English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Cited by Google

Cited by Google  Similars in

SciELO

Similars in

SciELO  Similars in Google

Similars in Google

Permalink

PermalinkIntroduction

The standard neoclassical paradigm of financial economics assumes that investors react to noteworthy news events by adjusting their investment portfolios because these events change the risk return profile of securities. Therefore, changes in the money supply, particularly narrow money (M1), are important indicators of changes in future macroeconomic conditions such as inflation, interest rate and unemployment, and so on that may affect share prices; sophisticated and unsophisticated investors alike will react according to their ability to access and understand research information and to reposition their portfolios. More specifically, neoclassical economists theorized that an increase in money supply strengthens the stock prices. Conversely, a fall in money supply should slow down the stock prices. In this framework, money supply will serve as a cause variable to affect share prices.

The post-Keynesian school of economics, based on its view that individuals allocate their wealth among the narrowly defined money and other financial assets (Froyen 2009, p. 100), questioned the directional causality of the above hypothesized relationship. This school of thought posits that movements in narrow money supply reflect the shift of money from liquidating other assets to transaction deposits and vice versa because of the preceding changes in stock prices. For example, rises in stock prices induce investors to liquidate their other assets to use the fund to purchase stocks and other financial assets. In this portfolio adjustment process, transaction deposits tend to increase, which in turn raises money supply. The trend is reversed when assets and stock prices are falling. As a result of this, some post-Keynesian economists argue that changes in stock prices cause changes in money supply and not the reverse.

The rationale for theoretically hypothesizing asymmetric adjustment process of the stock prices to the long run equilibrium can be attributed to the seemingly opposite effects of the efficient market hypothesis and the countercyclical monetary policy over different phases of business cycles or when monetary policy is used to counter negative contagions of international economic events such as the recent US subprime mortgage crisis and the current global crisis due to the European sovereign deb. For instance, during the contractionary phases of business cycles, the countercyclical monetary policy would usually increase the money supply reducing market interest rates, while the information from that state of the economy would precipitate investors to resist adjusting their required risk premium on the stock market portfolio downward because their perceived market portfolio risk increases. Thus, the stock prices only increase slowly. By the same logic, it may be argued that, during the expansionary phases of business cycles, investors are less likely to resist adjusting their required risk premium on the stock market portfolio downward while monetary authority is expected to reduce the growth in the money supply, raising market interest rates. Therefore, the stock prices more likely react to monetary policy actions asymmetrically over different phases of business cycles. Thus, if a corporation only relies on stock as the only source of capital, the monetary policy will affect its cost of capital differently. Based on the above analysis, it is hypothesized that the stock prices would more likely react to monetary policy actions asymmetrically over different phases of business cycles.

The article considers narrow money supply as broad money supply’s component time deposit is being rarely used in the share market. The asymmetric response of the stock prices to the changes in the money supply, if exists and is different from the behaviors of instruments in the direct financing segment of the financial market, may make equity (debt)-market-dependent firms more financially vulnerable to business cycle fluctuations than firms with access to other sources of financing. Thus, in their formulation of monetary policy, the policymakers should know the countercyclical monetary policy may have different effects due to stock price asymmetries. Additionally, keeping pace with the age of globalization, the equity market has been increasingly internationalized. Therefore, modeling the asymmetry in the Colombian stock prices may provide a better understanding of the relationship between countercyclical monetary policy and the equity markets in the context of a Latin American developing country with a bilateral trade agreement with her powerful northern neighboring economy of the United States. Considering the, this study empirically investigates neoclassical and post-Keynesian co-integrating relationships and the nature of the causality between the Colombian money supply and stock prices. To formally investigate these possibilities, this study follows Thompson’s (2006) approach to specify and estimate the threshold autoregressive (TAR) model, developed by Enders and Siklos (2001), to test for asymmetric co-integrating relationship and Granger causality between the Colombian narrow money supply and share prices using monthly data. This is to be noted here that such relationships were not examined before for Colombia or other Latin American countries. The findings of this study should be of much interest to policy makers, bankers, home and foreign investors, academics, and researchers.

The remainder of this paper is organized as follows: The next section reviews the current literature; the following section summarizes the Colombian financial sector; the section that follows describes the data for this study and some descriptive statistics; the following section briefly describes the methodology that will be used in the investigation and reports the empirical results; the nest section discusses the empirical findings and implications; and the final section provides some concluding remarks.

