]]>

Determinação dos prêmios de resseguro para doenças de alto custo na Colômbia através do método de Black-Scholes

Liliana Chicaíza* & David Cabedo**

* Profesora asociada, Universidad Nacional de Colombia. Administradora de Empresas, Universidad Nacional de Colombia. Ph.D. Economía y Gestión de la Salud, Universidad Politécnica de Valencia. Correo electrónico: lachicaizab@unal.edu.co

** Profesor titular, Universidad Jaume I. Licenciado en Ciencias Económicas y Empresariales, Universidad de Valencia. Ph.D. en Administración y Dirección de Empresas, Universidad Jaume I. Correo electrónico: cabedo@cofin.uji.es

Abstract

This article applied the Black-Scholes option valuation formula to calculating high-cost illness reinsurance premiums in the Colombian health system. The coverage pattern used in reinsuring high-cost illnesses was replicated by means of a European call option contract. The option's relevant variables and parameters were adapted to an insurance market context. The premium estimated by the Black- Scholes method fell within the range of premiums estimated by the actuarial method.

Key words:

reinsurance; catastrophic illness; option pricing

]]>Resumen

El artículo hace una aplicación del método de valoración de opciones de Black-Scholes al cálculo de primas de reaseguro de enfermedades de alto costo en el sistema de salud de Colombia. Se replicó el patrón de cobertura utilizado en el reaseguro de enfermedades de alto costo por medio del contrato de una opción call tipo europeo. Las variables y parámetros relevantes de la opción fueron adaptados al contexto del mercado de seguros. La prima estimada por medio de la metodología de Black-Scholes se ubicó dentro del rango estimado por medio del método actuarial.

Palabras clave:

Reaseguro; enfermedades de alto costo; valoración de opciones.

Résumé

L'article applique la méthode de valorisation d'options de Black-Scholes pour le calcul de primes de réassurance de maladies à coût élevé du système de santé de Colombie. Une opposition a été faite au patron de couverture utilisé pour la réassurance de maladies à coût élevé par le biais du contrat d'une option call de type européen. Les variables et paramètres importants de cette option ont été adaptés au contexte du marché d'assurances. La prime estimée au moyen de la méthodologie de Black-Scholes s'est située dans le rang d'estimation par le biais de la méthode actuaire.

Mots-clefs:

réassurance, maladies à coût élevé, valorisation d'options.

]]>Resumo

O artigo faz uma aplicação do método de valoração de opções de Black-Scholes ao cálculo de prêmios de resseguro de doenças de alto custo no sistema de saúde da Colômbia. Replicou-se o padrão de cobertura utilizado no resseguro de doenças de alto custo através de um contrato de uma opção call tipo europeu. As variáveis e parâmetros relevantes da opção foram adaptados ao contexto do mercado de seguros. O prêmio estimado através da metodologia de Black-Scholes localizou-se dentro do rango estimado através do método atuarial.

Palavras chave:

resseguro, doenças de alto custo, valoração de opções.

1. Introduction

The Colombian health system is comprised of Insuring Firms and Providing Firms. Insuring Firms (called Health Promotion Entities or Entidad Promotora de Salud, EPS, in Spanish) take care of its affiliates, the financial resources, organising the service and providing affiliates with risk management and high-cost illness reinsurance. Providing Firms are hospitals, clinics and physicians that actually deliver the health care itself.

This system simulates a competitive market by fixing a price known as "per capita payment unit" (PCPU) and by establishing a product named the Compulsory Health Plan (CHP). The PCPU is the value that the system gives to EPS per affiliate, according to age, gender and geographic location. The CHP is a comprehensive health protection plan covering maternity and general illness in the phases of health promotion and advancement, prevention, diagnosis and treatment of various 1st, 2nd, 3rd and 4th level activities and procedures. With the value of the PCPU per affiliate, insuring firms must guarantee CHP provision (Chicaíza, 2002).

One of the main risks facing insuring firms arises when the cost per insured individual becomes excessive. Reinsurance is the mechanism used by the system to protect EPS against the risk of covering affiliates with high-cost diseases. It is mandatory for insuring firms to reinsure high-cost illnesses. What is legally defined as high cost represents the minimum that must be reinsured. There are two available reinsurance methods:

Both ways of reinsuring high-cost diseases are found in the Colombian Health Care System. However, most EPS prefer the second possibility, since, it avoids discussion about controversial medical questions, and therefore facilitates the recovery of costs from the reinsurance firm[1].

