These five items explain that in many cases, financial statements certified as IFRS turn out not to be so, because in most corporate collapses unqualified financial statements have been signed. The same arguments are repeated by Saudagaran (2004) who states that high quality accounting systems produce comparable, reliable and relevant information to decision makers. Agrawal (2008) argues that IFRS will impact corporate governance as it (IFRS) involves an extensive use of judgment in the selection of appropriate accounting policies and alternative treatments at the time of adoption. Also, IFRS requires valuations and future forecasts, which will involve the use of estimates, assumptions and management judgment. It has been observed that the combination of all these factors can have a significant impact on an enterprise's reported earnings and financial position. In this way, boards and audit committee must be prepared to understand and play this role effectively. According to Agrawal (2008), investors, analysts and stakeholders may view earnings restatements negatively if the five items above are not taken into consideration.

There are numerous IFRS proponents who support the view that global financial reporting has positive effects on the functioning of global markets since standard and quality information will be available to users - including investors. In addition to this, it has been noted that global firms incur huge costs when preparing, auditing and interpreting information prepared using different accounting standards in different countries. Consequently, IFRS proponents such as the IASB (previously IASC), the International Organization for Securities commission organization (I) and Barth et al. (2008) among others argue that the adoption of IFRS will contribute towards a reduction in the cost of capital.

Although, there are calls for the universal adoption of IFRS including IASB, there is still considerable debate as to whether the adoption of IFRS is beneficial (Barth, Landsman & Lang, 2008, p. 1161 and Christensen, Lee & Walker 2008, p. 8). In this regard, consensus is yet to be reached on issues relating to improved accounting quality, reduced cost of capital, transparency and capital market effects.

Governance and IFRS Challenges in Africa and positive actions

Okeahalam and Akinboade (2003, p. 11) mention six items that constitute problems in Africa: Transition economies, a large number of state owned enterprises, a culture of corruption, a weak business environment and low financial intermediation all of which create extreme challenges. Many African economies started as socialist economies and over time have transitioned or are in the process of transitioning to capitalist economies involving privatization of enterprise and a reduction of government control. Some of these processes have involved massive corruption threatening many lives in their economies. Zambia is a leading example of this where privatization of the mines has created more problems that it has solved.

In light of the growing recognition of the importance of Corporate Governance and Financial Reporting Standards, African states have embarked on initiatives to facilitate IFRS adoption such as the newly launched Pan African Federation of Accountants (PAFA) in 2011 and the Francophone Chartered Accountants int'l Federation (FIDEF). In this regard, positive country level steps have been seen in Lesotho, Mauritius, Zambia, Kenya, Tanzania, Uganda, Ghana and the West African Monetary Economic Monetary Union (WAEMU) (8 countries). In spite of these efforts, challenges such as adherence issues (Uganda), conflicts with national law (South Africa), enforcement mechanisms (Kenya and Mauritius), implementation guidelines (Tanzania), non-compliant accounting systems and software (WAEMU, CEMAC, OHADA/SYCOA) need to be addressed. CEMAC is the French acronym for the Economic Community for Central African States comprising Cameroon, Central African Republic, Chad, Equatorial Guinea, Republic of the Congo and Gabon. OHADA is a system of business laws and institutional implementations adopted by sixteen West and Central African nations. It is the French acronym for "Organization pour l'Harmonisation en Afrique du Droit des Affaires", which translates into English as "Organization for the Harmonization of Business Law in Africa”.

It can therefore be said that IFRS acceptances has gained momentum and has had an impact on Africa, although a lot still needs to be done on the observance of standards and codes according to various World Bank reports.

Other initiatives in Africa towards the adoption and implementation of good corporate governance include the Africa Peer Review mechanism (APRM), an initiative under which 26 African leaders agreed to submit their countries and themselves to a peer review on selected areas of governance under the New Economic Partnership for African Development (NEPAD). NEPAD is a programme of the African Union (AU) adopted in Lusaka, Zambia in 2001. NEPAD is a radically new intervention, spearheaded by African leaders to pursue new priorities and approaches to the political and socio-economic transformation of Africa. NEPAD's objective is to enhance Africa's growth, development and participation in the global economy.