Brief literature review

This paper will examine possible asymmetric behavior in the response of stock prices to monetary policy shocks. Such asymmetries in financial market instruments have been studied extensively and documented in the literature of the indirect financing segment of the financial industry. Arak et al. (1983), Goldberger (1984), Forbes and Mayne (1989), Levine and Loeb (1989), Mester and Saunders (1995), Dueker (2000), and Tkacz (2001) report asymmetries in the U.S. prime lending rate. Thompson (2006) confirms the existence of asymmetries in the US prime lending-deposit rate spread. Cook and Hahn (1989), Moazzami (1999), and Sarno and Thornton (2003) find asymmetries in U.S. Treasury securities. Frost and Bowden (1999) and Scholnick (1999) report asymmetries in mortgage rates in New Zealand, and Canada. Heffernan (1997) and Hofmann and Mizen (2004) indicate asymmetric behavior of retail rates in the United Kingdom. Hannan and Berger (1991), and Neumark and Sharpe (1992), Diebold and Sharpe (1992) examine and found asymmetries in various deposit rates. Nguyen and Islam (2010) find asymmetries in the Thai lending-deposit rate spread and attributed it to oligopolistic nature of the Thai banking industry, Nguyen et al. (2010) report asymmetric cointegration between the US money supply M1 and S & P 500 equity index.

The Colombian financial sector

At the end of the 1980s, Colombia’s financial system, including several state-owned institutions, was small, overregulated, and highly specialized. Also, the spread between the lending and deposit rate was high. The high market rates prevented the financial institutions from channeling funds from savers to borrowers which in turn would hinder the economic growth, industrialization, as well as social progress of the country. Over the 1990s, financial sector reforms promoted competition, creatinga more efficient financial system that transform Colombian economy. The reforms allowed easy entries into the financial sector; improved regulations; and simplified mergers, conversions, breakups to promote bank businesses, and allowed foreign investment.

The financial crisis of the late 1990s affected mainly the less efficient public financial institutions with portfolios of lower-quality loans, and the savings and loan corporations lending heavily in-home mortgages whose values had shrunk significantly after the boom years. Consequently, these financial institutions suffered from losses between 1998 and 2001. The government responded to the crisis by an effective but fiscally expensive action and then allowing commercial banks to absorb the former mortgage institutions in 1999 (Colombia: A Country Study 2010, pp. 181-83).

Additionally, in 1991 the new constitution was inaugurated that abolished the 1967 law as part of Colombia’s pro-market reforms and removed many restrictions on capital movements. It also allowed the exchange rate to float within a band. In the same year, the large public and private foreign debt made the country vulnerable, and speculative attacks led the Central Bank to twice devalue the foreignexchange band and then to allow the exchange rate to float after a precautionary three-year extendedfund facility had been agreed with the IMF. In this agreement, the Central Bank reserved the right to intervene in the foreign-exchange market (Colombia: A Country Study 2010, p. 194). Also, as of 2007, Colombia had 60 financial establishments: 16 banks, 33 leasing and finance corporations, and 11 public specialized institutions. In 2006 domestic banks held approximately 80 percent of the financial-sector assets and foreign banks, 20 percent (Colombia: A Country Study 2010, p. 184).

As to the equity market institutional arrangements, the current Colombian stock exchange is the Stock Exchange of Colombia (Bolsa de Valores de Colombia), also known as BVC. The Stock Exchange of Colombia was created on July 3, 2001 by merging the then three existing stock exchanges in Colombia: Bogota Stock Exchange (Bolsa de Bogota), Medellin Stock Exchange (Bolsa de Medelin) and Cali’s Western Stock Exchange (Bolsa de Occidente). Stock Exchange of Colombia maintains offices in Bogota, Medellin, Pereira, and Cali. As of September 1, 2010, the Stock Exchange of Colombia had a market capitalization of 200 billion US dollars and 89 listed companies. Interestingly, the capital market authorities planned to unify the sock markets of Colombia, Chile, and Peru in the Stock Market in the Andes in 2011.

