affectionate bond with those reported, these individuals may disapprove of such conduct, especially if there is no clear and robust evidence, or even existing, by denying the evidence.

E49: “Possibly friends or acquaintances whom suspected of fraud”.

In the work environment, there may be referents who disapprove of the complaint, reported as people interested in maintaining the organization’s status quo, that is, before the complaint and the maintenance of any illegal activity. In addition, it was indicated that syndicates may disapprove of the conduct, since the conduct of these entities is usually the protection of employees in conflict, such as the one denounced.

Perceived Controls

The perceived controls represent elements that facilitate or impede the performance of a behavior (Ajzen, 1991). Control beliefs combine the perceived strength of each control and the perception of the control’s presence, which together influence the decision to perform the behavior.

This perceived behavioral control represents the ability to perform the behavior. Behavioral control indicates the availability of skills, resources and tools necessary to perform whistleblower behavior (Park & Blenkinsopp, 2009).

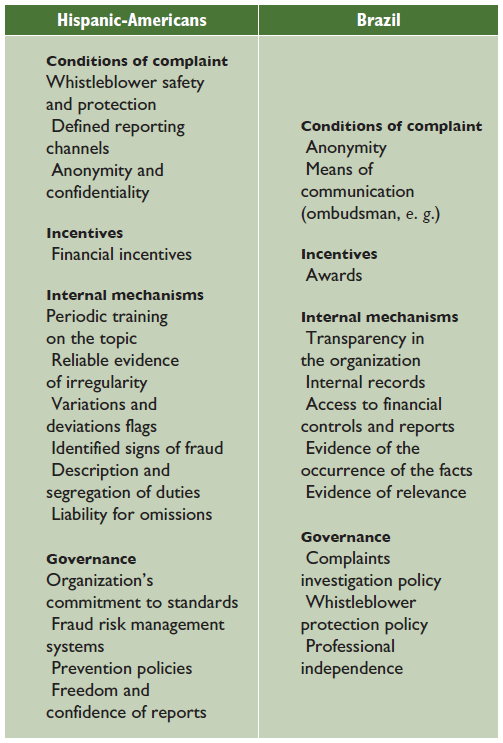

The survey of the necessary and facilitating conditions for the occurrence of the complaints was explored by questioning the factors or circumstances that would allow or influence the report of a suspected financial illicit fact. The analysis of the respondents’ answers allowed the categorization into variables of conditions, incentives, mechanisms and governance, detailed in Table 7.

The Hispanic-American respondents report in the variable conditions of denunciation the safety and protection of whistleblowers, since it is even one of the risks pointed out by the disadvantages of whistleblower behavior in this context. Among the reporting conditions, the existence of clearly defined reporting channels and anonymity and confidentiality, which are typical characteristics of reporting channels, were also pointed out (Alleyne et al., 2017).

Reporting channels are reported as relevant mechanisms that repeatedly condition the practice of reporting by respondents. The very existence of a whistle-blowing channel already highlights the value of this conduct, and therefore favors the employee’s propensity to report suspicious situations. The indication of anonymity and confidentiality is one of the possible strategies to be used in the reporting channels. Anonymity and confidentiality would be conditions that, in the event of a denunciation, would mitigate a large part of the risks and negative implications perceived by the denouncer.

E13: “anonymous report, and the company has a well-structured compliance program, where the whistleblower will not be punished, and the denounced act will be investigated”.

The interviewees perceive the financial incentives as a factor that could influence an eventual denunciation. Still, it is not an accepted element in the legislation of all countries. The internal mechanisms variable addresses technical conditions for the rationalization and legitimization of evidence as suspicious or illegal facts. Among these mechanisms, in the Hispanic-American environment, there was an indication of the need for training, signs of variations, indicators of deviations and signs of fraud, descriptive and segregation of functions, as well as accountability for eventual omissions.

The interviewees highlighted the relevance of indicators that can indicate deviations from behaviors and variations, through flags. These signals, also known as red flags, attribute to the individual impersonal evidence of discrepancy allowing greater security to carry out the reporting of the abnormal situation. Training on the subject is also listed as a favorable condition for affirming the individual’s effectiveness as well as for the dissemination of institutional guidelines and policies. Finally, accountability for omission is reported as a determinant, as it would not be possible to deny the fact for lack of evidence, but only for the negative evidence.