This initiative is similar to those promoted by regional bodies in other parts of the world. Montgomery (2007) cites results from 25 meetings of roundtables sponsored by the OECD in which 6 factors emerged as challenges. These included enforcement, ownership and control, shareholder rights and equitable treatment, responsibilities of the board, transparency and disclosure as well as the role of stakeholders. This list is very similar to the contents of many corporate governance codes. CACG (2006, pp.76-79) concurs with Montgomery but expands the list to include concentrated ownership structures, ineffective regulatory and judiciary systems, underdeveloped institutional capacities, limited underutilized human capital skills and capabilities, preponderance of small/fragmented economies, corrupt complex bureaucracies, expensive financing, heavy foreign debt and insignificant capital market. CACG's list is significant for emerging economies in Africa because 25 out of 40 highly indebted countries are in Africa, and 22 out of the 30 least literate countries are in Africa. The continent is also bedeviled by limited access to the Internet, phone, electricity and safe water. The CACG report makes an interesting observation that Africa constitutes only 1.8% of international trade and all these factors continue to complicate the governance situation in Africa.

]]>Governance and IFRS Lessons: Global comparative analysis

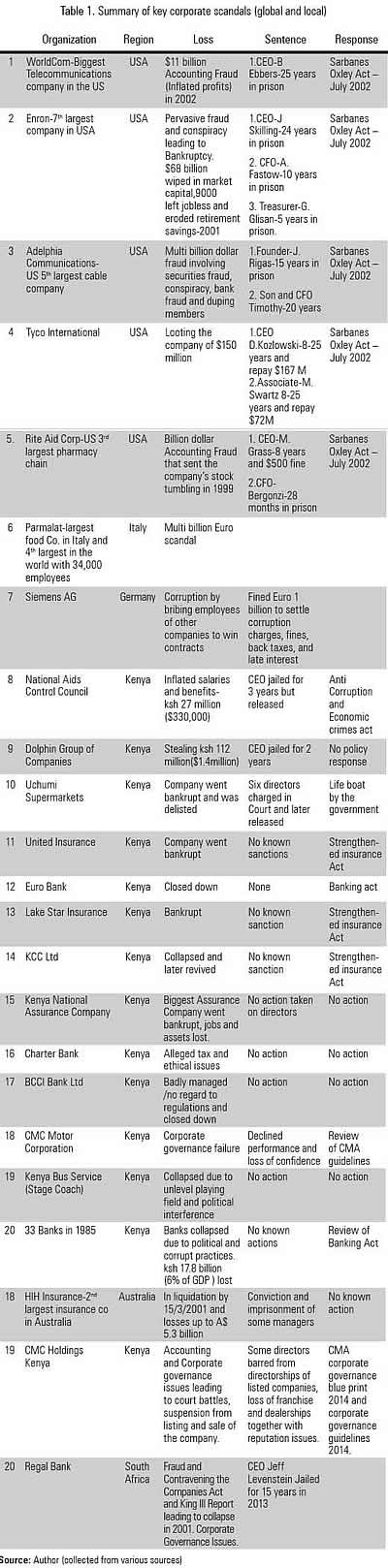

Lessons from around the world on the magnitude of losses and their impact on society do prove the need to ensure no more governance lapses. While the list depicts direct losses, others including the reputation of the firms involved shouldn't be overlooked. Some of the reasons cited for these failures include lapses in auditing, hiding loans or losses, insider trading and inflated revenue. The New York Times on 16/6/2002 listed top institutions including Arthur Andersen, Delloite & Touché, Ernst and Young, KPMG and PWC alongside other corporations. This section summarizes some of the consequences of corporate failures and scandals both in and outside Africa (See Table 1).

Enhancing Transparency and Accountability (ROSC reports)

According to NIFA, enhancing transparency and accountability is critical to achieving World Economic stability and minimizing the impact of global economic crisis. Countries can achieve this through compliance with the International Accounting Standards (IFRS) issued by the International Accounting Standards Board (IASB) and the International Standards on Auditing (ISA) issued by the International Federation of Accountants (IFAC). Findings on country code compliance with standards are reported by World Bank observer teams known as Report on Standards and Observation of Codes (ROSC) and the Financial Standards Compliance Index.