Regarding the commercial relation to the US, the US and Colombia have begun to negotiate for the US Andean Free Trade Agreement (AFTA) since early 2004. The initiative included Colombia, Ecuador, Peru, and Bolivia. Because of political upheaval at home, Bolivia moved to observer status at the end of July 2005. On November 22, 2006, Deputy US Trade Representative John Veroneau signed the Agreement on behalf of the United States. However, under pressure from congressional Democrats, the Bush administration renegotiated the agreement to include more stringent environmental and labor standards. It was signed again in 2007. Finally, this free trade agreement linking the economies of the Andean pack closer to the US economy as NAFTA did to the US, Canadian, and Mexican economies was approved by the US Congress and signed into law by President Obama in October 2011.

In the implementation of this agreement, Colombia agreed to eliminate measures that prevented US firms from hiring US professionals, and to phaseout market restrictions in cable television. Colombia also agreed to provide improved access for U.S. suppliers of portfolio management services. Additionally, over 80 percent of US exports of consumer and industrial products to Colombia will become duty free immediately, with remaining tariffs phased out over 10 years. With average tariffs on US industrial exports ranging from 7.4 to 14.6 percent, this will substantially increase US exports. As estimated by the International Trade Commission, the tariff reductions in the Agreement will expand exports of US goods alone by more than $1.1 billion, supporting thousands of additional American jobs and increasing US GDP by $2.5 billion.

The data and some descriptive statistics

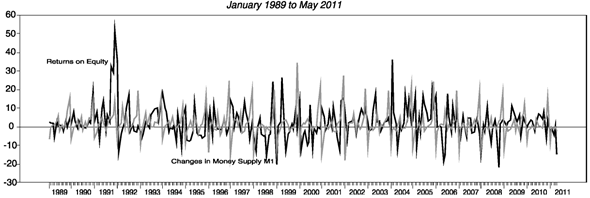

This study uses data on the Colombian monthly money supply M1 and share price index as a proxy for the market stock price index from International Financial Statistics, published by the IMF, over the period 1989:01 to 2011:05. The monthly share price index and the money supply are expressed in monthly percentage changes. Monthly percentage changes in the share price index, which are used as a proxy measure for the returns on the market equity portfolio, and monthly percentage changes in the monthly money supply are denoted by SPt and MSt respectively. Throughout this study, SPt and MSt are referred to as return on the equity and the money supply. Also, the difference between the return on the equity portfolio and the monthly percentage change in money supply M1 is referred to as the equity return-money supply M1 spread, denoted by MPt. Finally, since money supply M1 is the intermediate objective of the country’s monetary authority, changes in money supply are taken to be countercyclical monetary policy actions by the Colombian monetary authority in this study.

Figure 1 displays the behavior of the returns on the Colombian equity market, defined as the monthly percentage changes in the share price, and monthly percentage changes in money supply M1 over the sample period. The descriptive statistics reveal that the monthly percentage change in money supply M1 mean during the sample period was 2.35 percent, and ranged from -21.86 percent to 51.50 percent, with the standard deviation equal to 8.89 percent; while the mean monthly percentage change in share prices was 1.63 percent, and ranged from -17.92 percent to 34.31 percent, with the standard deviation equal to 7.03 percent. Moreover, given a level of the share price index, a decrease in the monthly money supply M1-contractionay countercyclical monetary policy actions-would widen the spread between the monthly percentage changes in share price index and in the monthly money supply M1. The opposite is true if the money supply M1 changes in the other direction due to the expansionary countercyclical monetary policy activities.

Methodology and structural break

Econometrically, two important characteristics of the time series under consideration for cointegration analysis that must be first considered are their structural breaks and cointegration. To discern the structural break possibility and to allow for the possibility of endogenous breaks in the spread between the Colombian equity returns and the monthly percentage changes in the money supply M1, following Perron’s (1997) procedure, an endogenous unit root test function with the intercept, slope, and the dummy were specified and estimated to test the hypothesis that Colombian equity return and the monthly percentage change in the money supply M1 spread has a unit root.

where DU=1(t>Tb) is a post-break constant dummy variable; t is a linear time trend; DT=1(t>Tb) t is a post-break slope dummy variable; D(Tb)=1(t=Tb+1) is the break dummy variable; and Bt are whitenoise error terms. The null hypothesis of a unit root is stated as

Β=1 The break date,Tb,is selected based on the minimum t-statistic for testing

B=1 (see Perron, 1997, pp. 358-359).