We focus our empirical work on this financial alternative because its coverage pattern can be replicated by using option contracts (Chicaíza and Cabedo, 2007). We use this equivalence to calculate an insurance premium valuation framework by using option pricing theory. Although the equivalence is well known in the theoretical literature, this is the first time that it has been applied to an actual case.

Insurance premiums have been traditionally established by means of actuarial methodologies. The method used here provides an alternative to the traditional ones.

The rest of the paper is structured as follows: in the next section we describe shortly the use of derivatives in risk hedging. In section 3 we propose a method to replicate the hedging pattern of a high-cost illness insurance operation by using option contracts. This section also demonstrates that, in an equilibrium situation, the premium paid for the coverage pattern when using option contracts must be equal to the premium paid when using insurance contracts. In Section 4 we apply the proposed method to value the premium to be paid to the reinsurer in one of the biggest Colombian EPS. We also compare the results thus obtained with those provided by actuarial methods, and in the final section, we summarise the main conclusions of the paper.

]]> 2. Derivatives in risk hedging

Many papers that have been published in recent financial literature show how derivatives in general and options in particular have been used for several kinds of risk hedging. For instance, in electricity markets with uncertainty surrounding spot prices and demand, Bessembinder and Lemmon (2002) developed an equilibrium model that links forward prices with future spot prices for different levels of expected demand and demand risk. Zettl (2002) studied the risks derived from alterations in oil prices and other inputs, and applied the option value theory to the valuation of exploration and production projects in the oil industry, using the discrete binomial model combined with Monte Carlo simulations. Yangxiang Gu (2002) used American-style call options for hedging against risks in real estate prices and proposed that this kind of options be used for employee compensation contracts in the USA.

Karpinski (1998) points out that as options were used for other markets (such as electricity or impressionist paintings); future and simple options were replaced by exotic and more complex options. Although returns have not been consistent, the difficulty involved in quantifying derivatives risk has become clear. In addition to this risk, speculation by unsupervised traders can also bring about financial disasters. The main alternative in confronting this problem has been to seek direct protection against this risk. On the one hand, according to Bhansali (1999), the introduction of credit derivatives and spread options provides protection against credit default risk without introducing any new risk. On the other hand, however, other mechanisms that have been designed, such as variance or volatility swaps (Demeterfi et al., 1999), refer to a future level of volatility. Although these swaps are forward or future contracts on volatility, they can be replicated theoretically by a covered portfolio of appropriately selected standard options. In this way, Das et al. (2001) studied the impact of insolvency probability correlations on credit. Duffe and Zhou (2001) analysed the impact of introducing credit derivatives in banks.

Options have also been used in transactions involving several countries, as in the case of currency options (Geczy et al., 1997), although some authors argue that this has increased world financial instability as there is a lag in the creation of institutions to regulate these transactions (McClintock, 1996).

But perhaps the use of derivatives as hedging tools is most striking in a field where risks have traditionally been managed by other instruments: the insurance operations field. At this point, the contributions on risks associated with natural catastrophes should be pointed out, such as those by Harrington (1997) and Niehaus (2002). The use of options and derivatives has allowed the costs involved in risk coverage to be reduced (Harrington, 1997) although it also seems to have introduced new risks. Niehaus (2002) points out that potential loss due to catastrophic risk has led financial researchers to ask the following questions: to what extent is catastrophic risk being shared? Is its distribution consistent with the notion of optimal risk ensuring? If the distribution is not optimal, what are the market imperfections leading to efficient distribution of catastrophic risk? Are there government policies or private market solutions that lead to a more efficient outcome?

The use of derivatives in this field has transcended the academic discussion and has been consolidated through the creation of specific trading markets. For example, in 1992, the CBOT launched the first coverage tool for the insurance industry: future and option contracts on catastrophic risks. The underlying asset for these products is an accident rate index for catastrophic risks. This index is built from data reported by US firms on premiums paid and insured values. Data availability has contributed to the proliferation of empirical studies on financial markets (Pouget, 2001). The success of these trading markets probably lies in the fact that the coverage framework provided by derivatives replicates those provided by traditional insurance operations.

