English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

PermalinkIntroduction

At international level, standards have been established to ensure the safe trade. One of these models for the standardization of secure logistics processes is BASC (Business Anti Smugling Coalition,), in this sense it is important to be able to analyze how this process of standardization contributes to improving internal operations, and the efficiency of this type of organizations that have taken these good standardized practices.

Which is why, in this research the answers to the following questions will be given:

What type of items and variables should be used to calculate the efficiency of Cali- Colombia firms that have assumed the BASC model?, what is the level of efficiency that the companies purpose of this study have reached?, can be established some sort of positive causation between the companies that were certified in BASC and the improvement of their level of efficiency?, what are the projections required to make inefficient companies reach their optimal efficiency?

Initially in this research, the concepts associated with the DEA Basic Model (Model CCR - O) and the evaluation of the efficiency of logistics processes through the Data Envelopment Analysis (DEA) are showed. For this study, the companies certified in BASC that submitted their financial statements in the Superintendency of Corporations of Colombia in 2014 were taken.

Then the variables and items used in this study are presented; subsequently the correlation of variables of inputs and outputs required for the calculation of the efficiency is analyzed. After this, it is presented the results of the financial efficiency analysis of the BASC certified companies in the city of Cali - Colombia with the efficiency scores calculated by the CCR - O model; subsequently, the efficient firms that can act as peer evaluators for the inefficient firms and the required projection for the output variable to achieve efficiency are determined.

1. Literature review

1.1. Growth of the economy

The current growth of the economy, the opening of markets and the trend of the same level, make a series of challenges for organizations which demands a greater effort to remain productive and thus achieve greater competitiveness in the market.

In the logic of the growth of the companies, these need efforts to increase their market share, financial efforts in human resources and efforts in fixed assets that may affect the level of efficiency of the companies and assist with compliance of organizational objectives. In this regard, it is necessary an effort not alien to the growth of the company, which from a broad point of view should cover the efforts mentioned above and in this way improve the logistics processes. Free trade treaties create a series of challenges in which in addition to the improvement of quality and price, the quality of the acquisition processes from the raw materials up to the delivery of the products and/or services must be improved.

As previously mentioned, it is necessary the implementation of a management system to ensure the safety of the processes that integrate the supply chain; and for this reason standards for secure commerce are implemented, as it is the BASC certification (Business Anti Smugling Coalition), which seeks answers to the issue of control management and safety of the trade. According to, processes in the international trade require formality and timely responsiveness, guarantees on the transactions and assurance of the supply chain, which is precisely achieved with the BASC certification.

1.2. DEA CCR - O

For the measurement of how effective the BASC model is, in this research work is defined a structure of input and output variables, with which it was measured the efficiency of the DEA CCR-OR model in this group of companies that assumed that standard in the city of Cali - Colombia.

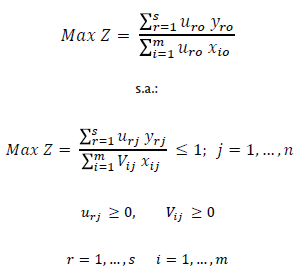

The data envelopment analysis (DEA) is a tool that allows the measurement of efficiency in the public or private organizations through a linear programming model. Charper, Cooper and Rhodes originally proposed this tool of analysis of efficiency in 1978. It is important to note that this tool proposes models for the evaluation of efficiency, one model oriented to entries (CCR - I) and another aimed at the outputs (CCR - O), the latter one seeks to maximize the outputs from the resources available. Maximize the efficiency seeks a fractional programming solution which has multiple solutions, in this sense, it is necessary the implementation of a linear programming model, and this is achieved by leaving the numerator constant (assuming a value of 1) and maximizing the numerator; this is called CCR oriented to the outputs or commonly called CCR - O.