ROSC Compliance

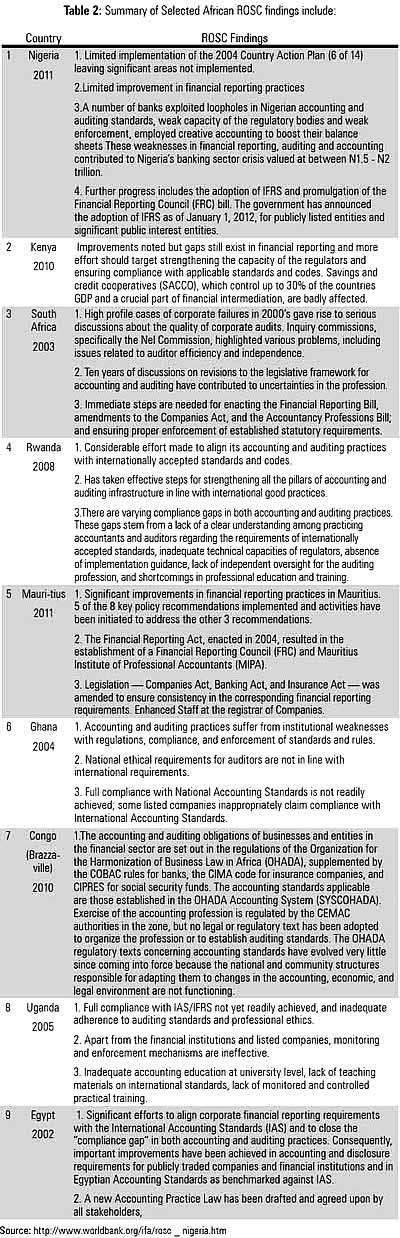

The World Bank's Reports on the Observance of Standards and Codes (ROSC) targeting its member countries on the implementation of international accounting and auditing standards for strengthening the financial reporting regime (World Bank, 2010) has been an indicator of compliance. The general findings of this program over the past decade continuously show that gaps still exist between domestic and international standards and that these gaps need to be closed so the financial reports generated are of high quality (Transparent, relevant, reliable and comparable) (See Table 2).

]]>

It can be seen that throughout Africa, weak capacity of regulatory bodies, weak monitoring and enforcement, lack of independent oversight of the auditing profession and general institutional weaknesses cut across the continent weakening financial reporting and attendant investor confidence.

Financial Standards Compliance Index

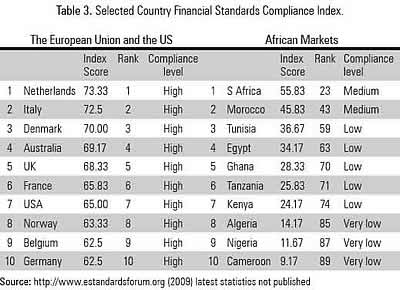

It is widely recognized that global financial stability rests on robust national systems, and therefore requires enhanced measures at the country level. (ROSC Uganda 2008, p.1). In a world of integrated capital markets, financial crises in individual countries can imperil international financial stability. This provides a basic “public goods” rationale for minimum standards, which benefit international and individual national systems. In this context, the World Bank and the International Monetary Fund (IMF) initiated the Reports on the Observance of Standards and Codes (ROSC), which cover twelve internationally recognized core standards and codes relevant to economic stability and private and financial sector development. The Financial Standards Compliance Index is made up of 12 key standards covering macroeconomic policy and data transparency, institutional market infrastructure and financial regulation and supervision. Africa has not fared well on these standards as can be seen in the table below. It can be seen that only two countries in Africa achieved a medium score while the other eight score 'low' and 'very low'. Since this data relates to some of the top economies in Africa, it can be argued that the financial standards compliance index is quite low meaning the 12 indicators above have not been sufficiently complied with. This is in total contrast to the EU and the US where the compliance index is considered high (See Table 3).

