Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Citado por Google

Citado por Google  Similares em

SciELO

Similares em

SciELO  Similares em Google

Similares em Google

Permalink

PermalinkINTRODUCTION

This paper analyzes the real economic convergence of Western Balkan countries (Albania, Bosnia and Herzegovina, FYR Macedonia, Kosovo,1 Montenegro and Serbia2) towards the EU-15 members states, that is, countries that accessed the European Union before the 2004 enlargement (Germany, France, Italy, Belgium, the Netherlands, Luxembourg, the United Kingdom, Ireland, Greece, Portugal, Spain, Austria, Finland, and Sweden). We focus on absolute (unconditional) and conditional beta convergence in the period 2004-2016, with two sub-periods: the pre-crisis period 2004-2008 and the period of crisis 2009-2013.

Economic convergence is defined as a tendency of poor countries to grow faster than rich countries (Barro & Sala-i-Martin, 1992). Convergence has always been in the focus of the European Union. With the accession of less developed states-the so-called EU cohesion countries (Ireland in 1973, Greece in 1981, and Portugal and Spain in 1986)-, the European Regional Development Fund was created in 1975 (Berend, 2016).

With the fall of the Berlin Wall and the beginning of the transition process in Central and Eastern Europe, the European Union continued to focus on convergence. In order to join the Union, transition countries have to fulfill certain economic, political, and institutional criteria: the Copenhagen criteria (1993). The countries have access to pre-accession funds, so that they can go through the transition process faster. Once they join the European Union, the new Member States eventually have to fulfill the Maastrich criteria, or convergence criteria, and join Europe's Economic and Monetary Union (i.e. adopt euro as their currency). From the experience of the European Union, convergence does not have to be defined only as a tendency of poor countries to grow faster than rich countries, but as an assimilation of countries.

The Western Balkan region is expected to be the next group of countries to join the European Union. These countries also started their transition process in the early 1990s, and the process should be faster. The countries share a similar economic history with the CEE countries, which joined the European Union in 2004, 2007, and 2013, thus Western Balkan countries could learn from the experience of the CEE countries. However, none of these countries are ready to join the European Union in the next few years. The catching-up process in the CEE countries that are EU Member States has been generally faster than in the Western Balkan region, partly due to the destructive impact of the Yugoslav wars in the 1990s, which delayed the economic transition process in many Western Balkan economies by nearly a decade (Zuk et al., 2018).

The Western Balkan countries have made some progress on their path towards EU membership and they converge towards the EU-28 Member States (Siljak & Nagy, 2018). The countries have signed the Stabilization and Association Agreement (SAA); four of them are candidate countries3 and only Kosovo does not have a visa-free regime with the European Union. The European Commission (2015) reports that the SAA Countries are moderately prepared to cope with competitive pressure and market forces within the European Union. Bosnia and Herzegovina and Kosovo are at an early stage in developing a functioning market economy.

The main objective of this research is to analyze whether the Western Balkan countries converge towards the old Member States of the European Union (EU-15). Other objectives are: to analyze the convergence process between different time periods, because it could evidence whether the recent financial crisis has negatively affected convergence; as well as to determine which policies the countries should pursue in order to increase per capita growth rate.

There are three research hypotheses of this analysis. The first hypothesis is that the absolute convergence rate is lower during the crisis period, compared to the pre-crisis period. The second hypothesis is that the conditional convergence process of the analyzed countries is slower in the crisis period, compared to the pre-crisis period, when economic variables are included in the models. The third hypothesis is that the conditional convergence process of the analyzed countries is slower in the crisis period, compared to the pre-crisis period, when economic and socio-political variables are included in the models. The sub-hypotheses are that the Western Balkan countries converge from below and that they act as a club.

The paper is organized as follows: Section 2 presents the theoretical background on convergence, followed by Methodology and Data in Section 3. Section 4 describes and discusses the empirical findings on absolute and conditional beta convergence. Section 5 presents the conclusions.

LITERATURE REVIEW

Convergence was popularized by Barro and Salai-Martin (1992), who analyze the convergence process across the forty-eight contiguous U.S. states in the period 1840-1988. The empirical results show that the speed of convergence is 2% per year, regardless of the time period. The authors conduct their respective research. Barro (1991) analyzes the impact of primary and secondary school enrollments, number of political assassinations, investment rates, and measures of distortions in capital markets on convergence. The research shows that education is an important determinant of growth rate; investment rate is strongly positively correlated to growth, while the coefficient of the initial income level is significantly negative. Sala-i-Martin (1994) confirms the speed of convergence of 2% per year across data sets.