1.3. DEA Basic Model (Model CCR - O)

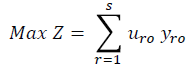

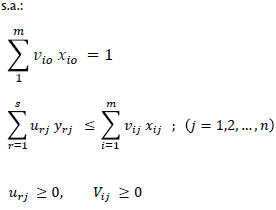

This model is expressed mathematically as it follows, if Yo = (ylo, y2o, y3o.....yso) and Xo = (xlo, x2o, x3..... xmo), represent the inputs and the outputs of the DMUo respectively, the measure of efficiency of the unit being evaluated can be obtained with the optimal solution of the following model:

Being u ro y v ro the group of DMU more favorable, the previous model can be converted to:

Where n is the number of DMU, m is the number of input variables and s is the number of output variables.

1.4. Evaluation of the efficiency of logistics processes using Data Envelopment Analysis (DEA, CCR - O)

The DEA tool is one of the most used in the evaluation of performance of public and private organizations (Nijkamp, Suzuki 2009). Within the logistics processes, its use is necessary to assess the efficiency, productivity, and observe the units that can be improved as a measure of competitiveness. The use of the technique has many applications within the logistics processes, for example, evaluation of the efficiency with a focus on the suppliers (Azadeh, Alem 2010; Çelebi, Bayraktar 2008; Farzipoor Saen 2009; Jong Joo, Min 2006; Kontis, Vrysagotis 2011; Min, Joo 2009; Mohammady Garfamy 2006; Narasimhan, Talluri, Mendez [no date]) in the evaluation of manufacturing (Shorouyehzad, Lotfi, Aryanezhad, Dabestani 2011), in the evaluation of reverse logistics (Haas, Murphy, Lancioni 2003; Tonanont, Yimsiri, KJ Rogers PhD 2009; Tonanont, Yimsiri, Jitpitaklert, Rogers 2008).

The data envelopment analysis (DEA) is a parametric tool that allows the evaluation of efficiency; it is important to note that the Data Envelopment Analysis looks for the obtaining of an efficient frontier, which is estimated by maximizing the outputs with a certain level of income; and the estimate of the inefficiency, which depends on the orientation and is calculated in the same way as the efficient frontier (Morollón, Morán, Cuervo 2005)

2. Methodology

For this study of efficiency, 42 companies certified in BASC Cali-Colombia were taken into account, and the information associated with the financial items, collected in the Superintendency of corporations of Colombia in 2014. Table 1 shows the companies that were considered for this investigation. For which there was special care in the choice of the input and output variables. It was worked with an approach to outputs, and the performance of these was analyzed.

Table 1 Magnitude of the variables of input and output of the certified companies in BASC Cali for research

| Social Reason | (I) Subtotal Inventories | (I) Total Current Assets | (I) Properties Plant And Equipment | (I) Suppliers | Operating Revenues (Annex 1) |

|---|---|---|---|---|---|

| Comestibles Aldor S.A. | 15735248 | 59829143 | 41939120 | 11850003 | 144126848 |

| Ocupar Temporales S.A . | 0 | 7747440 | 1430622 | 0 | 82560111 |

| Coral Visión Ltda Sociedad de Intermediación Aduanera | 0 | 2044341 | 1318353 | 0 | 3051359 |

| Sociedad de Intermediación Aduanera S.A. | 150 | 2647620 | 34254 | 48741 | 1718922 |

| Adhesivos Internacionales S.A.S. | 3134704 | 8894265 | 679159 | 930013 | 11729859 |

| Agraf Industrial S.A. | 1176103 | 5434996 | 4131348 | 1604733 | 18923849 |

| Acción del Cauca S.A. | 0 | 1922135 | 11894 | 10353 | 8837435 |

| Globalog S. A . | 5957 | 6744931 | 351766 | 291832 | 14738411 |

| Cristar S.A.S. | 20157597 | 55367914 | 22124669 | 9538784 | 137649408 |

| Grupo Empresarial Apparel Solutions Ltda. | 0 | 841464 | 47914 | 218862 | 9272880 |