3. Equivalence between option contracts and insurance contracts

One of the lines of research referred to in the preceding section is the relation between option contracts and insurance operations. We mentioned certain papers that deal with options on risks related to natural catastrophes. In this field coverage has traditionally been achieved by using insurance contracts. However, the option markets created in the nineties constitute an alternative to the traditional coverage method. The reason is probably very simple: option contracts and insurance and reinsurance operations are conceptually very close to each other:

]]>

Both are hedging operations: options cover agents against unexpected changes in prices, while insurance covers agents against unexpected contingencies (accidents, illness, etc.).

In the light of the above points, if we replicate an insurance operation using option contracts and we demonstrate that the premiums to be paid are equal for both transactions, we can use the option pricing theory to calculate the amount of the premium to be paid for the coverage.

]]> 3.1 Replicating the coverage pattern by using option contracts

Let us now assume that a hypothetical individual is considering taking out a reinsurance contract on highcost illnesses under the terms we have outlined above (financial alternative). We assume that the patient's disease will generate payments three times a year: at moments 1, 2 and 3, and that the accumulated payments exceed the deductible. Figure 1 represents this situation. On the left side of the figure we show the payments the individual must pay out when the insurance operation has not been agreed. On the right side we show the payments when the high-cost disease has been underwritten.

As can be seen, when the risk is insured there is a maximum cost for the individual. In nominal terms, the total cost paid out by the individual will equal the deductible plus the cost of the premium paid to the insurer at the beginning of the year. If the risk has not been insured, the individual must assume the total cost of the treatment, which, in the situation represented in Figure 1, is higher than the cost when he or she is insured.

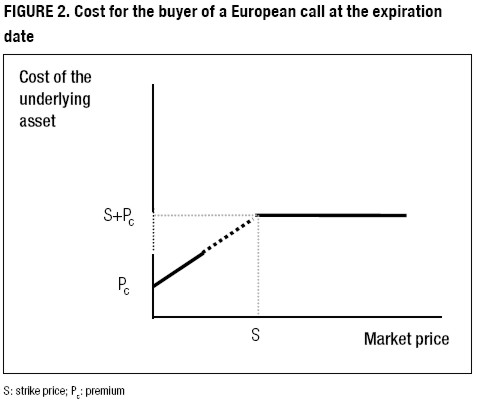

We now show how this coverage pattern can be replicated by an option purchase. In this case, the buyer of a European-style call guarantees a maximum price for buying the underlying asset at the expiration date: if the market price of the underlying asset is lower than the option strike price, the holder will not exercise the right. If he or she wants to buy the underlying asset, the market price must be paid. Furthermore, the cost of the asset bought will be the sum of its market price plus the premium paid when buying the option. On the other hand, if the market price is higher than the strike price, the holder will exercise the right and will pay the writer the strike price for the underlying asset. The total cost paid by the holder will be amount to the sum of the strike price and the premium. Figure 2 shows the cost of the underlying asset for a Europeanstyle option buyer at the expiration date, depending on the market price.

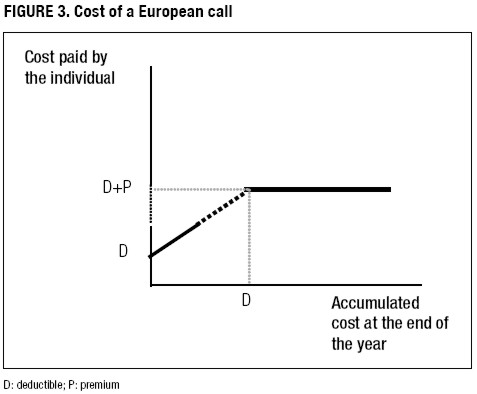

The two hedge schemes (figures 2 and 3) are similar: they guarantee a maximum cost to be paid when an exceptional situation occurs, and for this to be possible, the insured / buyer must pay a premium. Hence, the question raised is whether an insurance operation can be defined in terms of options contracts.