Strengthening Domestic Financial Systems (corporate governance)

Under NIFA, the principles and policies that foster the development of stable, efficient financial systems include corporate governance. The findings of this study are based on the implementation status of corporate governance codes that indicate material items to be reported upon. Most codes expect that a report on good corporate governance should ensure timely and accurate disclosures of all material information regarding the corporation to stakeholders. Generally and around the world, the key contents of corporate governance codes include compliance with guidelines on corporate governance codes and reasons for non compliance, establishment of board and board committees, supply and disclosure of information, election of directors, resignation of directors, AGM's, a balanced board, best practices relating to the rights of shareholders and an effective audit committee. It is however noted that good corporate governance may not survive in a place where country governance is still questionable. Governance in African countries has in many instances not measured up to many global standards and this has contributed to poor corporate governance. Some African countries have been under military rule or non-democratic civilian governments (Zimbabwe) and this has not helped corporate governance either (See Table 4).

This study has analyzed two cases in Africa's two largest economies shown in appendixes 3 and 4. Ned Bank South Africa is a strong Africa focused bank whose strategy is currently under threat following an alliance with Eco bank that trades on three West Africa exchanges. The study depicts possible loss and harm to the relationship where the reputation of one partner is questionable and disclosure is being avoided. The Cadbury Nigeria Case is a near Enron style case where compliance with regulation and falsifying financial statements characterized a scandal in a multinational listed on the Lagos Securities Exchange. Penalties and damages were incurred directly and indirectly.

Discussion of Findings and Recommendations

From ROSC reports on financial standards compliance and corporate governance, it appears that there is still more to be done. While it has been seen that a foundation has been laid, the impact of governance measured in wealth creation has not been felt in many parts of Africa. The Nigeria ROSC report for 2011 paints a grim picture showing that most recommendations have not been adopted and this has led to a financial crisis in that country. While the annual reports of many companies in Africa have indicated increased attention to governance reporting it is many people's opinion that the reports are not sufficient evidence of governance compliance. Many reports show board responsibilities and don't indicate any separation between the roles of the Chair, the CEO and management. Many conflicts of interest exist and no mechanisms for dealing with them. Directors resign often but no reasons are given and where professional advice is necessary, there is no evidence on how it is obtained. The development of ethical behavior in most institutions isn't clear as code of conduct executions lack clarity. Many companies in Africa do not indicate the corporate governance codes they have applied and many countries have not clearly spelt out how this should be done and the consequences.

Some suggestions border on the fact that some regulators and governments think that codes and standards may not be suitable for Africa. Singh and Newberry (2008, p. 484) suggest that those seeking IFRS for developing countries may need to devise an acceptable solution and obtain inside access to the standard-setting process to achieve this aim. However, this is unlikely to happen in emerging economies because they seem to be consumers of IFRS and are not part of the creation process.

Other recommendations on good corporate governance challenge the effectiveness of the audit committees responsible for overseeing the work of the auditors and independently review the workings of the organization. According to The Accountant (2006), the Enron audit committee carried out its duty in a cursory manner with some members missing meetings up to 75% of the time. In the case of HIH (Lipton, 2003) insurance in Australia, their terms of reference and minutes indicated they were only concerned with the accounts and the figures and never focused on risk management or internal controls with the meetings attended by everyone including the executive directors thus leading to a failure to attend to the risks faced by the company and a serious conflict of interest. Coffee (2005) suggests that any difficulty in achieving auditor independence in a corporation with a controlling shareholder may also imply that minority shareholders in concentrated ownership economies should directly select their own gatekeepers - a suggestion that can be complex to implement.

The Accountant (2006) argues that failure to grasp the concept of conflict of interest can also lead to serious flaws. In the case of CMC Motors Group in Kenya, the annual governance report clearly indicated there was no conflict of interest, but events within the company did show that the directors and the chairman had been doing business with the company leading to serious conflicts of interest among many other issues.

In line with the above, Bruner (2011, p. 319) argues that governance codes such as the new code proposed by the Financial Reporting Council (FRC) in the UK, will enhance the quality of engagement between institutional investors and companies and accommodate the seven principles included in the code. Unsurprisingly, the principles are not new; they simply reflect what appears in several suggestions. These principles include (1) disclosure of investor stewardship policies; (2) adoption of a robust policy for managing conflicts of interest; (3) active monitoring of all related companies; (4) adoption of clear guidelines on when and how to escalate activities as a method of protecting and enhancing shareholder value; (5) willingness to act collectively with other investors where appropriate; (6) adoption of voting policies; and (7) periodic reporting on stewardship and voting activities.