| Colombina del Cauca S.A. | 15652690 | 19606379 | 73092614 | 30438228 | 201035291 |

| Compañía Internacional de Alimentos S A.S. | 6795480 | 15557945 | 27273920 | 21994199 | 85027721 |

| Genfar S.A. | 35784211 | 126132875 | 19352200 | 24934928 | 218536987 |

| Centro de Mecanizados del Cauca S.A. | 16513209 | 20657011 | 9616235 | 4573507 | 24479846 |

| El Dorado Air Cargo S. A. S. | 0 | 2137374 | 63328 | 215611 | 1196616 |

| Bridgestone Firestone Colombiana S.A.S. | 15463446 | 68971111 | 298494 | 13683810 | 111008747 |

| Ups Scs Colombia Ltda. | 0 | 12705721 | 835319 | 7639635 | 64009165 |

| Carvajal S.A. | 20932689 | 261383285 | 40006818 | 18435183 | 96679792 |

| Laboratorios Baxter S.A. | 47606227 | 377710341 | 96518604 | 65142887 | 547374636 |

| Cartón de Colombia S.A. | 88488051 | 324882231 | 207791189 | 76291274 | 744890873 |

| Colgate Palmolive Compañía | 74137276 | 262135200 | 129876446 | 66562102 | 297597049 |

| Cadbury Adams Colombia S.A. | 26474647 | 136894534 | 64762107 | 45548440 | 299497308 |

| Transportes Centro Valle Ltda. | 266065 | 4118866 | 3652921 | 449430 | 13272315 |

| Transportes Rodríguez - Gonzalo | 0 | 3093086 | 438191 | 0 | 4207245 |

| Industrias del Maiz S.A. Corn Products Andina | 60751990 | 181578693 | 131520887 | 69345592 | 514873966 |

| Eternit Pacífico S.A. | 6655875 | 31276766 | 8663135 | 4476552 | 55991207 |

| Colombina S.A. | 85070792 | 223013032 | 188298976 | 100756237 | 680199335 |

| Laboratorios Recamier Ltda. | 14381724 | 63178247 | 8634996 | 14151229 | 93873979 |

| Plásticos Especiales S.A. | 23827540 | 52920803 | 24940992 | 12017258 | 83682925 |

| Industria de Aluminio India Ltda. | 2194308 | 7181389 | 7314909 | 548434 | 11764797 |

| Acción S.A. | 0 | 50983172 | 5059449 | 577489 | 353981531 |

| Agecolda S. A. | 0 | 261005 | 1571691 | 38199 | 696598 |

| Empresa Andina de Herramientas S. A. S. | 5180509 | 19147114 | 3160241 | 3006869 | 37666715 |

| Protécnica Ingeniería S.A. | 5859945 | 16632620 | 5131548 | 5062520 | 28577498 |

| Productos Yupi Limitada | 6423558 | 36847430 | 3890446 | 12893016 | 149427490 |

| Vallecilla B Vallecilla M & Cia S.C.A. Carval de Colombia | 17675742 | 57182386 | 19310832 | 12631017 | 77840169 |

| Carvajal Internacional S. A. | 0 | 355560627 | 0 | 104 | 95392210 |

| Ingenio del Cauca S. A. | 31065259 | 174262708 | 293212697 | 23972807 | 615026427 |

| Ingenio Providencia S.A. | 19918212 | 70094014 | 261713216 | 20442431 | 454716865 |

| Harinera del Valle S.A. | 50603928 | 314483704 | 57155350 | 14750735 | 361445218 |

| Ingenio Pichichi S.A. | 12031159 | 46547728 | 51224738 | 16507605 | 182952698 |

| Riopaila Industrial S.A. | 47706264 | 244755640 | 226582396 | 41303315 | 676090232 |

Source: The autors.

2.1. Variables considered in the study

Below, the variables considered in the study and their description are shown, this was established by the Superintendency of corporations.