Economic literature on convergence in Europe mainly focuses on the convergence process among the EU Member States. Potential member states are somehow neglected in the analyses.

Matkowski and Prochniak (2004) investigate the convergence process of eight CEE countries to the EU-15 between 1993 and 2001. The results show that the accession countries reveal strong economic convergence towards the EU and tend to develop faster than older EU members. Jelnikar and Murmayer (2006) confirm convergence in the EU-25 between 1995 and 2007 (predicted value). The EU-10 group moved closer to the average EU-15 income per capita level.

El Ouardighi and Somun-Kapetanovic (2007) analyze the convergence process of five Western Balkan countries towards the EU-27 between 1989 and 2005. They conclude that income inequality had increased and that convergence in per capita GDP had run at a slow annual rate. The authors (2009) expand the analyzed period to 2008 and conclude that the Western Balkans countries converge in the period 1989-2008, but there are differences in convergence patterns across sub-periods. Borys et al. (2008) investigate the convergence process of five Western Balkan countries towards ten CEE countries in the period 1993-2005. The results show that the main drivers of convergence have been total factor productivity growth and capital deepening, whereas labor has contributed only marginally to economic growth. Botric (2013) includes Croatia in the convergence analysis of the Western Balkan countries towards the EU-15 in the period 1995-2010. The results show that there is no convergence among the analyzed countries. Tsanana et al. (2013) investigate the catching-up process between the Balkan countries and the EU-15 between 1989 and 2009. The results show that the income gap of the Balkan countries relative to the EU-15 remained significant.

Benczes and Szent-Ivanyi (2015) analyze whether the EU countries (excluding Croatia and Luxembourg) converge between 2004 and 2014. The results confirm convergence in the analyzed group and show that the countries can be split into two main clusters: the new and the old Member States. Chapsa et al. (2015) analyze income convergence within the old Member States of the European Union, excluding Luxembourg as an outlier, over the period 1995-2013. The findings provide evidence of conditional convergence in the EU-14. Colak(2015) includes thirty-three countries in the convergence analysis: CEE-10 and SEE-8 towards the EU-15. The results show the presence of both absolute and conditional beta convergence for each group of countries. Oblath et al. (2015) analyze economic convergence in the European Union, excluding Luxembourg and Croatia, in the period 1999-2013, focusing on the ten new CEE members (the EU-10). The results of the analysis show that there was a rapid catch-up in both per capita GDP and general price levels of the less developed EU countries until 2008, followed by a significant slow-down.

Bicanic et al. (2016) investigate the convergence process in Yugoslavia and conclude that there was no beta convergence or sigma convergence, but both kinds of convergence developed with independence. Matkowski et al. (2016) analyze whether the EU-11 countries converge towards the EU-15 in the period 1993-2015. Even though the results confirm convergence, the most intensive convergence was in the period before the financial crisis. The crisis slowed down the convergence process in most CEE countries in the period 2007-2015. Strielkowski and Hõschle (2016) investigate convergence in the European Union and within the groups of countries in the EU. Their results do not show much evidence for the presence of convergence in the EU. They also show that the countries that were EU Members prior to 2004 seem to diverge instead of converge. Grêla et al. (2017) include twenty-six EU Member States in their convergence analysis in the period 1997-2014. The results confirm that per capita GDP growth rates in countries with lower initial per capita GDP level were higherthan in more developed economies. However, convergence was faster in the period 2001-2008 and was interrupted by the global financial crisis. Micallef (2017) also confirms beta convergence in the European Union, as relatively poorer countries experienced faster growth, compared to richer countries.

Alcidi et al. (2018) investigate income convergence in the EU-28 between 2000 and 2015.

The analysis shows that Central and Eastern European countries led the convergence process, while Southern regions have systematically under-performed compared to the EU average. Pipieh and Roszkowska (2018) include twenty transition countries-eight CEE and twelve CIS countries- in the convergence analysis. The analysis of the estimated beta parameters shows that the CEE group has become relatively homogeneous. It also confirms substantial heterogeneity among the CIS countries, as well as a lack of similar convergence patterns among them. Zuk et al. (2018) analyze the sources of economic growth in economies within and outside the European Union. Convergence has been much faster in the countries that became members of the EU than in the Western Balkan countries. Convergence was affected by the recent financial crisis, because it was particularly rapid before the crisis, but slowed down afterwards.