]]> Conclusions

This study has applied a literature review to assess the continent's response to NIFA suggestions regarding economic stability. The review looked at transparency and accountability as well as the strengthening of domestic markets. The findings include weak regulatory bodies, weak monitoring and enforcement, lack of independent oversight of the auditing profession and general institutional weaknesses with improvements over the years. World Bank ROSC reports also indicated lapses in IFRS implementation. Compliance with NIFA is therefore still low and guidelines are not fully followed. This is made manifested by recurrent financial crises, courtroom battles, suspensions and stock market delisting as well as challenges to reputations, some of which have trickledown effects for the economic development of the countries, with Nigeria being a case in point. It is therefore concluded that NIFA compliance is still low and ongoing efforts are still necessary for improving Africa's corporate governance and IFRS mechanisms so that wealth creation and resource management can trickle down to the wider population and reduce discontent among the population.

Future research could dwell on corporate governance and IFRS and state owned enterprises, corporate governance mechanisms, corporate governance and impact on poverty alleviation, enforcement of appropriate codes and relationship between corporate governance and country governance indicators.

Acknowledgements

Thanks to very insightful comments at Catholic University of Eastern Africa-Nairobi where this paper was first presented.

References

Agrawal, N. (2008). The Impact of IFRS on corporate governance. Live Mint. Retrieved from http://www.livemint.com/Politics/jQgcH4GFaiM3aNzAGERIkL/The-impact-of-IFRS-on-corporate-governance.html [ Links ]

Ashbaugh-Skaife, H., Collins, D. W. & LaFond, R. (2006). The effects of corporate governance on firms' credit ratings. Journal of Accounting and Economics, 42(1-2), 203-243. doi: http://dx.doi.org/10.1016/j.jacceco.2006.02.003 [ Links ]

ASX Corporate Governance Council., & Australian Stock Exchange. (2003). Principles of good corporate governance and best practice recommendations. Sydney: Australian Stock Exchange Ltd. [ Links ]

Bank for International Settlements. (1998). Report on the international Financial Architecture on work groups. Bank for International Settlements. Retrieved from: http://www.bis.org/publ/othp01.htm [ Links ]

Barth, M. E., Landsman, W. R., & Lang, M. H. (2008). International Accounting Standards and Accounting Quality. Journal of Accounting Research, 46(3), 467-498. doi:10.1111/j.1475-679X.2008.00287.x [ Links ]

Brown, L. & Caylor, M. (2004). Corporate Governance and Firm Performance. Georgia: Available at SSRN. doi: http://dx.doi.org/10.2139/ssrn.586423 [ Links ]

Bruner, C. (2011). Corporate Governance Reform in a Time of Crisis. Journal of Corporation Law, 36(2), 309-341. [ Links ]

Centre for Corporate Governance (CCG). (2006). Training Course for Directors. Handbook. Nairobi, Kenya. [ Links ]

Christensen, H, Lee, E. & Walker, M. (2008). Incentives or Standards: What Determines Accounting Quality Changes Around IFRS Adoption? In AAA 2008 Financial Accounting and Reporting Section (FARS) Paper.Minneapolis: SSNR. doi: http://dx.doi.org/10.2139/ssrn.1013054 [ Links ]

Coffee, J. (2005). A Theory of Corporate Scandals: Why the U.S. and Europe Differ'. Columbia Law and Economics Working Paper No. 274 Available at SSRN. doi: http://dx.doi.org/10.2139/ssrn.694581 [ Links ]

Economic Commission for Africa. (2002).Guidelines for Enhancing Good Economic and Corporate Governance in Africa. New York: Economic Commission for Africa. http://repository.uneca.org/bitstream/handle/10855/5544/Bib-39457.pdf?sequence=1 [ Links ]

Fama, E. F. (1980). Agency Problems and the Theory of the Firm. Journal of Political Economy, 88(2), 288-307. Retrieved from: http://www.jstor.org/stable/1837292 [ Links ]

IAS Plus. (2010). Background to International Financial Reporting Standards. Retrieved from: http://www.iasplus.com/en/resources/ifrsf/due-process/background-to-ifrs [ Links ]