2.1.1. Input Variables

Subtotal of inventories: The inventory is associated with the goods and other objects belonging to a natural person, a community.

Total Current assets: current assets are considered cash and all those other accounts which is expected to be converted, in turn, in cash, or that have been consumed during the normal cycle of operations.

Property, plant and equipment: The property, plant and equipment are tangible assets owned by a company for its use in the production or supply of goods and services, productive purposes, administrative or for leasing to third parties and are expected to be used for more than one economic period.

Suppliers: a supplier can be a person or a company that provides stock to other companies, which will be transformed to later sell or directly purchased for sale.

2.1.2. Output Variables

Operating Income: Are all the income assets or reduction of liabilities in the studied period, which is manifested in the increase of the capital, other than to the contributions of the partners.

For the calculation and analysis of the results the software DEA Solver PRO was used, with which in an specific framework the input and output variables, previously established for each company or DMU, were analyzed, with that it was able to calcute the efficiencies for the population under study. Table 1 shows the values (magnitude) of the input and output variables for each of the companies considered in the study.

3. Results

3.1. Implementation of DEA to BASC certified companies in Cali

The results of this research article make reference to: 1) the efficiency scores of the certified companies with BASC in the city of Cali, 2) the study of the correlation between the variables in the rese arch, 3) the classification of the different organizations by types of efficiency, 4) as well as to the projection of improvement of the output, i.e. operating revenues, with the aim of improving the relationship of input/output with the purpose of making an inefficient firm, efficient. To finally analyze the relationship between the organizational efficiency of the sector and the standardization with the standard for secure commerce BASC in the city of Cali.

Initially the correlation between the variables of the study is presented, used to analyze the technical or administrative efficiency. As seen in Table 2. The data shows a high positive correlation between the input and output variables, allowing to analyze the causality between the items.

Table 2 Correlation between the variables

| Social Reason | (I) Subtotal Inventories | (I) Total Current Assets | (I) Properties Plant And Equipment | (I) Suppliers | Operating Revenues (Annex 1) |

|---|---|---|---|---|---|

| Subtotal Inventories | 1 | ||||

| Total Current Assets | 0,75 | 1 | |||

| Properties Plant And Equipment | 0,70 | 0,55 | 1 | ||

| Suppliers | 0,92 | 0,67 | 0,68 | 1 | |

| Operating Revenues | 0,83 | 0,71 | 0,88 | 0,82 | 1 |

Source: The autors.

It can be seen that there is a high correlation of SUBTOTAL OF INVENTORY with suppliers (0.92), with OPERATING REVENUES (0.83); PROPERTY PLANT AND EQUIPMENT with OPERATING REVENUES (0.88) and SUPPLIERS with OPERATING REVENUES (0.82), on the other hand, the input variable with less correlation with output variables is PROPERTY PLANT AND EQUIPMENT. What evidence the relevance and correspondence between the selected variables.

It is important to emphasize that there is a high correlation between the internal variables of the organizations with the generation of operational income. This is consistent with the fact that the processes of standardization BASC, have as intentionality, the generation of efficiency and operational effectiveness, which requires a series of domestic conditions and availability of current assets, property plant and equipment; and resources available for the improvement of the logistical processes of organizations where it's deployed.

After evaluating the efficiency of the 42 companies certified with BASC in Cali, the CCR-O efficiency scores for each organization were obtained, as shown in Table 3. It is important to remember that a DMU is efficient if the score of efficiency is equal to 1 and has no gaps (the clearance in all the variables is equal to 0), in this case of study all the DMU's whose score of efficiency is one (1) did not show gaps in its variables, therefore to determine if a company is efficient, it is enough to observe that the efficiency score is equal to one (1). It was found that 5 of 42 companies are efficient, this leads to see that 11% of the total number of companies assessed are efficient.