]]>

The essential elements of an option contract are the buyer, the writer, the expiration date, the strike price, the premium and the underlying asset. Let us identify these elements when an individual is insuring against high-cost diseases. Some of these elements can be easily defined: the buyer and the writer will be the individual and the insurance company, respectively, and the strike price will be the deductible. But the key item is the underlying asset.

We define the underlying asset as the accumulated cost of treatment. If we define an expiration date as the end of the year (it must be borne in mind that annual covers are negotiated), and the premium of the option as the amount to be paid to the insurance company, we have all the items we need for an option contract.

We can replicate the coverage pattern of an insurance operation as follows:

Within this pattern, if the accumulated treatment costs at the end of the year (expiration date) are lower than the deductible, the individual will not have exercised his or her right and will have assumed all the payments. The patient's total cost will be the accumulated treatment cost plus the premium paid at the beginning of the year.

In contrast, if the accumulated costs are higher than the deductible, the individual will exercise this option. The individual has the right to "buy" accumulated treatment costs at a price equal to the deductible. As the market price (the actual accumulated cost) is higher than the deductible, the individual will exercise his or her right and "will buy" accumulated treatment cost at the strike price (the deductible). Or, what amounts to the same thing, the insurer will pay the individual the difference between the current accumulated costs (market price) and the deductible[2] (strike price). In this way the individual will only assume the part of the treatment costs that falls below the deductible.

The total cost will be the deductible plus the premium paid by the option. This coverage pattern is shown in Figure 3.

As can be seen, Figures 2 and 3 are essentially equivalent. This means that an individual can achieve the same coverage pattern by signing a reinsurance contract or, alternatively, by buying a call style option.

3.2 Premium equivalence

As shown above, we can replicate a reinsurance coverage pattern by using option contracts. In this section we will demonstrate that the premiums to be paid in both situations must be equivalent. With this aim we test the following hypothesis:

]]> In an equilibrium situation, the premium to be paid for the insurance contract must equal the premium to be paid for the purchase of the call style option. To test this hypothesis, let us assume a time when the price to insure against a high cost disease equals P monetary units (m.u.), whilst the price of buying an option such as those described above equals Pc m.u. Let us assume that:

An arbitrager would operate by working as an insurance company and entering into an agreement with an individual to insure the high-cost disease. The arbitrager would receive P m.u. for this.

At the same time the arbitrager would buy a call for Pc m.u. The profit obtained is the following:

The difference is positive but, what is more important, this profit is achieved without assuming any risk. If, at the expiration date, the accumulated cost does not reach the deductible, the arbitrager would not exercise the call style option, nor would he or she have any obligation with the insured individual. But if the accumulated cost at the end of the year is higher than the deductible, the arbitrager would pay the individual the difference between this cost and the deductible. However, this amount to be paid would be equivalent to that received from the option writer when exercising the call style option bought.

This "profit without risk" opportunity would be perceived immediately by the arbitragers in the market, who would begin to buy calls and to sell insurance contracts. This would produce an increase in the premiums to be paid by calls and a decrease in the premiums to be paid when entering into an insurance contract. These movements would continue until the equilibrium situation is restored.

A symmetric argument can be put forward for the opposite situation when:

]]>In conclusion, in an equilibrium situation premiums must be equivalent. Therefore, we can use the option valuation theory to value the premium of an insurance contract.

3.3 The introduction of the top boundary

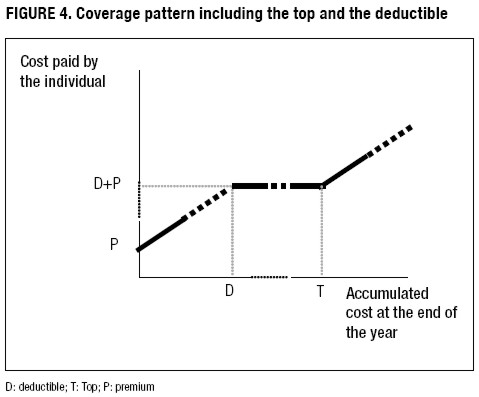

The situation described up to now does not always correspond to the insurance of a high-cost disease. We have only considered the deductible boundary, but, sometimes there is a second boundary: the top boundary. When considering the two boundaries, the coverage pattern provided by the insurance operation can be represented as shown in Figure 4.