E56: “When I observe variations in indicators with respect to standards”.

The Governance variable is already recognized in the literature through prevention policies and standards that establish guidelines and guidelines for employees. These factors are reported by individuals as elements that contribute to greater safety in making the complaint, expressed through the commitment of the organization, fraud risk management systems, prevention policies, as well as freedom for employees to make their reports and the trust of the company. In the Brazilian environment, the importance of professional independence was reported, mainly attributed to regulated professions and linked by the legislation to prevent money laundering.

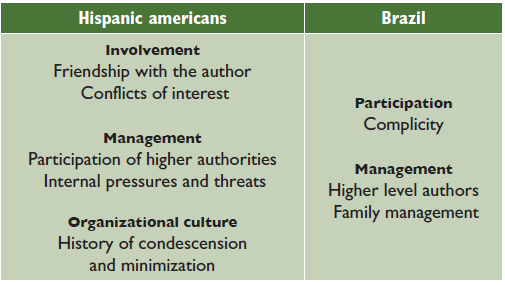

The analysis of the subcategory of unfavorable or limiting control beliefs was developed positively, since the negative presentation of unfavorable elements is the positive manifestation of favorable elements already presented among the favorable control beliefs. The survey started by asking respondents about factors or circumstances that would make it difficult or impossible to report a suspected financial crime, detailed in Table 8.

The variables reported to limit the possibility of denunciation that result from the involvement of the individual in some way in the fact, the management of the company and the organizational culture. Hispanic-American respondents reported that any indirect involvement of the whistleblower can be characterized by friendship with the perpetrator of the fact and conflicts of interest if he has also benefited from the fact, or enmity between both. For Brazilians, complicity in the offense would be a significant limitation on the effectiveness of the complaint.

E37: “If the suspect were from senior management, there would be no security in maintaining anonymity”.

Some characteristics were related to the participation of managers from higher levels or due to an environment of constant internal pressure and threats to the individual. The characteristics of the organization reported indicate that a history of condescending and minimizing previous complaints would signal to the individual that a complaint would be ineffective. The family management of companies, more typical in smaller businesses, was also pointed out by Brazilian interviewees, since there are ties that go beyond the professional relationship.

E44: “If there is a history that the complaints do not come to fruition or have resolutions that turn against the complainant”.

Objectives and Goals

The denouncing behavior before the theoretical elements serves as a means to achieve an objective (Ajzen & Kruglanski, 2019). In the theoretical perspective, these objectives are prior to the complaint and aimed at achieving a result. This central objective weighted by desirability reflects the convenience and the probability that it will be realized.

The exploration of the potential objectives that lead an individual to report were explored from the questioning on what reasons would influence respondents to report a suspected financial illicit fact. The objectives presented by the interviewees were classified into three variables of personal values, utilitarian and organization, detailed in Table 9.

All the stated objectives are broad and have a limited capacity to be reached only through a complaint, even though the actual behavior may cultivate the specific objective. Respondents indicated personal values of ethics, justice, integrity and honesty.

E20: “For ethics, to cooperate with justice, to contribute to the fight against money laundering and/or other financial crimes”.

Utilitarian objectives and organizational values are more latent compared to referents, and while utilitarian, respondents pointed out the benefit of the team and the work environment, in addition to self-protection. The benefit of the team and the work environment achieved by the complaints may not be as evident and measurable, but the risk of not reporting and being revealed is relevant, influencing the appreciation of whistleblower behavior.

E45: “For professional integrity, for ethical principles. To protect my image”.

Organizational elements are also relevant because they are attributed to culture, heritage preservation and organizational commitment as objectives that can be achieved by making a complaint. The complaint allows the maintenance of organizational behavior, reflected in a status or reputation. Thus, like other values, it can be perceived by realization but whose main impacts may be affecting non-realization in the future.

Goals represent the alternative options that an individual has to achieve a specific goal (Ajzen & Kruglanski, 2019). They can be considered as intermediate objectives to achieve an objective of later assessment. Active goals represent the perception of how the contemplated behavior will promote these goals to achieve the goal.