Table 3 Efficiency scores CCR - O model

| No. | DMU | Score | 1/Score | No. | DMU | Score | 1/Score |

|---|---|---|---|---|---|---|---|

| 1 | Comestibles Aldor S.A. | 0,22 | 4,53 | 22 | Cadbury Adams Colombia S.A. | 0,20 | 5,04 |

| 2 | Ocupar Temporales S.A. | 1 | 1 | 23 | Transportes Centro Valle Ltda. | 0,30 | 3,35 |

| 3 | Coral Vision Ltda. Sociedad de Intermediación Aduanera | 0,14 | 7,13 | 24 | Transportes Rodríguez - Gonzalo | 0,17 | 6,06 |

| 4 | Sociedad de Intermediación Aduanera S.A. | 0,12 | 7,8 | 25 | Industrias del Maíz S.A. Corn Products Andina | 0,26 | 3,89 |

| 5 | Adhesivos Internacionales S.A.S. | 0,14 | 6,7 | 26 | Eternit Pacífico S.A. | 0,16 | 6,06 |

| 6 | Agraf Industrial S.A. | 0,31 | 3,16 | 27 | Colombina S.A. | 0,29 | 3,49 |

| 7 | Acción del Cauca S.A. | 1 | 1 | 28 | Laboratorios Recamier Ltda. | 0,14 | 7,38 |

| 8 | Globalog S. A. | 0,31 | 3,14 | 29 | Plásticos Especiales S.A. | 0,14 | 6,94 |

| 9 | Cristar S.A.S. | 0,22 | 4,38 | 30 | Industria de Aluminio India Ltda. | 0,15 | 6,57 |

| 10 | Grupo Empresarial Apparel Solutions Ltda. | 1 | 1 | 31 | Acción S.A. | 1 | 1 |

| 11 | Colombiana del Cauca S.A. | 0,93 | 1,07 | 32 | Agecolda S. A. | 0,25 | 4,07 |

| 12 | Compañía Internacional de Alimentos S. A.S. | 0,49 | 2,02 | 33 | Empresa Andina de Herramientas S. A. S | 0,18 | 5,53 |

| 13 | Genfar S.A. | 0,15 | 6,31 | 34 | Protécnica Ingeniería S.A. | 0,16 | 6,41 |

| 14 | Centro de Mecanizados del Cauca S.A. | 0,1 | 9,25 | 35 | Productos Yupi Limitada | 0,37 | 2,72 |

| 15 | El Dorado Air Cargo S. A. S. | 0,07 | 12,78 | 36 | Vallecilla B Vallecilla M & Cía. S.C.A. Carval De Colombia | 0,12 | 8,06 |

| 16 | Bridgestone Firestone Colombiana S.A.S. | 0,48 | 2,05 | 37 | Carvajal Internacional S. A. | 1 | 1 |

| 17 | Ups Scs Colombia Ltda. | 0,49 | 2,02 | 38 | Ingenio del Cauca S A | 0,33 | 3,02 |

| 18 | Carvajal S.A. | 3,00E-02 | 29,08 | 39 | Ingenio Providencia S.A. | 0,59 | 1,70 |

| 19 | Laboratorios Baxter S.A. | 0,13 | 7,52 | 40 | Harinera del Valle S.A. | 0,11 | 9,33 |

| 20 | Cartón de Colombia S.A. | 0,21 | 4,65 | 41 | Ingenio Pichichi S.A. | 0,36 | 2,80 |

| 21 | Colgate Palmolive Compañía | 0,1 | 9,70 | 42 | Riopaila Industrial S.A. | 0,26 | 3,86 |

Source: The autors.

To the results of efficiency of the model used there was a classification in efficient enterprises (efficiency = 1 and zero slack), companies with high efficiency (1 > efficiency =0.80), companies with average efficiency (0.80 > efficiency =0.70) and companies with low efficiency (efficiency <0.70).

According to this classification Table 4 was built.

