Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Citado por Google

Citado por Google  Similares em

SciELO

Similares em

SciELO  Similares em Google

Similares em Google

Permalink

PermalinkI. Introduction

The sunk-cost fallacy (SCF) refers to a greater tendency to continue an endeavor once an investment in time, effort, or money has been made (Arkes & Blumer, 1985). Doing so is considered an error because a rational decision maker should only consider current marginal costs and benefits and should neglect sunk cost because it is irretrievable no matter which option is chosen (Navarro & Fantino, 2005; R. Thaler, 1980). This phenomenon can occur in humans and nonhuman animals (Sweis et al., 2018).

The likelihood that an individual will commit the SCF increases with the size of the initial investment (Garland & Newport, 1991). The researchers offered participants four scenarios: two specific to business dealing and the other two about personal purchases. The scenarios included high and low initial investments expressed as fixed sums or as high and low percentages of a total budget. The likelihood of continued investment was more influenced by the relative value than the absolute value. For example, participants were more likely to remain committed to remodeling a home office if 85% of the budget had already been used as opposed to the corresponding sum of $7.800.

Sunk costs have traditionally been categorized as investments of time, money, or effort (Arkes & Blumer, 1985). The most commonly studied investment is money. For example, an individual is more likely to wear an unattractive piece of clothing if it was expensive (Zeng, Zhang, Chen, Yu, & Gong, 2013). People are more likely to sit through a boring movie if the ticket price was at a premium (Arkes & Blumer, 1985; Strough, Mehta, McFall, & Schuller, 2008). In early studies by Staw and colleagues (Staw, 1976; Staw & Fox, 1977; Staw & Ross, 1978), participants were asked whether they would invest further in an initial investment they had already made. The researchers found that if the initial investment had turned out to be unprofitable, participants invested more additional funding than if it had been profitable. When investments of time were used, mixed results were reported. In one study, the researchers found similar likelihoods of further investment following an initial investment, regardless of whether they were of time or money (Strough et al., 2008). However, Klaczynski and Cottrell (2004) combined initial investments of time and effort and found that their participants performed similarly to when the investments were monetary. Soman (2001) compared money and time and found that participants produced the SCF less often when the investments were of time than when they were of money. The author attributed the difference to the greater difficulty of keeping a mental account of time expenditures. When Soman experimentally manipulated mental accounting by informing participants of the monetary value of time, the difference decreased.

Investments of effort have been studied least according to the published literature on the SCF. Navarro (2008) investigated conditions in which there was no investment of effort, low-effort investment, and high-effort investment but found no differences in the outcomes.

To our knowledge, there has only been one published study in which the authors reported differences in the likelihood of the SCF when the category of investment type varied. Strough, Schlosnagle, Karns, Lemaster, and Pichayayothin (2014) provided participants with a common set of scenarios in which an initial investment had been made and asked them to indicate whether they would discontinue investing, invest once more, or invest to the end of the project. The initial investments varied in terms of amount and type. Examples of the investment types appear below with scenarios indicated in brackets:

Money. You are staying in a hotel room on vacation. [You paid $10.95 to see a movie on pay TV and start it soon after arriving in the room. / You arrive at the room, turn on the TV, and start watching a movie on a regular channel.] After 5 minutes, the movie seems pretty bad, and you grow bored. How much longer would you continue to watch the movie?

Time. You are staying in a hotel room on vacation. [You watch a movie for 1 hour. / You watch a movie for 5 minutes.] The movie seems pretty bad, and you grow bored. How much longer would you continue to watch the movie? (Strough et al., 2014)

For the money scenario, the SCF was defined as being more likely to continue watching the movie when one had paid extra for it. For the time scenario, it was defined as being more likely to continue watching the movie when one had already watched it for an hour. The authors found that the SCF occurred more frequently when time was the investment category (M = .90, SD = .58) than when it was money [(M = .75, SD = .47), F (1, 425) = 19.65, p < .01, η 2 = .04]. Because the authors were unsure whether participants had perceived the monetary investment in the scenarios as equivalent to the temporal investment, they conducted another study in which the specific amounts of money were replaced by general descriptors, such as “hardly any” or “a whole lot” (p. 93). They found no main effect of investment type. However, if they designated scenarios, such as that of the movies on TV in the hotel room as “nonsocial”, they reported that the SCF was more likely when money had been invested compared to time. For “social” scenarios, the SCF was more likely when time had been invested. The authors concluded that, contrary to Soman (2001) suggestion that people simply track money better than they track time, the difference may depend on context (social v. nonsocial, for example).