METHODOLOGY AND DATA

There are two types of beta convergence: absolute (unconditional) and conditional. When assumed that countries converge to the same steady state, convergence is absolute. Convergence rate (3 coefficient) is obtained through regression analysis with one dependent and one independent variable. The (3 coefficient captures the rate at which the economy converges towards the steady state during one year. The dependent variable is per capita GDP growth rate, and the independent variable is the initial level of per capita GDP in purchasing powerterms (PPP), computed in natural logarithm:

where β is the convergence coefficient; 'Yi0T is the average annual growth rate of per capita GDP for country ;'; Y 0 is per capita GDP at PPP for country /at the beginning of time interval 0; α is a constant; εi is the stochastic error of the equation; and T is the end of the time interval.

The convergence hypothesis tests whether poor countries grow faster than rich countries, in per capita terms, so the β coefficient has to be negative. If the coefficient is positive, it indicates divergence.

In this analysis, the β coefficient is obtained through a cross-sectional linear regression analysis, using the average rates for a given period. Cross-sectional data is used because it is free of distortions caused by business cycles as well as by various demand-side and supply-side random shocks, both internal and external, that deviate the economy from a path towards the steady-state (Vojinovic et al., 2009, p. 127).

When it is assumed that countries are moving towards different steady states, because they have different structures, convergence is conditional. In the conditional convergence analysis, the β coefficient is obtained through a multiple regression; i.e., the absolute convergence model [1] is expanded with various economic, socio-political or institutional variables. In this analysis, economic variables are inflation rate, economic openness, and gross fixed capital formation, while socio-political variables are general government debt, unemplyoment rate, and population growth rate:

And

where EO is economic openness; Inf is inflation rate; GFCF is gross fixed capital formation; Debt is general government debt; Pop is population growth rate; and Unemp is unemployment rate.

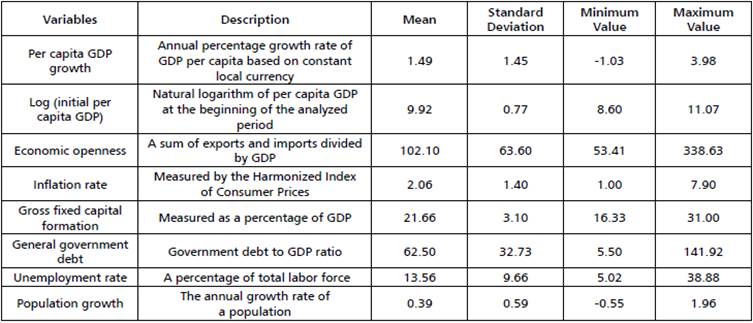

Theoretically, economic openness and gross fixed capital formation are expected to have a positive estimated coefficient. Inflation rate, general government debt, unemployment rate, and population growth rate are expected to have a negative estimated coefficient. This research is based on annual data. Table 1 presents the descriptive statistics of the variables used to estimate absolute and conditional convergence models in the period 2004-2016. The data set includes twenty-one countries.

EMPIRICAL RESULTS

We analyze the beta convergence of the Western Balkan countries towards the EU-15 Member States in the period 2004-2016 and two sub-periods: the period before the recent financial crisis 2004-2008 and the crisis period 2009-2013. We make this subdivision in order to test the research hypotheses on whether the convergence rates in the analyzed group are the lowest during the crisis period. We estimate three models for each period: absolute convergence models (Models 1-3), conditional convergence models when economic variables are included (Models 4-6), and conditional convergence models when economic and socio-political variables are included (Models 7-9). The regression results for absolute convergence in the analyzed periods are presented in Table 2.

Table 2 Absolute/unconditional convergence of the Western Balkan countries towards the EU-15.

Note: *** p<0.01, ** p<0.05, * p<0.1

Source: Authors' calculations based on World Bank data.