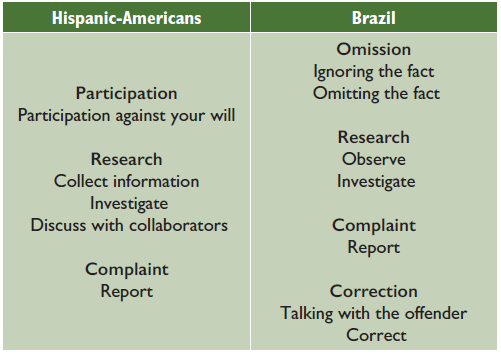

In order to identify the alternative options for a behavior, the interviewees were provoked to indicate the possible behaviors in view of the identification of a suspected financial illicit fact. Possible alternatives were classified in the variables of omission, participation, assessment, denunciation and correction.

All respondents indicated that in the event of identifying suspicious situations, they can ascertain the fact and report it. The complaint as manifested in the behavioral controls depends on a certain degree of reliability in the evidence, however this level of evidence is subjective and may vary according to the individual (table 10).

Prior to a report, until an enough level of security is reached, individuals may choose to ascertain this fact by collecting information, including talking to employees, to reach a sufficient level of security to affect the report. Brazilian interviewees expressed the possibility of talking to the offender to correct the problem, or alternatively omitting to know the suspected fact of illegality. In the Hispanic-American environment, the possibility of participation was reported through coercion by the offender to the whistleblowers.

E15: “Investigation of the situation before formally reporting it”.

E32: “Identification of the people involved and finding as much evidence as possible about the financial offense, in order to provide those responsible with conclusive information”.

The reporting of illegal or suspicious facts is the main mechanism for identifying financial crimes in the world and especially in Latin America, 43 to 55 percent (ACFE, 2020), and therefore criminal financial investigation strategies are more effective when they affect the whistleblower. The whistleblower or potential whistleblower are not always subject to legal action, sometimes they are not even known, and that is why it is very important to take actions that affect the object of people’s beliefs.

In this scope, the research sought to contribute by clearly highlighting the beliefs of individuals, separated by regions, and thus the police, justice and public policies could seek to trigger such beliefs to obtain reports of known, or still unknown crimes. Following the theoretical support of the theory of planned behavior and the theory of reasoned goal pursuit, we collect, analyze and present these beliefs.

The attitude beliefs of individuals demonstrate the social concern of employees that through reporting it is possible to protect the company, with the prevention of losses and the work environment, but also utilitarian consequences, such as self-protection, potential benefits, and reaffirmation of personal values. These beliefs are inherent to individuals and subject to positive reinforcement to induce new whistleblowers, however, it is possible to achieve greater effectiveness by curbing the beliefs that hinder the complaint indicated as the personal risks of whistleblowers, such as physical, financial and moral in the work environment.

Subjective beliefs depend on actual aspects of the individual, yet they can be very useful for investigators in the process of sensitizing witnesses to obtain conclusive statements. Recognizing the existence of stakeholders interested in ethical behavior is important for the cognitive process of complainants. Perceived beliefs about controls are primarily useful for anticipating and preventing fraud. In addition to reducing the volume of financial losses, this anticipation can facilitate the production of evidence for criminal investigations and accusations.

Conclusions

The survey identified behavioral beliefs for reporting financial crime suspects by Iberoamerican individuals. They were approached according to attitude beliefs, normative beliefs and control beliefs, segmented paired between Hispanic-American and Brazilian respondents.

The results of the research analysis allow the application of the concepts for the academic researchers, professional anti-fraud and judicial investigations. The practical applications are indirect, but the evidence allows managers and researchers to adapt their work practices and strategies. The beliefs of the revealed Latin American individuals are used in the process of constructing the judgment of the whistleblower’s intention, in which the individual considers several factors (Chiu, 2002; Zhang et al., 2009).

Knowledge about these factors contributes so that many criminal demands can be resolved and arbitrated between the parties, before reaching the court actors, which hinders their effectiveness. We believe that, based on different approaches to the subject, public policy makers, instructors of police courses on financial crimes and also on white-collar crimes, will be able to consider these factors in the training of their agents.

For managers, including internal auditing, compliance and controllership, it is relevant to know the beliefs of individuals in order to outline the most appropriate whistleblower channels, define compliance processes that contemplate the expectations of employees, in addition to establishing the controls and mechanisms that encourage whistleblower practices (Ciasullo et al., 2017; Kanojia et al., 2020; Said et al., 2017). In the criminal investigation process, the research findings contribute by presenting subsidies for investigators in the conduct of witnesses and potential whistleblowers (Alexander, 2004; Teichmann, 2018; Yakubu & Dikwa, 2020). Knowledge of the individual’s beliefs reveals valued incentives and can assist in the negotiation of complaints and collaboration agreements in the countries where they are allowed (Aubert, 2007; Teichmann, 2018; Teichmann & Falker, 2020; Yeoh, 2014).