Many attempts have been made to explain the mechanisms behind the SCF with varying degrees of success (Vasconcelos, 2019). One possibility in the occurrence of the SCF as a function of investment type is that humans are more sensitive to losses than to gains, and monetary losses may more often be perceived as unrecoverable as opposed to losses of time or effort (Soman, 2004). Prospect theory (Kahneman & Tversky, 1979) was designed to account for why individuals are risk-seeking when confronting potential losses (an effect known as loss aversion) but are risk averse when confronting the prospect of potential gains. Given that sunk cost refers to loss, it may be related to loss aversion (Whyte, 1986). For Soman (2004),

Loss aversion implies that a given difference between two options will have greater impact if it is viewed (or, framed) as a difference between two disadvantages (relative to a reference point) than if it is viewed (or, framed) as a difference between two advantages. That is, advantages and disadvantages may not be mirror images. (p. 388)

In other words, when an initial investment is made and the returns are unknown or are negative, this outcome likely is perceived as a disadvantage, and an individual may attempt to escape from it by investing further, which is the SCF (Garland & Newport, 1991; Kahneman & Tversky, 1979; Soman, 2004).

Kahneman and Tversky (1979) defined loss aversion as the preference for uncertain losses over certain losses. For example, when people are given a choice between statistically equivalent outcomes-a 100% chance of receiving $900 or a 90% chance of receiving $1.000-they are more likely to choose the sure gain. However, the opposite is true for losses. When given a choice between a certain loss of $900 or a 90% chance of losing $1.000, people are more likely to choose the uncertain option. People become more risk-seeking when choices are between losses. It may be that individuals perceive sunk cost as an option between accepting a sure loss (scrapping a project already invested in) or continuing to invest in an uncertain loss. After all, if it is money, persisting may offer a chance for the initial investment to be recovered (Garland & Newport, 1991; Kahneman & Tversky, 1979; Soman, 2001). With investments of time or effort, there is no chance of recovery. Thus, if loss aversion is a factor in the SCF, initial investments in the form of money may be more likely to prompt further investments than if the initial investments were of time or effort.

We had two aims in the study we describe here. The first was to further investigate whether time, effort, and money affect the likelihood of the SCF differentially. H 1 : The likelihood of the SCF will be greatest when the initial-investment type is money compared to when it is expressed as time or effort. Our second aim was to investigate the level of loss aversion as a predictor of the likelihood of the SCF. H 2 : Loss-aversion scores will be a significant predictor of the SCF, with greater levels of loss aversion predicting a greater likelihood of the SCF.

2. Method

2.1. Participants

The participants were 168 undergraduate college students (mean age = 22.19, SD = 6.01, 52% male) at a large, private university in the western United States. Students were recruited through an online system (SONA), wherein they self-enrolled for access to a survey in order to receive an Amazon gift card. The sample size was determined by a fixed enrollment period (one week) and was not changed prior to the analysis of results.

2.2. Materials and Procedure

Each participant signed an informed-consent form before receiving further instructions as per the requirements of the Institutional Review Board at the university where we conducted the research. We asked the participants to complete a sunk-cost questionnaire and a loss-aversion task in counterbalanced order using a Web-based survey tool (QualtricsOR , Provo, UT).

2.3 The SCF Questionnaire

The questionnaire included ten sunk-cost scenarios in which five scenarios were modified from those previously used by Strough et al. (2014) and another five modified from Bornstein and Chapman’s 1995 study (see Appendix A). The scenarios were modified to present different levels of initial investment in the form of time, effort, or money expressed as percentages. Questions specific to each scenario were presented twice: the first time after a low-initial investment was made and the second time after a high-initial investment was made, as in Strough et al. (2014). Thus, there was a total of six questions per scenario. Similar to the study by Garland and Newport (1991), participants were randomly assigned to an initial-investment ratio of 1:2 (for example, 10% and 20%; N = 56), 1:3 (5% and 15%; N = 53), or 1:5 (8% and 40%; N = 59).

The total number of questions answered by each participant was 60 (see Table 1). Scores were calculated using the procedure described by Strough et al. (2014), wherein, if a participant indicated that he or she would spend a greater percentage of time, effort, or money in the high-investment scenario compared to the low-investment scenario, he or she received a score of 1 for the question, which indicated that the SCF had occurred. Otherwise, the score was zero. Scores were summed within each investment type and across all 30 pairs of low-and-high initial investments, with higher scores indicating the more frequent occurrence of the SCF. The highest possible score was 30.

Table 1 Number of questions in the SCF questionnaire for each type of investmen t

| Time | Effort | Money | |

| Low-initial investment | 10 | 10 | 10 |

| High-initial investment | 10 | 10 | 10 |

Note: Participants were randomly assigned to initial-investment ratios of 1:2, 1:3, or 1:5 and were expressed as percentages.

Participants were also asked to indicate their gender, age, and estimated ACT score as part of a larger dissertation project which will not be reported here.