The regression results show that the Western Balkan countries converge towards the old Member States of the European Union in every analyzed period. The p coefficient in the period 2004-2016 is -1.41, which means that if the countries in the analyzed group are similar in terms of steady state characteristics, they converge to a common per capita GDP at the rate of 1.41%. In the period 2004-2008, the countries converge at the rate of 2.17%, and this is the only rate that exceeds the reference value of 2% from the Barro and Sala-i-Martin findings. The p coefficients for these two periods are highly significant (p-value=0.000). In the period 2009-2013, the convergence rate is 1.48%, lower than in the pre-crisis period. Therefore, there is not enough evidence to reject the first research hypothesis and we conclude that the recent financial crisis had a negative impact on absolute convergence in the analyzed group.

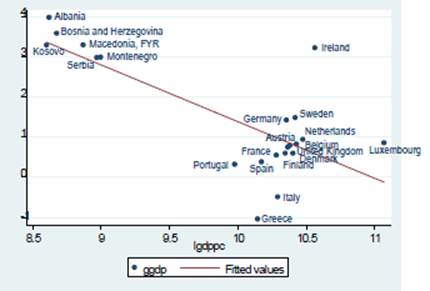

Figure 1 indicates convergence among the analyzed countries during the entire period. The figure plots per capita GDP in the initial year of 2004 (X-axis) against the average annual growth rates of per capita GDP in the period 2004-2016 (Y-axis), and it shows a negative relation between the variables, i.e. the regression line has a downward slope.

Source: Authors' calculations based on World Bank data.

Figure 1 Absolute beta convergence in the WB-EU-15 group, 2004-2016.

Figure 1 shows a polarization between the two groups of countries. The Western Balkan countries act as a club and their average per capita growth rate in the analyzed period was 3.3%. In the EU-15 group, the only country with per capita growth rate similar to the Western Balkans' average is Ireland (3.2%). However, Ireland's per capita GDP in 2004 is almost 6 times higher than the average per capita GDP in the Western Balkan group. The highest average growth rate among the Western Balkan countries was recorded in Albania (4.0%). The average rate in the EU-15 was 0.8%. Greece and Italy are the only countries with negative rates (-1% and -0.5%, respectively), while positive rates range from 0.3% in Portugal to 1.5% in Sweden.

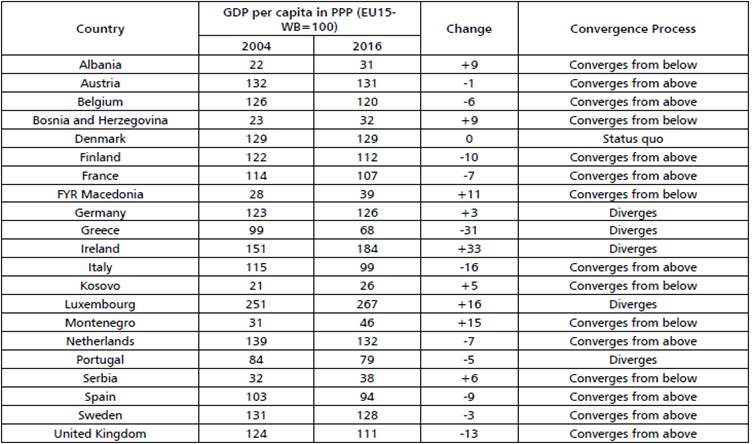

Table 3 presents the convergence process of each country in the analyzed group from 2004 to 2016.

Table 3 Convergence process of the Western Balkan countries and the EU-15.

Source: Authors' calculations based on World Bank data.

The results show that the Western Balkans region converges from below, and the EU-15 countries converge from above or diverge. Germany, Ireland,4 and Luxembourg diverge, due to higher growth rates than the EU-15 average (1.4%, 3.2%, and 0.9%, respectively), while Greece and Portugal diverge due to negative or low growth rates (-1.0% and 0.3%, respectively). The remaining EU-15 Member States converge from above.

Conditional Convergence

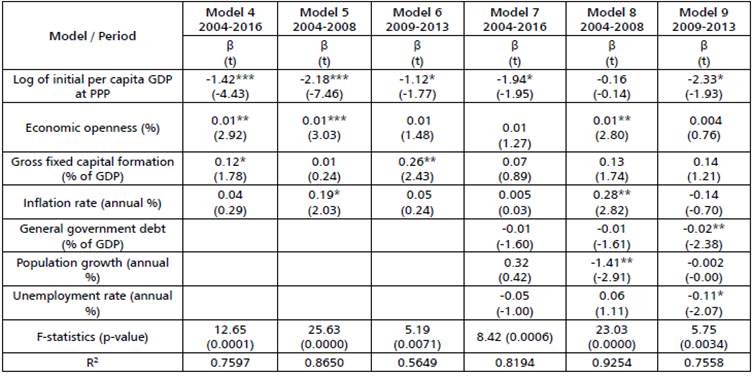

Table 4 presents the regression results for conditional convergence. Models 4-6 only include economic variables, while in Models 7-9 both economic and socio-political variables are included.