The estimation results of Perron’s endogenous unit root tests are summarized in Table 1. The postbreak intercept dummy variable, DU, is positive, while the post-break slope dummy variable, DT, is negative and they are significant at any conventional. Additionally, the break dummy variable, D(Tb ), is positive and statistically significant at 1 percent level. The results of this test suggest that the Colombian equity return-money supply spread followed a stationary trend process with a break date of December 1991, corresponding inauguration of the Colombian new constitution and its attendant economic and financial reforms.

Table 1: Perron’s Endogenous Unit Root Test, Colombian Monthly Data, 1989:01 to 2011:05

*Notes: Critical values for t-statistics in parentheses: Critical values-based n = 100 sample for the break date (Perron, 1997). “*” and “**” indicate significance at 1 percent and 5 percent levels

The Dickey-Fuller standard unit root tests and their extensions assume that the adjustment process is symmetric. If the adjustment process is asymmetric, then the implicitly assumed restrictive symmetric adjustment is indicative of model misspecification. To formally investigate the possibility of asymmetric adjustment process, the threshold autoregressive (TAR) method developed by Enders and Siklos (2001) are estimated to examine the behavior of the monthly percentage changes in the Colombian money supply M1, equity returns their spread.

The threshold autoregressive model allows the degree of autoregressive decay to depend on the state of the Colombian equity return-money supply spread, (i.e., “deepness” of cycles). The estimated TAR model empirically reveals if the spread tends to revert to the long-run position faster when the spread is above or below the threshold. Therefore, TAR model indicates whether troughs or peaks persist more when shocks push the spread out of it long term path. In this model’s specification, the null hypothesis that the Colombian equity return money supply spread contains a unit root can be expressed as P1 = P2, while the hypothesis that the spread is stationary with symmetric adjustments can be stated as P1 = P2.

To formally examine the behavior of the Colombian equity return-money supply spread, this study follows Thompson (2006) to regress the equity return-money supply spread on a constant, linear intercept dummy (with values of zero prior to December 1991 and values of one for December 1991 and thereafter). The saved residuals from the above estimated model, denoted by, are then used to estimate the following TAR model

where and the lagged values of are meant to yield uncorrelated residuals. As defined by Enders and Granger (1998), the Heaviside indicator function for the TAR specification is given as:

Empirical results

The overall empirical results in Table 2 indicates that the estimation results are devoid of serial correlation and have good predicting power as evidenced by the Ljung-Box statistics and the overall F-statistics, respectively. With the calculated statistic= 54.0081, the null hypothesis of a unit root (P1 = P2=0) is rejected at the 1 percent significance level (i.e. the spread is stationary). Given the partial test statistic F = 16.5517, the null hypothesis of symmetry, P1 = P2 is also rejected at any conventional significance level. Thus, the empirical results indicate that adjustments around the threshold value of the Colombian equity returnmoney supply M1 spread are asymmetric. In fact, the point estimates suggest that the spread tends to decay at the rate of = -7.3797 for above the threshold, = -7.3797 and at the rate of |ρ2| =1.8761 forbelow the threshold. Moreover, both ?1 <0, ρ2 <0 and (1+ ρ1) (1+ ρ2) < 1 are statistically significant at any conventional level, As shown by Petrucelli and Woolford (1984), the necessary and sufficient condition for the spread to be stationary is: ?1 <0, ρ2 <0 and (1+ ρ1) (1+ ρ2) < 1; thus, the estimates of 1.2 and satisfythe stationary (convergence) conditions.. About the stationarity of the spread, Ewing et al. (2006, p.14) pointed out that this simple finding is consisting.

Table 2: Unit Root and Tests of Asymmetry, Colombian Monthly Data, 1989:01 to 2011:05

*Notes: The null hypothesis of a unit root,H0 : ρ1 = ρ2 =0, uses the critical values from Enders and Siklos (2001, p. 170, Table 1 for four lagged changes and n = 100).“*” indicates 1 percent level of significance. The null hypothesis of symmetry, H0 : ρ1 = ρ2, uses the standard F distribution. is the threshold value determined via the Chan’s (1993) method? QLB (8) denotes the Ljung-Box Q-statistic with 8 lags.