Iliev, P. (2010). The Effect of SOX Section 404: Costs, Earnings Quality, and Stock Prices. The Journal of Finance, 65(3), 1163-1196. doi:10.1111/j.1540-6261.2010.01564.x [ Links ]

Leblanc, R. & Gillies, J. (2003). The Coming Revolution in Corporate Governance. Ivey Business Journal 68, 1-11. Retrieved from: http://iveybusinessjournal.com/topics/governance/the-coming-revolution-in-corporate-governance#.VGOLFjSG9qk [ Links ]

Leke, A, Lund, S, Roxburgh, Ch., & van Wamelen, A. (2010).What's driving Africa's growth? Insights & Publications (McKinsey & Company). Retrieved from:http://www.mckinsey.com/insights/economic_studies/whats_driving_africas_growth [ Links ]

Lipton, P. (2003). 'The Demise of HIH: Corporate Governance lessons'. Keeping Good Companies, 55(5), 273-277. [ Links ]

Mckinseys & Company (2002).Global investor Opinion Survey: Key findings. Retrieved from: http://www.eiod.org/uploads/Publications/Pdf/II-Rp-4-1.pdf [ Links ]

Montgomery, S. (2007). 'Corporate Governance in Developing Countries: Shortcomings, Challenges & Impact on Credit'. Congress to celebrate the fortieth annual session of UNCITRAL, Vienna 9-12 July 2007. Retrieved from: http://www.uncitral.org/pdf/english/congress/Cooper_S_rev.pdf [ Links ]

OECD. (2009). Principles of Corporate Governance. Paris: OECD. Retrieved from: http://www.oecd.org/corporate/ca/corporategovernanceprinciples/31557724.pdf [ Links ]

Okeahalam, C. & Akinboade, O. (2003).A Review of Corporate Governance in Africa: Literature, Issues and Challenges Paper. Global [ Links ]

Corporate Governance Forum, 15 June 2003. Retrieved from: http://www.researchgate.net/publication/237256378_A_Review_of_Corporate_Governance_in_Africa_Literature_Issues_and_Challenges [ Links ]

Ramalho, A. (2013). African Corporate Growth Depends on Corporate Governance. Institute of Directors in Southern Africa (IoDSA). Retrieved from: http://www.iodsa.co.za/news/129222/African-Corporate-Growth-Depends-on-Corporate-Governance.htm [ Links ]

Reilly, D. (2006). 'Sarbanes-Oxley Changes Take Root'. The wall street Journal, March 3. Retrieved from: http://online.wsj.com/articles/SB114135577334088374 [ Links ]

Robinson, T. & Munter, P. (2004). Financial Reporting Quality: Red Flags and Accounting Warning Signs. Commercial Lending Review. , 1-15Retrieved from: http://www.tsi-thailand.org/images/stories/TSI2012_Professional/Download/CISA2_FinancialReportingQuality.pdf [ Links ]

]]>ROSC Uganda (2008). Report on the observance of Standards and Codes (ROSC) on Uganda Accounting and Auditing Standards. Retrieved from: http://www.worldbank.org/ifa/rosc_aa_uga.pdf [ Links ]

Shleifer, A., & Vishny, R. W. (1997). A Survey of Corporate Governance. The Journal of Finance, 52(2), 737-783. doi:10.1111/j.1540-6261.1997.tb04820.x [ Links ]

Singh, R. & Newberry, S. (2008). Corporate Governance and International Financial Reporting standard (IFRS): The Case of Developing Countries. Research in Accounting in Emerging Economies, 8, 483-518. [ Links ]

Soederberg, S. (2002). The contradictions of the New International Financial Architecture: another procrustean bed for emerging markets? Third World Quarterly, 23(4), 607-620. Retrieved from: http://www.jstor.org/stable/3993478 [ Links ]

Stanwick, P. (2008). Corporate Governance in the 21st Century: Do We Need Global Standards? Queens University Belfast conference 7-9 September 2008. Retrieved from: http://wwwcrrconference.org [ Links ]

Tan, W. & Tan, M. (2004). The Impact of Corporate Governance on Value Creation in Entrepreneurial Firms. Singapore: Singapore Management University Library. Rencontres de St-gall 2004 (2004).Available at: http://works.bepress.com/weeliang_tan/7 [ Links ]