In this figure we show the four possible situations for the individual:

We can also replicate this coverage pattern by using option contracts. To do so, we construct an exotic option by combining a call purchase and simultaneous call writing.

Considering the call-put parity, the following relation will occur:

Pc > Pc1

And, therefore, the net premium to be paid by the individual (NP) will be:

Let us see how the coverage works with these options:

Finally, if the cost of the treatment (C) is higher than the top (T),

Both options will be exercised. By exercising the first call the insurer will reimburse the individual the difference between the cost of the treatment and the deductible (D):

where IIND denotes the incomes for the individual.

But the insurer will also exercise the call he or she has bought. By settling this call by differences, the individual will pay the insurer the difference between the cost of the treatment (C) and the top (T):

In summary, the individual will pay the cost of the treatment, the net premium and the difference between the cost and the top, and will receive the difference between the cost of the treatment and the deductible. The net exit of funds for the individual will be determined by:

]]>

EIND = C + NP + (C - T) - (C - D) =

where EIND denotes the cost to be paid by the individual.

The coverage pattern provided by simultaneously using two calls is the same of figure 4 in an equilibrium situation.

To summarise, we have demonstrated that we can replicate the coverage pattern provided by a reinsurance operation using an exotic option, constructed by combining two option contracts. Moreover, we have shown that the premiums to be paid by options and by the reinsurance coverage must be equal. Therefore, we can use option pricing theory to estimate the amount of the premium to be paid by a reinsurance operation.

4. Data and valuation model

For the empirical application of the proposed valuation method, we used the medical bills of an EPS[3] that has been operating in the Colombian Health Care System since January 1999.[4] All figures are expressed in Colombian 2002 pesos[5]. We selected the bills corresponding to the period between October 1999 and September 2002 (over 600,000). In this three-year period, the EPS signed three reinsurance contracts for high-cost diseases. The relevant details of these contracts are shown in Figure 5.

As seen, for example, for the period between October 2001 and September 2002, the EPS entered into an insurance contract with a deductible of $50.000.000 for which it had to pay a monthly premium per affiliate of between $202 and $417.

]]> We divided the analysis period into two sub‑periods:

Within the calculation period, we estimated the cost accumulated over 12 months at September 2000 and at September 2001 for each affiliate. Most of the accumulated accounts were very small. Therefore, we chose for working purposes only those above $8.000.000[6]. Thus, we finally worked with 700 affiliates for the period ending September 2000, and with 1,200 affiliates for the period ending September 2001.

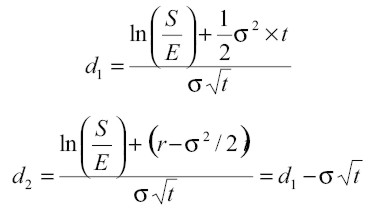

For the valuation of the premium, we used the Black- Scholes (1973) model[7]. The variables needed to apply the model are as follows:

S: the price of the underlying asset. This is defined individually for each EPS affiliate.

E: the strike price, equal to the deductible agreed with the reinsurer.

]]> r: the continuous time interest rate. This is the rate standing at the time the option is valued.t: time to maturity. One year. The reinsurance is underwritten annually and the right to compensation can only be exercised at the end of that period.

σ: volatility of the yield (price variation) of the underlying asset.

Once the values of these variables are known, the premium can be calculated directly with the well-known Black-Scholes model given by the equations:

where the underlying asset does not generate any return.

In addition, the following hypotheses were assumed when applying the model:

]]> 4.1 Volatility estimation

The key variable when valuing these premiums is the volatility of the yield of the underlying asset. As it is not an observable variable, a hypothesis must be assumed in order to estimate volatility from the information available at the moment of the valuation. To achieve this aim, first we constructed a time series for the yield of the underlying asset and then estimated the volatility from this time series.

To construct the time series, we calculated the daily mean value of the medical bills recorded by the EPS for all the days in the calculation period (October 1999 - September 2001). From this information, for the first day of 2000, we calculated the accumulated value of the mean medical bill over the previous 12 months. We repeated this operation for every day between October 2000 and September 2001. In this way we obtained a daily series of accumulated recorded bills over one year.

The next step was to estimate the daily variation of these accumulated values in relative terms. We used the logarithmic approximation and obtained a oneyear time series of daily returns of the underlying asset. This series is shown in Figure 6.