Table 4 Conditional convergence of the Western Balkans towards the EU-15.

Note: *** p<0.01, ** p<0.05, * p<0.1

Source: Authors' calculations based on World Bank, IMF, and EUROSTAT data.

The regression results for Models 4-6 show that the Western Balkan countries converge towards the EU-15 in every analyzed period. In the period 2004-2016, the countries converge at the rate of 1.42%. In the pre-crisis period, the convergence rate is 2.18%, and decreases to 1.12% in the period of crisis. Again, the p coefficients for the entire period and the period before the crisis are highly significant (p-value=0.000). Based on the results, we conclude that the recent financial crisis had a negative impact on the conditional convergence process, when only economic variables are included in the models. Therefore, we do not have enough evidence to reject the second hypothesis.

When economic and socio-political variables are included in the models, the countries converge in the entire analyzed period and the crisis period at the rates of 1.94% and 2.33%, respectively. The P coefficient for the period 2004-2008 is negative, but statistically insignificant. The convergence rate for the period of crisis is the highest among the analyzed periods, and we conclude that the recent financial crisis did not affect negatively the conditional convergence process when economic and socio-political variables are included. Therefore, we reject the third research hypothesis.

This research includes three economic variables: economic openness, inflation rate, and gross fixed capital formation; as well as three socio-political variables: general government debt, unemployment rate, and population growth rate. In Models 4-6, all selected macroeconomic variables have positive effects on per capita growth. Economic openness is a determinant of growth in the periods 2004-2016 and 2004-2008, and gross fixed capital formation is a determinant in the periods 20042016 and 2009-2013. Inflation rate is a statistically significant variable only in the period 2004-2008. In Models 7-9, economic openness and inflation rate have a positive effect on per capita growth in the period 2004-2008, while population growth rate has a negative effect. In the crisis period, general government debt and unemployment rate have a negative effect on per capita growth. In the entire analyzed period, none of the selected macroeconomic variables are statistically significant; therefore, they are not determinants of per capita growth.

None of the EU-15 countries had to go through the transition process, but they are not all at the same development level. While Ireland achieved high growth rates, Greece, Portugal, and Spain are still left behind. The convergence of these countries slowed down after their EU accessions (Podkaminer, 2013, p. 4). The roots of the problem go back to the early 1900s, when the least successful countries in Europe were those of the Iberian Peninsula and the Balkans. The main causes of their failure to progress were their social capability, inherited cultural traditions, educational backwardness in the Balkans, and limited resource base. The countries could not adjust to modern technological sectoral requirements and, as a consequence, lost further ground (Berend, 2016, p. 37).

The Western Balkan countries are still going through the transition process from centrally planned to market economies. Some of the characteristics of the centrally planned system are state ownership of the economy, low trade and investment, fixed prices, low debt, and almost nonexistent unemployment rate.

In centrally planned, non-market economies, companies were state-owned, and there was no free trade. As a result, the Western Balkan countries have lower economic openness rates, compared to the EU-15 countries. While the average rate in the EU-15 Member States increased from 100.8% in the period 2004-2008 to 107% in the period 2009-2013, it decreased from 87.8% to 87.7% in the Western Balkans. Gross fixed capital formation decreased in both groups between the analyzed periods: from 25.4% to 23.2% in the Western Balkans, and from 22.7% to 19.8% in the EU-15.