For each inefficient Company, DEA suggests the combination of inputs and outputs that are necessary to achieve efficiency (projections of the inefficient DMU on the efficient frontier), in the case of the output variables, for an efficient DMU, the magnitude of these should improve (increase). The magnitude of the increase in the magnitude of each output variable for each company is presented in Table 5.

Table 5 Necessary increase in the magnitude of the output variables to achieve the efficiency

| No. | DMU | Score | Increase In Operating Revenues |

|---|---|---|---|

| 1 | Comestibles Aldor S.A. | 0,22 | 654126542 |

| 3 | Coral Visión Ltda. Sociedad de Intermediación Aduanera | 0,14 | 21785393 |

| 4 | Sociedad de Intermediación Aduanera S.A. | 0,13 | 13421919 |

| 5 | Adhesivos Internacionales S.A.S. | 0,15 | 78603562 |

| 6 | Agraf Industrial S.A. | 0,32 | 59893312 |

| 8 | Globalog S.A. | 0,32 | 46393477 |

| 9 | Cristar S.A.S. | 0,23 | 603355680 |

| 11 | Colombina del Cauca S.A. | 0,93 | 216061055 |

| 12 | Compañía Internacional de Alimentos S.A.S. | 0,50 | 171447569 |

| 13 | Genfar S.A. | 0,16 | 1378975007 |

| 14 | Centro de Mecanizados del Cauca S.A. | 0,11 | 226521870 |

| 15 | El Dorado Air Cargo S. A. S. | 0,08 | 15298622 |

| 16 | Bridgestone Firestone Colombiana S.A.S. | 0,49 | 227348114 |

| 17 | Ups Scs Colombia Ltda. | 0,50 | 129225103 |

| 18 | Carvajal S.A. | 0,03 | 2811178790 |

| 19 | Laboratorios Baxter S.A. | 0,13 | 4116087338 |

| 20 | Cartón de Colombia S.A. | 0,22 | 3462087225 |

| 21 | Colgate Palmolive Compañía | 0,10 | 2886451510 |

| 22 | Cadbury Adams Colombia S.A. | 0,20 | 1508569097 |

| 23 | Transportes Centro Valle Ltda. | 0,30 | 44520541 |

| 24 | Transportes Rodríguez - Gonzalo | 0,17 | 25481239 |

| 25 | Industrias del Maíz S.A. Corn Products Andina | 0,26 | 2000985700 |

| 26 | Eternit Pacífico S.A. | 0,16 | 339555124 |

| 27 | Colombina S.A. | 0,29 | 2376524462 |

| 28 | Laboratorios Recamier Ltda. | 0,14 | 693032147 |

| 29 | Plásticos Especiales S.A. | 0,14 | 580741997 |

| 30 | Industria de Aluminio India Ltda. | 0,15 | 77294489 |

| 32 | Agecolda S.A. | 0,25 | 2834769 |

| 33 | Empresa Andina de Herramientas S.A.S | 0,18 | 208242285 |

| 34 | Protécnica Ingeniería S.A. | 0,16 | 183290419 |

| 35 | Productos Yupi Limitada | 0,37 | 406056345 |

| 36 | Vallecilla B Vallecilla M & Cia S.C.A. Carval De Colombia | 0,12 | 627013051 |

| 38 | Ingenio del Cauca S. A . | 0,33 | 1857019676 |

| 39 | Ingenio Providencia S.A. | 0,59 | 772431596 |

| 40 | Harinera del Valle S.A. | 0,11 | 3371890866 |

| 41 | Ingenio Pichichi S.A. | 0,36 | 512953015 |

| 42 | Riopaila Industrial S.A. | 0,26 | 2608223207 |

Source: The autors.

It was considered only the outputs variables taking into account that the CCR - O model was used, and this model determines which outputs would be the ideal to optimize the efficiency of the DMU.