The Accountant (2006). Applied Corporate Governance: Lessons from Corporate Failures. Nairobi: Journal of the institute of Certified Public Accountants of Kenya, 13-14. [ Links ]

World Bank (2005). 'T O O L K I T 2 Developing Corporate Governance Codes of Best Practice users guide'. Washington, USA: The World Bank and IFC. Retrieved from: http://www.gcgf.org/wps/wcm/connect [ Links ]

World Bank (2010). Report on the observance of Standards and Codes (ROSC) on Kenya Accounting and Auditing Standards. World Bank Group. Retrieved from: http://www.worldbank.org/ifa/rosc_aa.html [ Links ]

Appendixes

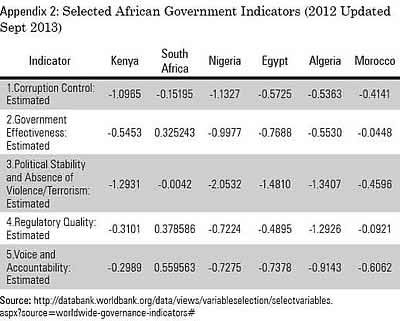

-2.5 Weakest and 2.5 Strongest

The Worldwide Governance Indicators (WGI) are a research dataset summarizing the views on the quality of governance provided by a large number of enterprise, citizen and expert survey respondents in industrial and developing countries. This data is gathered from a number of survey institutes, think tanks, non-governmental organizations, international organizations, and private sector firms.

- Reflects perceptions of the extent to which public power is exercised for private gain, including both petty and grand forms of corruption, as well as "capture" of the state by elites and private interests.

- Reflects perceptions of the quality of public services, the quality of the civil service and its degree of independence from political pressures, the policy formulation and implementation quality, and the credibility of the government's commitment to such policies.

- Reflects perceptions of the likelihood that the government will be destabilized or overthrown by unconstitutional or violent means, including politically motivated violence and terrorism.

- Reflects perceptions of the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development. ]]> Reflects perceptions of the extent to which a country's citizens are able to participate in selecting their government, as well as freedom of expression, freedom of association, and a free media.

Appendix 3: NED Bank South Africa and Eco Bank Nigeria 2013

Ned bank South Africa traces its roots back to 1831 in Amsterdam but is now a South African bank with an African focus and at the end of 2012 it had a market capitalization of US $9 billion. Its asset base then was US $80.5 billion with 28,000 employees and it was listed on the Johannesburg Security Exchange (JSE). It resisted an HSBC buyout in 2010 but deepened its strategic alliance with Eco Bank, which operates in 36 African states and is traded on the Ghana, Nigeria and Ivory Coast Security Exchanges. The alliance was to provide facilities to support Eco Bank's corporate development programs including its transformational banking acquisition in Nigeria and in so doing secured the right to acquire up to 20% of Eco Bank Transnational Inc. It loaned Eco Bank $285m to help it acquire Nigeria Oceanic Bank and in the West African press, Eco Bank claimed it had a similar right to subscribe to 20% of Ned Bank under an unclear arrangement. The Ned Bank press statement did not mention these reciprocal arrangements which were in perpetuity.

These arrangements required shareholder approval from both sides given the significant dilution it would have for Ned Bank and neither bank included this in their annual report in spite of their significance.

While no court cases have been filed nor has impropriety been found, an analyst's presentation indicated that the 2.478 million new shares to be acquired with the $285 million loan would convert to 11.5 us cents per share whereas the shares were trading at 9c in Lagos and would only represent a 12.6% share of the company. To acquire the full 20%, Ned Bank would have to buy the additional shares at market rates resulting in an additional $164 million on top of the loan.

In the course of the year allegations of fraud by the chairman and CEO of Eco Bank of writing off debts to a company owned by the chairman and selling assets on the cheap to related parties appeared and these investigations are ongoing by Nigerian regulators. It also surfaced that Oceanic Bank, the purchase which was financed by Ned Bank collapsed in 2008 under Nigeria Central Bank management under claims of fraud. Two South African Companies, Ethos Private Equity and Old Mutual Private Equity lost fortunes in the bank. The matters got even more clouded as the Public Investment Corporation of South Africa, which holds 6.5% of Ned bank and whose operations include acquiring African assets, is also a major shareholder of Eco Bank.