In the centrally planned system, all prices were fixed. When the system collapsed, the countries started to lose control over inflation. Inflation stabilized in the countries of Central Europe and the Baltics in the early 1990s, but in Bulgaria and Romania the first attempts at stabilization failed (Joshi et al., 2014). The countries experienced hyper-inflation of 1058% and 154%, respectively, in 1997. Among the countries of the former Yugoslavia, Serbia has the highest average inflation rate, 8.0%. In the period 1995-2001, the average rate was 62.9% and it fell below 2% in 2015. In Albania, the rate fell from 20.6% in 1998 to 0.4% in 1999, and since 2003, the rate has not exceeded 3.5%. The Western Balkan countries still have higher inflation, compared to the EU-15 group. The inflation rate in the Western Balkans decreased from 4.7% in the pre-crisis period to 3.3% during the period of crisis, while in the EU-15 the rate decreased form 2.4% to 1.7%. Due to the crisis, a significant number of countries in the European Union faced episodes of negative inflation rates (European Commission, 2018). In 2010, Ireland was the only Member State whose inflation rate was negative, -0.9%, mainly due to the severe economic downturn in the country. In 2013 and 2014, Greece had the lowest rate among the EU-15 countries, -0.9% and -1.3%, respectively. The country's inflation rate deviated due to country-specific factors that limited its scope to act as meaningful benchmarks for other Member States (European Commission, 2018, p. 28).

The former Communist countries did not inherit high general government debt from the centrally planned system. Debt rates, as a percentage of GDP, have increased during the recent financial crisis. In the Western Balkans, the average debt rate increased from 30% in the period 2004-2008 to 37.4% in the period 2009-2013. In the pre-crisis period, Kosovo did not record any debt, because the country declared independence from Serbia in 2008. The highest debt rate in this region is in Serbia, 50.5%. In the EU-15, the average rate increased from 56.6% to 79.8%. Twelve EU-15 Member States are also members of the Eurozone. One of the convergence criteria a country needs to fulfill is that its general government debt rate does not exceed 60% of GDP. In 2016, only Denmark, Luxembourg, and Sweden did not exceed the value. Greece had the highest debt rate of 180%, while Ireland's rate decreased from 119.4% in 2013 to 72.8% in 2016.

Unemployment was almost nonexistent in communism. However, with the crises that led to the collapse of the system, unemployment rate jumped from zero to 50% in Yugoslavia's successor states (Berend, 2016). The consequences are still present. The average unemployment rate in the Western Balkan region decreased from 28.4% in the pre-crisis period to 25.3% in the crisis period. In the EU-15, the rate increased from 6.7% to 9.7%. In the period 2004-2016, the lowest average rate among the Western Balkan countries was 14.6% in Albania, which was only 2.7 percentage points lower than the highest rate in the EU-15, 17.3% in Spain. The highest unemployment rate is in Kosovo, 38.9%.

Both groups of countries have experienced a decline in population growth rate. While in the Western Balkan region the rate decreased from -0.04% in the period 2004-2008 to -0.1% in the period 2009-2013, in the EU-15 countries it decreased from 0.7% to 0.5% between the analyzed periods.

CONCLUSION

This paper examines the convergence process of the Western Balkan countries-which are considered to be the next group to join the European Union-towards the EU-15 Member States, countries that were members of the European Union before the 2004 enlargement. The analyzed period is 2004-2016 with two sub-periods: the pre-crisis period 2004-2008, and the crisis period 2009-2013. Two types of beta convergence are analyzed: absolute (unconditional) and conditional convergence.

The empirical results suggest the absolute convergence of the Western Balkan countries towards the EU-15 Member States in every analyzed period. The recent financial crisis had a negative impact on the convergence process, since the convergence rate in the period 2004-2008 is higher than the rate in the period 2009-2013.

Analyzing the convergence process of individual countries between 2004 and 2016, the results show that the Western Balkans countries converge from below, while the EU-15 countries either converge from above or diverge.

The polarization between the analyzed groups is present. The Western Balkan countries act as a club of their own.

When economic variables are included, regression results for the conditional convergence models show the highest convergence rate in the period before the crisis. When economic and sociopolitical variables are included in these models, the convergence rate is the highest in the crisis period, while the P coefficient in the pre-crisis period is not statistically significant. Therefore, there is no sufficient evidence to reject the first and second research hypotheses.

This research shows that selected macro-economic variables have an impact on per capita growth in at least one analyzed period. Economic openness, inflation rate, and gross fixed capital formation have a positive impact on per capita growth, while general government debt, population growth rate, and unemployment have a negative impact.

The Western Balkan countries are transition countries, and for most of them, datasets are not complete. Corruption index or savings rate are commonly used variables in convergence analyses, but these variables could not be used in this research, which is a limitation of this study.

According to the empirical results of this research, the Western Balkan countries should pursue policies that will open their economies to more investment and trade, decrease unemployment, and keep their general government debt and inflation low. These policies should lead to higher per capita growth rates and a faster convergence process.