Given |ρ2|>|ρ1|, the return on equity and the monthly percentage change in the Colombian money supply M1 spread adjusts to the threshold value slower when a contractionary countercyclical policy action or an economic shock causes the money supply M1 to fall relative to the share price index, widening their spread, than when an expansionary countercyclical monetary policy action or a shock causes money supply M1 to move in the opposite direction, narrowing their spread.

The presence of asymmetric adjustments in the Colombian equity return-money supply M1 spread necessitates the estimation of an TAR VEC model to further investigate the short-run and long-run dynamics with respect to the return on the Colombian equity (SPt) and the money supply M1 (MSt).

wherei = 1,2 and It is set in accordance with equation (3). As pointed out by Thompson (2006, p. 327-328) the above specified TAR VEC model differs from the conventional errortent with the two underlying series that comprise the spread (the of the monthly percentage changes in the Colombian money supply M1 and in share price index or equity return) being co-integrated in the conventional, linear combination sense.

correction models by allowing asymmetric adjustments toward the long-run equilibrium. Also, the asymmetric error correctional model replaces the single symmetric error correction term with two error correction terms. Thus, in addition to estimating the long-run equilibrium relationship and asymmetric adjustment, the model also allows for tests of short run dynamic between changes in the monthly percentage changes in the Colombian money supply M1 and in equity return. This in turn reveals the nature of their Granger causality.

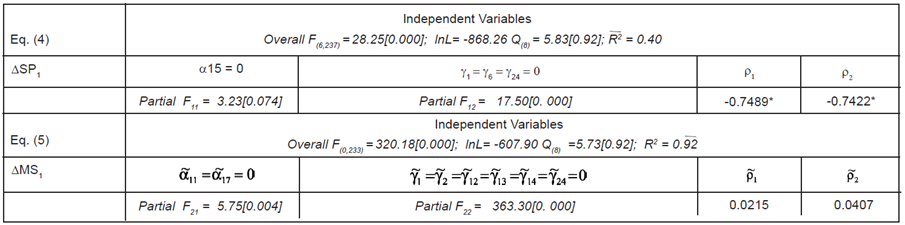

The estimation results are reported in Table 3 In the summary of the estimation results, the partial Fij represents the calculated partial F-statistics with the p-value in squared brackets testing the null hypothesis that all coefficients are equal to zero. The t-statistics are reported with “*” indicating the 1 percent significant level. QLB (8) is the Ljung-Box statistics and its significance is in squared brackets, testing for the first eight of the residual autocorrelations to be jointly equal to zero. ln L is the log likelihood. The overall Fstatistic with “*” indicates the significance level of 1 percent.

Table 3: Asymmetric Error Correction Model, Colombian Monthly Data, 1989:01 to 2011:05

Notes: Partial F-statistics for lagged values of changes in the change in stock price and money supply M1, respectively, are reported under the specified null hypotheses. Q(8) is the Ljung-Box Q-statistic to test for serial correlation up to 8 lags. “*” indicates 1 percent level of significance of the t-statistics.

Overall empirical results suggest that the estimated equation (4) is absent of serial correlation and have good predicting power as evidenced by the LjungBox statistics and the overall F-statistics, respectively. As to the short-run dynamic adjustment, the calculated partial F-statistics in equations (4) and (5) indicate bidirectional Granger-causality between the monthly percentage change in the Colombian money supply M1 and equity returns. These results In addition to revealing the short-run dynamic Granger-causality, the asymmetric error correction model also captures the long run adjustments of the lending and deposit rates. |ρ2|>|ρ1|, in equation (4) is consistent with the TAR model’s estimation results and an indication that the Colombian equity returns and the monthly percentage change in the money supply M1 spread adjusts to the threshold value slower when a contractionary countercyclical policy action or an economic shock causes the money supply M1to fall relative to the share price index, widening the spread. Additionally, both and are statistically significant at 1 percent level. Economically, this result suggests that the Colombian return on equity responds more strongly to contractionary than to expansionary monetary policy in the long run. With regard to the money supply M1, the estimation results for equation (5) show that, but neither nor is significant. These empirical findings suggest that the adjustments to the long-run threshold aredone imply that the monthly percentage change in the Colombian money supply M1 and equity return adjustments affected each other’s movements, i.e., there is evidence of Granger bi-directional causality. These empirical findings suggest that both the neoclassical and post Keynesian positions on the relationship between money supply and return on equity prevail in the Colombian financial market in the short run, solely by the return on equity. As to the short run, the Granger bidirectional causality indicate that investors in Colombian equity market respond to countercyclical monetary policy and the Colombian monetary authority uses the policy to manage the equity market.