The issue that is a concern in South Africa is lack of progress in the regulator's investigation of the alleged Eco Bank transactions with its related parties which are thought to be lacking in corporate governance and a possible early warning sign. The outcome of these investigations will shed light on the options available to Ned Bank as it is believed it could suffer potential losses but, worse still, the question of why such a transaction exists if there are questions regarding the leadership reputation of the entities involved. Even though both banks are giants and their stocks are trading, these disclosure failures are worrying, may have serious implications and have obviously put a check on Ned Bank's Pan African strategy.

- Corporate Governance scandal threatens Ned bank's Africa Strategy. ]]>

http://www.bdlive.co.za/opinion/columnists/2013/10/21/corporate-governance-scandal-threatens-nedbanks-africa-strategy . Stuart Theobald, 21 October 2013, 07:37

Appendix 4: Cadbury Nigeria PLC 2006 - Overstatement in Financial Statements

Cadbury Nigeria was founded in 1965 as a subsidiary of Cadbury Schweppes, a major global player in confectionery and beverages markets with operations in 200 countries and 40,000 employees. Cadbury Nigeria engages in the manufacture and sale of sugar confectionery, gum and food beverages in two segments. It owns the Stanmark Cocoa Processing Company.

In October 2006, the board of Cadbury Nigeria PLC notified the world, including its stockholders and regulatory bodies, that it had discovered "Overstatements" in its accounts, which, in its words, had spanned many years. It quickly appointed Price WaterHouseCoopers, an independent auditing firm to investigate these "Overstatements," and they submitted a report that the overstatement could be around 13-15 billion naira ($90 million) leading to a provision for a 15 million pounds goodwill impairment from the transaction. The overstatement was first detected after due diligence performed by Cadbury UK when increasing its acquisition from 46 to 50%. Analysts and reports from Nigeria indicated several lapses.

Sales and stock buybacks were reported including false stock certifications. Overstatement of profits, misrepresentation of sales and false supplier certificates characterized the financial statements. In 2006, the year of the scandal, the company recorded a loss of $15 million with more expected, and share prices dropped 5-26%. Offshore compensation of certain senior employees was detected and this had not been authorized by the compensation committee as required by policy.

Other analysts and members of the Nigerian institute of Directors pointed at serious governance issues including a failure of board oversight functions. The CFO and CEO exercised delegated powers and after the US Enron debacle, directors learned and were expected to pay close attention to the affairs of the company. Even more interestingly, the audit committee was made up of 3 executive directors, contrary to the code of practice. Internal control and organization, integrity, audit committee, external auditors and the entire management were cited as having been problematic because of their failure to comply and detect the irregularities that led to this overstatement. Questions were raised regarding whistle blowing and why it didn't work. Why didn't the banks scrutinize the financial statements before lending any money?

Lastly, the Union Registrars, the filing company for Cadbury Nigeria with the duty to report to the SEC any actual or suspected breach, infringement or non-compliance with any SEC rules and regulations in the Nigerian code of corporate governance failed. However, the Union Registrars did not pay dividends and failed to notify SEC in writing as required when Cadbury Nigeria failed to transfer dividend payments to shareholders within 7 business days.

What was the damage? A scandal of this magnitude is always very expensive. The CFO, CEO and all the officials that presided over this company were disqualified from operating in the Nigerian Capital Market thus denting many people's careers. The Company suffered heavy penalties and their shares listing was suspended while the registrar and the auditors received penalties for their roles. The loss of share value from a loss of public confidence, the damage to the Cadbury brand, the reputation of the external auditor associated with the big 4 and the 300 shareholders suing the company for breach of duty all complicated the matter.

]]> 1. Corporate Governance Issues in Financial Reporting-The Cadbury Challenge http://www.nigeriavillagesquare.com/articles/oladele-o-solanke/corporate-governance-issues-in-financial-reporting-the-cadbury-challenge.html2. An evaluation of the limitations of the corporate governance codes in preventing corporate collapses in Nigeria. http://iosrjournals.org/iosr-jbm/papers/Vol7-issue2/P072110118.pdf