At this point we need to forecast the value of the volatility for the valuation period (October 2000-September 2002) in order to estimate the option premium. With a reduced number of observations, as in this case, perhaps the most suitable alternative is the simplest one: to consider the volatility of the last time period as the best forecast for the next period. However, before assuming this behaviour, we tested the possibility of an autoregressive conditionally heteroscedastic (ARCH) pattern.

We studied both the autocorrelation and partial autocorrelation functions. They do not suggest the existence of an autoregressive or moving average pattern for the daily variation of accumulated medical bills. This was further confirmed by the Ljung‑Box test, the results of which do not allow us to reject the null hypothesis that the variable has no statistically significant autocorrelation (see Figure 7). Once autocorrelation in the series had been ruled out, we tested the existence of autocorrelation when we square the variable. Again, as shown in Figure 7, the Ljung‑Box test rejects the tested null hypothesis, and this indicates that an ARCH pattern is not probable. Moreover, in searching for this pattern, we estimated the Lagrange multiplier test proposed by Engle (1982). The results, shown in Figure 7, definitively reject an autoregressive conditionally heteroscedastic pattern.

Once we have rejected using an ARCH pattern, a possible alternative is to use the realised volatility as a forecast for future values. Hence we estimated the standard deviation for the daily return of accumulated medical bills during the period October 2000 - September 2001. The standard deviation on a daily basis equals 0.0155. However, the relevant value for the deviation is that expressed in annual terms. Multiplying 0.0155 by the square root of the number of days on which bills were recorded gives us a result of 0.239. This is the value corresponding to the standard deviation for the period October 2000 - September 2001, on an annual basis. We use this value as a forecast for the volatility in the validation period, that is, October 2001 - September 2002.

4.2 The estimation of the premium

After determining the volatility, the other parameters of the model must be specifically defined in order to calculate the premium. At this point, the market price of the underlying asset becomes especially important. As we have stated above, we define the underlying asset as the accumulated cost over the previous 12 months. If we estimate a premium for each of the affiliates, there will be as many different prices as there are EPS affiliates. We know the number of affiliates at the moment we value the premium, but not the number of affiliates for the following year. For this reason we assumed one of the aforementioned hypotheses: the distribution of accumulated bills does not change between consecutive periods.

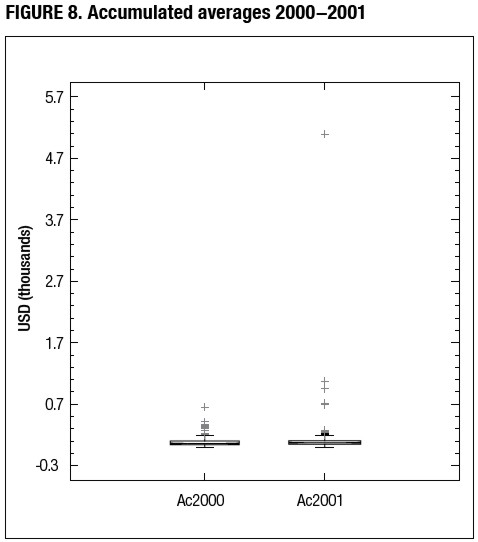

]]> To test this hypothesis at the moment we value the premiums (October 2001), we compare the statistical distribution of the accumulated costs for the two consecutive annual periods where data are available: October 1999 - September 2000 and October 2000 - September 2001. Both distributions are represented in the box graph shown in Figure 8.

As can be seen, there is a high degree of coincidence between the two boxes, which suggests that there are no significant differences between the averages of the two periods. This is supported by the Kolmogorov‑Smirnov test, where the null hypothesis is the equality between the distribution functions for both periods against the alternative hypothesis that assumes that the statistical distribution for the period between October 1999 and September 2000 is different from that for the period October 2000 - September 2001. The value for the Kolmogorov-Smirnov statistic is 0.064, while the critical value for a 99% confidence level is 0.068. This allows us to conclude, with a level of confidence of 99% that the null hypothesis cannot be rejected and we accept that both time periods have the same statistical distribution. In other words, the statistical distribution for the variable studied (the daily return of the accumulated cost) has not changed between two consecutive time periods. We assume this behaviour for the future and therefore we do not expect changes in the statistical distribution between the period October 2000 - September 2001 and the period October 2001 - September 2002 (the latter being the validation period).