In the judicial sphere, knowledge of the beliefs of individuals can make denunciations and investigations of financial or organizational crimes more effective. By activating the object of the individual’s beliefs, it is possible to influence a behavior, optimizing resources and efforts, in addition to helping to prevent the occurrence of fraud, which would result in a greater focus for justice and the police to invest in investigations of other crimes. Analyzing these contributions through the lens of the “theory of reasoned goal pursuit” becomes even more important, because depending on the alternative goals chosen by the witness, behavioral beliefs can moderate the possibility of denunciation or become innocuous. Still, for police officers and investigators these contributions serve as cognitive tools that allow extracting more effective testimonies.

The results are also useful for academics and researchers, to compare with intercultural results of the influences and perceptions about ethical behaviors in whistleblowers (Owusu et al., 2020; Park et al., 2008). In addition, it will allow the construction of a research instrument under the behavioral lenses adjusted to the Latin American context for whistleblower behavior (Ajzen & Kruglanski, 2019).

The results evidenced show similarities between the groups and with other global regions, however some evidence stands out in the different regions, influencing the whistleblower culture and the effectiveness of facing financial crimes. Hispanic-American respondents indicated elements of the most recurrent financial offenses for various characteristics of various types, including accounting fraud, extortion and arms trafficking. The potential recipients of the complaints were assigned to work teams, internal sectors of the company and external entities, however the Brazilian interviewees pointed out possibilities to police and justice agencies.

The beliefs of the individuals’ attitude had benefits indicated by the respondents as protection of the company, prevention of losses, benefit of the organizational environment, self-protection, and reaffirmation of personal values; however, Hispanic-American respondents included the possibility of potential benefits for the whistleblower himself, such as credibility, reputation, tranquility, promotion and recognition. When reporting the disadvantages of a complaint, Brazilian respondents distinguished themselves by pointing out moral risks of being pointed out by labels of traitors from colleagues.

The analysis of referents related to the subjective norm that could approve the individual’s behavior of making a complaint, in a relatively similar way in the work teams, internal control sectors, the organization’s management and external entities of the company. When listing the referents who may disapprove of a complaint, the respondents themselves and the work teams were indicated, however Hispanic-American respondents indicated differently people with emotional and friendship, and with the unions.

The control beliefs revealed by the interviewees showed similar variables in the two regions. Regarding the necessary conditions, the Hispanic Americans emphasize the need for mechanisms that clearly show the signs of irregularities and the demand to train for greater effectiveness of complaints. Regarding the unfavorable elements, these same interviewees highlighted the lenient organizational culture as a factor that limits the occurrence of complaints, in addition to their own involvement and management in the illicit.

Results show that it is possible to contribute to the literature by pointing out in detail characteristics that to a greater or lesser degree positively and negatively influence the reporting interest in the Ibero-American environment. These same evidences can be as implications for local managers to improve their reporting channels and thus make them more effective, resulting in benefits for the company and society.

The research presents as a limitation the approach of the internal factors of the application of criminal justice or its previous restrictions in the administrative scope, mainly related to the perceptions about financial frauds and the several related criminal typologies. Furthermore, because it is an analysis of beliefs internal to the organization designated in the variables of the theory of planned behavior and the reasoned goal pursuit, which limits the inclusion of factors external to the possible identification of fraud. Another important limitation stems from the grouping of Hispanic-American countries into a single subset, given the diversity of local cultures, which needs to be considered for future studies.

These limitations indicate the possibility of research gaps that need to be explored for greater effectiveness of criminal justice. Among these opportunities, the inclusion of variables external to the organization and the criminal investigation process is suggested, such as local culture, the perception of enforcement level, among others. The offender’s profile is another possibility to increase the research, as the abilities and organizational position of the criminal actors can affect the intention and probability of denouncing an eventual illicit act. Finally, it is worth pointing out as a possibility of deepening the research of local beliefs in different Hispanic-American countries, since each local reality imposes specific social characteristics, such as the justice system and legislation, which can influence the individual’s beliefs.