The company Grupo Empresarial Apparel Solutions LTDA. was used 30 times as a reference parameter for assessing other organizations. Followed by the companies Ocupar Temporales S.A. with 26, Acción del Cauca S.A. with 6, Carvajal Internacional S.A. with 2 and Acción S. A. with 1 organization as pair evaluators, for other companies under research.

4. Conclusion

In this research work, the efficiency of the certified companies with BASC in Cali, Colombia were assessed. For this it was discussed how efficient organizations are when it is considered as entries the total inventory, current assets, property plant and equipment and the resources of suppliers and how this is reflected in the operating revenues of the organizations under study The foregoing, using the model that assumes constant returns to scale (CRS) with a focus on outputs (CCR - O), proving efficient 5 of the 42 companies surveyed in the study.

It was able to analyze that in spite of the fact that there is a group of companies that presented an optimal efficiency, there is also a group of inefficient companies that require improving its internal processes in order to be able increase its operating revenues. The following values are the projections generated by the model of DEA CCR-O used to achieve the efficiency of the inefficient organizations: Comestibles Aldor S.A. (654.126.541), Coral Visión Ltda. Sociedad de Intermediación Aduanera (21.785.393), Sociedad de Intermediación Aduanera S.A. (13.421.918), Adhesivos Internacionales S.A.S. (78.603.561), Agraf Industrial S.A. (59.893.311), Globalog S.A. (46.393.476), Cristar S.A.S. (603.355.679), Compañia Internacional de Alimentos SAS. (171.447.568), Genfar S.A. (138.975.006), Centro de Mecanizados del Cauca S.A. (226.521.869), El Dorado Air Cargo S.A.S. (15.298.622), Bridgestone Firestone Colombiana S.A.S. (227.348.113), Ups Scs Colombia Ltda. (129.225.103), Carvajal S.A. (2.811.178.790), Laboratorios Baxter S.A. (4.116.087.337), Cartón de Colombia S.A. (3.462.087.225), Colgate Palmolive Compañía (2.886.451.510), Cadbury Adams Colombia S.A. (I.508.569.096), Transportes Centro Valle Ltda (44.520.540), Transportes Rodríguez - Gonzalo (25.481.238), Industrias del Maíz S.A. Corn Products Andina (2.000.985.699), Eternit Pacifico S.A. (339.555.124), Colombina S.A. (2.376.524.461), Laboratorios Recamier Ltda. (693.032.147), Plásticos. Especiales S.A. (580.741.996), Industria de Aluminio India Ltda. (77.294.488), Agecolda S.A. (2.834.768), Empresa Andina de Herramientas S.A.S. (208.242.285), Protécnica Ingeniería S.A. (183.290.419), Productos Yupi Limitada (406.056.345), Vallecilla B Vallecilla M & Cia S.C.A. Carval De Colombia (627.0I3.050), Ingenio del Cauca S.A. (1.857.0I9.675), Ingenio Providencia S.A. (772.431.596), Harinera del Valle S.A. (3.371.890.866), Ingenio Pichichí S.A. (512.953.015), Riopaila Industrial S.A. (2.608.223.207). From the research work carried out it can also be concluded that the average of the BASC certified organizations in Cali - Colombia was 33.95 %. From the 42 companies under investigation only five presented an optimal efficiency. It can be inferred that in spite of the fact that some companies certified in BASC of the city of Cali presented a financial efficiency of 1, it is not significant for the whole sector. Also, with the input and output variables analyzed through the DEA model, it can be concluded that the BASC certification does not generate a causality for the improvement of the efficiency for companies subject to this research by the foregoing there is an invitation to the researchers to continue analyzing the efficiency of the BASC certified companies, selecting and evaluating other variables of input and output that can be used to analyze the correlation and causality of the standardization processes used with the operational and financial efficiency, in order to facilitate the decision making process to achieve productivity and competitiveness of the organizations of the sector that implement this type of international standards.