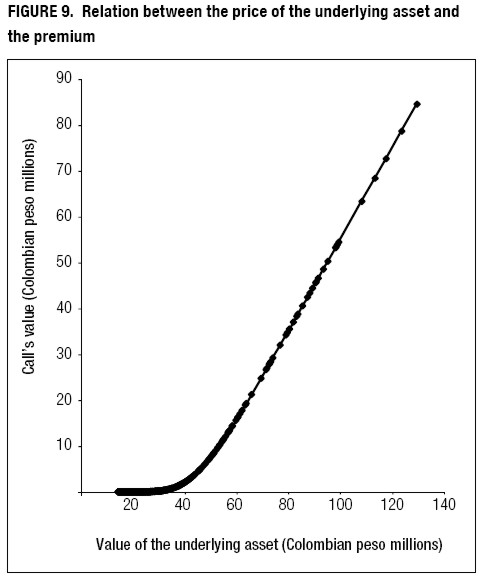

With this assumption we estimate the premium for each of the affiliates, considering its accumulated cost at September 2001. For example, for the affiliate with the highest accumulated cost ($129.184.208) the premium is $84.660.626. We repeated this calculation for each of the 1,200 affiliates considered in September 2001. Figure 9 shows the premium calculated with the market price of the underlying asset (the individual accumulated cost).

]]> 4.3 Comparative analysis between the option premium and the one calculated by actuarial methods

The sum of all premiums for all affiliates with accumulated bills higher than $14.202.442 equals $2.078.754.970[10] and the number of affiliates at the time of valuation was 620,193. Hence, the premium per affiliate would be $3.351,79 for a whole year's coverage. However, this premium is not paid immediately at the beginning of the coverage period, but rather is deferred 12 months and paid in instalments at the beginning of each month. Thus, the former individual figure must be transformed into a 12-month constant pre‑payable rent with an interest rate[11] of 0.01025, the current value of which is $3.351,79; the result means that the EPS should pay a monthly premium per affiliate of $295,25 . At present, the EPS that provided data for this study has underwritten a contract with the reinsurer in which the monthly premium lies within the range between $202 and $417 per affiliate (see Figure 5).

The value estimated by means of the option-pricing theory therefore lies inside the range negotiated with the reinsurer, which was estimated using actuarial techniques.

Nevertheless, the estimation made to present has not taken into account the existence of a $450.000.000 top, above which the EPS pays the excess. This variable is easily introduced into the model. As stated above, this involves the simple design of an exotic option contract that replicates this situation. This would be equivalent to assuming that, when the described call style option (strike price: $50.000.000, one year period, etc.) is bought from the reinsurer, a call is simultaneously sold to the reinsurer with the same features, but at a strike price of $450.000.000.

When both options are negotiated, the coverage situation can be described as follows (see also Figure 4):

For the EPS, selling a call option represents an income or a lower premium to be paid to the reinsurer for the coverage. Therefore, with regard to the call options bought by the EPS, we calculated the amount corresponding to the premiums of the calls sold by this firm. The data used are the same, with the exception of the strike price, which is now $450.000.000. As the top was set at such a high level, with respect to the normal accumulated annual bill, almost all the premiums are lower than $1. We only obtain premiums above $1 for values of the underlying asset above $115.000.000, although the amount is still insignificant. As a consequence, the existence of this top boundary has no significant impact on the valuation of the premiums to be paid by the EPS.

]]> 5. Conclusions

The calculations made show that the Black-Scholes model, used to value options, may also be used to estimate reinsurance premiums of high cost-illness. The premium estimated by this method is not far from the premiums estimated by the actuarial method.

To sum up, as options provide a similar scheme of protection to that of insurance, given that they are both financial tools allowing coverage of certain risks in exchange of a premium, it is reasonable to use option valuation theory in valuing insurance premiums in general and high-cost diseases reinsurance in particular.