2.4 Loss-Aversion Task-the Endowment Effect

Loss aversion was measured using an endowment-effect task similar to that used by Gächter, Johnson, and Herrmann (2007). It involved the difference between what participants were “willing to pay” (WTP) for a lamp that was pictured on the computer screen together with a hypothetical retail price of $29.99 and what they were “willing to accept” (WTA) to sell that object when it was in their possession (see Appendix B). Participants used an on-screen slider to indicate their preferred price across a range from $5 to $55. The difference between the WTA and WTP (WTA-WTP) became the measure of loss aversion, with higher scores indicating greater aversion.

3. Results

3.1 SCF Questionnaire

Each participant’s SCF score was calculated from the questionnaire results. The highest possible score was 10 for each investment type-time, effort, or money. Table 2 shows the mean score and standard deviation for each initial-investment ratio across initial-investment types. The mean total SCF score (across all investment types) for participants in the 1:2 condition was M = 7.21 (SD = 5.67), M = 9.77 (SD = 5.66) for those in the 1:3 condition, and M = 11.68 (SD = 7.31) for those in the 1:5 condition. The distribution of SCF scores for each investment type (effort, time, and money) was positively skewed, and the data were transformed using a squareroot transformation with 1.0 added to each score to assure that it was non-zero. The transformation did not change the direction or significance of the results. Analyses using the untransformed data are reported here.

Table 2 Mean SCF scores by initial-investment ratio and investment type. The mean and standard error of the mean for all ratios appear as Total.

| Effort | Time | Money | N | |

| M(SD) | M(SD) | M(SD) | ||

| Ratio 1:2 | 2.04(1.79) | 2.27(1.94) | 2.91(2.57) | 56 |

| Ratio 1:3 | 2.55(1.94) | 3.04(1.96) | 4.19(2.59) | 53 |

| Ratio 1:5 | 3.14(2.49) | 3.49(2.49) | 5.05(2.86) | 59 |

| Total | 2.58(2.14) | 2.94(2.20) | 4.07(2.81) | 168 |

Note: The maximum SCF score for each cell was 10.

3.2 Loss-Aversion Task

Participants’ mean WTP score was M = $17.82, SD = 8.71. The mean WTA was M = $21.51, SD = 7.79. Loss-aversion scores were calculated by subtracting a participant’s WTP from the WTA. Results ranged from -$15.68 to $40.18, M = 3.69, SD = 9.28, where higher scores indicated greater loss aversion.

3.3 Hypothesis Analysis

To test the hypotheses, a 3x 3 (initial-investment type by initial-investment ratio) mixed-design ANCOVA was used with loss aversion as a covariate (see Table 3).

Table 3 ANCOVA results, including the within-subject variable of initial-investment type and the betweensubject variables of initial-investment ratio and los s

| Within-Subject Variable | df | F | n2p | p |

| Initial-investment Type | 1.58 | 60.40 | 269 | <.001 |

| Investment-type * Ratio | 3.17 | 3.33 | .039 | .018 |

| Error | 259.61 | |||

| Between-Subject Variables | df | F | n2p | p |

| Initial-investment Ratio | 2 | 7.93 | .088 | .001 |

| Loss Aversion | 1 | 4.13 | .025 | .044 |

| Error | 164 |

Note: The maximum SCF score for each cell was 10.

Mauchly’s Test of Sphericity was violated, χ 2(2) = 49.84, p < .001 (Grieve, 1984). For this reason, the degrees of freedom were corrected using GreenhouseGeisser estimates of sphericity (ε = .79). Levene’s test of equality of error variances was significant for effort [F (2, 165) = 3.59, p = .030] and time [F (2, 165) = 3.37, p = .037] but not significant for money [F (2, 165) = .87, p = .422]. Though the assumption of equal variances was violated for effort and time, the F-test is generally regarded as robust against this violation (Rheinheimer, 1999).

There was a significant main effect of initial-investment ratio when holding loss aversion constant, F (2, 164) = 7.93, p = .001, η 2 = .088. Pairwise comparisons indicated no significant differences between initial-investment ratios of 1:2 and 1:3, p = .07, 95%CI = [−.05, 1.88] or between ratios of 1:3 and 1:5, p = .34, 95%CI = [ .32,.1.58]. There was a significant difference between ratios 1:2 and 1:5, p < .001, 95%CI = [.60, 2.48]. When SCF scores were transformed to compensate for positive skewness, the difference between initial-investment ratios of 1:2 and 1:3 also became significant, p = .043, 95%CI = [.01,.49].