Discussion of empirical findings and implications

As to the empirical results from the estimations of equations (4) and (5) for the long run, these findings seem to suggest that the Colombian monetary authority either use monetary policy only to influence the equity market in the short run or has not been successfully in influencing the stock market with the monetary policy in the long run.

Possibly, the most important contribution of this study to the literature as well as to the investment strategies is the empirically determination of the time lag of the bidirectional Granger causality between the Colombian countercyclical monetary policy, as reflected in changes in money supply, and the equity market in the short run. Statistically, the retentions of the estimated coefficients αi’s and yj’s of equation (4) and the estimated coefficients ai’s and yj’s of equation (5) are of based on a 5 percent significance level.

Economically, the inclusions of coefficients a15 and of equation (4) indicate that that the change the equity index fifteen months ago and the change in the money supply twenty four months ago help predict the change of the Colombian stock price index in the current month. Likewise, the inclusions of the coefficients and of equation (5) suggest that the Colombian monetary authority looked at the change in the equity index seventeen months ago and the changes in the money supply M1 in the last two years to formulate its countercyclical monetary policy in the current month.

From the portfolio repositioning perspective, the retentions of the estimated coefficients of equation (4) indicate changes in countercyclical monetary policy actions, as reflected in changes in money supply M1, back to two years ago affect the current change in the equity return. This finding implies that after implemented, it will take two years for the implemented countercyclical monetary policy to achieve its effectiveness fully in the Colombian equity market. Customarily, the time period when the adverse economic condition occurs until the corrective policy action achieves its effectiveness fully is divided into the recognition lag, the action lag, and impact lag; therefore, the empirical findings suggest that the impact lag of Colombian countercyclical monetary policy on the equity market was two years. Thus, however long it takes for the Colombian monetary authority to recognize the macroeconomic problems (recognition lag) and to formulate and implement (action lag) the corrective policy actions, it will take two years for the implemented countercyclical monetary policy to achieve its full effectiveness. These empirical findings should be very useful for both domestic and international investors, who are interested in investing in Colombian stock market; particularly, in responding to the negative contagions of the US subprime mortgage and the current European sovereign debt crises, the Colombian monetary authority has increased the money supply significantly.

Concluding remarks

The results of this study empirically confirm the co-integration relationship between the stock price index and the narrowly defined money supply. In fact, their co-integrating relationships are asymmetric. This asymmetric relationship indicates that the countercyclical monetary policies affect the cost to raise new financial resources of corporations differently in different phases of business cycles in the long-run. More specifically, the results reveal that the stock price adjusts more slowly to the threshold value when the Colombian monetary authority eases the money supply widening the equity returnmoney supply M1 spread than when the monetary authority tightens the monetary policy, narrowing the spread. These findings suggest that the stock price is more responsive to signals of possible contractionary monetary policy as reflected in the decline money supply M1.

The empirical results in turn suggest that equity (debt)-market-dependent firms are more vulnerable to business cycle fluctuations (at least in regard to their cost of capital) than firms with access to other sources of financing. Thus, policymakers should be aware that counter-cyclical monetary policy may have different effects due to the asymmetric behavior of stock prices in their formulation of monetary policy. Additionally, keeping pace with the age of globalization, the equity market has been increasingly internationalized; these findings may provide a better understanding of the countercyclical monetary policy and the equity market in Latin American economies.

With regard to the short-run dynamic co-integration as measured by the Granger causality between stock price and the money supply, the partial F-statistics in equations (4) and (5) reveal the bidirectional Granger causality between the Columbian returns on equity and changes in money supply. This empirical finding suggests that both the neoclassical and post Keynesian positions on the relationship between equity returns and money supply M1 present in the Colombian financial market. Possibly, the most useful information for the domestic and international investors, who are interested in the Colombian equity market, is the impact lag of the Colombian countercyclical monetary policy is two years.