In any case, beyond the particular application we have carried out in this paper, the proposed premium valuation method can be extended to other firms and other insuring situations: the variables we have defined can be easily adapted to other situations, and most of the hypotheses we have assumed (e.g. those relative to a unique volatility for all the affiliates) can be substituted by others relevant to each particular situation with no modification to the valuation procedure. It allows the valuation of premiums by using an alternative instrument to the one used by insurance firms, which would help increase competition in negotiations with the Colombian reinsurance market.

In any case, any adaptation to the model requires the availability of enough information. Lack of information is perhaps the main limitation to be found now in applying it to other firms.

Pie de página

[1] There are differences in the criteria about what a treatment precisely includes, ambiguity about the scope of the coverage due to the difficulty of assessing whether a certain event has gone beyond the expected frequency (as it is this excess that is to be reinsured), and so on. Moreover, legal definitions of high cost in health care may include pathologies, syndromes, procedures, surgical operations, services, events and treatments, all of which complicates negotiations between agents over reinsurance contracts and the costs of their claims.

[2] The contract is settled by differences.

[3] The EPS preferred to remain anonymous.

]]> [4] Records prior to this date were not considered reliable.[5] The average exchange rate for that year was $2.507.

[6] For this value, considering the level for the deductible (strike price), the premium would be about 0.

[7] This is a suitable model for valuing European-style options like the one we price in this paper. Nevertheless, other valuation models, i.e. the binomial model, can be used at this point.

[8] This is only a simplifying hypothesis. It is not essential for the method we propose.

[9] Some tests on this hypothesis are calculated below.

[10] Lower values provide premiums below $1.

[11] The nominal Colombian market interest rate, (12.3%) divided by 12.

References

]]>Bhansali, J. D. (1999). Credit derivatives: An analysis of spread options. Derivatives Quarterly, 5(4), 29-35. [ Links ]

Black, F. & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81, 637-59. [ Links ]

Bessembinder, H. & Lemmon, M. L. (2002). Equilibrium pricing and optimal hedging in electricity forward markets. The Journal of Finance, 57(3), 1347-1383. [ Links ]

Chicaíza, L. (2002). El mercado de la salud en Colombia y la problemática del alto costo. Problemas del Desarrollo, 33(131), 163- 187. [ Links ]

Chicaíza, L. & Cabedo, J. (2007). Las opciones financieras como mecanismo para estimar las primas de seguro y reaseguro en el sistema de salud colombiano. Cuadernos de Administración, 20(34), 221-236. [ Links ]

]]>Das, S., Fong, G. & Geng, G. (2001). Impact of correlated default risk on credit portfolios. The Journal of Fixed Income, 11(3), 9-19. [ Links ]

Demeterf, I. K., Derman, E., Kamal, M. & Zou, J. (1999). A guide to volatility and variance swaps. Journal of Derivatives, 6(4), 9-32. [ Links ]

Duffee, G. & Zhou, C. (2001). Credit derivatives in banking: Useful tools for managing risk? Journal of Monetary Economics, 48(1), 25- 54. [ Links ]

Engle, R. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of UK inflation. Econometrica, 50(4), 897-1007. [ Links ]

Geczy, C., Minton, B. & Schrand, C. (1997). Why firms use currency derivatives. Journal of Finance, 52(4), 1323-1354. [ Links ]

]]>Harrington, S. E. (1997). Insurance derivatives, tax policy, and the future of the insurance industry. Journal of Risk and Insurance, 64(4), 719-726. [ Links ]

Karpinsky, A. (1998). The risky business of risk management derivatives disasters revisited. Australian Banker, 112(2), 60-63. [ Links ]

Mcclintock, B. (1996). International financial instability and the financial derivatives market. Journal of Economic Issues, 30(1), 13-34. [ Links ]

Niehause, G. (2002). The allocation of catastrophe risk. Journal of Banking and Finance, 26(2 & 3), 585-596. [ Links ]

Pouget, S. (2001). Finance de marché expérimentale: une revue de littérature, Finance. Revue de l'Association Française de Finance, 22(1), 37-63. [ Links ]

]]>Yanxiang, G. A. (2002). Valuing the option to purchase an asset at a proportional discount. Journal of Financial Research, 25(1), 99-109. [ Links ]

Zettl, M. (2002). Valuing exploration and production projects by means of option pricing theory. International Journal of Production Economics, 78(1), 109-116. [ Links ]

]]>