H 1. The mean total SCF score (across all initialinvestment ratios) was M = 2.58 (SD = 2.14 for participants in the effort condition), M = 2.94 (SD = 2.20) for those in the time condition, and M = 4.07 (SD = 2.81) for those in the money condition. There was a significant main effect of initial-investment type when loss aversion was held constant, F(1.58, 259.61) = 60.40, p < .001, η 2 = .269. Bonferroni pairwise comparisons indicated significant differences between effort and time, p = .001, 95% CI = [.13, .59], between effort and money, p < .001, 95% CI = [1.10, 1.86], and between time and money, p< .001, 95% CI = [.77, 1.47].

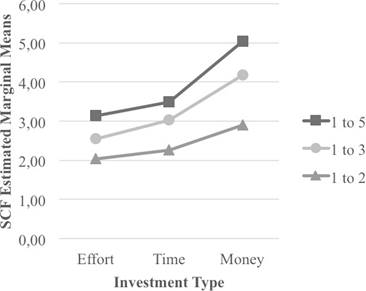

There was a significant interaction between the initialinvestment type and the initial-investment ratio when holding loss aversion constant, F (3.17, 259.61) = 3.33, p =.018, η 2 = .039. Figure 1 shows the estimated marginal means of the SCF score by initial-investment type and ratio when loss aversion was held constant. The SCF scores increased from effort, to time, to money, but this pattern became even more apparent as the initialinvestment ratio increased from 1:2 to 1:3 to 1:5. There were small differences in the SCF score between investment types when the ratio was 1:2 but larger differences across investment types for ratios 1:3 and 1:5.

Figure 1 Estimated marginal means of the SCF score for each investment type and ratio. Loss-aversion scores were held constant at 3.69.

H 1 was confirmed, as the SCF was more likely when the initial investment was money, M = 4.07 and less likely when it was expressed as time, M = 2.94, or as effort, M = 2.58. All pairwise differences were statistically significant. This finding is consistent with Soman (2001) in which the investment of time produced the SCF less often than money did and provides new evidence that the investment of effort can also produce the SCF.

H 2. Loss aversion was a significant covariate in the model, F (1, 164) = 4.13, p = .044, η 2 = .025. However, the correlation between total SCF scores across investment type and loss-aversion scores was not significant at α 2 tail = .05, r = .13, p = .094. In an exploratory analysis, additional correlations were derived for SCF scores in terms of time, effort, or money, rather than the aggregate. The results indicated non-significant negative correlations, rather than positive ones as specified by the hypothesis, between loss aversion and SCF scores involving effort (r = .09, p = .235), time (r = .14, p = .071), and money (r = .12, p = .117). Therefore, H 2 was not supported.

4. Discussion

In this study, we explored factors that influence the occurrence of the SCF. We replicated findings regarding initial-investments levels using percentages rather than fixed sums.

Our research was one of the first to compare three different types of investment-time, effort, and money-in relation to the SCF using a scenario-based procedure. We also varied the relative level of initial investments and showed that their ratio was directly related to the likelihood of the SCF regardless of investment type. However, we failed to provide evidence for a direct relation between loss aversion and the SCF.

Limitations of our study should be considered in future research. The effects of initial-investment type and level aligned with previous research findings. Nevertheless, some participants reported that describing investments in terms of percentages was confusing.

The endowment-effect task used as a measure of loss aversion produced different results than those reported previously. In the study by Gächter et al. (2007), only 5 percent of participants produced a negative loss-aversion score (WTA < WTP ), and the ratio of mean WTA to mean WTP was 1.95. In our study, 32 percent of participants produced a negative score, the mean WTA was 21.44 (SD = 8.37), and the mean WTP , 17.46 (SD = 7.65), a ratio of 1.22. The differences may be attributable to methodologies. For example, in the Gächter et al. study, participants could purchase and sell a miniature model car that was placed directly in front of them, allowing them full access to it.

Our participants were students at a religiously affiliated university and shared a similar religious background that stresses generosity to others. This factor may have enhanced the offer price for the lamp and reduced the asking price, thus decreasing the WTA-to-WTP ratio. This admittedly speculative possibility may merit further research.

Some implications of our findings may be important. First, the SCF is more likely to occur with relatively larger initial investments. This may be an important consideration for policymakers (see also Arkes & Blumer, 1985). Second, the SCF is most likely to occur when the initial investment is money. This finding may be useful for programs designed to teach rational decision making. Future research could also explore potential adaptive benefits of the SCF (Gigerenzer, 2008).

It may be valuable to create environments that capitalize on decision-making fallacies rather than try to reduce them (R. H. Thaler & Sunstein, 2008). For example, (Volpp et al., 2008) used deposit contracts to help participants lose weight. The contract included a monetary investment made by the participant that was lost if his or her weight goal was not achieved. Our findings suggest that such contracts would be most successful when the deposit is monetary and relatively large.